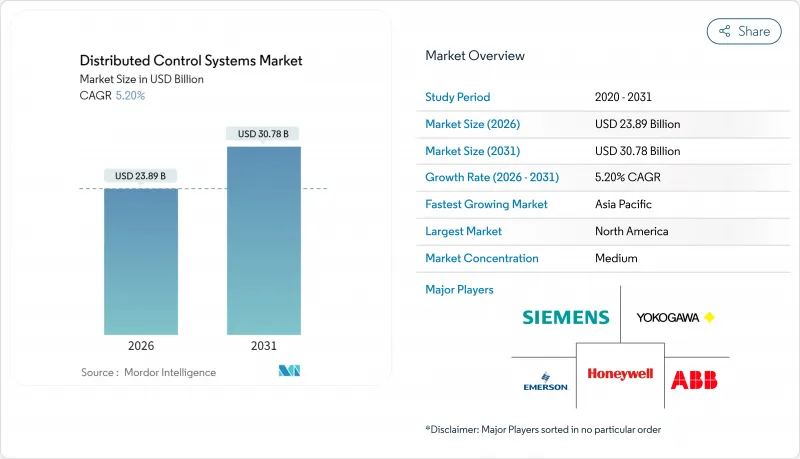

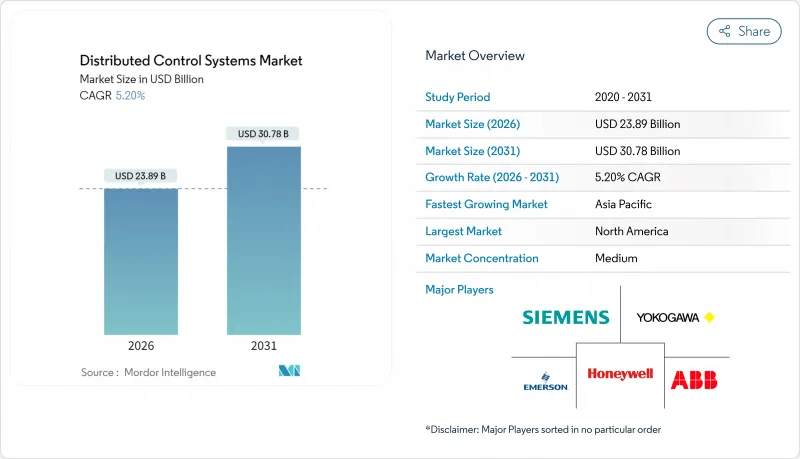

분산 제어 시스템 시장은 2025년 227억 1,000만 달러로 평가되었고, 2026년 238억 9,000만 달러에서 2031년까지 307억 8,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 5.20%로 성장이 전망됩니다.

그린 수소의 보급 확대, 탄소 포집 프로젝트, 원자력 발전의 증강, 제약 업계에서의 연속 생산으로의 이행이 성장을 지지하고 있습니다. 각 공급업체는 운영상의 이익을 창출하기 위해 소프트웨어 정의 아키텍처, 디지털 트윈 통합 및 엣지 연결성을 확대하고 있으며, 소규모 플랜트는 진입 비용을 줄이는 축소판 플랫폼을 채택하고 있습니다. 사이버 보안 요구사항 증가, 인증 엔지니어 부족, 반도체 공급 제약의 잔존이 확대 페이스를 억제하는 것, 성장 그 자체를 저해하지 않습니다. 경쟁의 초점은 예측 보전, 모듈식 도입 및 자본 지출을 분산시키는 구독형 라이선싱에 집중되어 있습니다.

