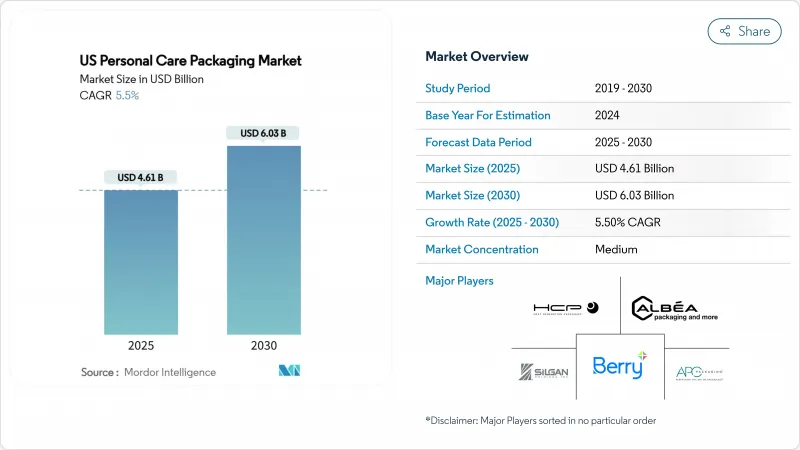

미국의 퍼스널케어 포장 시장 규모는 2025년 46억 1,000만 달러로, 예측 기간 중(2025-2030년) CAGR은 5.5%로 확대되어, 2030년까지 60억 3,000만 달러에 이를 것으로 예측됩니다.

PFAS의 지속적인 단계적 폐지, 지속가능성의 의무화, 소셜 미디어 주도의 눈길을 끄는 팩의 추구에 의해 재료의 선택과 디자인 철학이 재구성되고 있습니다. 미네소타 주에서는 2025년에 화장품에 대한 의도적인 PFAS 첨가를 금지하는 엄격한 주 규칙이 있으며, 컨버터 각 회사는 새로운 장벽 화학 탐구와 재활용 인프라 업그레이드를 강요받고 있습니다. 서부 가구는 퍼스널케어 용품에 매년 1,038달러를 지출하고 있으며, 이는 전국 평균 908달러를 크게 웃돌고 있습니다. 이 추세는 2025년 4월 Amcor가 Berry Global과 전체 주식을 통합하여 2028년까지 6억 5,000만 달러의 시너지 효과와 30억 달러 이상의 현금 흐름을 창출할 것으로 예상된다는 점에서 분명합니다. 이러한 힘은 미국의 퍼스널케어 포장 시장 전체의 꾸준한 가치 성장, SKU의 보급, 리필 대응 디자인에 대한 수요 증가를 지원하고 있습니다.

2024년 퍼스널케어 지출은 가구당 908달러에 이르고, 연평균 지출 1,038달러인 구미에서는 더욱 상승합니다. 견조한 임금 상승은 SKU의 다양화, 프리미엄 팩 마감, 틈새 배합으로 이어져, 미국의 퍼스널케어 포장 시장 전체의 수량 요건을 밀어 올립니다. 소비자가 유리와 금속을 품질과 지속가능성에 연결하기 때문에 유리와 금속의 형식이 가장 혜택을 받습니다.

디자인은 이제 마케팅 채널을 겸하고 있으며, 브랜드는 인상적인 모양, 엠보싱, 사진 빛나는 특주 색채에 대한 투자를 촉진하고 있습니다. 유리병과 브러시드 알루미늄 에어로졸은 기존의 HDPE 병보다 우수합니다. 이는 소셜 플랫폼의 에코 메시지와 비주얼 스토리텔링과 일치하기 때문입니다. L'Oreal이 IBM과 제휴하고 지속 가능한 처방에 대해 AI를 훈련한 것은 기술 융합이 어떻게 외형과 기능을 모두 지원하는지 명확하게 보여줍니다.

새로운 블로우 성형 금형과 정밀 펌프의 개발은 라인 당 100만 달러를 초과할 수 있습니다. 소규모 컨버터는 특히 바이오 수지가 특수 기계와 장기간 인증을 필요로 하는 경우 여러 시험에 자금을 제공하는 데 어려움을 겪습니다. 접을 수 있는 어플리케이터에 대한 특허 출원은 차별화된 디스펜싱 기술 뒤에 복잡성과 자본 집약성을 보여줍니다.

플라스틱은 저비용, 설계 유연성 및 확립된 공급망을 통해 2024년 50.6%의 미국 퍼스널케어 포장 시장 점유율을 유지합니다. 그러나 종이 및 판지 분야는 PFAS 단속과 재생 가능한 기재에 대한 소비자의 지지에 힘입어 2030년까지 연평균 복합 성장률(CAGR) 9.5%를 보일 것으로 예측되고 있습니다. 브랜드는 장벽 코팅 판지와 보존성을 손상시키지 않고 습기 테스트를 통과하는 섬유 성형 병을 시도합니다. 재활용 PET의 통합과 시험적 화학 재활용 플랜트는 순환성에 대한 우려를 완화하고 플라스틱 리드를 보호합니다.

순환형 경제 정책에 따라 컨버터는 소비자 사용 후 수지(PCR) 함유율을 높여 인출 제도를 구축하도록 요구되고 있습니다. 동시에 유리와 금속은 럭셔리 제품으로 자리매김하여 이익을 얻고 있습니다. 럭셔리 스킨 케어 브랜드는 무한한 재활용 가능성을 느끼면서 가격 프리미엄을 정당화하기 위해 무거운 벽의 플라콘과 브러시가 있는 알루미늄 스틱을 채용하고 있습니다. 소재의 혁신은 수직 통합에 의해서도 촉진되고, 확대하는 미국의 퍼스널케어 포장 시장에 대한 PCR 공급을 확보하는 Amcor의 수지 조달 투자가 그 예입니다.

