분산 제어 시스템 시장 : 컴포넌트별, 용도별, 최종 용도 산업별, 지역별 예측(-2030년)

Distributed Control System Market by Component, Application, End-use industry, Region - Global Forecast to 2030

상품코드:1777134

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 296 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

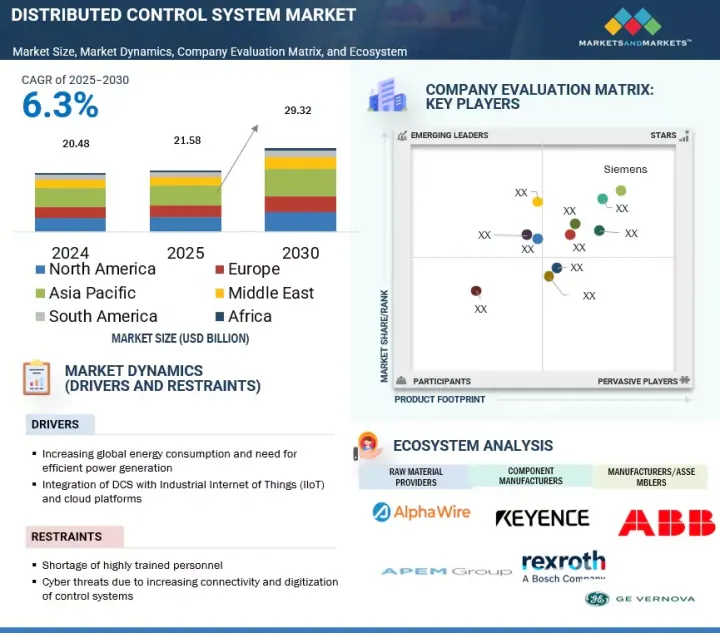

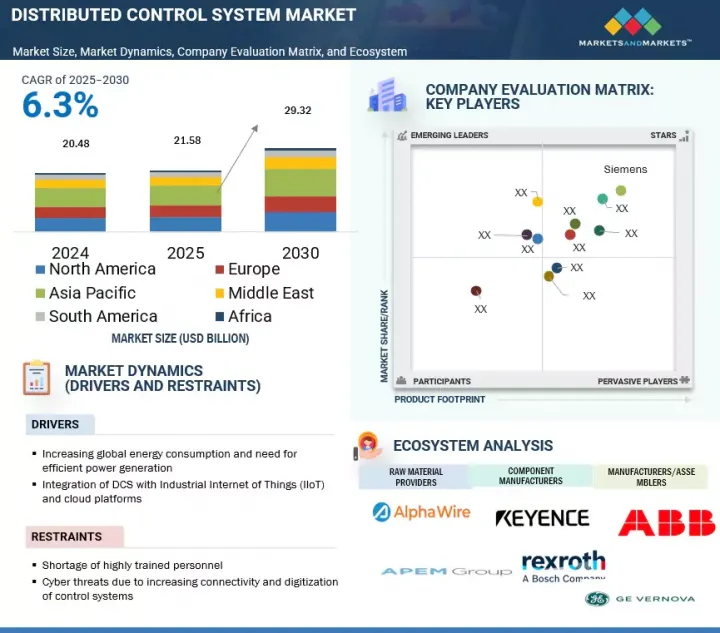

세계의 분산 제어 시스템 시장 규모는 2025년 215억 8,000만 달러에서 2030년에는 293억 2,000만 달러에 이르고, CAGR은 6.3%를 나타낼 전망입니다.

사물 인터넷(IoT), 인공 지능(AI), 클라우드 컴퓨팅, 고급 분석과의 통합 등 DCS의 혁신은 시스템의 기능을 향상시킵니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러)

부문별

분산 제어 시스템 시장 : 컴포넌트별, 용도별, 최종 용도 산업별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카

이러한 발전으로 예측 유지보수, 실시간 데이터 분석 및 의사 결정이 개선되어 DCS가 화학 및 발전과 같은 산업에 더욱 매력적인 솔루션이 되고 있습니다. 또 다른 주요 촉진 요인은 분산 제어 시스템의 운영 효율성입니다. 이 시스템은 공정 다운타임을 줄이고 유연성과 민첩성을 높입니다. 이로 인해 DCS 시스템은 복잡한 공정 산업에 적합한 옵션이 되었습니다.

