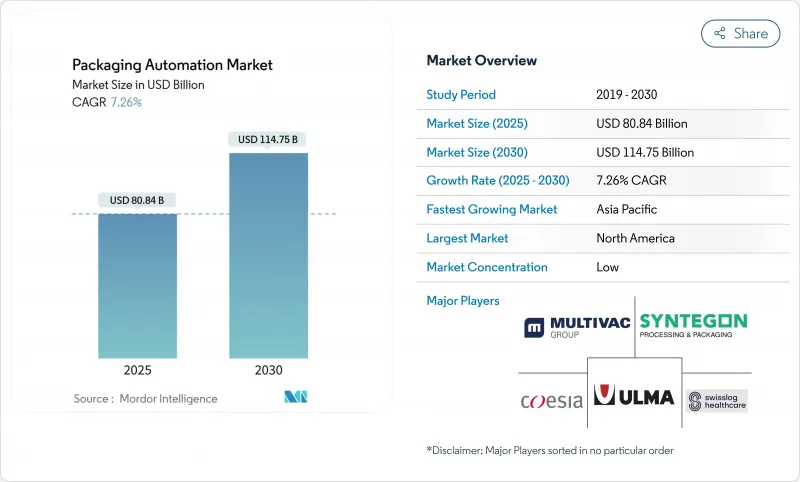

포장 자동화 시장 규모는 2025년 808억 4,000만 달러, 2030년 1,147억 5,000만 달러에 이르고, CAGR은 7.26%를 나타낼 전망입니다.

지능형 제조 시스템에 대한 지속적인 투자로 노동력 격차가 줄어들고 라인 정확도가 향상되고 규제에 대한 기대가 높아지고 있습니다. 이 분야는 전자상거래에 의한 생산량의 성장과 엄격한 의약품의 직렬화에 의해 이익을 얻고 있으며, 라인은 처리량과 추적성의 균형을 잡아야 합니다. 북미가 리더십을 유지하고 있지만 아시아태평양은 중국의 수십억 달러 규모의 로봇 투자에 힘입어 가장 급속히 확대되고 있습니다. 매출은 여전히 하드웨어가 지배적이지만, 사용자가 소유권보다 가동 시간의 보증을 요구하게 되어, 서비스 중심의 성과주의 모델이 가속하고 있습니다. 골판지, 종이 기구, 자재관리의 각 공급업체의 통합은 고객의 실적를 확장하고 자동화 공급자에게 새로운 규모를 만들어 냅니다.

포장기계의 출하량은 2024년에 상승하여 대량 생산되는 식품업무에 더해 유연한 소량생산 형식을 요구하는 제약라인에 의해 뒷받침됩니다. 제약 제조업체는 개별화된 의약품 포장을 허용하기 위해 2025년에 1,600억 달러를 사이트 업그레이드에 투입합니다. E-Commerce 풀필먼트 센터는 수천 개의 상자의 변이를 만들어내는 라이트 사이징 시스템을 채택하여 노동 생산성을 높이면서 골판지 사용량을 반감시킵니다. 한 섹터에서 입증된 솔루션이 다른 섹터로 전환되고 포장 자동화 시장 침투가 가속됨에 따라 업계를 가로지르는 기술 이전이 가속화됩니다. 이러한 기운이 함께, 한정된 다운타임으로 SKU 클래스간을 시프트할 수 있는 적응형 로봇과 통합 비전에 대한 수요가 증폭됩니다.

모바일 로봇과 결합된 적절한 크기의 박스 시스템은 수개월 내에 물류 현장의 생산성을 97% 향상시켜 2차 포장이 얼마나 중요한 효율화 레버가 되었는지를 명확히 했습니다. 가변 치수 오토메이션은 현재 포장 자동화 시장의 41.42%를 차지하며, 이는 혼합 주문을 신속하게 처리할 필요성을 반영합니다. 아시아태평양의 온라인 소매 매출은 급증하고 있으며, 2024년에는 지역 설비 투자액이 180억 달러로 확대될 것으로 예측됩니다. 서양의 옴니채널 모델과 함께 라인 속도, 소프트웨어 오케스트레이션, 인체공학을 기반으로 하는 팔레타이징에 지속적인 압력이 걸려 포장 자동화 시장 전체의 지속적인 업그레이드를 자극하고 있습니다.

