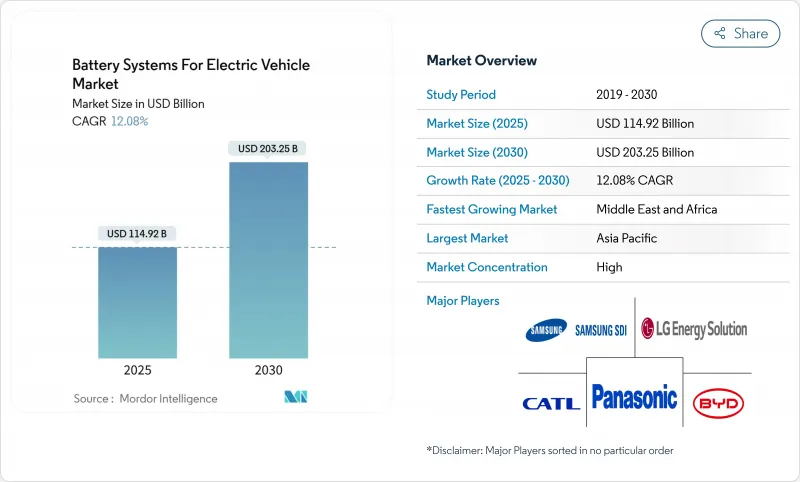

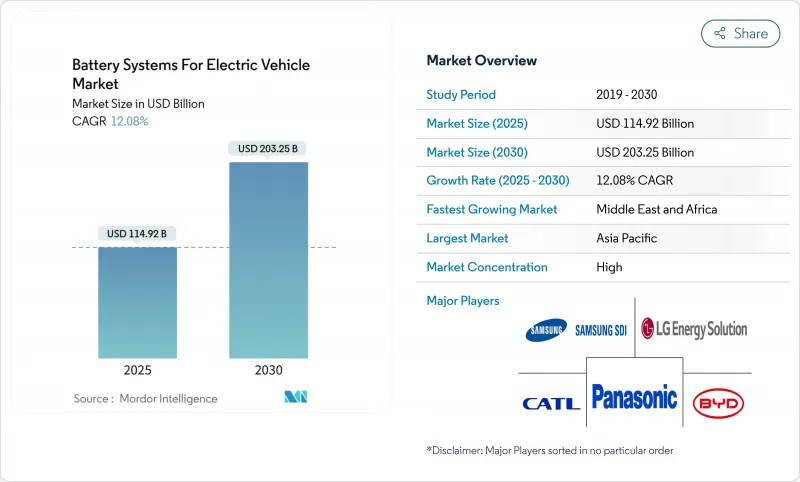

전기자동차 배터리 시스템 시장은 2025년에는 1,149억 2,000만 달러로 추정되고, 2030년에는 CAGR 12.08%로 성장할 전망이며, 2,032억 5,000만 달러로 확대될 것으로 예측됩니다.

북미와 유럽에서 인센티브 주도의 채용 목표, 리튬 이온 화학의 급속한 비용 저하, 아시아, 북미, 유럽에 걸친 수직 통합형의 기가 팩토리 전개가 이 확대를 지원하고 있습니다. 또한 리튬 이온 및 나트륨 이온과 커패시터를 결합한 멀티 케미스트리 팩이 설계 유연성을 넓히는 한편, 보다 높은 에너지 밀도와 안전성을 약속하는 솔리드 스테이트의 돌파구도 이 시장에 이익을 가져오고 있습니다. 미국과 유럽연합(EU)의 규제 프레임워크가 현지 함량 규제를 강화하는 가운데 중국 제조업체가 인산철 리튬의 비용 우위를 이용하여 점유율을 획득하고 있기 때문에 경쟁의 치열함은 여전히 높습니다. 공급망 분기, 열폭주로 인한 리콜, 중요한 광물의 변동은 전망을 약화시키지만 지속적인 성장 궤도를 미치지 못합니다.

