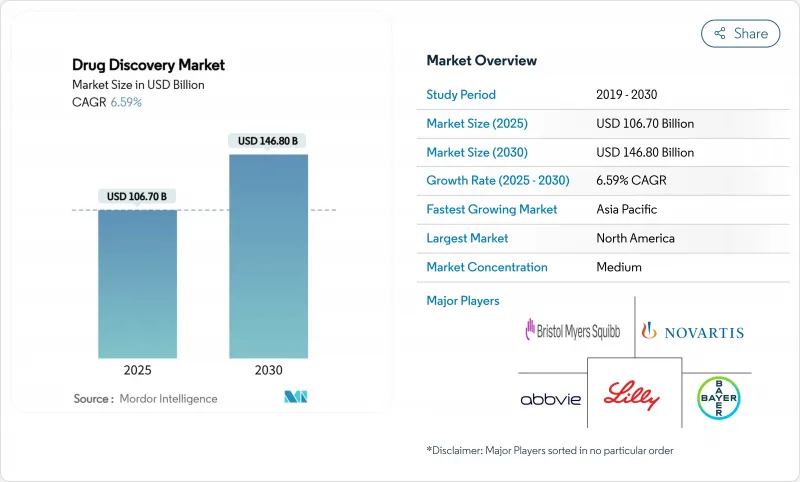

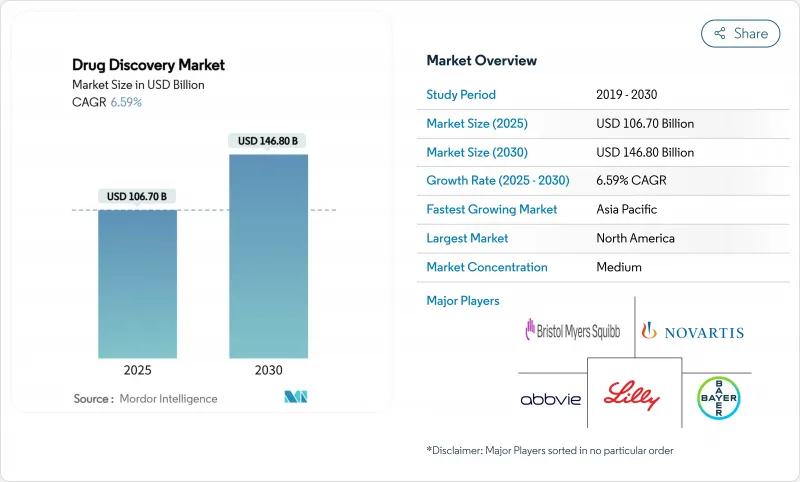

세계의 Drug Discovery 시장 규모는 2025년에 1,067억 달러로 추정되고, 2030년에는 1,468억 달러에 이를 전망이며, CAGR 6.59%로 확대될 것으로 예측됩니다.

성장을 뒷받침하고 있는 것은 만성질환의 만연률 상승, 연구개발비의 지속적인 증가, 탐색 워크플로우 전체에서 인공지능의 도입이 가속되고 있다는 것입니다. 주요 제약 회사는 후기 단계에 있는 의약품에 자원을 돌리기 위해 바이오테크놀러지 기업은 기동적인 사업 모델을 활용하여 신규 치료법의 개발에 임하고 있습니다. 인공지능은 후보 화합물의 동정 기간을 수년에서 수개월로 단축하고 전임상 비용을 절감함으로써 중견기업의 폭넓은 진입을 촉진하고 있습니다. Precision Medicine은 표적 요법 및 희귀질환 프로그램에 대한 투자를 조타하고 규제 당국의 지원 이니셔티브는 미충족 요구의 높은 적응증을 위한 빠른 패스웨이를 정교하게 하고 있습니다.

만성질환 및 희귀질환은 프로그램의 우선 순위를 재정의하고 있으며, 높은 미충족 요구 및 상업적 가능성에서 암 영역에서만 활성 프로젝트의 41%를 모으고 있습니다. 신경과학의 파이프라인도 기업이 알츠하이머병, 본태성 진전 및 기타 쇠약성 질환에 대한 치료법을 추구함에 따라 확대되고 있습니다. 이 동향은 희소질환에도 미치고 있습니다. 2024년에 승인된 신규 세포 및 유전자 치료제의 88%가 희소질환용 의약품의 지정을 받고 있으며, 유전학적으로 정의된 소규모 집단으로 축족을 옮기는 것으로 밝혀졌습니다. 희귀 질병 연구에 대한 투자는 정교한 바이오마커 전략을 추진하고, 표적 검증을 개선하며, 조기 개발 위험을 완화합니다. 이러한 역학은 첨단 Drug Discovery 플랫폼에 대한 수요를 높이고 전문적인 자본을 끌어들여 Drug Discovery 시장의 장기적인 성장을 가속합니다.