병은 2024년 미국의 퍼스널케어 포장 시장 규모의 38.2%를 차지했고 그 이유는 친숙함, 선반에서의 임팩트, 로션, 샴푸, 바디소프 등의 범용성에 있습니다. 그러나 플렉서블 파우치는 전자상거래의 큐브 효율과 재료 사용량이 적어 CAGR 11.2%를 보일 것으로 예측됩니다. 리캡 가능한 입구와 스탠드업 방식은 소비자의 편의성을 높이고 초박형 필름은 출하 중량을 억제합니다.

튜브, 스틱, 정밀 펌프는 선케어용 SPF 스틱이나 단가보다 투여 정밀도가 중요한 레티놀 미용액용 에어리스 펌프 등 타겟으로 하는 용도에 대응합니다. 접이식 카톤은 브랜드가 커브 사이드 재활용을 단순화하는 단일 소재 종이 솔루션으로 전환함에 따라 지보를 강화하고 있습니다. 모든 형식에서 NFC 칩과 QR 코드는 팩을 참여 허브로 승화시켜 혼잡한 미국의 퍼스널케어 포장 시장에서 중요한 차별화 요인이 되고 있습니다.

The US Personal Care Packaging Market size is estimated at USD 4.61 billion in 2025, and is expected to reach USD 6.03 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Persistent PFAS phase-outs, mounting sustainability mandates and the social-media driven quest for eye-catching packs are reshaping material selection and design philosophies. Tight state rules Minnesota's 2025 ban on intentionally added PFAS in cosmetics among them push converters to explore new barrier chemistries and upgrade recycling infrastructure. Regional spending patterns amplify these shifts: households in the West devote USD 1,038 each year to personal-care items, well above the USD 908 national average, which explains the region's early uptake of premium, sustainable formats. Brand owners also intensify vertical integration to lock in packaging innovation capacity, a trend underscored by Amcor's all-stock combination with Berry Global in April 2025, expected to generate USD 650 million in synergies and more than USD 3 billion in cash flow by 2028. Together, these forces support steady value growth, SKU proliferation and rising demand for refill-ready designs across the US personal care packaging market.

Personal-care outlays reached USD 908 per household in 2024 and climb even higher in the West, where annual spending averaged USD 1,038. Steady wage gains translate into greater SKU variety, premium pack finishes and niche formulations, which in turn boost unit-volume requirements across the US personal care packaging market. Glass and metal formats benefit the most because consumers associate them with quality and sustainability.

Design now doubles as a marketing channel, prompting brands to invest in striking shapes, embossing and custom colorways that photograph well. Glass jars and brushed-aluminum aerosols outperform conventional HDPE bottles because they align with eco-messaging and visual storytelling on social platforms. L'Oreal's partnership with IBM to train AI on sustainable formulations underscores how tech convergence supports both look and function.

Developing a new blow-mold or precision pump can exceed USD 1 million per line. Small converters struggle to fund multiple trials, particularly when bio-based resins demand specialized machinery and extended qualification. Patent filings for collapsible applicators illustrate the complexity as well as the capital intensity behind differentiated dispensing technology.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic retained 50.6% US personal care packaging market share in 2024 thanks to low cost, design flexibility and well-established supply chains. Yet the paper and paperboard segment is projected to log a 9.5% CAGR through 2030, buoyed by PFAS crackdowns and consumer favor for renewable substrates. Brands experiment with barrier-coated cartons and molded-fiber jars that pass moisture tests without compromising shelf appeal. Recycled PET integration and pilot chemical recycling plants help plastics defend their lead by easing circularity concerns.

Circular-economy policies push converters to raise post-consumer-resin (PCR) content and build take-back schemes. Simultaneously, glass and metal profit from luxury positioning: prestige skin-care labels deploy heavy-walled flacons and brushed-aluminum sticks to justify price premiums while touting infinite recyclability. Material innovation is also spurred by vertical integration, exemplified by Amcor's resin-sourcing investments that safeguard PCR supply for the expanding US personal care packaging market.

Bottles commanded 38.2% of the US personal care packaging market size in 2024 due to familiarity, shelf impact and versatility across lotions, shampoos and body washes. However, flexible pouches are projected to log an 11.2% CAGR, propelled by e-commerce cube-efficiency and lower material usage. Reclosable spouts and stand-up formats bolster consumer convenience, while ultra-thin films curb shipping weight.

Tubes, sticks and precision pumps cater to targeted applications think SPF sticks for sun-care or airless pumps for retinol serums where dosing accuracy matters more than unit cost. Folding cartons gain ground as brands migrate to mono-material paper solutions that simplify curbside recycling. Across all formats, NFC chips and QR codes elevate packs into engagement hubs, a key differentiator in the crowded US personal care packaging market.

US Personal Care Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard), Product Type (Bottles, Tubes and Sticks, Pumps and Dispensers, Pouches and More), Application (Skin Care, Hair Care, Oral Care, and More), Sustainability Attribute (Recyclable, Post-Consumer-Recycled Content, Refillable/Reusable, Compostable/Bio-based). The Market Forecasts are Provided in Terms of Value (USD).