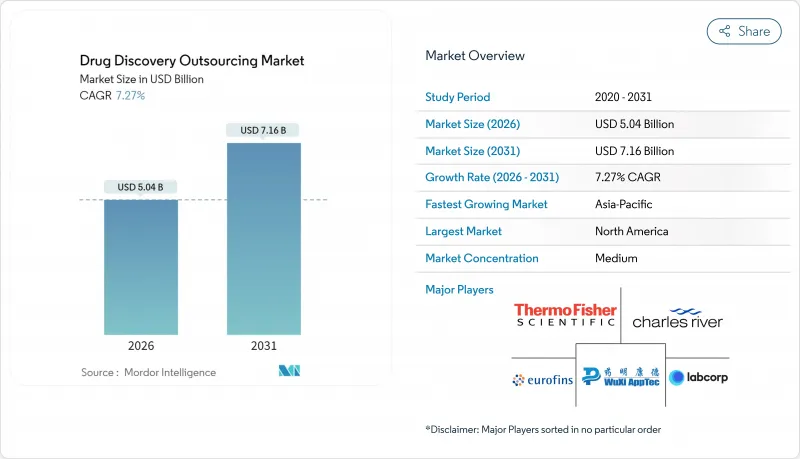

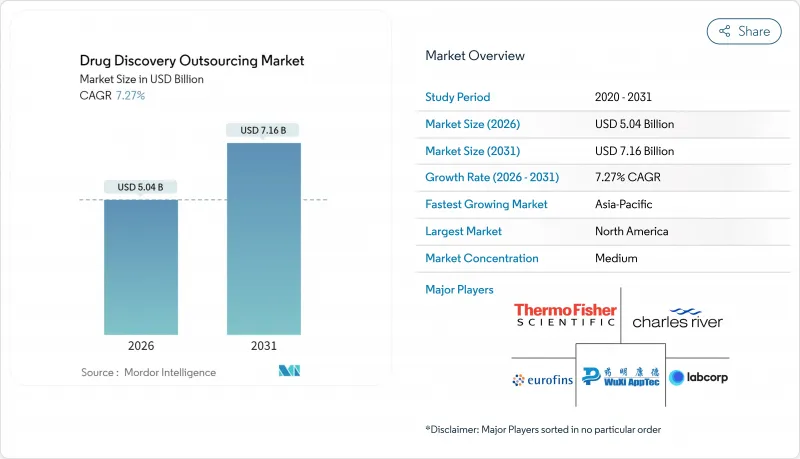

신약 개발 아웃소싱 시장은 2025년에 47억 달러로 평가되었고, 2026년 50억 4,000만 달러에서 2031년까지 71억 6,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 7.27%를 나타낼 전망입니다.

이러한 꾸준한 성장은 네 가지 근본적인 요인에 기반을 두고 있습니다 : 제약 부문의 외부 혁신으로의 전환, 차세대 치료법의 과학적 복잡성 증가, 초기 발견 워크플로우를 가속화하는 디지털 기술, 그리고 내부 자본 투입의 재조정 필요성입니다. 종합 서비스 계약 연구 기관(CRO)들이 의약 화학, 생물학, 컴퓨터 기반 설계 부문로 영역을 확장함에 따라 경쟁 강도가 높아지고 있습니다. 북미는 여전히 매출의 중심지이지만, 아시아태평양 지역은 비용 효율적인 AI 기반 플랫폼과 지원 정책 프레임워크를 통해 격차를 좁혀가고 있습니다. 수요는 점점 더 종양학, 신경학, 희귀 질환 파이프라인에 집중되고 있으며, 여기서 계산 도구는 히트-투-리드 주기를 단축하고 표적 검증 정확도를 향상시킵니다.

연간 신약 개발 예산은 지속적으로 증가하고 있으나, 내부 자본 배분은 여전히 압박을 받고 있습니다. 승인된 분자당 평균 총비용은 현재 26억 달러를 초과하여, 경쟁 우위를 제공하지 않는 업무 흐름을 외부화하도록 기업들을 압박하고 있습니다. CRO 파트너십은 기업들이 자원 배치를 치료 부문 우선순위에 맞추도록 지원하여, 프로그램 위험 프로필 변화에 따라 생산 능력을 유연하게 조정할 수 있게 합니다. 스탠퍼드 대학의 SyntheMol과 같은 AI 모델은 9시간도 채 되지 않아 25,000개의 항생제 후보 물질을 생성했으며, 이는 알고리즘 설계와 고속 대량 합성이 결합될 때 가능한 생산성 향상을 보여줍니다. 이러한 속도는 선행 기업들이 경쟁사들이 동일한 표적 군을 다루기 전에 특허 위치를 확보할 기회를 제공합니다.

