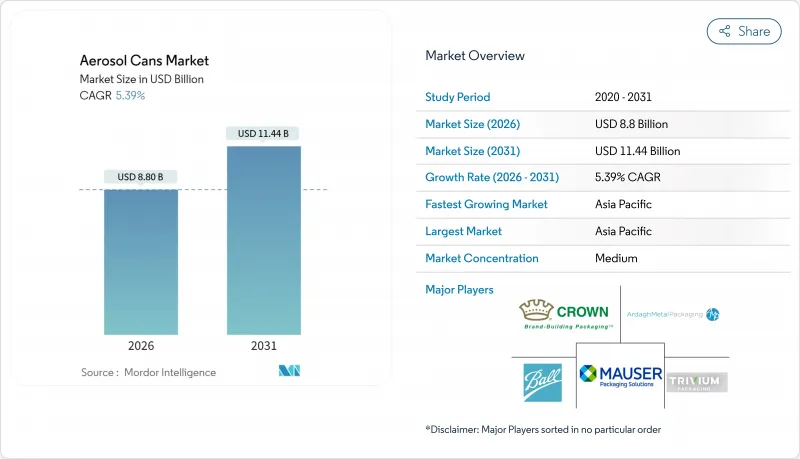

에어로졸 캔 시장 규모는 2026년에 88억 달러로 추정되고 있으며, 2025년 83억 5,000만 달러에서 성장한 수치입니다. 2031년 114억 4,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.39%로 성장할 것으로 전망됩니다.

지속적인 성장은 포장 산업에서 재생가능 소재로의 전환, 순환형 경제 목표와의 규제 무결성, 알루미늄 용기가 보다 엄격한 휘발성 유기 화합물(VOC) 제한을 충족하는 입증된 능력으로 형성됩니다. E커머스의 확대는 복잡한 물류 네트워크를 견딜 수 있는 누설 방지 및 선반출 가능한 포장 형태를 요구하는 브랜드에 의해 한층 더 기세를 더하고 있습니다. 저GWP 추진제와 단일 소재 캔 설계의 혁신은 시장 리더의 경쟁 차별화를 강화하고 있습니다. 한편, 원재료 비용의 변동성과 급속하게 보급되는 리필 가능한 컨셉이 단기적인 이익률을 억제하는 요인이 되고 있습니다.

알루미늄의 무한 리사이클성은 확대 생산자 책임 제도 하에서 제품 수명 종료시의 성능을 문서화할 필요가 있는 브랜드 오너에게 결정적인 소재로 변모시켰습니다. 볼사의 ReAl 합금은 강도를 유지하면서 캔 본체의 탄소 실적를 50% 삭감하고, 지금까지 생산된 알루미늄의 75%가 현재도 유통되고 있는 기존 세계의 재활용 인프라의 폐쇄 루프 이점을 강화하고 있습니다. 이러한 실적은 기후 변화 보고 요건과 플라스틱 삭감 목표에 직면하는 소비재 대기업과의 장기 공급 계약을 지원하고 있습니다.

고급 퍼스널케어 제품 라인은 사용자 체험을 향상시키고 고가격화를 가능하게 하는 브러쉬드 메탈조의 미관과 특수 밸브가 점점 지정되고 있습니다. 볼사와 메도우사가 2025년에 발매 예정의 리필식 「MEADOW KAPSUL」카트리지는 고급 스킨케어 및 헤어 케어 브랜드가 지속가능성과 디자인으로 차별화를 도모하기 위해, 세련된 알루미늄 에어로졸 용기를 채택하는 사례를 나타내고 있습니다. 전자상거래는 이 동향을 가속화하고 있습니다. 금속 용기는 라스트 마일 배송시의 함몰이나 누출에 강하고, 디지털 판매 촉진을 위한 360도 촬영에도 대응할 수 있기 때문입니다.

2025년 7월 시행의 EPA 개정법에서는 제품 가중 반응성 상한치가 의무화되어 고반응성 용제의 대체가 요구되고 있습니다. 유럽의 병행 F-가스 규제는 규정 준수 복잡성을 심화시켜 소규모 기업이 R&D를 아웃소싱하거나 영향을 받는 라인에서 철수하도록 유도합니다. 폐기 규칙은 사용한 캔의 통기 및 압축 포장이 문서화 프로토콜 하에서 의무화되어 처리 비용이 증가하는 한편, 리퍼블릭 서비스사의 전용 시설 등 전문적인 재활용 솔루션 수요도 높아지고 있습니다.

2025년 시장 규모에서 알루미늄이 84.72%를 차지하며, 그 확립된 인프라와 대부분의 리사이클 규정 하에서의 수용성을 뒷받침하고 있습니다. 이 주도적 지위는 비용 효율적인 폐쇄 루프 공급을 지원하며 EU에서 이미 시행된 확대 생산자 책임 제도와도 일치합니다. 에어로졸 캔 시장은 ReAl 합금의 진보에 의해 혜택을 받고 있으며, 함몰 저항성을 손상시키지 않고 판 두께 중량을 15% 삭감. 단위당 경제성을 유지하면서 탄소 배출 지표를 저감하고 있습니다.

