ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

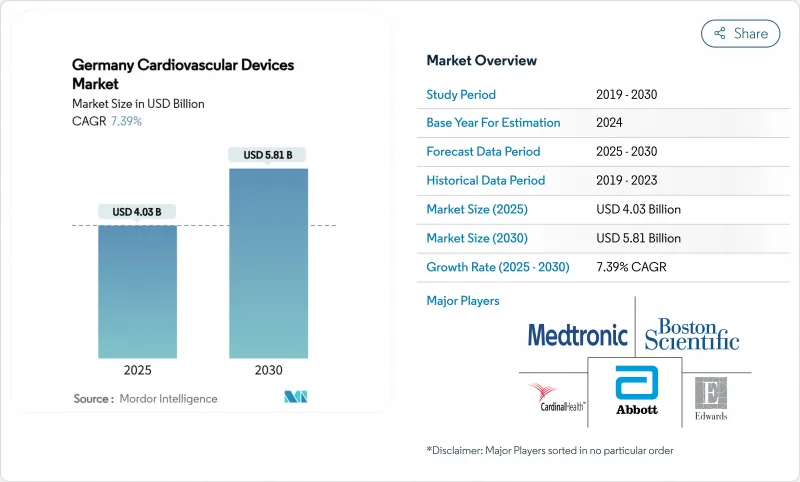

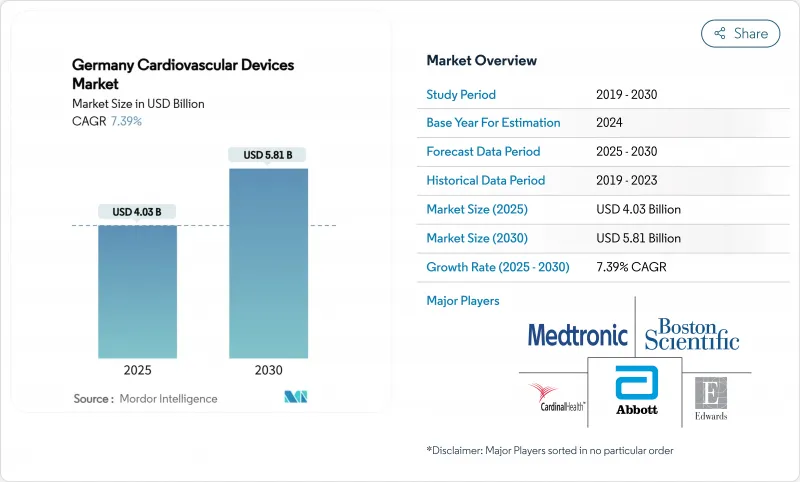

독일의 심혈관 기기 시장 규모는 2024년 37억 6,000만 달러, CAGR 7.39%로 성장하여 2030년에는 58억 1,000만 달러에 이를 것으로 예측됩니다.

수술 건수 증가, 인구의 고령화, 원격 모니터링 의무의 확대가 장기적인 수요를 지원하고 있습니다. DRG 지불은 보존 요법보다 카테터 기반 개입을 선호하기 때문에 병원은 심장 구조와 리듬 관리 시스템에 계속 투자하고 있습니다. 동시에 만성 심부전 환자의 원격 모니터링이 의무화됨에 따라 이식형 루프 레코더와 클라우드 분석에 경상 수익이 생겨 독일의 심혈관 기기 시장은 데이터 주도의 서비스 분야로 변모합니다. EU-MDR의 컴플라이언스 비용이 많은 저수익 SKU를 제거하고 혁신을 AI 대응 진단, 저침습 시스템, 입원 기간을 단축하는 완전 이식형 펌프로 이동시킵니다. 약리학적 진보는 조기 질환에서 장비의 보급을 억제하지만, 독일의 초고령화 인구 역학은 교체 및 업그레이드 사이클을 활발하게 만들어 2030년까지 예측 가능한 한 자리 대 중반의 수익 궤도를 유지합니다.

독일 심혈관 기기 시장 동향과 통찰

보험 적용되는 심혈관 절차의 급속한 확대

독일의 DRG 시스템은 인터벤션 치료를 실시하는 병원에 보답하는 것으로, 경 카테터 대동맥 판막 이식의 수기 건수는 누적 10만 건을 넘고 있습니다. 카테터 검사실은 외과 수술실로 대체를 계속하고 있으며, 변막증 수술과 TAVI 간의 진료 보수의 동등성에 의해 자본 설비의 투자 회수 기간이 단축되고 있습니다. 80대 환자의 95%가 TAVI를 받고 있는 현재 장비 제조업체는 밸브에 색전 방지 필터를 번들하여 평균 판매 가격을 인상하는 동시에 병원이 뇌졸중 감소의 품질 지표를 충족하도록 돕고 있습니다.