본격적인 패키징 셀에는 많은 양의 선행 투자가 필요하며, 많은 중소기업들은 이것을 엄청난 것으로 느낍니다. 동시에 커넥티비티의 향상으로 운영 기술이 사이버 위협에 노출되어 제조업은 산업 사고의 1/4 이상을 차지하고 있습니다. 기업은 자동화 하드웨어와 계층화된 보안 모두에 투자해야 하며 예산이 늘어나고 도입이 늦어지고 있습니다. Robots-as-a-Service 모델은 OPEX로 지출을 이동하고 구독 내에서 관리되는 사이버 보안을 제공함으로써 이 두 가지 장애물을 해결합니다. 이 접근법은 밸런스 시트에 미치는 영향을 줄이지만 포장 자동화 시장 전반에 걸쳐 확장하려면 여전히 시장 교육이 필요합니다.

2024년 포장 자동화 시장 점유율은 케이스 포장이 32.12%를 차지했고 유통 시 상품 보호에 필수적인 역할을 담당하고 있는 것으로 밝혀졌습니다. 지속가능성이 더 얇은 골판지와 정밀한 접착제 도포를 뒷받침하고 있기 때문에 케이스 부문내의 성장은 안정되어 있습니다. 팔레타이징은 매출이 작고 CAGR 12.31%로 확대되고 있습니다. Fanak의 새로운 CRX-25iA 코봇은 30kg의 하중을 다룰 수 있으며 쉽게 티칭 펜던트를 제공하면서 셀 풋 프린트를 압축합니다. 협동작용 로봇은 시운전을 단축하고 작업자의 인체공학을 개선하기 때문에 이 부문은 자동화 보급의 선행 지표가 됩니다.

업스트림에서 유연한 무균 형식이 개인화 치료를 지원하기 때문에 충전 기계가 의약품에 대한 투자를 받고 있습니다. 라벨링 라인은 의약품 및 음료의 규제 추적성을 충족하는 직렬화 모듈을 추가합니다. 랩핑과 캡핑은 경량 필름의 진보를 배경으로 증가했으며, 밴딩 기술은 테스트 도입으로 플라스틱을 80% 줄였습니다. 가방 포장 라인은 내구성이 강한 할록스강으로 수명을 연장한 연마재 분야에서 각광을 받고 있습니다. 이러한 제품 간의 상호작용은 여러 작업을 융합하여 적응성이 있는 포장 자동화 시장 솔루션이 되는 엔드 투 엔드 셀로의 움직임을 시사합니다.

식품 제조업체는 2024년 포장 자동화 시장의 28.53%를 차지했고 대량 SKU와 엄격한 위생 기준의 혜택을 누리고 있습니다. 의약품 포장은 그 기준선은 작은 것, 주사 요법 증가에 따라 11.98%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다. Syntegon의 Pharmatag 2025 라인은 엄격한 무균 상태에서 액체를 채우는 반면, 작은 로트에도 대응할 수 있도록 포맷을 빠르게 전환합니다. 아시아태평양의 음료 라인은 중간층 수요 증가에 대응하기 위해 고속 통조림과 슬리빙을 설치합니다.

퍼스널케어 브랜드는 자동화된 멀티라인 오더 픽킹을 통해 럭셔리한 커스텀 팩에 주력하고 있습니다. 화학제품 제조업체는 부식성 매체에 대한 노출을 제한하기 위해 페스트의 EX 인증 액추에이터를 활용한 밀폐 충전 및 밀봉을 채택하고 있습니다. 의약품의 직렬화가 위조품 대책으로서 소비재로 이행하고, 포장 자동화 시장의 응용 범위가 넓어짐에 따라 기술의 크로스 오버가 가속화되고 있습니다.