규제 프레임워크는 전기 드라이브 트레인의 최저 판매 대수를 고정함으로써 수요를 가속시킵니다. 미국은 대상 자동차 1대 당 최고 7,500달러의 세액 공제를 제공하고 국산차 비율 임계값을 매년 인상하고 있습니다. 캘리포니아의 고급 클린카 Ⅱ규칙은 2025년 제로 배출 차량 판매 대수의 22%, 2035년까지 100%를 달성할 것을 자동차 업체에 의무화하고 있습니다. 영국은 2030년까지 80%의 전기자동차 판매를 의무화하고 캐나다는 2035년까지 100%를 목표로 하고 있습니다. 컴플라이언스 위반은 많은 양의 위약금을 부과하게 되므로 대부분의 자동차 제조업체는 다년간 배터리 인수 계약을 체결하여 셀 제조업체에게 판매량 확보 및 현금 흐름 가시성을 제공합니다.

학습 곡선 효과 및 재료 대체로 비용이 낮아지고 있습니다. 톱 클래스의 셀 제조업체 몇사는 2024년에는 1kWh당 118달러였던 팩 코스트를, 2026년에는 60달러 이하로 내리는 것을 목표로 하고 있습니다. 에너지 밀도는 비용량을 25-50% 높이는 실리콘 리치 음극에 의해 상승하고, 인산철 리튬은 세련된 정극 코팅에 의해 체적 밀도를 향상시킵니다. 비용이 급격히 떨어지면 대응 가능한 시장은 엔트리 레벨 승용차, 이륜차 및 비용에 민감한 상용차로 확장됩니다.

업스트림 정화에 집중하면 제조업체가 지정학적 위험에 노출됩니다. 중국은 세계의 인산철 리튬 양극재의 80%를 정제하고, 코발트의 대부분은 어느 나라가 생산하고 있습니다. 리튬 수요는 2030년까지 5배로 늘어날 것으로 예상되지만, 광산 승인이 늦어지면서 가격 변동이 셀 제조업체의 금리를 압박하고 있습니다. 다각화 노력을 실현하는 데는 몇 년이 걸리므로 유력 공급업체에 대한 의존도가 높아지고 가격 전망이 나빠집니다.

2024년 전기자동차 배터리 시스템 시장 점유율은 리튬 이온 기술이 94.12%를 차지했으며, 2030년까지 수량 리더로 이어지고 있습니다. 팩 수준의 급속한 혁신으로 무게 밀도는 300Wh/kg을 목표로 하는 반면, 비용은 60 USD/kWh 미만으로 떨어지고 있습니다. 이 부문의 제조 에코시스템은 재료, 셀 형식, 재활용 흐름에 걸쳐 규모의 이점을 강화하고 신차 OEM의 진입 장벽을 낮추고 있습니다.

고체 전지의 CAGR은 39.92%로 가장 높고, 덴드라이트의 성장을 억제하며, 1,000사이클 후의 용량 저하를 5%로 억제하는 세라믹제 세퍼레이터에 뒷받침되고 있습니다. 뛰어난 에너지 저장 능력으로 컴팩트한 팩 설계가 가능하게 되어, 고성능 모델이나 장거리 모델에 있어서 중요한 요소인 차내 스페이스의 해방이나 차체 중량의 경량화를 실현합니다. 상업적 준비가 되는지 여부는 자동 소결 라인과 고압 라미네이션 라인이 10년 후반까지 기존의 리튬 이온과 동등하게 제조 비용을 절감할 수 있는지 여부에 달려 있습니다.

니켈 망간 코발트 화학은 2024년 전기자동차 배터리 시스템 시장 규모의 61.38%를 차지했으며, 최대 항속 거리를 필요로 하는 고급 승용차와 소형 트럭에서의 지위를 확립하고 있습니다. 지속적인 코발트 함량 감소 및 망간 리치 배합은 가격 상승과 윤리적 조달 우려에 노출되는 것을 줄여줍니다.

인산철 리튬은 견고한 안전성, 풍부한 원료 공급량, 저비용을 배경으로 급상승하여 저렴한 부문 및 대형 상용차를 매료시킵니다. CAGR 성장률 44.16%의 나트륨 이온 배터리는 -40℃까지의 저온 동작이 가능하며, 빈번한 급속 충전 사이클에도 견딜 수 있습니다. 리튬 함량이 제한없이 0에 가깝기 때문에 가격 위험이 완화되어 리튬 매장량이 부족한 지역에서 국내 자원을 이용할 수 있습니다. 나트륨 이온과 리튬 이온을 결합한 하이브리드 팩은 성능을 유지하면서 비용을 최적화하고 밀도가 200Wh/kg에 도달하면 나트륨 이온 완전 이행에 가교되는 아키텍처를 구축합니다.

