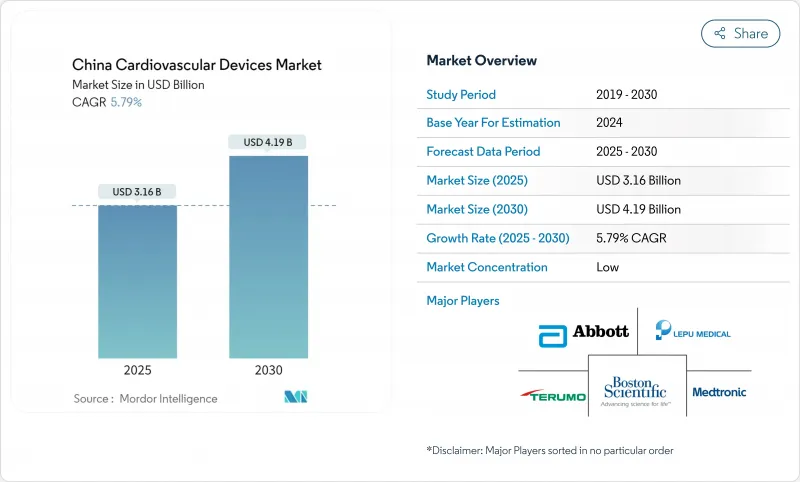

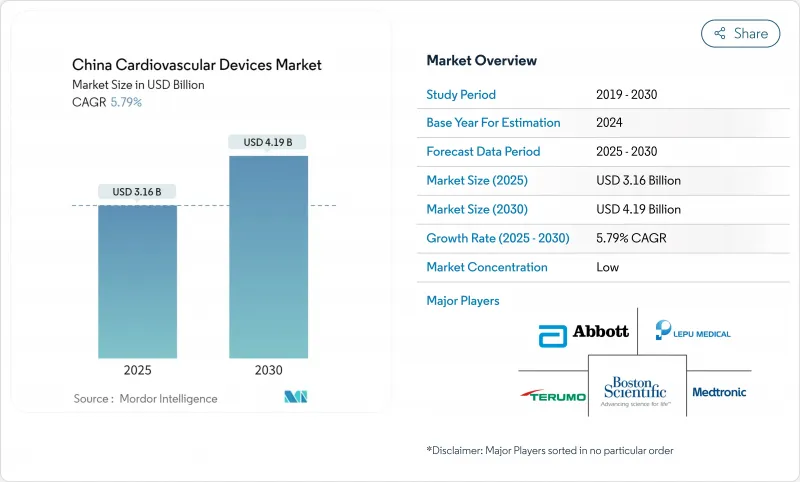

중국의 심혈관 장비 시장 규모는 2025년 31억 6,000만 달러, 2030년에는 41억 9,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 5.79%로 예상됩니다.

평균 수명이 늘어나고 3억 3천만 명으로 추정되는 심혈관 환자인 'Healthy China 2030'의 정책적 기울기로 인하여 수술 건수는 계속 증가하고 있으며, 인터벤션 기술과 모니터링 기술이 모두 도입되고 있습니다. 관상동맥 스텐트의 수량 기준 조달(VBP)에 가장자리를 둔 가격 압축은 95%의 가격 하락을 일으켰지만 전체 스텐트의 사용률은 10% 가까이 상승하고 비용 개혁이 어떻게 장치의 보급을 촉진하는지를 이야기하고 있습니다. 국내 제조업체는 2025년까지 중고급 심장혈관 기기의 70%의 국산화를 목표로 하는 'Made in China 2025'에도 추진되어, 이러한 개혁에 승진하고 있습니다. 동시에 중국에서는 흉부 통증 센터의 네트워크가 확대되어 도어 투 벌룬 시간의 중앙값이 117.7분에서 46.9분으로 단축되어 진보된 영상 진단, 가이드와이어, 긴급 모니터링에 대한 수요에 힘쓰고 있습니다.

흉부 통증 센터의 전국 전개에 의해 도어 투 벌룬 시간이 46.9분까지 단축되어, 고성능 가이드와이어, 약제 용출 스텐트, 혈관내 이미징 시스템의 보급이 가속하고 있습니다. 인공지능 트리아지의 통합으로 90분 이내의 1차 PCI 시행률은 24.47%에서 60.41%로 상승했으며, 연결된 ECG 플랫폼은 30일 사망률을 4.14%에서 2.73%로 감소시켰습니다. 중국 심장혈관 학회(China Cardiovascular Association)에 의해 유지되는 국가 기준은 성과 지표를 공표하고 있기 때문에 현 수준의 병원은 임상 효율을 나타내는 기기를 향해 제품의 선택을 표준화하도록 촉구되고 있습니다. 이 표준화는 조달 예측 가능성을 높이고 증거 기반 프로토콜을 따르는 국내 혁신자에 대한 입찰 시간을 단축합니다. 이 프로그램이 중부 및 서부 지방으로 확장됨에 따라 경쟁력 있는 가격 설정과 입증된 임상 결과를 양립하는 장비 제조업체는 중국의 심혈관 장비 시장에서 판매량을 늘릴 수 있습니다.