만성 질환은 현재 전 세계 의료비 지출의 대부분을 차지하며 치료 가능한 환자 풀을 크게 확장하고 있습니다. 종양학 부문만 해도 2024년 매출의 31.5%를 차지했는데, 이는 종양 생물학이 복잡한 신호 전달 네트워크를 포함하여 전문적인 발견 도구 키트의 혜택을 받기 때문입니다. 세포 및 유전자 치료제는 37건의 규제 승인을 획득하며 난치성 질환에 대한 정밀 접근법의 유효성을 입증하고, 핵산 공학이 가능한 외부 파트너사에 대한 투자를 촉진하고 있습니다. 네트워크 기반 다중 오믹스 분석은 표적 선별 정확도를 향상시켜, 고비용의 전환 연구가 견고한 기전적 토대 위에 설 것이라는 확신을 스폰서에게 제공합니다.

정부는 특히 대규모 유전체 데이터셋에 의존하는 AI 기반 발견 프로그램을 대상으로 데이터 거주 규정 강화 및 전자 실험실 노트 감사를 강화하고 있습니다. 단일 규정 위반 시 평균 1,480만 달러의 벌금 및 시정 비용이 발생하여, 스폰서들은 파트너사의 사이버 보안 태세와 블록체인 기반 추적성 솔루션을 철저히 검증해야 합니다. 연방 학습(Federated Learning)과 제로 지식 암호화(Zero-Knowledge Encryption) 방식이 주목받는 이유는 원시 환자 데이터를 중앙 집중화하지 않고도 국가 간 모델 훈련을 가능하게 하기 때문입니다.

의약화학은 2025년 매출의 37.74%를 차지하며, 구조-활성 관계 및 물리화학적 특성 최적화에서 핵심적 역할을 입증했습니다. 이 부문은 합성 경로를 간소화하고 용매 폐기물을 줄여 지속가능성 지표와 원가 효율성을 개선하는 C-H 활성화 기술 발전의 혜택을 받습니다. 또한 저분자는 만성 질환 치료에 확장성이 유지되므로 장기적 수요를 확보합니다. 고처리량 스크리닝은 소형화된 분석 형식과 클라우드 기반 분석 기술로 수백만 개의 후보 물질을 며칠 내 순위를 매길 수 있어 13.12%의 예상 연평균 성장률(CAGR)을 기록할 전망입니다. AI 스코어링 알고리즘 통합은 신호 대 잡음 비율을 높이고 후속 단계에서의 실패율을 감소시킵니다. 연속적인 화학-생물학 워크플로우를 제공하는 업체들은 아이디어 구상부터 후보물질 선정까지 원스톱 솔루션을 추구하는 의뢰사들의 지출 비중을 확보합니다.

자율 합성 로봇의 확대 적용은 시장 선도업체들의 차별화를 더욱 강화합니다. 이러한 시스템은 설계와 테스트 간의 반복 주기를 단축시켜 머신러닝 모델에 풍부한 데이터셋을 공급합니다. 생산성 향상은 CRO가 효능 및 선택성 마일스톤 달성 시 부분적 위험을 부담하는 고정가격 계약을 뒷받침합니다. 이러한 모델은 협력 관계의 경제성을 재정의하며 신약개발 아웃소싱 시장에서 해당 서비스 라인의 입지를 공고히 하고 있습니다.

2025년 시점에서 저분자 화합물은 수익의 64.7%를 차지했습니다. 경구 투여의 편리성과 성숙한 규제 경로를 흡수하고 있기 때문입니다. 이 부문에는 제조 설비의 대규모 도입 기반도 있으며, 만성 질환 치료에서 스폰서 기업에게 예측 가능한 제품 원가를 제공합니다. 대조적으로, 세포 및 유전자 치료는 단일 유전자 질환에서의 근치적 치료의 가능성을 원동력으로 2031년까지 연평균 복합 성장률(CAGR) 15.55%라는 가장 강한 성장세를 기록했습니다. 높은 조작 기술 요구 사항과 콜드체인 물류의 복잡성으로 인해 많은 프로그램이 바이러스 벡터 장비와 세포 처리 클린 룸을 갖춘 외부 파트너에게 위탁을 진행하고 있습니다.