아시아태평양은 광물 가공부터 셀 조립, 차량 제조까지 일관된 공급망에 힘입어 2024년 전기자동차 배터리 시스템 시장에서 64.32%의 점유율을 유지했습니다. 중국만은 국내 수요가 견조하게 추이하고, 특히 동남아시아와 라틴아메리카로의 수출이 급증할 전망이기 때문에 2030년까지 대폭적인 성장을 지지하고 있습니다. 일본은 고체연구를 진행하고 한국은 경쟁력을 회복하기 위해 고망간화학으로 축발을 옮깁니다. 정부의 인센티브 조정 및 협력적인 인프라 지출은 지역 생태계를 지속적으로 강화합니다.

북미는 2위 시장 규모를 기록하고, 인플레이션 저감법은 청정 에너지 자금에 3,690억 달러를 투입하며, 중요한 광물의 기준치를 끌어올려 새로운 기가팩토리와 중류 정제 프로젝트의 견고한 파이프라인을 형성합니다. 마찬가지로 유럽은 그린딜 정책과 유럽 전지 동맹을 배경으로 CAGR 9.40%로 전진하고 있습니다. 전략적 자율성은 관민 합작 사업이 자금을 제공하는 지역 밀착형의 정극 생산과 셀 조립을 추진합니다. 독일은 실리콘 리치 음극을 추진하는 연구 파트너십을 주도하고, 스페인과 프랑스는 대중 시장을 위한 인산철 리튬에 주력하고 있습니다.

중동 및 아프리카는 CAGR 15.74%에서 가장 높은 성장을 이루고 있습니다. 사우디아라비아는 경제 다양화와 자동차 제조의 다운스트림 확보를 위해 종합 배터리 복합 시설에 60억 달러를 투자합니다. 아랍에미리트(UAE)은 2035년까지 전기자동차 보급률 25%를 목표로 내걸고, 에미리트 간 고속도로를 따라 충전 코리도 정비를 진행하고 있습니다. 가나, 모로코, 르완다의 초기 단계 프로젝트는 양허적 자금 조달과 개발 지원 기관에 의한 기술 지원의 혜택을 받고 있으며, 이륜차와 경상용차의 지역 전화를 대륙에 자리잡고 있습니다.

The battery systems for electric vehicles market stands at USD 114.92 billion in 2025 and is forecast to climb to USD 203.25 billion by 2030, reflecting a 12.08% CAGR by 2030.

Incentive-driven adoption targets in North America and Europe, rapid cost declines in lithium-ion chemistry, and vertically integrated gigafactory roll-outs across Asia, North America, and Europe underpin this expansion. The market also benefits from solid-state break-throughs that promise higher energy density and safety, while multi-chemistry packs combining lithium-ion with sodium-ion or ultracapacitors widen design flexibility. Competitive intensity remains high as Chinese producers use lithium iron phosphate cost advantages to win share, even as regulatory frameworks in the United States and the European Union tighten local-content demands. Supply-chain bifurcation, thermal-runaway recalls, and critical-mineral volatility temper the outlook but do not derail the secular growth trajectory.

Regulatory frameworks accelerate demand by anchoring minimum sales volumes for electric drivetrains. The United States offers tax credits up to USD 7,500 per qualifying vehicle and escalates domestic-content thresholds each year. California's Advanced Clean Cars II rule obliges automakers to reach 22% zero-emission sales in 2025 and 100% by 2035. The United Kingdom mandates 80% electric sales by 2030, while Canada targets 100% by 2035. Because non-compliance triggers sizable penalties, most vehicle makers lock in multi-year battery offtake contracts, providing cell manufacturers with volume security and cash-flow visibility.

