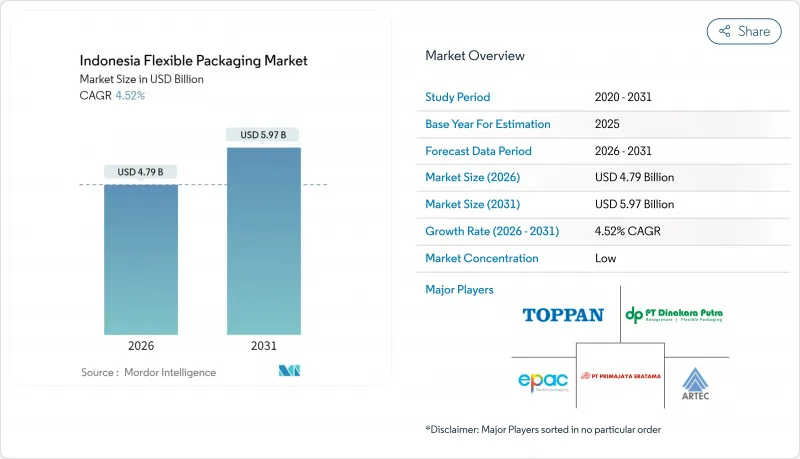

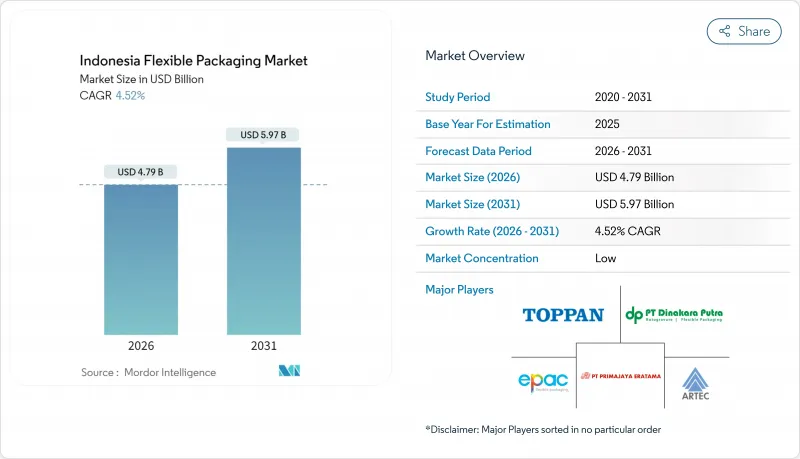

인도네시아의 연포장 시장은 2025년 45억 8,000만 달러로 평가되었으며, 2026년 47억 9,000만 달러에서 2031년까지 59억 7,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)에 있어서 CAGR은 4.52%를 나타낼 것으로 전망되고 있습니다.

이 성장 궤적은 동남아시아 최대의 경제 규모를 자랑하는 인도네시아의 입장을 반영하고 있으며 도시화가 진행되는 인구가 포장 식품과 온라인 소매로 꾸준히 이행하고 있는 것이 배경에 있습니다. 모두 연포장 형식에 대한 의존도가 높은 분야입니다. 소분포 포장에 대한 수요 증가, 지속적인 전자상거래 활동, 기업의 지속가능성에 대한 대처가 함께 인도네시아의 연포장 시장에 유리한 소재, 제품, 기술의 변화를 뒷받침하고 있습니다. 중국을 중심으로 한 수입 완성품은 국내 컨버터에 있어서 여전히 비용상의 과제가 되고 있습니다. 그러나 2025년에 시행 예정인 확대생산자책임(EPR)규제에 의해 현지재생원료 수요가속이 전망되고 있습니다. 경쟁 대응책은 현재 수직 통합, 배리어 필름 혁신, 디지털 인쇄 능력에 초점을 맞추고 있으며, 이들은 인도네시아의 2,550만 사에 이르는 디지털 대응 중소기업을 위한 소량 생산을 가능하게 하는 것입니다.

포장 식품은 2024년 국내총생산(GDP)의 6.47%를 차지했고 인도네시아 식품음료기업협회는 도시 가구가 조리된 식품과 고급 스낵을 선호하는 경향에서 이 비율이 더욱 상승할 것으로 예측했습니다. 2024년 10월에 도입된 의무적인 할랄 표시에는 명확하고 내구성이 있는 인쇄가 요구되어, 인도네시아의 습윤한 다도 섬형 공급망에 있어서 제품의 품질을 유지하는 고배리어성 다층 필름에 대한 수요가 높아지고 있습니다. 수입된 특수식품과 가처분소득 증가도 고급 보호구조에 대한 수요를 더욱 뒷받침하고 있습니다. 이러한 배경에서 첨단 산소 및 습기 장벽 필름을 제공하는 컨버터는 유제품, 고기 제품, 과자 가공업자로부터의 수주를 확대하고 있습니다. 인도네시아의 연포장 시장은 이러한 꾸준한 수량 성장과 진열에 적합한 스탠드업 파우치를 선호하는 현대 유통 채널로의 전환으로부터 직접적인 혜택을 누리고 있습니다.