프로세스 산업에서 정밀한 제어 및 운영의 우수성에 대한 요구가 증가함에 따라 고급 DCS 소프트웨어의 채택이 가속화되고 있습니다. 이러한 정교한 플랫폼은 실시간 통찰력을 제공하여 산업이 중요한 프로세스를 탁월한 정확도로 모니터링할 수 있도록 지원합니다. DCS 소프트웨어는 최신 데이터 분석 및 시각화 도구를 활용하여 복잡한 워크플로우를 최적화하고 비효율성을 최소화하며 의사 결정을 개선합니다. 이 기능은 실시간 정밀도가 가장 중요한 석유 및 가스, 발전, 고급 화학 산업과 같은 산업에 매우 중요합니다. DCS 소프트웨어에 실시간 모니터링 및 분석이 통합되어 사전 예방적인 공정 조정이 가능해지고, 다운타임이 감소하며, 운영 효율성이 향상되어 최근 산업 환경의 요구 사항을 충족할 수 있습니다.

DCS 솔루션은 확장성이 뛰어나 단일 컴퓨터 설정부터 대규모 다중 스테이션에 이르기까지 다양한 규모의 배치 지향 공정을 지원합니다. 이 기능은 저렴한 자동화 수단을 찾고 있는 중소기업과 우수한 통합 제어가 필수적인 대기업에 DCS를 특히 매력적인 솔루션으로 만듭니다. 모듈식 구조를 가진 최신 DCS를 사용하면 최소한의 인프라로 시작하여 생산 요구가 증가하거나 공정 요구 사항이 변경됨에 따라 점진적으로 확장할 수 있습니다. 이러한 유연성으로 인해 자원 활용도가 높아지고 초기 자본 비용이 감소하며, 소규모에서 대규모까지 다양한 배치 크기를 처리할 수 있습니다. 이는 제약, 식품 및 음료, 특수 화학 산업에 이상적인 솔루션입니다.

북미의 산업 및 에너지 부문, 특히 발전소와 정제소는 수십 년 전에 건설된 노후화된 인프라로 인해 도전 과제에 직면해 있습니다. 신뢰성, 효율성 및 안전성을 강화해야 하는 시급한 필요성으로 인해 현대화에 대한 상당한 투자가 촉진되고 있습니다. DCS는 이러한 변화에 핵심적인 역할을 하며, 첨단 자동화, 실시간 모니터링 및 정밀한 공정 제어를 원활하게 통합할 수 있게 해줍니다. 기존 시스템을 최첨단 DCS 솔루션으로 대체함으로써 산업은 운영을 최적화하고, 다운타임을 줄이며, 중요 자산의 수명을 연장하여 최신 성능 및 환경 기준을 준수할 수 있습니다. 이러한 요인들이 이 지역의 분산 제어 시스템 시장의 성장에 기여하고 있습니다.

본 보고서에서는 분산 제어 시스템 시장을 컴포넌트별(소프트웨어, 하드웨어, 서비스), 용도별(연속 프로세스, 배치식 프로세스), 최종 용도 산업별(석유 및 가스, 발전, 화학, 식품 및 음료, 의약품, 금속 및 광업, 펄프 및 제지, 수처리 및 폐수 처리, 기타), 지역별(북미(미국, 캐나다, 멕시코), 유럽(러시아, 독일, 이탈리아, 프랑스, 기타), 아시아태평양(인도, 일본, 한국, 중국, 기타), 중동(GCC 국가, 기타), 아프리카(아프리카, 브라질, 나이지역아, 기타), 남미(브라질, 아르헨티나, 베네수엘라, 기타)에서 정의, 기술, 예측했습니다. 비즈니스 개요, 솔루션, 서비스, 계약, 파트너십, 합의, 합병, 인수 등 주요 전략, 분산 제어 시스템 시장과 관련된 최근 동향에 대한 통찰력을 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

고객사업에 영향을 주는 동향/혼란

가격 분석

공급망 분석

생태계 분석

기술 분석

무역 분석

주된 회의 및 이벤트(2025-2026년)

규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

특허 분석

사례 연구 분석

투자 및 자금조달 시나리오

AI/생성형 AI가 분산 제어 시스템 시장에 미치는 영향

세계의 거시경제 전망

미국 관세가 분산 제어 시스템 시장에 미치는 영향(2025년)

