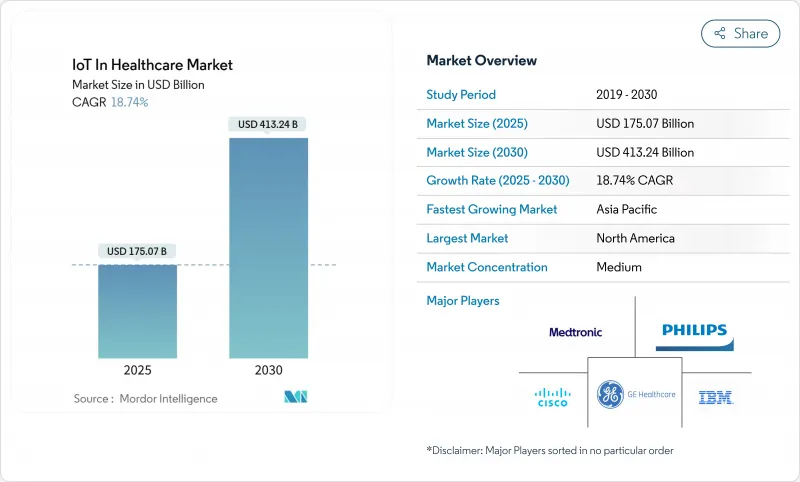

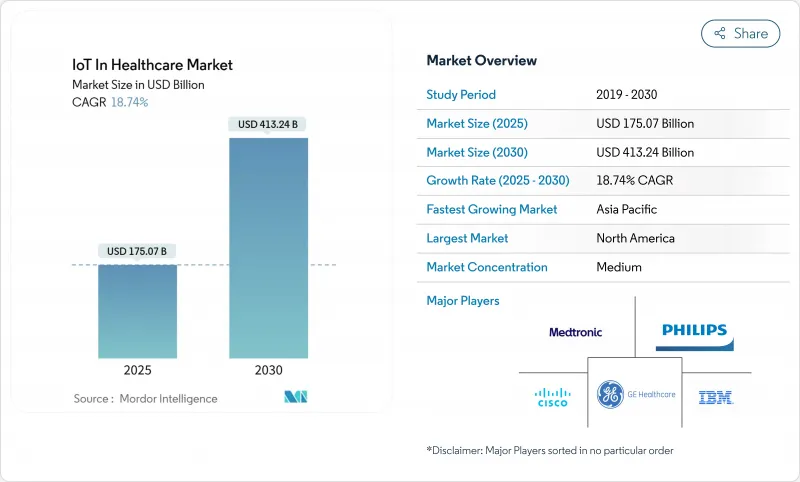

헬스케어 분야 IoT 시장의 2025년 시장 규모는 1,750억 7,000만 달러로 추정되고, 2030년에는 4,132억 4,000만 달러에 이를 것으로 예측되며, CAGR 18.74%로 성장할 전망입니다.

급속한 진보는 진료 보상의 근대화, 성숙해지고 있는 5G 캠퍼스 네트워크, 중단 없는 환자 모니터링에 대한 팬데믹 후의 기대로부터 발생합니다. 이러한 힘이 결합되어 연결 장치는 선택적 부가 기능이 아닌 필수 헬스케어 인프라로 자리매김되어 의료 제공업체를 지속적인 참여와 데이터 중심의 개입으로 향하게 합니다. 투자의 기세는 도입 시간을 90% 단축한 사설망의 전개 및 임상의가 침대 옆에서 투여 전에 가상적으로 약제 프로토콜을 테스트할 수 있는 디지털 트윈 시뮬레이션에 의해 더욱 유지되고 있습니다. 이러한 변화는 데이터 유동성, 에지 분석, 디바이스 상호 운용성을 향한 자본의 지속적인 재분배를 시사하며, 헬스케어 분야 IoT 시장 기회를 확대하고 있습니다.

iRhythm사의 Zio AT는 2024년에 98% 환자의 어드히어런스를 기록하여 라이프 스타일을 무너뜨리지 않고 지속적인 심장 원격 측정이 가능함을 보여주었습니다. 같은 해 Dexcom의 시판되는 Stelo 포도당 모니터가 FDA의 인가를 받아 규제된 바이오센서에 대한 소비자의 접근이 확대되었습니다. 클라우드에 연결된 애널리틱스는 이러한 스트림을 실시간 알림으로 변환하여 응급 응시 및 재입원을 줄입니다. Movano의 Evie Ring과 같은 특수 폼 팩터는 충분한 서비스를 받지 못한 레이어를 대상으로 하며 새로운 세분화의 역학을 시사합니다. 장치의 다양성이 높아짐에 따라 헬스케어 분야 IoT 시장은 만성 질환 관리 및 예방적 스크리닝의 사용자 풀을 증가시킵니다.