2025년에 시행된 EPR 규제에서는 생산자가 2029년까지 소비 후 플라스틱 폐기물을 30% 삭감할 의무가 있으며, 재활용 가능한 단일 소재 필름과 인증된 퇴비화 가능 소재에 대한 투자가 촉진되고 있습니다. 현지 스타트업의 Greenhope사와 Biopac사는 PHA(폴리하이드록시알칸산) 및 전분 베이스의 필름의 양산화를 진행하고 있어 한편, 다논·인도네시아 등의 다국적 기업은 이미 페트병에 25%의 리사이클 소재를 사용하고 있어 식품그레이드의 재생 폴리에스테르(rPET) 수요 증가 환경 배려를 어필하고 싶은 브랜드는 배리어 성능을 유지하면서 폐기 처리를 간소화하는 대체 기재를 지정하는 경향이 있습니다. 이 때문에 인도네시아의 연포장 시장에서는 아시아 및 수출 시장을 위한 리사이클 기준을 충족하는 필름의 수주가 견조하게 추이하고 있습니다.

2024년 초, 저렴한 수입품으로 국내 원료 경쟁력이 저하된 결과 국내 업스트림 부문의 가동률은 55%를 밑돌았습니다. 컨버터 기업은 스팟 수지 가격이 전월 대비 15% 이상 변동하기 때문에 비용을 확실히 헤지할 수 없어 고정 가격 포장 계약의 이익률이 압박되고 있습니다. 제안된 안티 덤핑 관세는 국내 공급을 안정시킬 수 있지만, 국내 크래커의 증산 또는 수입 할당의 계약이 이루어질 때까지 불확실성이 남아 있습니다. 이러한 이유로 인도네시아의 연포장 시장에서는 견고한 최종 용도 수요가 있음에도 불구하고 신중한 생산 능력 확대가 계속되고 있습니다.

플라스틱은 비용 효율성과 뛰어난 방습 특성으로 2025년에도 매출 점유율 67.61%를 유지해 인도네시아의 연포장 시장을 지원했습니다. 폴리에틸렌(PE) 및 폴리프로필렌(PP) 필름은 스낵 과자, 냉동 식품, 농업 용도에 필수적인 소재로 계속되고 있습니다. 그러나 PE 60만 5,000톤, PP 59만 9,000톤에 이르는 수입 의존도가 가격 안정성을 제한하고 있습니다. 바이오플라스틱 및 퇴비화 가능 소재는 베이스는 작은 것, EPR(생산자 책임 확대)의 기한이 다가오는 가운데, 7.45%라는 가장 빠른 CAGR을 기록하고 있습니다.

경쟁 대응책으로는 Greenhope사의 PHA 베이스 필름이나 바이오팩사의 퇴비화 기준 적합 전분 블렌드 필름을 들 수 있습니다. 브랜드 소유자는 기계적 강도를 유지하면서 재활용을 단순화하는 단일 소재 PE 라미네이트 시험을 진행하고 있습니다. 생분해성 고분자 공장에 대한 정부 지원책으로 현재의 비용 프리미엄에도 불구하고 대체기재용 인도네시아 연포장 시장 규모는 2031년까지 계속 확대될 전망입니다.

2025년 시점에서 가방·파우치는 식품, 퍼스널케어, 농약 제품 라인에 있어서 범용성으로부터, 인도네시아의 연포장 시장 규모의 46.88%를 차지했습니다. 스탠드업 형식, 지퍼, 주둥이는 현대 소매 환경에서 편리함과 매장에서의 소구력을 높입니다. 필름과 랩은 육류 가공업이나 원예 산업에, 라벨은 프리미엄 브랜딩 예산을 획득하는 용도로 활용되고 있습니다.

향 주머니 및 스틱 팩은 CAGR 6.35%로 확대되어 군도 시장의 저렴한 가격과 무료 샘플 요구를 충족합니다. 디지털 인쇄기에 의해 금형을 변경하지 않고 지역 고유의 언어나 공휴일의 디자인이 가능하게 되어, 발매까지의 리드 타임을 며칠로 단축하고 있습니다. 일회용 플라스틱에 대한 규제 강화를 받아, 컨버터는 리필 파우치나 리사이클 가능한 라미네이트 구조를 제안해, 소형 포맷의 편리성과 환경 규제 준수의 밸런스를 도모하고 있습니다.