제6장 분산 제어 시스템의 출하 규모

소개

대규모

중규모

소규모

제7장 분산 제어 시스템 시장(컴포넌트별)

소개

소프트웨어

하드웨어

서비스

제8장 분산 제어 시스템 시장(용도별)

소개

연속 프로세스

배치식 프로세스

제9장 분산 제어 시스템 시장(최종 이용 산업별)

소개

석유 및 가스

발전

화학

식품 및 음료

의약품

금속 및 광업

펄프 및 종이

물 및 폐수 처리

기타

제10장 분산 제어 시스템 시장(지역별)

소개

아시아태평양

중국

인도

한국

일본

기타

북미

미국

캐나다

멕시코

유럽

러시아

독일

영국

프랑스

이탈리아

기타

중동

GCC

기타

남미

베네수엘라

브라질

아르헨티나

기타

아프리카

남아프리카

알제리

나이지역아

기타

제11장 경쟁 구도

개요

주요 참가 기업의 전략/강점(2020-2025년)

시장 점유율 분석(2024년)

시장 평가 프레임워크

수익 분석(2020-2024년)

제품 비교

기업평가와 재무지표

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

SIEMENS

SCHNEIDER ELECTRIC

HONEYWELL INTERNATIONAL INC.

HITACHI, LTD.

GE VERNOVA

ABB

EMERSON ELECTRIC CO.

YOKOGAWA ELECTRIC CORPORATION

ROCKWELL AUTOMATION

VALMET

TOSHIBA CORPORATION

MITSUBISHI ELECTRIC CORPORATION

AZBIL CORPORATION

ANDRITZ

OMRON CORPORATION

기타 기업

CONCEPT SYSTEMS

ZAT AS

INGETEAM

WEG

ZHEJIANG CHITIC CONTROL ENGINEERING CO., LTD.

WATLOW ELECTRIC MANUFACTURING COMPANY

SCHWEITZER ENGINEERING LABORATORIES, INC.

SHANGHAI AUTOMATION INSTRUMENTATION CO., LTD.

HOLLYSYS GROUP BEIJING

MIKRODEV

제13장 부록

HBR

영문 목차

영문목차

The global distributed control system market is anticipated to reach USD 29.32 billion by 2030 from USD 21.58 billion in 2025, registering a CAGR of 6.3%. Innovations in DCS, such as integration with the Internet of Things (IoT), artificial intelligence (AI), cloud computing, and advanced analytics, enhance system capabilities.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD million)

Segments

Distributed Control System Market by shipment Scale, component, application, and end-use Industry

Regions covered

North America, Europe, Asia Pacific, South America, the Middle East, and Africa

These advancements enable predictive maintenance, real-time data analysis, and improved decision-making, making DCS more attractive to industries such as chemicals and power generation. Another key driving factor is the distributed control system's operational efficiency. It reduces process downtime and increases flexibility and agility. This has made the DCS system a feasible option for complex process industries.

"Software segment is expected to account for the largest market share in 2025."

The increasing need for precise control and operational excellence in process industries fuels the adoption of advanced DCS software. These sophisticated platforms deliver real-time insights, enabling industries to monitor critical processes with unparalleled accuracy. By leveraging cutting-edge data analytics and visualization tools, DCS software optimizes complex workflows, minimizes inefficiencies, and enhances decision-making. This capability is vital for industries such as oil & gas, power generation, ascended chemicals industries, where real-time precision is paramount. The integration of real-time monitoring and analytics in DCS software ensures proactive process adjustments, reduces downtime, and drives operational efficiency, meeting the demands of modern industrial environments.

"Batch-oriented process is anticipated to be the second fastest-growing segment during the forecast period."

DCS solutions are highly scalable and accommodate batch-oriented processes across a broad spectrum of scales, starting from a single computer setup to a large multi-station one. This feature makes DCS particularly attractive to small- and medium-sized manufacturers looking for cheaper means of automation, as well as large manufacturers with hard requirements for good integrated control. Being modular in nature, a modern DCS permits a business to start with minimal infrastructure, which they can incrementally grow as their production demands grow or change with their process needs. With such flexibility, there is an increased utilization of resources and less capital cost upfront, while handling batch sizes from small to very large. This makes it an ideal solution for pharmaceuticals, food & beverages, and specialty chemicals.