세계 반도체의 과잉 생산 능력 및 소형화의 진전으로 단가 인하가 계속되고, 병원은 예산 1달러당 더 많은 엔드포인트에 접속할 수 있게 됩니다. 5G 및 LPWAN 인프라의 분산은 신뢰성을 향상시키면서 데이터 전송 오버헤드를 줄여줍니다. 엣지 지원 칩셋은 로컬에서 신호를 처리하므로 클라우드의 점화 요금 및 대기 시간이 저하됩니다. 전력 효율이 뛰어난 센서에 대한 자동차 분야의 투자는 의료 설계에도 파급되어 웨어러블 패치의 배터리 수명이 연장됩니다. IEEE P2413을 기반으로 한 상호 운용성 표준은 멀티 벤더 통합을 간소화하고 프로젝트 리드 타임을 단축하며 자금 제약이 있는 공급자에게 헬스케어 분야 IoT 시장의 매력을 강화합니다.

HIPAA의 갱신안에서는 다 요소 인증, 정지 시의 암호화, AI를 활용한 정보 유출의 억제가 의무지어져, 초년도의 컴플라이언스 예산은 93억 달러에 이를 것으로 추산되고 있습니다. EU 공급자는 GDPR(EU 개인정보보호규정)과 AI 법을 양립시켜 조달 사이클을 연장합니다. 헬스케어는 1건당 1,010만 달러로 여전히 정보 유출의 가장 비싼 업계이며 CIO의 신중한 행동을 촉구하고 있습니다. 블록체인의 시험 운용은 불변의 감사 추적을 약속하지만 에너지 사용량에 우려를 줍니다. 보안 벤더가 상승을 기대하는 한편, 타성은 헬스케어 분야 IoT 시장의 확대 속도를 억제하고 있습니다.

2024년 매출의 46%를 서비스가 차지했습니다. 이는 ROI를 인출하기 위해 병원이 컨설팅, 통합 및 수명 주기 지원에 의존하고 있음을 반영합니다. 시스템과 소프트웨어는 AI와 클라우드 네이티브 스택이 새로운 디바이스 구축의 기준이 되기 때문에 CAGR 19.7%를 보일 것으로 예측됩니다. 메드트로닉은 연구 개발에 27억 달러를 투자하고 구독 수익을 촉진하는 분석 레이어를 통합했습니다. Philips는 이미 130만 대의 IoT 엔드포인트를 AWS에서 오케스트레이션하고 있으며 컴퓨팅 비용을 36% 절감하고 있습니다. 따라서 헬스케어 분야 IoT 시장은 단발 하드웨어 판매보다 플랫폼 중심주의에 기울고 있습니다.

엣지 애널리틱스, 사이버 보안 미들웨어, 예측 유지보수 대시보드는 신규 지출 요구의 대부분을 차지합니다. 병원은 장비 임대와 실시간 분석, 24시간 365일 서비스 데스크를 번들한 결과 기반 계약을 협상합니다. 엔드 투 엔드 오케스트레이션을 자랑하는 벤더는 조직이 여러 공급업체의 패치워크에서 벗어나면서 더 높은 월렛 점유율을 얻습니다. 2030년까지 서비스 소계는 절대 금액으로 하드웨어를 능가할 것으로 예상되며, 헬스케어 분야 IoT 시장 전체의 고수익 프로파일을 지원합니다.

원격 의료는 2024년 기본 이용 사례로 29.3%의 점유율을 유지했는데, 노동력 부족 및 처리량 압력을 배경으로 자산과 직원 추적이 CAGR 21.3%로 상승할 전망입니다. 사설 5G와 초광대역 태그는 침대 수준의 지오펜싱을 지원하여 ICU 복도에서 인공호흡기 검색 시간을 단축합니다. 예측 유지 보수 일정은 장비의 가동 시간과 감사 규정 준수를 향상시킵니다. 이러한 운영 승리는 추적 프로젝트를 더 광범위한 헬스케어 분야 IoT 시장에 신속하게 투자 회수하는 게이트웨이로 간주하는 CFO를 유혹합니다.

입원 환자 모니터링은 AI 트리어지 엔진에 원격 측정을 제공하는 5G 게이트웨이를 사용합니다. 투약 관리 키오스크는 실시간으로 복약 준수를 기록하여 부작용을 억제합니다. 화상 처리 장치는 에지 가속기를 도입하여 CT 스캔을 즉시 렌더링하여 방사선 기사의 소요 시간을 단축합니다. 응급 대응 팀은 병원 명령 센터에 연결된 지오태그가 있는 공황 버튼을 사용하여 문에서 바늘까지 시간을 몇 분 단축합니다. 이러한 워크플로우는 수익원을 다양화하고 의료 산업에서 IoT의 침투를 깊게 합니다.