북미는 2024년 포장 자동화 시장에 34.14%의 점유율을 차지했습니다. 고급 제조 인프라와 FDA의 직렬화 의무화를 활용하고 있습니다. 의약품 제조업체는 2025년 1,600억 달러를 투자하여 장비를 업그레이드하고 클린룸 대응 로봇 수요를 유지할 것입니다. ABB의 미시간에서 2,000만 달러의 확장은 공급업체가 지역 고객에게 헌신하고 있다는 점을 강조합니다. 전자상거래의 처리 허브가 급증하고 적응성이 높은 2차 포장 수요가 증폭되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.64%로 가장 빠른 성장 지역일 것입니다. 중국은 2024년 산업용 로봇에 66억 달러를 투입해 로봇 밀도를 두배로 늘리는 정책을 반영했습니다. 상하이에서 개최되는 ProPak 2025에는 스마트 패키징 솔루션의 출전자가 2,500개 이상 모여 이 지역의 수작업 라인에서 디지털 공장으로의 이동을 강조합니다. Estun Automation과 같은 국내 공급업체는 경쟁력 있는 가격의 로봇 팔로 점유율을 얻어 현지에서 포장 자동화 시장을 확대하고 있습니다.

유럽에서는 지속가능성에 대한 규제와 인더스트리 4.0 보조금을 통해 도입을 추진하고 있습니다. 스웨덴이 있는 시설에서는 자동 밴딩을 통해 플라스틱 랩을 80% 절감하여 순환형 경제의 목표를 달성했습니다. 독일의 선진 기계 제조업체가 수출 경쟁력을 유지하기 위해 AI 모듈을 추가. 또한 중동 및 아프리카에서는 식량 안보를 강화하기 위해 자동화된 유제품 라인을 시험적으로 도입하고, 브라질 남미 공장에서는 지역 음료 수요 증가에 대응하기 위해 팔레타이저를 도입하고 있습니다. 이러한 다양한 이니셔티브로 세계 포장 자동화 시장의 밑단이 확산되고 있습니다.

The packaging automation market size is valued at USD 80.84 billion in 2025 and is forecast to reach USD 114.75 billion by 2030, registering a 7.26% CAGR.

Continued investment in intelligent manufacturing systems is narrowing labor gaps, lifting line precision, and meeting rising regulatory expectations. The sector benefits from e-commerce volume growth that overlaps with stringent pharmaceutical serialization, forcing lines to balance throughput with traceability. North America retains leadership, yet Asia-Pacific delivers the fastest expansion, supported by China's multi-billion-dollar robotics outlays. Hardware still dominates revenue, but service-centric, outcome-based models accelerate as users seek guaranteed uptime rather than ownership. Consolidation across corrugated, folding carton, and material handling suppliers is enlarging customer footprints and creating fresh scale for automation providers.

Packaging machinery shipments climbed in 2024, propelled by pharmaceutical lines that demand flexible, small-batch formats beside high-volume food operations. Pharmaceutical manufacturers are committing USD 160 billion to site upgrades in 2025 to enable personalized medicine packaging. E-commerce fulfillment centers adopt right-sizing systems generating thousands of box variations, halving corrugate use while boosting labor productivity. Cross-industry technology transfer quickens as solutions proven in one sector migrate to another, accelerating packaging automation market penetration. The combined momentum amplifies demand for adaptive robotics and integrated vision that can shift between SKU classes with limited downtime.

Right-sized box systems coupled with mobile robots lifted a distribution site's productivity by 97% within months, underscoring how secondary packaging has become the pivotal efficiency lever. Variable-dimension automation now comprises 41.42% of the packaging automation market, reflecting the need to process mixed orders at speed. Asia-Pacific's surging online retail sales are projected to escalate regional equipment outlays to USD 18 billion in 2024. Coupled with omnichannel models in Europe and North America, the shift places sustained pressure on line speeds, software orchestration, and ergonomic palletizing, stimulating continuous upgrades across the packaging automation market.