"North America is likely to account for the second-largest share of the distributed control system market ."

North America's industrial and energy sectors, particularly power plants and refineries, face challenges from outdated infrastructure, much of which was built decades ago. The urgent need to enhance reliability, efficiency, and safety drives substantial investments in modernization. DCS are pivotal in this transformation, enabling seamless integration of advanced automation, real-time monitoring, and precise process control. By replacing legacy systems with state-of-the-art DCS solutions, industries can optimize operations, reduce downtime, and extend the lifespan of critical assets, ensuring compliance with modern performance and environmental standards. These factors contribute to the growth of the distributed control system market in the region.

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 35%, Tier 2 - 40%, and Tier 3 - 25%

By Designation: C-Level Executives - 30%, Directors - 25%, and Others - 45%

By Region: North America - 35%, Europe - 18%, Asia Pacific - 20%, Middle East - 10%, Africa - 5%, and South America - 12%

Note: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million. Others include sales managers, engineers, and regional managers.

ABB. (Switzerland), Schneider Electric (France), Emerson Electric Co. (US), Siemens (Germany), Honeywell International Inc. (US), GE Vernova (US), Rockwell Automation (US), Yokogawa Electric Corporation (Japan), Valmet (Finland), TOSHIBA CORPORATION (Japan), Azbil Corporation (Japan), Hitachi, Ltd. (Japan), Mitsubishi Electric Corporation (Japan), OMRON Corporation (Japan), Hollysys Group Beijing (China), ANDRITZ (Austria), Concept Systems (US), ZAT a.s (Czech Republic), Ingeteam (Spain), Zhejiang Chitic Control Engineering Co., Ltd.(China), Watlow Electric Manufacturing Company (US), Schweitzer Engineering Laboratories, Inc. (US), WEG (Brazil), Shanghai Automation Instrumentation Co., Ltd. (South Korea), Mikrodev (Turkey) are key players in the distributed control system market. The study includes an in-depth competitive analysis of these key players in the distributed control system market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report defines, describes, and forecasts the distributed control system market market, by component (software, hardware, services), application (continuous process, batch-oriented process), end-use industry (oil & gas, power generation, chemicals, food & beverages, pharmaceuticals, metals & mining, pulp & paper, water & wastewater treatment, other industries), and region [North America (US, Canada, Mexico), Europe (Russia, Germany, Italy, France, Rest of Europe), Asia Pacific (India, Japan, South Korea, China, Rest of Asia Pacific), Middle East (GCC Countries, Rest of Middle East) Africa (South Africa, Algeria, Nigeria, Rest of Africa), and South America (Brazil, Argentina, Venezuela, Rest of South America)]. The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the distributed control system market. A thorough analysis of the key industry players has provided insights into their business overview, solutions, and services; key strategies such as contracts, partnerships, agreements, mergers, and acquisitions; and recent developments associated with the distributed control system market. This report covers the competitive analysis of upcoming startups in the distributed control system market ecosystem.

Key Benefits of Buying the Report

The report includes the analysis of key drivers (mounting investments to expand power generation capacity, increasing electricity generation using renewable energy sources, rising need for operational efficiency and process control), restraints (availability of low-cost alternatives, high costs and long timelines related to DCS certifications, cyber risks and high degree of redundancy), opportunities (mounting demand for distributed energy systems, rising development of integrated grid networks), and challenges (reliance on outdated, legacy equipment vulnerable to cyber threats, reduced oil production due to presence of alternative energy sources) influencing the growth of the distributed control system market.

Product Development/Innovation: EPC companies effectively use next-level project management, pre-fabrication, and combined design capabilities to increase efficiency and decrease complexity at the site. Innovations in the distributed control system sector include AI for scheduling, remote construction monitoring, and 3D modeling digital twins to enhance precision and reduce delays. The industry increasingly adopts low-carbon designs with carbon capture, renewable energy, and waste heat recovery. These trends help EPC contractors provide flexible, scalable, and energy-compliant distributed control system infrastructure while supporting global demand growth and decarbonization efforts.