하이브리드 탐색 플랫폼은 현재 인실리코에 의한 표적 우선순위화와 CRISPR 편집 기술을 융합시켜 1차 세포에서의 질병 인과 관계를 검증하고 있습니다. 이러한 통합 실험은 개념 증명을 가속화하고 임상 응용에 대한 위험을 줄입니다. 플라스미드 백본 설계와 면역원성 분석을 모두 습득한 CRO는 과학적 요구와 스폰서의 아웃소싱 수요가 어우러지는 위치에 스스로를 자리매김하여 신약 개발 아웃소싱 시장에서 이 고부가가치 틈새 부문에서의 성장을 확고히 하고 있습니다.

북미는 제약기업의 본사가 밀집되어 벤처자본에 의한 바이오테크 기업과 AI 스타트업이 많이 존재하기 때문에 2025년 수익의 40.58%를 창출했습니다. 미국의 CRO는 벤처 자금을 최첨단 자동화 기술, 다층화 화합물 라이브러리, 엄선된 인간 데이터 자산에 투입하고 있습니다. 실세계 데이터에 대한 규제 당국의 개방적인 자세는 비임상시험 패키지의 축소를 통해 프로젝트의 처리 속도를 더욱 가속화합니다. 캐나다는 전임상 혁신에 대한 정부의 인센티브로 지역 생태계를 보완하고 품질 기준을 손상시키지 않고 재정적 이점을 제공합니다.

아시아태평양 지역은 2026-2031년의 연평균 12.84%의 가장 가파른 성장률을 보일 전망입니다. 이는 확대되는 인재 풀, 낮은 운영 비용, 바이오의약품 자립을 우선시하는 국가 로드맵에 힘입은 것입니다. 중국은 화학, 생물학, GMP 시설을 통합한 캠퍼스 단지로 지역 매출을 주도합니다. 인도는 방대한 합성 화학 역량과 영어 사용 인력을 통해 입지를 강화하고 있습니다. 한국은 AI 기반 표적 발견을 뒷받침하는 게놈 빅데이터 허브에 투자하고 있습니다. 이러한 역동성은 과학적 정교함을 희생하지 않으면서 비용 절감을 추구하는 세계의 스폰서들을 유인하여, 해당 지역의 신약 개발 아웃소싱 시장 점유율을 높이고 있습니다.

유럽은 엄격한 품질 기준, 깊은 학술 네트워크, RNA 치료제 등 복잡한 모달리티 전문 지식을 배경으로 견조한 실적을 유지하고 있습니다. 독일과 스위스는 고정밀 분석과 항체 공학을 전문으로 하고 영국은 지원적인 데이터 거버넌스 틀 아래에서 AI 퍼스트의 신약 개발 벤처를 육성하고 있습니다. 성장률은 아시아태평양에 미치지 않는 것, 컴플라이언스의 우수성으로 알려진 유럽은 고부가가치 프로젝트의 안정된 파이프라인을 확보하고 있습니다. 유럽연합의 '호라이즌 및 유럽' 프로그램에 의한 국경 간이니셔티브는 중소규모의 CRO(의약품 개발 수탁기관)와 주요 제약 스폰서를 연결하여 단순한 수탁처가 아닌 전략적 파트너로서 유럽의 역할을 강화하고 있습니다.

The drug discovery outsourcing market was valued at USD 4.70 billion in 2025 and estimated to grow from USD 5.04 billion in 2026 to reach USD 7.16 billion by 2031, at a CAGR of 7.27% during the forecast period (2026-2031).

This steady expansion is built on four underlying factors: the pharmaceutical sector's pivot toward external innovation, the growing scientific complexity of next-generation therapies, digital technology's acceleration of early discovery workflows, and the need to re-balance internal capital commitments. Competitive intensity is increasing as full-service contract research organizations (CROs) extend their footprints across medicinal chemistry, biology, and in-silico design. North America remains the revenue anchor, yet Asia-Pacific is closing the gap through cost-efficient, AI-enabled platforms and supportive policy frameworks. Demand is increasingly concentrated in oncology, neurology, and rare disease pipelines, where computational tools shorten hit-to-lead cycles and improve target validation accuracy.

Annual discovery budgets continue to climb, yet internal capital allocation remains under pressure. Average fully-loaded cost per approved molecule now exceeds USD 2.6 billion, compelling sponsors to externalize workflows that do not confer competitive distinction. CRO partnerships help companies match resource deployment with therapeutic priorities, allowing them to dial capacity up or down as program risk profiles evolve. AI models such as Stanford's SyntheMol generated 25,000 antibiotic candidates in under nine hours, illustrating the productivity lift available when algorithmic design meets high-throughput synthesis. Such speed gives early movers a chance to secure patent positions before rivals address the same target families.