그린 수소의 생산 능력 발표는 2024년에 1,640만 톤에 이르렀으며, 신규 플랜트마다 200만-1,000만 달러 상당의 고도의 제어 플랫폼이 도입됩니다. DCS 아키텍처는 간헐적인 재생에너지 처리, 수소 안전성 확보, 5년 이내에 20-30%로 예측되는 전해조 효율의 급속한 향상에 대응할 수 있는 유연성이 요구됩니다. 공급업체는 플랜트의 단계에 따라 확장 가능한 모듈식 제어 노드를 패키징하여 운영자가 전반적인 교체 없이 업그레이드할 수 있도록 합니다. 유럽과 중동이 도입을 선도하고 있지만, 북미 개발업체도 인플레이션 억제법(IRA) 우대 조치와 관련된 견적 의뢰서를 급속히 발행하고 있습니다. 장기적인 투자 전망으로 분산 제어 시스템 시장의 프로젝트는 2030년을 크게 넘어 안정적인 파이프라인이 형성되고 있습니다.

규제 당국은 현재 새로운 원자로마다 에어 갭 방식의 안전 클래스 DCS와 인증된 중복성을 요구하고 있습니다. 미국 원자력 규제 위원회(NRC)는 2025년 사이버 규칙을 강화했으며, 적합 비용은 상승했으며, 준수 플랫폼의 프리미엄 가격을 고정화했습니다. SMR 공급업체는 물리적 배선 거리를 단축하고 건설 일정을 단축하며 원격 진단을 지원하는 디지털 안전 채널을 지정합니다. 유럽과 중국은 비슷한 틀을 표준화하고 있으며, 걸프 국가들은 해수 담수화 시설의 탈탄소화를 위한 원자로 유닛을 추가로 도입하고 있습니다. 18개월 이상 걸리는 인증 사이클은 새로운 진입을 막아 분산 제어 시스템 시장에서 기존 공급업체의 입지를 강화하고 있습니다.

오픈 프로세스 오토메이션의 파일럿 도입은 기존 DCS 구축에 비해 52%의 비용 절감을 입증하고 있으며, 자본 지출을 신중하게 검토하는 중소규모 오퍼레이터에게 매력적인 선택이 되고 있습니다. 공급업체 측은 구독 라이선스, 유연한 I/O 및 하드웨어 수를 줄이는 사전 설계된 라이브러리로 대응하고 있습니다. 그러나 가격 상승에 대한 우려로 ASEAN, 라틴아메리카, 아프리카의 일부 지역에서 프로젝트가 연기되고 분산 제어 시스템 시장의 성장률이 0.8포인트 내려갔습니다.

2025년 하드웨어는 분산 제어 시스템 시장에서 54.35%의 점유율을 유지했습니다. 이는 현장 입증된 컨트롤러, 범용 I/O 및 중복 네트워크에 대한 최종 사용자 선호도를 반영합니다. 에너지 및 화학 분야에서의 갱신 사이클에 힘입어 하드웨어의 분산 제어 시스템 시장 규모는 123억 4,000만 달러에 달했습니다. 공급업체는 현재 아날로그 신호, 디지털 신호 및 HART 신호를 모든 채널에서 수용할 수 있는 구성 가능한 I/O 슬라이스를 출하하여 캐비닛 수를 최대 30%까지 줄일 수 있습니다. 유니버설 카드는 설계 후기 단계의 변경에도 대응하고 엄격한 스케줄에 직면하는 EPC 계약자에게 매력적인 기능입니다. 컨트롤러 플랫폼은 그린 수소 플랜트의 고밀도 PID 루프에 고속 사이클 시간을 추가하여 재생에너지로 인한 전원 공급 변동 시에도 정확도를 보호합니다.

소프트웨어 수익은 규모가 작고 운영자가 분석 기술, 가상화 및 OT-IT 융합을 도입함에 따라 연간 7.55%의 성장을 보이고 있습니다. 히스토리안 계층에 내장된 모델 예측 알고리즘은 설정값을 미세 조정하여 에너지 소비를 2-5% 삭감합니다. 가상화 서버는 단일 하이퍼바이저에서 여러 제어 도메인을 호스팅하여 장애 조치 및 패치 관리를 용이하게 합니다. 서비스 포트폴리오도 진화하고 있습니다. 에머슨의 상주 엔지니어는 KPI 달성을 보장하고 ABB의 라이프사이클 소프트웨어 계획은 사이버 강화 및 경보 합리화 업데이트를 통합합니다. 이 전환은 분산 제어 시스템 시장 전체의 가치 획득 구조를 재구축하고 자본재로부터 지속적인 서비스 수입으로의 초점 이행을 가져옵니다.