Market Development: In January 2022, Valmet and Mercer International signed a long-term agreement to advance Mercer's global digital transformation programme. The agreement's execution began with the replacement of distributed control systems (DCS) with the Valmet DNA Automation System at the Mercer Peace River pulp mill in Alberta and the Mercer Celgar pulp mill in British Columbia, Canada.

Market Diversification: The report offers a comprehensive analysis of the strategies employed by EPC players to facilitate market diversification. It outlines innovative service and operating models and new partnership frameworks across various regions underpinned by technology-driven business lines. The findings emphasize opportunities for expansion beyond traditional operations, identifying geographical areas and customer segments that are currently served but remain underserved and are suitable for strategic entry.

Competitive Assessment: The report provides in-depth assessment of market shares, growth strategies, and service offerings of leading players, such as ABB (Switzerland), Schneider Electric (France), Emerson Electric Co. (US), Siemens (Germany), Honeywell International Inc. (US), GE Vernova (US), Rockwell Automation (US), Yokogawa Electric Corporation (Japan), Valmet (Finland), TOSHIBA CORPORATION (Japan), Azbil Corporation (Japan), Hitachi, Ltd. (Japan), Mitsubishi Electric Corporation (Japan), OMRON Corporation (Japan), Hollysys Group Beijing (China), among others, in the distributed control system market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants

2.1.2.2 Key data from primary sources

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of primaries

2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.3 DEMAND-SIDE ANALYSIS

2.3.3.1 Demand-side assumptions

2.3.3.2 Demand-side calculations

2.3.4 SUPPLY-SIDE ANALYSIS

2.3.4.1 Supply-side assumptions

2.3.4.2 Supply-side calculations

2.4 GROWTH PROJECTION

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DISTRIBUTED CONTROL SYSTEM MARKET

4.2 DISTRIBUTED CONTROL SYSTEM MARKET, BY COMPONENT

4.3 DISTRIBUTED CONTROL SYSTEM MARKET, BY END-USE INDUSTRY

4.4 DISTRIBUTED CONTROL SYSTEM MARKET, BY APPLICATION

4.5 DISTRIBUTED CONTROL SYSTEM MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Mounting investment to expand power generation capacity

5.2.1.2 Increasing electricity generation using renewable energy sources

5.2.1.3 Rising need for operational efficiency and process control

5.2.2 RESTRAINTS

5.2.2.1 Availability of low-cost alternatives

5.2.2.2 High costs and long timelines related to DCS certifications

5.2.2.3 Cyber risks and high degree of redundancy

5.2.3 OPPORTUNITIES

5.2.3.1 Mounting demand for distributed energy systems

5.2.3.2 Rising development of integrated grid networks

5.2.4 CHALLENGES

5.2.4.1 Reliance on outdated, legacy equipment vulnerable to cyber threats

5.2.4.2 Reduced oil production due to presence of alternative energy sources

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 PRICING RANGE OF DISTRIBUTED CONTROL SYSTEMS, BY SHIPMENT SCALE, 2024

5.4.2 AVERAGE SELLING PRICE TREND OF DISTRIBUTED CONTROL SYSTEMS, BY REGION, 2022-2024

5.5 SUPPLY CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Advanced process control (APC)

5.7.1.2 Industrial IoT (IIoT) and edge computing

5.7.2 COMPLEMENTARY TECHNOLOGIES

5.7.2.1 Supervisory control and data acquisition (SCADA)

5.7.2.2 Human-machine interface (HMI)

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Manufacturing execution systems (MES)

5.7.3.2 Asset performance management (APM)

5.8 TRADE ANALYSIS

5.8.1 IMPORT SCENARIO (HS CODE 903290)

5.8.2 EXPORT SCENARIO (HS CODE 903290)

5.9 KEY CONFERENCES AND EVENTS, 2025-2026

5.10 REGULATORY LANDSCAPE

5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10.2 REGULATIONS

5.11 PORTER'S FIVE FORCES ANALYSIS

5.11.1 THREAT OF NEW ENTRANTS

5.11.2 THREAT OF SUBSTITUTES

5.11.3 BARGAINING POWER OF SUPPLIERS

5.11.4 BARGAINING POWER OF BUYERS

5.11.5 INTENSITY OF COMPETITIVE RIVALRY

5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.12.2 BUYING CRITERIA

5.13 PATENT ANALYSIS

5.14 CASE STUDY ANALYSIS

5.14.1 MID-SIZED PROCESS PLANTS IMPLEMENT ABB'S FREELANCE DCS TO ENSURE PROCESS CONSISTENCY

5.14.2 FOOD AND BEVERAGE PLANT USES ROCKWELL AUTOMATION'S INTEGRATED CONTROL SOLUTIONS TO REDUCE WASTE AND ENHANCE PRODUCTION VISIBILITY