Learning-curve effects and materials substitution continue to drive cost trajectories downward. Several top-tier cell makers aim to push pack costs below USD 60 per kWh by 2026, versus USD 118 per kWh in 2024. Energy density climbs through silicon-rich anodes that raise specific capacity by 25-50%, while lithium iron phosphate improves volumetric density with refined cathode coatings. Rapid cost declines widen the total addressable market into entry-level passenger cars, two-wheelers, and cost-sensitive commercial fleets.

Concentration in upstream refining exposes manufacturers to geopolitical risk. China refines 80% of global lithium iron phosphate cathode material, while one country produces the majority of cobalt. Demand for lithium is expected to grow five-fold by 2030, yet mine approvals lag, forcing price swings that compress cell-maker margins. Diversification efforts require several years to materialize, extending dependence on dominant suppliers and undermining price visibility.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Lithium-ion technology held 94.12% of the battery systems for electric vehicles market share in 2024 and remains the volume leader through 2030. Rapid pack-level innovation drives gravimetric densities toward 300 Wh/kg while trimming cost below USD 60 per kWh. The segment's entrenched manufacturing ecosystem spans materials, cell formats, and recycling streams, reinforcing scale advantages and lowering entry barriers for new vehicle OEMs.

Solid-state cells record the highest 39.92% CAGR, propelled by ceramic separators that curb dendrite growth and cut capacity fade to 5% after 1,000 cycles. Their superior energy storage enables compact pack designs that free cabin space and trim curb weight, key factors in high-performance or extended-range models. Commercial readiness hinges on automated sintering and high-pressure lamination lines that slash production cost to parity with conventional lithium-ion by the late decade.

Nickel manganese cobalt chemistry accounted for 61.38% of the battery systems for the electric vehicles market size in 2024, anchoring its position in premium passenger cars and light trucks that demand maximum range. Continuous cobalt-content reduction and manganese-rich formulations cut exposure to price spikes and ethical sourcing concerns.

Lithium iron phosphate rises sharply on the back of robust safety, abundant raw material supply, and lower cost, attracting budget segments and heavy-duty commercial vehicles. Sodium-ion cells, growing at 44.16% CAGR, unlock cold-temperature operation down to -40 °C and tolerate frequent fast-charge cycles. Their near-zero lithium content buffers price risk and allows domestic resource utilization in regions lacking lithium reserves. Hybrid packs combining sodium-ion and lithium-ion optimize cost while maintaining performance, creating an architecture bridge toward full sodium-ion transition once density reaches 200 Wh/kg.

The Battery Systems for Electric Vehicles Market Report is Segmented by Battery Type (Lithium-Ion, Nickel-Metal Hydride, and More), Battery Chemistry (NMC, NCA, LFP, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Technology (Battery Electric Vehicle (BEV), Plug-In Hybrid Electric Vehicle (PHEV), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific maintained 64.32% share of the battery systems for electric vehicles market in 2024, anchored by an integrated supply chain that stretches from mineral processing through cell assembly to vehicle manufacturing. China alone supports a significant growth through 2030 as domestic demand remains strong and exports surge, particularly to Southeast Asia and Latin America. Japan advances solid-state research while Korea pivots toward high-manganese chemistries to regain competitiveness. Government incentive alignment and coordinated infrastructure spending continue to reinforce the regional ecosystem.

North America registers the second-largest market, the Inflation Reduction Act channels USD 369 billion in clean-energy funding and sets escalating critical-mineral thresholds, creating a robust pipeline of new gigafactories and mid-stream refining projects. Similarly, Europe advances at 9.40% CAGR on the back of its Green Deal policies and the European Battery Alliance. Strategic autonomy drives localized cathode production and cell assembly funded by public-private joint ventures. Germany leads research partnerships that push silicon-rich anodes, whereas Spain and France focus on mass-market lithium iron phosphate.

The Middle East & Africa region posts the highest regional growth at 15.74% CAGR. Saudi Arabia invests USD 6 billion in an integrated battery complex to diversify its economy and secure downstream automotive manufacturing. The United Arab Emirates targets 25% electric vehicle penetration by 2035, anchoring charging-corridor build-outs along inter-emirate highways. Early-stage projects in Ghana, Morocco, and Rwanda benefit from concessional finance and development-agency technical assistance, positioning the continent for localized two-wheeler and light-commercial electrification.