하이브리드 아키텍처는 중앙 집중식 모니터링 노드와 분산형 에지 컨트롤러를 결합하여 2025년에는 분산 제어 시스템 시장 규모의 45.40%를 차지했습니다. 플랜트에서는 이 토폴로지를 채용해, 레거시 I/O를 단계적으로 이행, 배선을 유지하면서, 전면적인 리플레이스 없이 새로운 분석 기능을 레이어링하고 있습니다. 일반적인 리노베이션 사례에서는 온프레미스 가상 머신이 제어 로직을 호스팅하고 확정 이더넷 링이 필드 모듈을 연결하여 50마이크로초 미만의 낮은 지연을 제공합니다. 하이브리드 구성은 사이버 보안 구역화를 단순화하여 안전 루프를 격리하면서 보안 프록시를 통한 데이터 액세스를 가능하게 합니다.

완전 이중화 고가용성 설계는 제약, LNG, 원자력과 같은 최종 사용자가 예기치 않은 다운타임 제로를 요구하기 때문에 8.95%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 리던던시는 컨트롤러, 전원, 스위치, 심지어 GPS 동기화 타임 스탬프 및 이벤트 시퀀싱의 정확성을 유지합니다. Siemens는 Audi 생산 라인에서 모션 제어를 중단하지 않고 서버간에 워크로드를 마이그레이션하는 가상 PLC를 입증했습니다. 중앙 집중식 컨트롤러는 유연성보다 결정론적 사이클이 우선하는 터빈 섬과 배치식 소화조에서 여전히 사용되고 있지만, 모듈형 디지털 플랜트가 새로운 설비 투자를 지배하는 동안 분산 제어 시스템 시장 점유율은 떨어지고 있습니다.

분산 제어 시스템(DCS) 시장 보고서는 업계를 다음 구분으로 분석합니다. 구성 요소별(하드웨어, 소프트웨어, 서비스) 최종 사용자 업종별(발전, 석유 및 가스, 기타) 아키텍처별(집중형 컨트롤러 시스템, 기타) 도입 모드별(온프레미스 등), 플랜트 규모별(소규모(5000 I/O 미만) 등), 지역별(북미, 유럽 등) 시장 예측은 금액(달러)으로 제시됩니다.

2025년 시점에서 아시아태평양은 분산 제어 시스템 시장의 37.60%를 차지했습니다. 이것은 중국의 정제 및 화학 능력과 인도의 급속한 인프라 정비에 지지된 것입니다. 지역 공급업체인 Supcon사는 도시 수도 사업과 중규모 화학 플랜트 안건을 획득하고 있지만, 수십억 달러 규모의 LNG나 원자력 프로젝트에서는 여전히 세계의 대기업이 주도권을 잡고 있습니다. 베이징의 스마트 제조 프로그램은 DCS 데이터와 기업 AI를 연계시키는 리노베이션 사업에 자금을 제공하고 소프트웨어 수요를 확대하고 있습니다. 인도의 생산 연동형 장려금(PLI) 제도는 의약품 및 전지 플랜트의 유치를 촉진하고, 이러한 플랜트는 당초부터 모듈식으로 확장 가능한 DCS를 지정하고 있습니다. 동남아시아 국가에서는 연포장 라인과 바이오 디젤 장비가 추가되어 중간 정도의 단일 자릿수 성장을 유지하고 있습니다.