미드 및 하이엔드의 심혈관 기기의 70%를 국내에서 공급한다는 산업 정책의 목표에 의해 자본은 연구 파이프라인에 제공되어, 현지의 대기업은 매출의 11-14%를 연구 개발에 충당하고 있어, 이것은 세계의 의료 기술의 평균을 크게 웃돌고 있습니다. 그 결과 관상 동맥 분기 스텐트, 펄스 자기장 절제 시스템, 자기 부상 펌프 등 국가 의료 제품 관리국(NMPA)의 혁신 채널을 클리어한 제품이 출시되었습니다. 복잡한 심장 판막 분야에서는 여전히 외국 브랜드가 우위를 차지하고 있지만, 중국의 진출기업은 현재 많은 전달 시스템이나 폴리머 코팅 기술로 세계의 동업 타사와 어깨를 나란히 하고, 지방의 입찰에서의 조달은 현지에 등록된 SKU로 이동하고 있습니다. 업계 이해관계자들은 현지화의 추진이 2027년까지 말초 혈관과 전기생리학의 틈새 분야에도 침투하여 중국의 심혈관 기기 시장의 국산 솔루션에 대한 구조적 경사가 강해질 것으로 예상하고 있습니다.

스텐트에서 페이스메이커, 제세동기, 밸브에 이르기까지 VBP의 연장이 잇따랐고, 3년간 2,600억 위안이 절약되었지만, 프리미엄 라인의 평균 판매 가격과 총이익률은 하락했습니다. 다국적 기업은 마진 유지와 점유율 유지 사이에서 보다 엄격한 트레이드오프에 직면하고 있으며, 국내 기업은 하단 라인을 보호하기 위해 스케일 메리트에 의존하고 있습니다. 판매량 증가는 수익을 끌어올리지만 단기적인 영향은 톱 라인의 성장에 부정적이며 중국의 심혈관 기기 시장 전체의 CAGR을 감속시킵니다.

2024년 중국 심혈관 기기 시장의 68.20%는 치료 및 수술용 디바이스가 차지했으며, 주요 시설에서 연간 2,200건의 관동맥 인터벤션과 VBP에 의한 대수 증가가 기여했습니다. NMPA가 2025년 2월에 MicroPort Sorin의 새로운 페이싱 리드를 승인함에 따라 심장 리듬 관리의 틈새가 가속화되어 밀폐 씰과 리드 코일 야금의 지역 발전이 부각되었습니다. 혈관내 결석 파쇄술, 신제신경술, 차세대 약제 코팅 풍선이 새로운 조류를 형성하고 있으며, 국산화에 의해 수입품보다 저비용화가 진행되고 있습니다. 예측기간 동안 국내 혁신자들은 중간 정도의 복잡성을 지닌 임플란트에서 해외의 기존 기업을 계속 구축할 것으로 예상되며, 중국의 심혈관 장비 시장에서 이 범주의 우위성이 강화됩니다.

진단 및 모니터링 장비는 2030년까지 연평균 복합 성장률(CAGR) 6.98%로 확대될 것으로 예측됩니다. 스마트 웨어러블에 통합된 AI 대응 ECG 분석이 조기 발견을 가정에 가져오는 반면, 병원의 흉부 통증 네트워크는 트리아지 최적화를 위해 높은 처리량의 CT 스캐너와 MRI 스캐너를 계속 구입하고 있습니다. 현지 시약 제조업체가 지원하는 심장 바이오마커 측정은 신속한 제외 프로토콜을 지원하며 3억 3,000만 명의 환자 수영장에 기여합니다. 클라우드 네이티브 데이터 플랫폼은 NMPA의 사이버 보안 지침 개정을 지원하고 공급업체가 software-as-medical-device 모듈의 신속한 승인을 보장하는 데 도움이 됩니다. 가정에서의 만성 질환 관리가 증가함에 따라 커넥티드 다이아그노스틱스는 순수한 인터벤션 SKU로부터 점유율을 계속 빼앗아 중국의 심혈관 장비 시장 규모에 두께를 더할 것으로 보입니다.