심부전 원격 모니터링의 의무화

2023년부터 법정보험사는 만성 심부전 환자의 원격 텔레메트리를 다루어야 하며 이식형 루프 레코더와 비침습적 혈행동태센서의 채택 의욕을 높이고 있습니다. 대학 센터는 지속적인 데이터 피드를 분석하고 조기 외래 개입을 유도하는 명령 허브를 설립하고 재입원을 줄이고 입원 침대를 해제합니다. 공급업체는 하드웨어, 분석 대시보드 및 진료 보상 코딩 지원을 통합한 구독 패키지를 제공하여 병원이 에피소드 후속 작업에서 항상 모니터링 워크플로로 마이그레이션하도록 권장합니다.

EU-MDR 시판 후 비용

2021 MDR은 증거 역치를 끌어올려 집중적인 시판 후 조사를 도입했기 때문에 일부 소규모 기업에서는 재인증 비용이 최대 300% 상승했습니다. EU 전반에 걸쳐 50만대의 장비를 평가할 수 있는 노티파이드 바디가 43개밖에 없기 때문에 인증 대기열은 2026년까지 계속됩니다. 독일의 중소기업 중 상당수는 새로운 시험에 자금을 제공하는 것보다 소량의 카테터를 폐기하고 구매를 선도적 다국적 기업에 집계하고 틈새 응용 제품의 유형을 줄입니다.

부문 분석

치료 및 수술용 디바이스는 인구 100만명당 164건의 TAVI 사례가 뒷받침해 2024년 독일의 심혈관 기기 시장 점유율 69.20%를 획득했습니다. 약물 용출성 스텐트, 좌심방 액세서리 폐색 장치 및 보조 인공 심장에 대한 의존성 증가는 집중 치료실 입주 기간을 단축하는 저침습 솔루션에 대한 병원의 선호를 뒷받침합니다. 경피적 관상동맥 인터벤션의 성숙에도 불구하고, 석회화 병변과 같은 고위험 서브세트는 새로운 OPS 코드로 상환되는 결석 파쇄 카테터에 대한 수요를 유지하고 있습니다.

진단 및 모니터링 장비는 규모가 작고 AI를 활용한 ECG 분석 및 심부전 원격 모니터링의 의무화에 의해 뒷받침되며 2030년까지 연평균 복합 성장률(CAGR) 6.33%로 성장할 전망입니다.

독일의 심혈관 기기 시장 보고서는 업계를 기기 유형별(진단·감시 기기(심전도(ECG), 원격 심장 모니터링, 기타 진단·감시 기기), 치료·수술 기기(심장 보조 장치, 심박 관리 장치, 카테터, 그래프트, 심장 밸브, 스텐트, 기타 치료·수술 기기))로 분류하고 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 도입

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

시장 개요

시장 성장 촉진요인

보험 적용된 TAVI 및 TMVR 절차의 급속한 확대가 경 카테터 심장 밸브 수요를 뒷받침

원격 심부전 원격 모니터링의 의무화(G-BA 2022)가 이식형 루프 레코더의 보급을 가속

독일의 국민 1인당 PCI 건수는 EU에서 최고 DES와 가이드와이어 교환 사이클 유지

남부 및 동부주의 초고령화 인구 동태가 심박 조율기 및 보조 인공 심장의 이식 건수를 견인

연구개발세제 우대조치와 MDR 이행이 국내 이노베이터를 지원(BIOTRONIK 등)

Krankenhaus-Zukunft법에 의한 디지털 ICU/OR혈행동태 모니터링 시스템에의 자금 원조

시장 성장 억제요인

EU-MDR 시판 후 비용으로 인해 중소기업이 기존 심혈관 SKU를 철수해야 하는 상황

대학 센터를 넘어 심실 보조 장치 임플란트 채택을 억제하는 DRG 예산 한도

밸류베이스 조달이 스텐트와 풍선의 가격 하락을 촉진

약물 요법의 진보(SGLT2i 등)에 의한 디바이스 치료량의 조정

가치/공급망 분석

규제 전망

기술적 전망

Five Forces 분석

신규 참가업체의 위협

공급기업의 협상력

구매자의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

진단 및 모니터링 장비

심전도 시스템

원격 심장 모니터

심장 MRI

심장 CT

심 에코/초음파 검사

분획 혈류 예비능(FFR) 시스템

치료 및 수술용 기기

관상동맥 스텐트

약제 용출 스텐트

베어 메탈 스텐트

생체 흡수성 스텐트

카테터

PTCA 풍선 카테터

IVUS/OCT 카테터

심장 리듬 관리

페이스메이커

이식형 제세동기

심장 재동기 치료 장비

심장 벨브

TAVR/TAVI

기계식 밸브

조직/생체 인공 밸브

보조 인공 심장

인공 심장

그래프트 & 패치

기타 심장혈관 외과용 기기

용도별

관상동맥질환

부정맥

심부전

심장 구조 질환

고혈압증

기타

최종 사용자별

병원

재택치료

기타

제6장 경쟁 구도

시장 집중도

시장 점유율 분석

기업 프로파일

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

BIOTRONIK SE & Co. KG

B. Braun Melsungen AG

Edwards Lifesciences Corp.