플라스틱 에어로졸은 연간 8.18%로 성장하여 완벽한 투명성, 내충격성, 산성 처방에 적합하다는 브랜드 요건을 충족합니다. 플라스틱 팩의 금속 미사용 "SprayPET Revolution"은 수지 제조업체가 고급 장벽 층을 전개하는 동안 폴리머가 압력 임계치를 충족하고 주류 PET 재활용 인프라와의 호환성을 유지할 수 있음을 입증했습니다. 플라스틱은 금속 냄새나 냉간 충격이 우려되는 퍼스널케어 제품이나 식품 스프레이 용도에 있어서 확고한 지위를 구축하고 있습니다. 이러한 기세가 있음에도 불구하고, 단일 소재 규제와 금속 가격의 변동으로 인해 알루미늄은 에어로졸 캔 시장 전략의 핵심으로 계속되고 있습니다.

단일 스트로크 충격 압출 성형으로 용접 피팅를 최소화하고 품질 관리를 간소화하는 원피스 모노블록 라인은 2025년 생산량의 64.58%를 차지했습니다. 균일한 두께 구조는 낙하 시험 내성과 고내압 성능으로 정평이 나며, 헤어 스프레이나 자동차용 브레이크 클리너 SKU의 가연성 추진제에 필수적입니다.

한편, 2피스캔은 CAGR7.05%로 확대 경향이 있습니다. 서보 제어 바디 제조업체 기술에 의한 측면 시임 강도의 향상과 재료 사용량을 삭감하는 하이브리드 금속 게이지의 채택이 배경에 있습니다. 브랜드 오너는 키가 크고 슬림한 형상의 제조와 원통형 본체를 왜곡없이 덮는 고화질 리소그래피를 높이 평가했습니다. 계절 상품의 발매에 수반하는 신속한 디자인 변경 수요에 대응하기 위해, 제조업체는 모노블록과 투피스의 생산을 전환 가능한 모듈식 금형에 투자해, 시장 기호의 변화에 대비하고 있습니다.

아시아태평양은 2025년 소비량의 39.62%를 차지했으며 7.86%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 이는 중국이 주요 소비지이자 생산 거점이라는 이중 역할을 담당하고 있다는 점에서 지원됩니다. 도시화와 가처분 소득 증가가 퍼스널케어용 에어로졸 제품의 보급을 뒷받침하는 한편, 지역 당국은 알루미늄의 폐쇄 루프 이점과 시너지 효과를 발휘하는 재활용 의무를 부과하고 있습니다. 일본 브랜드 소유자는 단일 소재 디자인을 추진하고 인도의 미용 부문의 가속은 현지 충전 업체의 생산량 확대로 이어지고 있습니다.

유럽은 기술과 규제 측면에서 계속 선도적 입장에 있습니다. 프론가스 규제나 VOC 상한치에 의해 환경에 배려한 추진제로의 이행이 가속해, 규제 대응 제품 포트폴리오를 가지는 기존 기업이 우위성을 발휘하고 있습니다. 독일과 영국은 경량 캔의 연구 개발을 주도하고, 동유럽 공장은 저비용 충전 능력을 확대하고, 지역 횡단적인 FMCG 계약에 대응하고 있습니다. 시장 성장은 프리미엄 제품과 지속가능한 제품에 기울어져 있으며 기존 카테고리 수요 포화가 확대를 제한하고 있습니다.

북미에서는 혁신 주도의 안정된 수요가 지속되고 있습니다. EPA 반응성 규제는 처방의 재설계가 요구되는 반면, 견고한 R&D 자금으로 현지 컨버터는 제품 포트폴리오의 유연성을 유지하고 있습니다. 미국은 OTC 의료품과 DIY용 도료 에어로졸로 주도적 입장에 있으며, 멕시코는 니어쇼어 제조 거점으로서 존재감을 높여가고 있습니다. 캐나다 소비자층에서는 저취기 가정용 스프레이에 대한 관심이 높아지고 있어 수계 추진제의 채택을 뒷받침하고 있습니다. 이러한 동향이 결합되어 성숙하면서도 수익성이 높은 지역 시장 전체에서 중간 정도의 단일 자리 성장이 지속되고 있습니다.

Aerosol cans market size in 2026 is estimated at USD 8.8 billion, growing from 2025 value of USD 8.35 billion with 2031 projections showing USD 11.44 billion, growing at 5.39% CAGR over 2026-2031.