중동은 6.95%라는 가장 빠른 CAGR을 기록하고 있으며, 사우디아라비아의 '비전 2030'이 원동력이 되고 있습니다. 이 계획은 왕국의 전력망의 40%를 자동화하고 그린 수소 클러스터를 구축합니다. GCC 국가들은 3조1,000억 달러 규모의 자본 프로젝트를 약속하고 있으며, 각 프로젝트는 설계 단계부터 OT-IT 융합을 통합하고 있습니다. 현지 통합업체는 다국적 기업과 제휴하여 현지 조달 비율을 달성하고 분산 제어 시스템 시장에서 공급업체 생태계를 확대하고 있습니다.

북미에서는 노후화된 전력 및 화학 인프라의 근대화가 진행되고, 에너지성(DOE) 및 국토 안보부(DHS)의 프로그램 하에서 사이버 보안 대책이 자금 조달의 필수 조건으로서 포함되고 있습니다. 인플레이션 억제법(IRA)은 중공업용 DCS를 많이 사용하는 이산화탄소 포집 기술 및 청정 연료에 대한 우대 조치를 촉진합니다. 유럽에서는 지속가능성에 중점을 두고 프로세스 플랜트는 고급 분석 기술을 도입하여 에너지 절감과 'Fit for 55' 목표에 부합합니다. 남미에서는 구리 및 리튬 채굴에 투자가 진행되고, 원격지용으로 엣지 접속 제어가 채용되는 한편, 아프리카에서는 현지 재생에너지를 융합한 해수 담수화나 송전망의 업그레이드가 전개되어, 2자리 성장 수요가 점재합니다.

The distributed control systems market was valued at USD 22.71 billion in 2025 and estimated to grow from USD 23.89 billion in 2026 to reach USD 30.78 billion by 2031, at a CAGR of 5.20% during the forecast period (2026-2031).

The green-hydrogen build-out, carbon-capture projects, nuclear power additions, and the pharmaceutical shift to continuous production anchor growth. Vendors are expanding software-defined architectures, digital-twin integration, and edge connectivity to unlock operational gains, while small plants adopt scaled-down platforms that lower entry costs. Rising cybersecurity requirements, shortages of certified engineers, and residual semiconductor constraints temper the pace but do not derail the expansion. Competitive momentum centers on predictive maintenance, modular deployment, and subscription licensing that spread capital outlays.

Green-hydrogen capacity announcements reached 16.4 million tons in 2024 and each new plant installs sophisticated control platforms valued at USD 2-10 million. DCS architectures must handle intermittent renewable power, ensure hydrogen safety, and flex for rapid electrolyzer efficiency gains forecast at 20-30% within five years. Vendors are packaging modular control nodes that scale with plant phases, letting operators upgrade without wholesale rip-and-replace. Europe and the Middle East lead early adoption, but North American developers are quickly issuing RFQs tied to Inflation Reduction Act incentives. The long investment horizon underpins a stable pipeline of distributed control systems market projects well beyond 2030.

Regulators now demand air-gapped, safety-class DCS with certified redundancy for every new reactor. The U.S. Nuclear Regulatory Commission tightened cyber rules in 2025, raising qualification costs but also locking in premium pricing for compliant platforms. SMR vendors specify digital safety channels that shorten physical wiring runs, cut construction schedules, and support remote diagnostics. Europe and China are standardizing on similar frameworks, while Gulf countries add nuclear units to decarbonize desalination. Certification cycles that run 18 months or more keep new entrants out and reinforce the position of incumbent suppliers in the distributed control systems market.