29개의 블록버스터 의약품이 출시된 후, 세계의 연구개발 수익은 2024년에는 5.9%로 상승했으며, 기업은 시장에 대한 길이 명확한 후기 단계의 자산에 자원을 돌리게 되었습니다. 2024년 3분기 생명과학 분야의 벤처 자금 조달액은 전년 동기 대비 10% 증가했습니다. 기업이 생산성을 높이기 위해 계산 전문 지식을 요구하고 있기 때문에 파트너십이 급증하고 2025년에는 105건의 AI를 중심으로 한 발견 안건이 등록되었습니다. 자본은 더욱 선별적이며 강력한 메커니즘적 근거, 규제의 명확성, 차별화된 가치 제안을 가진 프로그램을 선호합니다. 지속적인 자금 유입은 견고한 혁신 사이클을 지원하고 Drug Discovery 시장의 확대를 지원합니다.

성공적인 자산 1개당 평균 투자액은 22억 3,000만 달러에 이르렀고, 중견 및 중소기업의 혁신자는 이 부담을 통감하고 있습니다. 기존의 10년에서 15년의 개발 기간은 특히 맞춤형 제조를 필요로 하는 복잡한 치료법에서는 자본을 압박하고 환자에 대한 접근을 지연시킵니다. 자금이 장기화된 프로그램에 구속된 상태로 남아 있기 때문에 기회 비용이 증가합니다. 기업은 전임상 탐색을 4년 단축하고 실험적 반복을 삭감하는 AI 대응 플랫폼을 채용함으로써 이러한 압력에 대항하고 있습니다. 리스크 분담을 위한 공동연구는 비용을 분산하고 개발업무 수탁기관은 모듈화된 능력을 제공하지만 자본 시장이 부족한 지역에서는 자금 조달의 제약이 계속되어 조사 시장 전체의 성장을 억제하고 있습니다.

세포 및 유전자 치료 후보는 CAGR 12.8%로 확대되어 치유 가능성이 투자의 우선순위를 시프트시키는 가운데, Drug Discovery 시장 전체의 성장을 상회합니다. 4,418개 첨단 치료제 파이프라인은 개발자들의 관심을 높여주며, 미국에서는 2024년 8가지 승인을 받고 규제 당국의 기세를 확인할 수 있습니다. 저분자는 예측 가능한 화학적 성질과 확립된 제조 방법에 의해 여전히 Drug Discovery 시장 규모의 56%를 차지하고 있지만, 생물학적 제제에 비해 성장은 감속하고 있습니다. RNA 치료제는 모달리티의 수렴을 나타내며, 저분자의 범용성과 생물학적 특이성의 교대 역할로서 2030년까지 300억 달러의 매출이 전망되고 있습니다. 개발자는 레거시 능력보다 분자 병리학을 기반으로 치료법을 선택하게 되었으며, 이 전략적 재조합은 Drug Discovery 시장의 역동성을 강화하고 있습니다.

벡터 엔지니어링과 동종 세포 플랫폼의 채택은 확장성을 향상시키고 상품 원가를 낮추어 유전자 치료의 광범위한 상업적 실행 가능성을 가능하게 합니다. 한편, 펩티드 및 올리고뉴클레오티드 플랫폼은 지금까지 치료 불가능한 것으로 여겨진 세포내 표적에 대해 신속한 합성 및 양호한 독성 프로파일을 제공합니다. 이러한 변화를 총칭하면 Drug Discovery 시장이 다양해지고 경쟁 전략은 플랫폼의 다양성과 양식에 민감하지 않은 파이프라인으로 재조정됩니다.

AI를 활용한 CADD는 CAGR 13.2%로 성장하여 최적화된 ADMET 특성을 가진 신규 화합물을 생성할 수 있는 트랜스포머 모델에 지지되고 있습니다. 예측 알고리즘은 실리코에서 수백만 개의 변종을 평가하고 의료 화학에서 무차별 검진 및 자르기 사이클에 대한 의존도를 줄입니다. 대조적으로, 높은 처리량 스크리닝은 방대한 화합물 라이브러리 및 확립된 로봇 기술을 활용하여 Drug Discovery 시장 규모의 32%와 최대 점유율을 유지하고 있습니다. 팀은 인공지능을 활용하여 라이브러리를 조율하고, 그 후 정화된 하위 집합에 HTS를 전개하며, 계산 인사이트 및 경험적 검증을 결합하여 히트의 질을 극대화합니다.