Sustained growth is shaped by the packaging sector's pivot toward recyclable materials, regulatory alignment with circular-economy targets, and the proven ability of aluminum containers to meet stricter volatile-organic-compound (VOC) limits. E-commerce expansion adds momentum as brands seek leak-proof, shelf-ready pack formats that withstand complex fulfillment networks. Innovation in low-GWP propellants and mono-material can designs is strengthening the competitive differentiation of market leaders. At the same time, raw-material cost volatility and fast-rising refillable concepts temper near-term margins.

Aluminum's infinite recyclability has turned it into a decisive material for brand owners that must document end-of-life performance under extended producer responsibility schemes. Ball Corporation's ReAl alloy cuts the can body's carbon footprint by 50% while maintaining strength, reinforcing the closed-loop advantages of an existing global recycling infrastructure where 75% of aluminum ever produced remains in active circulation. Such credentials underpin long-term supply contracts with consumer-goods majors that face climate-reporting requirements and plastic-reduction targets.

Premium personal-care lines increasingly specify brushed-metal aesthetics and specialized valves that elevate user experience and enable higher pricing. Ball and Meadow's 2025 launch of refillable MEADOW KAPSUL cartridges illustrates how luxury skin- and hair-care brands turn to elegant aluminum aerosols to differentiate on sustainability and design. E-commerce accelerates this trend because metallic containers resist dents and leakage during last-mile delivery while offering 360-degree imaging for digital merchandising.

EPA amendments effective July 2025 enforce product-weighted reactivity ceilings that oblige formulators to swap high-reactivity solvents or face penalties. Parallel F-gas restrictions in Europe intensify compliance complexity, pushing smaller firms to outsource R&D or exit affected lines.Disposal rules now require spent cans to be vented and baled under documented protocols that elevate processing costs, yet also spur specialized recycling solutions such as Republic Services' dedicated facilities.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Aluminum captured 84.72% of the 2025 volume, underscoring its entrenched infrastructure and acceptance under most recycling codes. This leadership supports cost-efficient closed-loop supply and aligns with extended-producer-responsibility statutes already active in the EU. The aerosol cans market benefits from ReAl alloy advances that trim gauge weight by 15% without compromising dent resistance, keeping unit economics competitive while lowering carbon metrics.

Plastic aerosols, growing 8.18% annually, address brand requirements for full transparency, shatter resistance, and compatibility with acidic formulas. Plastipak's metal-free SprayPET Revolution validates that polymers can meet pressure thresholds and remain compatible with mainstream PET recycling infrastructures as resin suppliers roll out advanced barrier layers, plastics secure footholds in personal-care and food spray applications where metal taste or cold shock are concerns. Even with this momentum, mono-material legislation and metal price volatility keep aluminum at the core of the aerosol cans market strategy.

One-piece monobloc lines own 64.58% of 2025 unit output thanks to single-stroke impact-extrusion that minimizes weld seams and simplifies quality control. The configuration's uniform wall thickness supports a reputation for drop-test resilience and elevated internal pressures, essential for flammable propellants in hair-spray or automotive brake-cleaner SKUs.

Two-piece cans, posting a 7.05% CAGR, gain traction as servo-controlled body-maker technology enhances side-seam strength and allows hybrid metal gauges that lower material use. Brand owners appreciate the ability to produce tall, slim profiles and high-definition lithography that wraps around the cylindrical body without distortion. With demand for fast design turnarounds in seasonal product drops, manufacturers invest in modular tooling that switches between monobloc and two-piece runs, hedging against market preference shifts.

The Aerosol Cans Market Report is Segmented by Material Type (Aluminium, Steel, Tinplate, and More ), Can Type (One-Piece (Monobloc), Two-Piece, Three-Piece), Propellant Type (Compressed Gas, Bag-On-Valve, and More), Capacity (ml) (Less Than 100, 101-300, and More), End-User Industry (Personal Care and Cosmetics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific composed 39.62% of 2025 consumption and is rising at an 7.86% CAGR, anchored by China's dual role as leading consumer and production hub. Urbanization and disposable-income growth support wider adoption of personal-care aerosols, while regional authorities impose recycling mandates that dovetail with aluminum's closed-loop advantages. Japanese brand owners advance mono-material designs, and India's accelerating beauty segment amplifies volumes for local fillers.

Europe remains a technology and regulation frontrunner. F-gas and VOC ceilings prompt swift migration to green propellants, rewarding incumbents with compliant product portfolios.Germany and the United Kingdom lead in lightweight-can R&D, while Eastern European plants extend low-cost filling capacity to pan-regional FMCG contracts. Market growth leans toward premium and sustainable offerings as volume saturation limits expansion in traditional categories.

North America demonstrates steady, innovation-driven demand. EPA reactivity rules compel formula redesigns, yet robust R&D funding helps local converters maintain portfolio agility. The United States leads in OTC healthcare and DIY paint aerosols, while Mexico strengthens as a near-shore manufacturing base. Canadian consumers show elevated interest in low-odor household sprays, bolstering adoption of water-based propellants. Together these trends sustain mid-single-digit growth across a maturing yet profitable regional landscape.