헬스케어 분야 IoT 시장 보고서는 컴포넌트별(의료기기, 시스템 및 소프트웨어, 기타), 용도별(원격의료, 환자 모니터링, 기타), 최종 사용자별(병원 및 진료소, 재택치료 및 환자, 기타), 연결 기술별(Bluetooth Low Energy(BLE), Wi-Fi, 셀룰러 및 5G, 기타), 전개 모드별(클라우드 및 온프레미스, 엣지)로 구분됩니다.

북미는 2024년에 42.2%의 매출을 유지했으며, 메디케어의 원격 모니터링 CPT 코드 상설과 FDA에 의한 웨어러블 진단의 패스트 트랙 환경에 의해 강화되는 EHR의 강력한 보급이 디바이스와 플랫폼의 통합을 용이하게 해, 벤처 캐피탈의 활동이 신흥 기업에 스케일링 연료를 공급합니다. 각 주 메디케이드 프로그램은 연방 정부의 상환을 점점 모방하고 대응 가능한 인구를 확대하고 있습니다. 그 결과, 헬스케어 분야 IoT 시장은 미국과 캐나다에서 예측 가능한 수요 곡선을 즐길 수 있습니다.

유럽에서는 상호 운용성 프로젝트에 8억 1,000만 유로를 할당하는 유럽 의료 데이터 공간(European Health Data Space) 아래 꾸준한 성장을 기록했습니다. 독일 병원 개혁법은 전자 의료 기록을 의무화하고 미들웨어 업그레이드를 촉진했습니다. EU 배터리 규칙 2023/1542는 설계 복잡성을 높이지만 지속가능성 의무에 부합합니다. 동시에, AI 방법은 알고리즘의 투명성 규칙을 명확히하고, 임상의의 신뢰를 조성합니다. 이러한 협조적인 정책으로 유럽은 품질 주도형이면서 컴플라이언스를 중시하는 헬스케어 분야 IoT 시장의 일각을 차지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 23.25%로 가장 빠르게 성장할 전망입니다. 일본의 의료 DX 이니셔티브는 국가 ID 카드와 보험 데이터베이스를 연결하여 IoT 데이터 흐름을 간소화합니다. 중국에서는 100개 이상의 스마트 병원이 5G 캠퍼스 그리드를 활용하여 엔드 투 엔드 환자 추적을 실시했습니다. 인도의 Ayuschman Barat Digital Mission은 미래의 장치 통합을 위한 기본 ID를 발행합니다. 스마트폰의 높은 보급률 및 경쟁력 있는 통신 요금 설정이 가정용 모니터링 키트를 뒷받침해, 헬스케어 분야 IoT 시장의 저변은 대도시 이외에도 퍼지고 있습니다. 남미와 중동 및 아프리카는 이제 막 시작되었지만, 광대역 격차가 축소되면 비약적인 보급이 예상됩니다.

The IoT in healthcare market is valued at USD 175.07 billion in 2025 and is projected to reach USD 413.24 billion by 2030, advancing at an 18.74% CAGR.

Rapid progress stems from reimbursement modernization, maturing 5G campus networks, and a post-pandemic expectation for uninterrupted patient oversight. Combined, these forces position connected devices as indispensable healthcare infrastructure rather than optional add-ons, pushing providers toward continuous engagement and data-driven interventions. Investment momentum is further sustained by private network deployments that cut implementation time by 90% and by digital-twin simulations that allow clinicians to test drug protocols virtually before bedside administration. Together, these shifts signal a durable reallocation of capital toward data liquidity, edge analytics, and device interoperability that enlarges the IoT in healthcare market opportunity horizon.

Medical-grade wearables have shifted from fitness novelties to clinically validated diagnostics. iRhythm's Zio AT logged 98% patient adherence in 2024, showing that continuous cardiac telemetry is feasible without lifestyle disruption. FDA clearance of Dexcom's over-the-counter Stelo glucose monitor in the same year widens consumer access to regulated biosensors.Cloud-linked analytics convert these streams into real-time alerts, cutting emergency visits and readmissions. Specialized form factors such as Movano's Evie Ring target underserved cohorts, signaling new segmentation dynamics. As device diversity grows, the IoT in healthcare market gains incremental user pools across chronic-disease management and preventive screening.