5.14.3 COLOMBIAN OIL AND GAS COMPANY ADOPTS ABB'S MODERN FREELANCE DCS PLATFORM TO REDUCE DOWNTIME AND BOOST CYBERSECURITY

5.15 INVESTMENT AND FUNDING SCENARIO

5.16 IMPACT OF AI/GEN AI ON DISTRIBUTED CONTROL SYSTEM MARKET

5.16.1 ADOPTION OF AI/GEN AI IN DCS APPLICATIONS

5.16.2 IMPACT OF AI/GEN AI IN DCS SUPPLY CHAIN, BY REGION

5.17 GLOBAL MACROECONOMIC OUTLOOK

5.17.1 INTRODUCTION

5.17.2 FOCUS ON LONG-TERM ENERGY SECURITY

5.17.3 TECHNOLOGICAL ADVANCEMENTS

5.17.4 FINANCING AND GOVERNMENT POLICY SUPPORT

5.17.5 HIGH CAPEX AMID INFLATION

5.18 IMPACT OF 2025 US TARIFF ON DISTRIBUTED CONTROL SYSTEM MARKET

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON COUNTRIES/REGIONS

5.18.4.1 US

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.5 IMPACT ON END-USE INDUSTRIES

6 SHIPMENT SCALES OF DISTRIBUTED CONTROL SYSTEMS

6.1 INTRODUCTION

6.2 LARGE-SCALE

6.3 MEDIUM-SCALE

6.4 SMALL-SCALE

7 DISTRIBUTED CONTROL SYSTEM MARKET, BY COMPONENT

7.1 INTRODUCTION

7.2 SOFTWARE

7.2.1 RISING DEPLOYMENT OF DCS IN CLOUD COMPUTING TO BOLSTER SEGMENTAL GROWTH

7.3 HARDWARE

7.3.1 INCREASING ADOPTION OF INDUSTRIAL AUTOMATION SOLUTIONS TO FUEL SEGMENTAL GROWTH

7.4 SERVICES

7.4.1 GROWING FOCUS ON OPERATIONAL EFFICIENCY DUE TO HIGH COMPLEXITY OF INDUSTRIAL PROCESSES TO DRIVE MARKET

8 DISTRIBUTED CONTROL SYSTEM MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 CONTINUOUS PROCESS

8.2.1 RAPID ADVANCES IN CLOUD-BASED SYSTEMS TO BOOST SEGMENTAL GROWTH

8.3 BATCH-ORIENTED PROCESS

8.3.1 TRACEABILITY AND PRECISE CONTROL THROUGH DCS INTEGRATION TO ACCELERATE SEGMENTAL GROWTH

9 DISTRIBUTED CONTROL SYSTEM MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 OIL & GAS

9.2.1 INCREASING COMPLEXITY AND HAZARDOUS NATURE OF OPERATIONS TO AUGMENT SEGMENTAL GROWTH

9.3 POWER GENERATION

9.3.1 RISING EMPHASIS ON ENSURING OPERATIONAL RELIABILITY, EFFICIENCY, AND REGULATORY COMPLIANCE TO SPUR DCS DEMAND

9.4 CHEMICALS

9.4.1 GROWING FOCUS ON SAFEGUARDING AGAINST EXPLOSIVE SUBSTANCES TO CONTRIBUTE TO SEGMENTAL GROWTH

9.5 FOOD & BEVERAGES

9.5.1 MOUNTING DEMAND FOR HIGH-QUALITY, SAFE, AND TRACEABLE PRODUCTS TO BOLSTER SEGMENTAL GROWTH

9.6 PHARMACEUTICALS

9.6.1 GROWING NEED TO ENHANCE PRODUCTIVITY AND REDUCE OPERATIONAL COSTS TO FOSTER SEGMENTAL GROWTH

9.7 METALS & MINING

9.7.1 INCREASING INVESTMENT IN ADVANCED AUTOMATION SOLUTIONS TO EXPEDITE SEGMENTAL GROWTH

9.8 PULP & PAPER

9.8.1 RISING NEED TO MANAGE NUMEROUS INTERCONNECTED CONTROL LOOPS TO ACCELERATE SEGMENTAL GROWTH

9.9 WATER & WASTEWATER TREATMENT

9.9.1 RAPID URBANIZATION AND POPULATION GROWTH TO DRIVE MARKET

9.10 OTHER INDUSTRIES

10 DISTRIBUTED CONTROL SYSTEM MARKET, BY REGION

10.1 INTRODUCTION

10.2 ASIA PACIFIC

10.2.1 CHINA

10.2.1.1 Mounting adoption of renewable energy to achieve decarbonization targets to drive market

10.2.2 INDIA

10.2.2.1 Increasing investment in grid modernization and clean energy capacity projects to fuel market growth

10.2.3 SOUTH KOREA