Full-scale packaging cells require significant upfront cash that many SMEs find prohibitive. Simultaneously, rising connectivity exposes operational technology to cyber threats, with manufacturing representing over one quarter of industrial incidents. Firms must invest in both automation hardware and layered security, stretching budgets and slowing adoption. Robots-as-a-Service models address this dual hurdle by shifting spending to OPEX and providing managed cybersecurity within the subscription. The approach lessens balance-sheet impact, yet market education is still needed before it scales across the packaging automation market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Case packaging accounted for 32.12% of packaging automation market share in 2024, underscoring its essential role in safeguarding goods during distribution. Growth within the case segment remains steady as sustainability pushes thinner corrugate and precision glue application. Palletizing, though smaller in revenue, is expanding at 12.31% CAGR. FANUC's new CRX-25iA cobot, able to handle 30 kg loads, compresses cell footprints while offering easy teach pendants. Collaborative robots shorten commissioning and improve worker ergonomics, making the segment a leading indicator of wider automation uptake.

Upstream, filling machines win pharmaceutical investment as flexible aseptic formats accommodate personalized therapies. Labeling lines add serialization modules that satisfy regulatory traceability in medicine and beverages. Wrapping and capping rise on the back of lightweight film advances, with banding technology reducing plastic by 80% in pilot deployments. Bagging lines gain footing in abrasive material sectors where ruggedized Hardox steel prolongs service life. The interplay among these products signals a move toward end-to-end cells that fuse multiple tasks into an adaptive packaging automation market solution.

Food manufacturers held 28.53% of the packaging automation market in 2024, benefiting from high-volume SKUs and rigid hygiene standards. Despite its smaller baseline, pharmaceutical packaging is poised for 11.98% CAGR as injectable therapies rise. Syntegon's Pharmatag 2025 line fills liquids under strict sterility while switching formats quickly to handle short runs. Beverage lines in Asia-Pacific install high-speed canning and sleeving to satisfy rising middle-class demand.

Personal-care brands focus on luxurious, custom packs enabled by automated multi-line order picking. Chemical producers adopt enclosed filling and sealing to limit exposure to aggressive media, leveraging Festo's EX-certified actuators. Technology crossover accelerates as pharma serialization migrates into consumer goods to combat counterfeits, broadening application scope for the packaging automation market.

The Packaging Automation Market Report is Segmented by Product Type (Filling, Labeling, Case Packaging, and More), End-User (Food, Beverage, Pharmaceuticals, and More), Automation Level (Fully-Automated Lines, Semi-Automated Lines, Collaborative/Hybrid Systems), Solution (Hardware, and More), Packaging Stage (Primary, Secondary, Tertiary/End-of-Line), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 34.14% to the packaging automation market in 2024, leveraging sophisticated manufacturing infrastructure and FDA serialization mandates. Drug makers will spend USD 160 billion on facility upgrades during 2025, sustaining demand for clean-room ready robots. ABB's USD 20 million expansion in Michigan underscores vendor commitment to regional customers. E-commerce fulfillment hubs proliferate, amplifying calls for adaptive secondary packaging.

Asia-Pacific is the fastest region at 10.64% CAGR through 2030. China spent USD 6.6 billion on industrial robots in 2024, reflecting policy ambitions to double robot density. Shanghai's ProPak 2025 will gather more than 2,500 exhibitors in smart packaging solutions, highlighting the region's shift from manual lines to digital factories. Domestic suppliers such as Estun Automation are winning share with competitively priced robotic arms, expanding the packaging automation market locally.

Europe drives adoption through sustainability regulation and Industry 4.0 grants. A Swedish facility cut plastic wrap by 80% via automated banding, satisfying circular-economy goals. Germany's advanced machine builders add AI modules to retain export competitiveness. Elsewhere, Middle East and Africa pilot automated dairy lines to bolster food security, while South American plants in Brazil install palletizers to serve growing regional beverage demand. These diverse initiatives collectively extend the global packaging automation market footprint.