Chronic illnesses now account for the majority of worldwide health-care expenditure and greatly expand addressable patient pools. Oncology alone captured 31.5% of revenue in 2024 because tumor biology involves complex signaling networks that benefit from specialized discovery toolkits. Cell and gene therapies have received 37 regulatory approvals, validating precision approaches for intractable disorders and motivating investments in external partners capable of nucleic-acid engineering. Network-based multi-omics analysis is improving target triage accuracy, giving sponsors confidence that costly translational studies will rest on solid mechanistic foundations.

Governments are tightening data-residency rules and auditing electronic lab notebooks, especially for AI-driven discovery programs that rely on large genomic datasets. A single compliance breach averages USD 14.8 million in penalties and remediation, forcing sponsors to vet partners' cybersecurity postures and blockchain-based traceability solutions. Federated learning and zero-knowledge encryption methods are gaining traction because they allow model training across country borders without centralizing raw patient data.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Medicinal chemistry captured 37.74% of revenue in 2025, confirming its central role in optimizing structure-activity relationships and physicochemical profiles. This branch benefits from advances in C-H activation that streamline synthetic routes and cut solvent waste, improving sustainability metrics and cost of goods. The segment also secures long-term demand because small molecules remain scalable for chronic indications. High-throughput screening holds 13.12% projected CAGR due to miniaturized assay formats and cloud-based analytics that can rank millions of hits in days. Integration of AI scoring algorithms lifts signal-to-noise ratios and reduces downstream attrition. Providers that offer contiguous chemistry-biology workflows gain wallet share as sponsors seek one-shop solutions for ideation through candidate nomination.

Expanded use of autonomous synthesis robots further differentiates market leaders. These systems shorten iteration loops between design and test, feeding machine-learning models with richer datasets. The productivity lift supports fixed-price contracts where CROs assume partial risk on achieving potency and selectivity milestones. Such models are re-defining partnership economics and solidifying the service line's hold on the drug discovery outsourcing market.

Small molecules held 64.7% of revenue in 2025 because they absorb oral dosing convenience and mature regulatory pathways. The segment also commands a large installed base of manufacturing assets, giving sponsors predictable cost of goods for chronic therapies. In contrast, cell & gene therapies recorded the strongest momentum at a 15.55% CAGR outlook through 2031, driven by curative potential in monogenic diseases. High operator skill requirements and cold-chain logistics complexity push many programs toward external partners equipped with viral vector suites and cell processing cleanrooms.

Hybrid discovery platforms now meld in-silico target prioritization with CRISPR editing to verify disease causality in primary cells. Such integrated experimentation accelerates proof-of-concept and de-risks clinical translation. CROs that master both plasmid backbone design and immunogenicity analytics position themselves at the confluence of scientific need and sponsor outsourcing appetite, cementing growth in this high-value niche of the drug discovery outsourcing market.

The Drug Discovery Outsourcing Market Report is Segmented by Type (Medical Chemistry Services, Biology Services, and More), Drug Type (Small Molecules, and More), Therapeutic Area (Oncology, Infectious Disease, and More), End-User (Pharmaceutical Companies, and More), Sourcing Model (Full-Time Equivalent (FTE), and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 40.58% of 2025 revenue attributable to its dense cluster of pharmaceutical headquarters, venture-backed biotechs, and AI start-ups. U.S. CROs channel venture flows into state-of-the-art automation, layered compound libraries, and curated human data assets. Regulatory openness toward real-world evidence further accelerates project throughput by shrinking non-clinical packages. Canada complements the regional ecosystem with governmental incentives for pre-clinical innovation, bringing fiscal benefits without compromising quality expectations.

Asia-Pacific shows the steepest trajectory at 12.84% CAGR between 2026 and 2031, buoyed by an expanding talent pool, lower operating costs, and national roadmaps that prioritize biopharma self-sufficiency. China leads regional revenue thanks to integrated campus sites that combine chemistry, biology, and GMP suites. India strengthens its position through extensive synthetic chemistry capacity and an English-speaking workforce. South Korea invests in genomic big-data hubs that underpin AI-driven target discovery. Collectively, these dynamics lure global sponsors seeking cost relief without sacrificing scientific sophistication, enhancing the region's share of the drug discovery outsourcing market.

Europe sustains strong performance on the back of rigorous quality standards, deep academic networks, and domain expertise in complex modalities such as RNA therapeutics. Germany and Switzerland specialize in high-precision analytics and antibody engineering, while the United Kingdom fosters AI-first discovery ventures under supportive data governance frameworks. Although growth rates trail those of Asia-Pacific, Europe's reputation for compliance excellence secures a steady pipeline of high-value projects. Cross-border initiatives funded by Horizon Europe link small CROs with large pharma sponsors, reinforcing the continent's role as a strategic partner rather than just a capacity provider.