Pharmacogenomics는 유전자 돌연변이를 약물 반응과 연관시킴으로써 임상시험 설계 및 시판 후 안전성을 향상시키고 지지를 모으고 있습니다. DNA 코딩 라이브러리는 친화력 기반 선택을 허용하면서 조합을 제공하고 AI 화학을 보완합니다. 나노 기술은 용해성과 조직 침투성을 향상시키고 표적 영역을 넓히는 캐리어 시스템을 도입합니다. 통합된 데이터 환경을 통해 이러한 기술을 조직하는 기업은 속도, 정확성, 감소를 얻고 통합 플랫폼의 의약 시장 점유율을 확대합니다.

북미가 2024년 Drug Discovery 시장 규모의 35%를 차지하며 선도했습니다. 이는 깊은 연구 인프라, 풍부한 자본, 같은 해 7건의 FDA에 의한 첨단 치료제의 승인에 뒷받침됩니다. 벤처기업의 자금 조달력 및 희소질환 혁신 허브 등의 정책적 틀이 기세를 지속시키고 있습니다. 그러나, 의약품 1품당 평균 비용은 22억 3,000만 달러로 상승하고, 중소기업에 있어서 큰 과제가 되고 있기 때문에 AI를 활용한 효율화 툴의 채용에 박차가 걸려, 특정 기능의 국경을 넘은 아웃소싱이 촉진되고 있습니다.

아시아태평양은 가장 성장하는 지역으로, 2030년까지 연평균 복합 성장률(CAGR)은 10.8%가 될 전망입니다. 중국, 한국, 일본 정부는 AI가 풍부한 혁신 클러스터를 촉진하고, 시험 규제를 간소화하며, 인프라를 조성합니다. 중국만으로도 세계 파이프라인 후보자의 23%에 기여하고 있으며, 이 지역의 과학적 능력 증가 및 대규모 환자 풀을 반영하고 있습니다. 항체 약물 복합체에 대한 연구가 활발히 이루어졌으며, 임상시험의 아웃소싱은 비용 효율적인 운영으로부터 혜택을 받고 확대되는 Drug Discovery 시장에 대한 공헌이 강화되고 있습니다.

유럽은 호라이즌 유럽의 자금 조달 메커니즘과 규제 당국의 심사 조화를 목표로 하는 범 EU 이니셔티브를 활용하여 견고한 과학적 기반을 유지하고 있습니다. 중점 분야에는 희귀질환이나 선진 치료가 포함되어 산학 컨소시엄이 실용화를 가속하고 있습니다. 중동 및 아프리카는 생명과학공원에 대한 국부투자에 의해 지지를 받으면서 지역에 만연하는 질병에 적응한 능력을 구축하고 있습니다. 남미는 천연물 발견에 중점을 둔 생물 다양성과 NIH의 500,000 샘플의 천연물 라이브러리의 혜택을 누리고 있습니다. 지역을 넘어서는 협력체제가 강화되어 다양한 전문지식에 접근할 수 있어 단일 시장의 리스크가 경감되고, 전체적으로 Drug Discovery 시장이 확대됩니다.

The global drug discovery market size stands at USD 106.70 billion in 2025 and is forecast to reach USD 146.80 billion by 2030, expanding at a 6.59% CAGR.

Growth is propelled by rising chronic disease prevalence, sustained R&D spending, and the accelerating adoption of artificial intelligence across discovery workflows. Large pharmaceutical companies are directing resources toward late-stage assets, while biotechnology firms leverage agile operating models to advance novel modalities. Artificial intelligence shortens candidate identification from years to months and reduces pre-clinical costs, encouraging wider participation from mid-tier players. Precision medicine is steering investment toward targeted therapies and rare-disease programs, and supportive regulatory initiatives are refining expedited pathways for high-unmet-need indications.

Chronic and rare conditions are redefining program priorities, with oncology alone attracting 41% of active projects due to high unmet need and commercial potential. Neuroscience pipelines are also expanding as companies pursue therapies for Alzheimer's disease, essential tremor, and other debilitating disorders. The trend extends to orphan indications: 88% of novel cell and gene therapies approved in 2024 carried Orphan Drug designations, underscoring a pivot toward smaller, genetically defined populations. Investment in rare disease research drives sophisticated biomarker strategies, improving target validation and de-risking early development. These dynamics collectively lift demand for advanced discovery platforms and attract specialized capital, bolstering long-run growth of the drug discovery market.

Global R&D returns rose to 5.9% in 2024 after the launch of 29 blockbuster drugs, prompting companies to channel resources into late-stage assets with clearer paths to market. Venture funding in life sciences increased 10% year-over-year in Q3 2024, reflecting renewed confidence despite macroeconomic uncertainty. Partnerships surged, with 105 AI-centric discovery deals registered in 2025 as firms sought computational expertise to boost productivity. Capital is becoming more selective, favoring programs with strong mechanistic rationale, regulatory clarity, and differentiated value propositions. Sustained inflows underpin a robust innovation cycle, supporting the expansion of the drug discovery market.