Open process automation pilots show 52% cost savings over classic DCS builds, tempting small and mid-tier operators that weigh every capital dollar Vendors counter with subscription licenses, flexible I/O, and pre-engineered libraries that trim hardware counts. Yet sticker shock still postpones projects in ASEAN, Latin America, and parts of Africa, shaving 0.8 percentage points off distributed control systems market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware retained a 54.35% distributed control systems market share in 2025, reflecting end-user preference for field-proven controllers, universal I/O, and redundant networks. The distributed control systems market size for hardware hit USD 12.34 billion, buoyed by replacement cycles in energy and chemicals. Vendors now ship configurable I/O slices that accept analog, digital, or HART signals on any channel, cutting cabinet counts by up to 30%. Universal cards also support late-stage design changes, a compelling feature for EPC contractors facing tight schedules. Controller platforms add fast cycle times for high-density PID loops in green hydrogen plants, safeguarding accuracy when power supply fluctuates with renewables.

Software revenue, though smaller, is rising 7.55% per year as operators embrace analytics, virtualization, and OT-IT convergence. Model-predictive algorithms embedded in historian layers fine-tune setpoints and shave energy consumption 2-5%. Virtualized servers host multiple control domains on a single hypervisor, easing failover and patch management. Service portfolios evolve as well: Emerson's factory resident engineers guarantee KPIs, while ABB's lifecycle software plans bundle cyber hardening and alarm-rationalization updates. This pivot reshapes value capture across the distributed control systems market, shifting focus from capital goods to recurring service streams.

Hybrid architectures blended centralized supervisory nodes with distributed edge controllers to secure 45.40% of the distributed control systems market size in 2025. Plants adopt this topology to migrate legacy I/O in phases, preserve wiring, and layer new analytics without wholesale rip-and-replace. In a typical retrofit, on-premise virtual machines host logic while deterministic Ethernet rings connect field modules, yielding latency under 50 microseconds. Hybrid layouts also simplify cybersecurity zoning, keeping safety loops isolated yet data-accessible via secure proxies.

Fully redundant high-availability designs grow fastest at 8.95% CAGR as pharma, LNG, and nuclear end-users mandate zero unplanned downtime. Redundancy spans controllers, power, switches, and even GPS-synchronized time stamps to maintain sequence-of-events accuracy. Siemens demonstrated a virtual PLC in a production Audi line that migrated workloads between servers without interrupting motion control. Centralized controllers still serve turbine islands and batch digesters where deterministic cycles trump flexibility, but their share of the distributed control systems market declines as modular digital plants dominate new capex.

Distributed Control System (DCS) Market Report Segments the Industry Into by Component (Hardware, Software, Services), by End-User Vertical (Power Generation, Oil & Gas, and More), Architecture (Centralized Controller Systems and More), Deployment Model(On-Premise and More), Plant Size(Small ( Less Than 5000 I/O) and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 37.60% share of the distributed control systems market in 2025, anchored by China's refining and chemicals capacity and India's rapid infrastructure build-out. Regional suppliers like Supcon win municipal water and mid-tier chemical jobs, yet global majors still dominate multi-billion-dollar LNG and nuclear projects. Beijing's smart-manufacturing program funds retrofits that couple DCS data with enterprise AI, expanding software pull-through. India's PLI incentives spur pharmaceutical and battery plants that specify modular, scalable DCS from day one. Southeast Asian economies add flexible packaging lines and biodiesel units, sustaining mid-single-digit growth.

The Middle East posts the fastest 6.95% CAGR, powered by Saudi Arabia's Vision 2030, which automates 40% of the kingdom's grid and builds green-hydrogen clusters. GCC states commit to USD 3.1 trillion in capital projects, each embedding OT-IT convergence from design. Local integrators partner with multinationals to meet localization quotas, broadening the vendor ecosystem within the distributed control systems market.

North America modernizes aging power and chemicals infrastructure, embedding cybersecurity as a funding prerequisite under DOE and DHS programs. The Inflation Reduction Act funnels incentives to carbon capture and clean fuels, both heavy DCS users. Europe emphasizes sustainability; process plants deploy advanced analytics to trim energy and comply with Fit-for-55 targets. South America invests in copper and lithium mining that uses edge-connected control for remote sites, while Africa rolls out desalination and grid upgrades blending local renewables, creating pockets of double-digit demand.