The China cardiovascular devices market size stands at USD 3.16 billion in 2025 and is forecast to reach USD 4.19 billion by 2030, advancing at a 5.79% CAGR over the period.

Rising life expectancy, an estimated 330 million cardiovascular patients, and the policy tilt of "Healthy China 2030" continue to lift procedure volumes and the uptake of both interventional and monitoring technologies . Price compression sparked by volume-based procurement (VBP) on coronary stents triggered a 95% price fall yet lifted overall stent usage by nearly 10%, illustrating how cost reform can amplify device penetration. Domestic producers are capitalising on these reforms, aided by "Made in China 2025," which targets 70% local production of mid- to high-end cardiovascular equipment by 2025 . Simultaneously, China's expanding chest-pain-center network has cut median door-to-balloon times from 117.7 minutes to 46.9 minutes, adding momentum to advanced imaging, guidewire, and emergency monitoring demand.

The national roll-out of chest-pain centers has shortened door-to-balloon intervals to as low as 46.9 minutes, driving stronger uptake of high-performance guidewires, drug-eluting stents, and intravascular imaging systems . Integration of artificial-intelligence triage further lifted primary PCI rates within 90 minutes from 24.47% to 60.41% and pushed connected ECG platforms that cut 30-day mortality from 4.14% to 2.73% . National standards maintained by the Chinese Cardiovascular Association make performance metrics public, prompting county-level hospitals to standardise product choices toward devices demonstrating clinical efficiency. This standardisation increases procurement predictability and compresses time-to-tender for domestic innovators aligned with evidence-based protocols. As the program expands into central and western provinces, device makers that couple competitive pricing with proven clinical outcomes are positioned to capture incremental volumes within the China cardiovascular devices market.

The industrial policy goal of 70% domestic supply for mid- to high-end cardiovascular equipment has redirected capital into research pipelines, with leading local firms dedicating 11-14% of sales to R&D, well above the global med-tech average. Resulting product launches span coronary bifurcation stents, pulsed-field ablation systems, and magnetic levitation pumps, all cleared through the National Medical Products Administration's (NMPA) innovation channel. While foreign brands still dominate complex heart-valve segments, Chinese entrants now match global peers in many delivery-system and polymer-coating technologies, shifting procurement in provincial tenders toward locally registered SKUs. Industry stakeholders expect the localisation push to permeate peripheral vascular and electrophysiology niches by 2027, reinforcing the structural tilt of the China cardiovascular devices market toward home-grown solutions.

Successive VBP extensions from stents to pacemakers, defibrillators, and valves have saved CNY 260 billion across three years but crimped average selling prices and gross profit margins for premium lines. Multinationals face tougher trade-offs between margin retention and share maintenance, while domestic firms rely on scale economics to protect bottom lines. Although higher volumes cushion revenue, the short-run impact is negative for top-line growth, moderating the overall China cardiovascular devices market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Therapeutic and Surgical Devices contributed 68.20% of the China cardiovascular devices market in 2024, buoyed by 2,200 annual coronary interventions at leading centers and VBP-induced volume surges. The cardiac-rhythm-management niche accelerated after NMPA cleared MicroPort Sorin's new pacing lead in February 2025, underscoring local progress in hermetic sealing and lead-coil metallurgy. Intravascular lithotripsy, renal denervation, and next-gen drug-coated balloons form the emerging wave, with localisation tipping cost-of-goods lower than imports. Over the forecast period, domestic innovators are expected to keep displacing foreign incumbents across mid-complexity implants, reinforcing the primacy of this category within the China cardiovascular devices market.

Diagnostic and Monitoring Devices are projected to expand at a 6.98% CAGR through 2030. AI-enabled ECG analytics integrated into smart wearables bring early detection into homes, while hospital chest-pain networks still buy high-throughput CT and MRI scanners for triage optimisation. Cardiac-biomarker assays backed by local reagent makers support rapid rule-out protocols, serving the 330 million strong patient pool . Cloud-native data platforms align with the NMPA's revised cybersecurity guidance, helping vendors secure faster approval for software-as-medical-device modules. Given rising chronic-disease management at home, connected diagnostics should keep edging wallet share away from purely interventional SKUs, adding depth to the China cardiovascular devices market size.

The China Cardiovascular Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Therapeutic & Surgical Devices), Application (Coronary Artery Disease, Arrhythmia & Conduction Disorders, Heart Failure & Cardiomyopathy, and More), End-User (Hospitals & Cardiac Centres, Ambulatory Surgical Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).