10.2.3.1 Rapid industrialization and infrastructure development to bolster market growth

10.2.4 JAPAN

10.2.4.1 Growing focus on advancing power infrastructure to augment market growth

10.2.5 REST OF ASIA PACIFIC

10.3 NORTH AMERICA

10.3.1 US

10.3.1.1 Increasing allocation of funds to ensure grid resilience to foster market growth

10.3.2 CANADA

10.3.2.1 Rising need for resilient grid operations to contribute to market growth

10.3.3 MEXICO

10.3.3.1 Rapid modernization of transmission systems to boost market growth

10.4 EUROPE

10.4.1 RUSSIA

10.4.1.1 Rising deployment of automation tools to improve operational efficiency to drive market

10.4.2 GERMANY

10.4.2.1 Increasing use of DCS solutions in smart factories to bolster market growth

10.4.3 UK

10.4.3.1 Growing reliance on automated process control and remote monitoring platforms to drive market

10.4.4 FRANCE

10.4.4.1 Growing emphasis on smart grid infrastructure development to fuel market growth

10.4.5 ITALY

10.4.5.1 Increasing investment in high-voltage networks to augment market growth

10.4.6 REST OF EUROPE

10.5 MIDDLE EAST

10.5.1 GCC

10.5.1.1 Qatar

10.5.1.1.1 Escalating adoption of digital control and automation systems to accelerate market growth

10.5.1.2 UAE

10.5.1.2.1 Strong focus on automation, safety, and real-time monitoring to bolster market growth

10.5.1.3 Saudi Arabia

10.5.1.3.1 Growing emphasis on industrial automation and energy diversification to drive market

10.5.1.4 REST OF GCC

10.5.2 REST OF MIDDLE EAST

10.6 SOUTH AMERICA

10.6.1 VENEZUELA

10.6.1.1 Rising efforts to rebuild water, refining, and petrochemical infrastructure to augment market growth

10.6.2 BRAZIL

10.6.2.1 Mounting adoption of automation systems to strengthen energy security to contribute to market growth

10.6.3 ARGENTINA

10.6.3.1 Growing need for industrial automation and stable energy infrastructure to drive market

10.6.4 REST OF SOUTH AMERICA

10.7 AFRICA

10.7.1 SOUTH AFRICA

10.7.1.1 Rapid industrialization and shortage of skilled labor to augment market growth

10.7.2 ALGERIA

10.7.2.1 Increasing focus on solar energy, grid modernization, and digital utility management to fuel market growth

10.7.3 NIGERIA

10.7.3.1 Growing concern about power outages and transmission inefficiencies to accelerate market growth

10.7.4 REST OF AFRICA

11 COMPETITIVE LANDSCAPE

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2025

11.3 MARKET SHARE ANALYSIS, 2024

11.4 MARKET EVALUATION FRAMEWORK

11.5 REVENUE ANALYSIS, 2020-2024

11.6 PRODUCT COMPARISON

11.7 COMPANY VALUATION AND FINANCIAL METRICS

11.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.8.1 STARS

11.8.2 EMERGING LEADERS

11.8.3 PERVASIVE PLAYERS

11.8.4 PARTICIPANTS

11.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.8.5.1 Company footprint

11.8.5.2 Region footprint

11.8.5.3 Component footprint

11.8.5.4 Application footprint

11.8.5.5 End-use industry footprint

11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024