Global semiconductor overcapacity and miniaturization advances continue to pull unit prices down, allowing hospitals to connect more endpoints per budget dollar. The dispersion of 5G and LPWAN infrastructure trims data-transmission overheads while improving reliability. Edge-ready chipsets now process signals locally, lowering cloud egress fees and latency. Automotive-sector investments in power-efficient sensors spill over into medical designs, extending battery life on wearable patches. Interoperability standards under IEEE P2413 streamline multi-vendor integration, shrinking project lead-times and reinforcing the attractiveness of the IoT in healthcare market for cash-constrained providers.

Proposed HIPAA updates mandate multi-factor authentication, encryption at rest, and AI-driven breach containment, adding an estimated USD 9.3 billion to first-year compliance budgets. EU providers juggle GDPR with the AI Act, extending procurement cycles. Healthcare remains the most expensive industry for breaches at USD 10.1 million per incident, driving cautious CIO behavior. Blockchain pilots promise immutable audit trails but raise energy-use worries. While security vendors see upside, inertia tempers expansion speed of the IoT in healthcare market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services accounted for 46% of 2024 revenue, reflecting hospitals' reliance on consulting, integration, and lifecycle support to unlock ROI. Systems and Software is forecast to grow at 19.7% CAGR as AI and cloud-native stacks become the baseline for new device introductions. Medtronic invested USD 2.7 billion in R&D to embed analytics layers that drive subscription revenue. Philips already orchestrates 1.3 million IoT endpoints on AWS, lowering compute spend by 36%. The IoT in healthcare market, therefore, tilts toward platform centricity rather than one-off hardware sales.

Edge analytics, cyber-secured middleware, and predictive-maintenance dashboards dominate fresh spending requests. Hospitals negotiate outcome-based contracts that bundle device leasing with real-time analytics and 24/7 service desks. Vendors that master end-to-end orchestration capture higher wallet share as organizations phase out multi-supplier patchworks. By 2030, the services subtotal is projected to eclipse hardware in absolute dollars, anchoring a high-recurring-revenue profile across the IoT in healthcare market.

Tele-medicine retained a 29.3% share in 2024 as the foundational use-case, yet Asset and Staff Tracking is climbing at 21.3% CAGR on the back of workforce shortages and throughput pressures. Private 5G and ultra-wideband tags support bed-level geofencing, cutting search times for ventilators in ICU corridors. Predictive maintenance schedules improve equipment uptime and audit compliance. These operational wins entice CFOs who view tracking projects as quick payback gateways into the broader IoT in healthcare market.

In-patient monitoring embraces 5G gateways that feed telemetry into AI triage engines. Medication-management kiosks register dose adherence in real time, curbing adverse events. Imaging suites deploy edge accelerators to render CT scans instantly, slashing radiologist turnaround. Emergency response teams use geotagged panic buttons linked to hospital command centers, shaving minutes off door-to-needle times. Collectively, these workflows diversify revenue streams and deepen penetration of the IoT in the healthcare industry.

The IoT in Healthcare Market Report is Segmented by Component (Medical Devices, Systems and Software, and More), Application (Tele-Medicine, In-Patient Monitoring, and More), End-User (Hospitals and Clinics, Home-Care / Patients, and More), Connectivity Technology (Bluetooth Low Energy (BLE), Wi-Fi, Cellular and 5G, and More), Deployment Model (Cloud and On-Premise / Edge), and Geography.

North America retained 42.2% revenue in 2024, fortified by Medicare's permanent remote-monitoring CPT codes and an FDA fast-track environment for wearable diagnostics Strong EHR penetration eases device-platform integration, while venture-capital activity supplies scaling fuel for startups. State Medicaid programs increasingly replicate federal reimbursement, expanding addressable populations. As a result, the IoT in healthcare market enjoys predictable demand curves across the United States and Canada.

Europe posted steady growth under the European Health Data Space, which allocates EUR 810 million to interoperability projects. Germany's hospital reform law mandates electronic patient records, propelling middleware upgrades. The EU Battery Regulation 2023/1542 raises design complexity but aligns with sustainability mandates. Simultaneously, the AI Act clarifies algorithmic transparency rules, fostering clinician trust. These coordinated policies position Europe as a quality-driven yet compliant slice of the IoT in healthcare market.

Asia-Pacific is the fastest climber at 23.25% CAGR to 2030. Japan's Medical DX initiative links national ID cards to insurance databases, streamlining IoT-data flow. In China, more than 100 smart hospitals leverage 5G campus grids for end-to-end patient tracking. India's Ayushman Bharat Digital Mission seeds foundational IDs for future device integration. High smartphone penetration and competitive telecom pricing encourage household monitoring kits, expanding the IoT in healthcare market footprint well beyond megacities. South America and the Middle East and Africa are nascent but primed for leapfrog adoption once broadband gaps narrow.