Siemens Healthineers AG

GE HealthCare Technologies Inc.

Philips Healthcare

Terumo Corp.

LivaNova PLC

Getinge AB(Maquet Cardiopulmonary)

Zoll Medical Corp.

Schiller AG

Dragerwerk AG & Co. KGaA

Straub Medical AG

Lepu Medical Technology

CardioFocus Inc.

MicroPort Scientific Corp.

WL Gore & Associates Inc.

제7장 시장 기회와 전망

SHW

영문 목차

영문목차

The Germany cardiovascular devices market size is USD 3.76 billion in 2024 and is forecast to expand at a 7.39% CAGR to reach USD 5.81 billion by 2030.

Higher procedure volumes, an aging population, and expanding remote-monitoring mandates anchor long-term demand. Hospitals continue to invest in structural-heart and rhythm-management systems as DRG payments favor catheter-based interventions over conservative therapy. At the same time, mandatory telemonitoring of chronic heart-failure patients generates recurring revenue for implantable loop recorders and cloud analytics, turning the Germany cardiovascular devices market into a data-driven services arena. EU-MDR compliance costs eliminate many low-margin SKUs, shifting innovation toward AI-enabled diagnostics, minimally invasive systems, and fully implantable pumps that shorten inpatient stays. Although pharmacological advances temper device uptake in early-stage disease, Germany's super-aged demographic keeps replacement and upgrade cycles brisk, sustaining a predictable mid-single-digit revenue trajectory through 2030.

Germany Cardiovascular Devices Market Trends and Insights

Rapid Expansion of Reimbursed Cardiovascular Procedures

Germany's DRG system rewards hospitals for interventional care, lifting procedure counts for transcatheter aortic valve implantation beyond 100,000 cumulative cases. Catheter laboratories continue to replace surgical suites, and reimbursement parity between valve surgery and TAVI compresses payback periods for capital equipment. As 95% of octogenarian patients now receive TAVI, device makers bundle valves with embolic-protection filters to enlarge average selling prices while helping hospitals meet stroke-reduction quality metrics

Mandatory Remote Heart-Failure Telemonitoring

Since 2023, statutory insurers must cover remote telemetry for chronic heart-failure patients, motivating adoption of implantable loop recorders and non-invasive hemodynamic sensors. University centers have established command hubs that analyze continuous data feeds and trigger early outpatient interventions, cutting readmissions and freeing inpatient beds. Vendors offer subscription packages that integrate hardware, analytics dashboards, and reimbursement coding support, encouraging hospitals to migrate from episodic follow-up to always-on monitoring workflows.

EU-MDR Post-Market Costs

The 2021 MDR raised evidence thresholds and introduced intensive post-market surveillance, raising recertification costs by up to 300% for some small firms. With only 43 notified bodies to assess 500,000 devices EU-wide, certification queues stretch into 2026. Many German SMEs drop low-volume catheters rather than fund new trials, consolidating purchasing toward large multinationals and reducing product variety for niche applications.

Other drivers and restraints analyzed in the detailed report include:

Krankenhaus-Zukunft Act Spurs Digital ICU/OR Hemodynamic-Monitoring Upgrades

Pharmacotherapy Advances Moderating Device Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic and Surgical Devices captured 69.20% Germany cardiovascular devices market share in 2024, boosted by 164 TAVI cases per million residents. Growing reliance on drug-eluting stents, left-atrial appendage occluders, and VADs underscores hospitals' preference for minimally invasive solutions that shorten intensive-care occupancy. Despite the maturity of percutaneous coronary intervention, high-risk subsets such as calcified lesions sustain demand for lithotripsy catheters reimbursed under new OPS codes.

Diagnostic and Monitoring Devices, although smaller, will expand at 6.33% CAGR to 2030, buoyed by AI-driven ECG analytics and mandatory heart-failure telemonitoring.

The Germany Cardiovascular Devices Market Report Segments the Industry Into by Device Type (Diagnostic and Monitoring Devices [Electrocardiogram (ECG), Remote Cardiac Monitoring, Other Diagnostic and Monitoring Devices], Therapeutic and Surgical Devices [Cardiac Assist Devices, Cardiac Rhythm Management Device, Catheter, Grafts, Heart Valves, Stents, Other Therapeutic and Surgical Devices]).