Average outlay per successful asset climbed to USD 2.23 billion, a burden acutely felt by small and mid-cap innovators. Traditional 10-15-year pathways strain capital and delay patient access, especially for complex modalities requiring bespoke manufacturing. Opportunity costs rise as funds remain tied up in protracted programs. Companies counter these pressures by embracing AI-enabled platforms that cut pre-clinical discovery by four years and slash experimental iterations. Risk-sharing collaborations distribute costs, while contract research organizations provide modular capacity, yet financing constraints persist in regions lacking deep capital markets, tempering overall drug discovery market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cell and gene therapy candidates expand at a 12.8% CAGR, eclipsing overall drug discovery market growth as curative potential shifts investment priorities. The pipeline of 4,418 advanced therapies reflects surging developer interest, while eight U.S. approvals in 2024 validate regulatory momentum. Small molecules still command 56% of drug discovery market size due to predictable chemistry and established manufacturing, yet growth is decelerating relative to biologics. RNA therapeutics illustrate modality convergence, bridging small-molecule versatility and biologic specificity with projected USD 30 billion sales by 2030. Developers increasingly select modalities based on molecular pathology rather than legacy capability, a strategic realignment reinforcing the dynamism of the drug discovery market.

Adoption of vector engineering and allogeneic cell platforms is improving scalability and lowering cost of goods, enabling wider commercial viability for gene therapies. Meanwhile, peptide and oligonucleotide platforms offer rapid synthesis and favorable toxicity profiles for intracellular targets historically deemed undruggable. Collectively, these shifts diversify the drug discovery market and recalibrate competitive strategies toward platform versatility and modality-agnostic pipelines.

AI-driven CADD grows at a 13.2% CAGR, underpinned by transformer models capable of generating novel chemical entities with optimized ADMET properties. Predictive algorithms evaluate millions of variants in silico, reducing reliance on brute-force screening and trimming cycles in medicinal chemistry. In contrast, high-throughput screening retains the largest share at 32% of the drug discovery market size by leveraging massive compound libraries and established robotics. Integration, not substitution, is the prevailing trend: teams use AI to triage libraries, then deploy HTS on refined subsets, combining computational insight with empirical validation to maximize hit quality.

Pharmacogenomics gains traction by linking genetic variants to drug response, enhancing trial design and post-marketing safety. DNA-encoded libraries offer combinatorial reach while enabling affinity-based selection, complementing AI chemistries. Nanotechnology introduces carrier systems that improve solubility and tissue penetration, broadening target space. Companies that orchestrate these technologies through unified data environments gain speed, accuracy, and lower attrition, thereby enlarging the drug discovery market share of integrated platforms.

The Drug Discovery Market Report is Segmented by Drug Type (Small Molecule, Biologic, and More), Technology (High Throughput Screening, Pharmacogenomics, and More), Process Workflow (Target Identification, Target Validation, and More), Therapeutic Area (Oncology, and More), End User (Pharmaceutical Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 35% of the drug discovery market size in 2024, supported by deep research infrastructure, abundant capital, and seven FDA approvals for advanced therapies in the same year. Venture funding resilience and policy frameworks such as the Rare Disease Innovation Hub sustain momentum. However, average per-drug costs rising to USD 2.23 billion challenge smaller enterprises, spurring adoption of AI-enabled efficiency tools and encouraging cross-border outsourcing of selected functions.

Asia-Pacific is the fastest-growing region, poised for a 10.8% CAGR through 2030. Governments in China, South Korea, and Japan promote AI-rich innovation clusters, streamline trial regulations, and subsidize infrastructure. China alone contributes 23% of global pipeline candidates, reflecting the region's mounting scientific capacity and large patient pools. Antibody-drug conjugate research flourishes, and clinical trial outsourcing benefits from cost-effective operations, reinforcing the region's contribution to the expanding drug discovery market.

Europe maintains a robust scientific base, leveraging Horizon Europe funding mechanisms and pan-EU initiatives aiming to harmonize regulatory review. Focus areas include rare diseases and advanced therapies, with academic-industry consortia accelerating translation. The Middle East & Africa build targeted capabilities in diseases of regional prevalence, supported by sovereign-wealth investment in life-science parks. South America emphasizes natural-product discovery, benefiting from its biodiversity and the NIH's 500,000-sample natural-product library. Cross-regional collaboration intensifies, enabling access to diverse expertise, reducing single-market risk, and collectively enlarging the drug discovery market.