The Indonesia flexible packaging market was valued at USD 4.58 billion in 2025 and estimated to grow from USD 4.79 billion in 2026 to reach USD 5.97 billion by 2031, at a CAGR of 4.52% during the forecast period (2026-2031).

This trajectory reflects Indonesia's position as Southeast Asia's largest economy, with an urbanizing population that is steadily shifting toward packaged foods and online retail, both of which rely heavily on flexible formats. Growing demand for small-portion packs, sustained e-commerce activity, and corporate moves toward sustainability are reinforcing material, product, and technology shifts that favor the Indonesia flexible packaging market. Imported finished goods, primarily from China, remain a cost challenge for domestic converters; however, mandatory Extended Producer Responsibility (EPR) regulations, set to take effect in 2025, are expected to accelerate demand for locally recycled feedstock. Competitive responses now center on vertical integration, barrier-film innovation, and digital printing capabilities that enable low minimum-order runs for Indonesia's 25.5 million digitally enabled SMEs.

Packaged foods contributed 6.47% to national GDP in 2024, a share the Indonesian Association of Food and Beverage Entrepreneurs expects to rise as urban households favor ready-to-eat meals and premium snacks. Mandatory halal labels introduced in October 2024 require clear, durable printing, pushing brands toward high-barrier multi-layer films that preserve product integrity across Indonesia's humid, multi-island supply chain. Imported specialty foods and rising disposable incomes further drive demand for premium protective structures. Against this backdrop, converters offering advanced oxygen- and moisture-barrier films are gaining orders from dairy, meat, and confectionery processors. The Indonesia flexible packaging market benefits directly from this steady volume growth and the shift to modern trade channels that prefer merchandisable stand-up pouches.

EPR regulations effective 2025 require producers to cut post-consumer plastic waste by 30% by 2029, spurring investments in recyclable mono-material films and certified compostables. Local start-ups Greenhope and Biopac are scaling PHA- and starch-based films, while multinationals such as Danone Indonesia already use 25% recycled content in water bottles, creating pull-through for food-grade rPET. Brands seeking to signal their environmental credentials now specify drop-in substrates that maintain barrier performance while simplifying end-of-life handling. The Indonesian flexible packaging market, therefore, records strong order inflows for films that meet Asian and export-market recyclability standards.

Domestic upstream utilization fell below 55% in early 2024 after cheaper imports cut local feedstock competitiveness. Converters cannot reliably hedge costs because spot resin price swings exceed 15% month-on-month, compressing margins on fixed-price packaging contracts. Proposed anti-dumping duties may stabilize the domestic supply; however, uncertainty persists until local crackers increase output or import quotas are tightened. The Indonesia flexible packaging market therefore experiences cautious capacity expansions despite solid end-use demand.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastics retained 67.61% revenue share in 2025 owing to cost efficiency and robust moisture-barrier properties, anchoring the Indonesia flexible packaging market. Polyethylene and polypropylene films remain integral to snacks, frozen food, and agricultural applications; however, import dependence for 605,000 t of PE and 599,000 t of PP limits price stability. Bioplastics and compostables, though starting from a smaller base, log the fastest 7.45% CAGR as EPR deadlines loom.

Competitive responses include PHA-based films by Greenhope and starch blends from Biopac that comply with compostability norms. Brand owners are trialing mono-material PE laminates that simplify recycling while maintaining mechanical strength. Government incentives for biodegradable polymer plants should keep the Indonesian flexible packaging market size for alternative substrates expanding through 2031 despite current cost premiums.

Bags and pouches commanded 46.88% of Indonesia flexible packaging market size in 2025, thanks to versatility across food, personal care, and agrochemical lines. Stand-up formats, zippers, and spouts enhance convenience and shelf appeal in modern retail. Films and wraps serve the meat processing and horticulture industries, whereas labels capture premium branding budgets.

Sachets and stick packs, advancing at 6.35% CAGR, address affordability and sampling needs across archipelagic markets. Digital presses enable region-specific languages and holiday designs without altering tooling, trimming launch cycles to days. Regulatory scrutiny of single-use plastics prompts converters to propose refill pouches and recyclable laminate structures, striking a balance between small-format convenience and environmental compliance.

The Indonesia Flexible Packaging Market Report is Segmented by Material (Paper, Plastic, Metal Foil, Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, and More), End-User Industry (Food, Beverage, Healthcare and Pharmaceutical, and More), Printing Technology (Flexography, Rotogravure, Digital Printing, and More). The Market Forecasts are Provided in Terms of Value (USD).