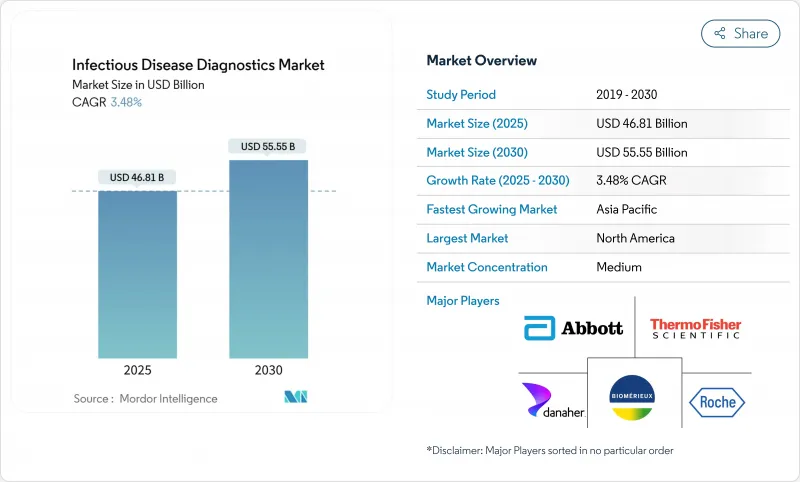

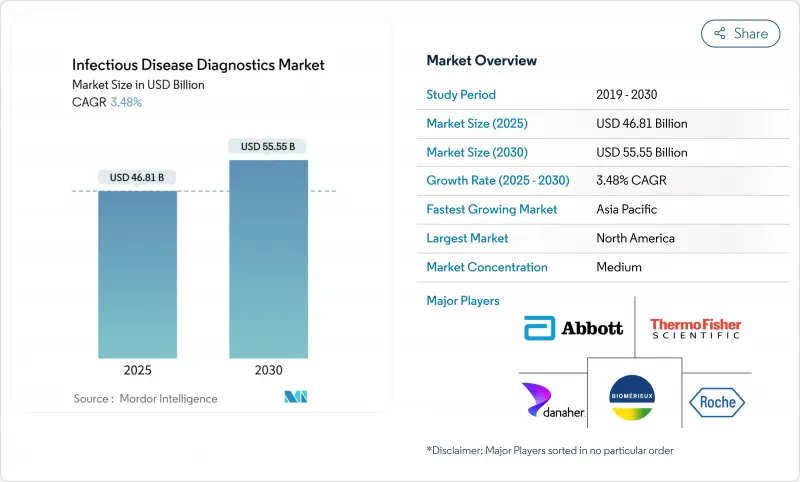

감염증 진단 시장은 2025년에 468억 1,000만 달러, 2030년에는 555억 5,000만 달러에 이르고, CAGR 3.48%를 나타낼 전망입니다.

이 꾸준한 궤적은 감염증 진단 시장이 유행 질병의 주도 수요에서 풍토병 관리, 기후 관련 아웃 브레이크 및 지속적인 기술 업그레이드를 지원하는 장기 성장으로 전환하고 있음을 보여줍니다. 지출은 호흡기 검사뿐만 아니라 매개 병원체, 항균제 내성 병원체, 신흥 병원체 등에도 퍼져 있으며 COVID-19의 수량 감소를 보완하는 데 도움이 됩니다. 시약 판매는 여전히 수익의 기간이지만, 자동화의 효율화를 요구하는 검사실에서는 소프트웨어 대응 워크플로우 툴이 급속히 확대되고 있습니다. CRISPR, 아이소서멀, AI로 무장한 신규 참가 기업이 감염증 진단 시장에서 기존 기업의 점유율 싸움에 도전하고 있기 때문에 경쟁의 격렬함은 증가하고 있습니다.

기후 변화에 의해 모기의 서식지가 넓어지기 때문에 공급자는 한때 열대에 한정되어 있던 병원체의 검사를 실시하게 되어 있습니다. 세계보건기구(WHO)는 2024년 8월 천연두를 3등급 긴급사태로 분류했습니다. WHO의 2024년 우선순위 목록에는 신속한 진단이 필요한 15가지 내성균이 포함되어 있습니다. 새로운 위협이 표면화됨에 따라 실험실은 수시로 메뉴를 업데이트해야하며 감염증 진단 시장 전체의 기업에 경상 수익을 제공합니다.

규제 당국에 의한 소비자 검사의 승인은 급속히 진행되고 있습니다. 2024년 8월, FDA는 최초의 OTC 매독 검사법을 인가하고 소매 진단이 주류가 되었습니다. 매독 이환율은 2018년부터 2022년까지 80% 상승했기 때문에 지역 약국과 전자상거래 포털은 현재 신속 키트를 보유하고 있습니다. 세파이드의 핑거스틱 C형 간염 검사는 1차 클리닉의 케어 갭을 해소하기 위해 방문 시 바이러스 확인을 추가합니다. 지불자는 다운스트림 비용을 줄이는 조기 치료 시작을 평가하기 때문에 복잡한 코딩이 계속되는 가운데 상환 과정이 따라 왔습니다.

지불자는 청구를 승인하기 전에 엄격한 코딩을 요구하고 있으며, 추가된 종이 작업이 소규모 실험실의 캐시 사이클을 연장하고 있습니다. 정부의 진료 보상 체계는 특히 저·중소득국에서 선진적인 분자 플랫폼의 전체 비용을 커버하는 것은 드물고, 그 때문에 도입이 제한되고 있습니다. 이러한 환경하에 있는 실험실은 기증자 프로그램에 의존하고 있으며, 임상적 필요성은 분명하지만, 상업적 기세는 약해지고 있습니다. 통일된 결제 모델은 감염증 진단 시장 전체에 대한 보급이 진행될 것으로 보입니다.

호흡기 패널은 2024년에 감염증 진단 시장 점유율의 20.13%를 차지했지만, 중재 병원체 및 신흥 병원체는 2030년까지 연평균 복합 성장률(CAGR) 5.78%를 나타낼 전망입니다. 2024-2025년에 기록적인 1,300만 명의 뎅기열 환자가 발생하여 병원은 검사 메뉴를 확충해야 합니다. Mpox, 간염, HIV 자기 검사, AI 보조 결핵 분석은 임상 폭을 확장합니다. 세계적인 이동과 기후 변화에 의해 감염지역이 변화하기 때문에 매개충검사에 수반되는 감염증 진단 시장 규모는 계속 증가하고 있습니다.

성장은 병원 감염에 대한 신속한 항균제 감수성 도구와 STI 홈 키트에 대한 FDA의 OTC 인증에 의존합니다. 검사 시설은 WHO가 내성 박테리아 목록에 박테리아를 추가할 때 신속하게 업데이트하는 플랫폼을 강조합니다. 이러한 유연성은 감염증 진단 시장에서 공급업체의 끈적거림을 강화합니다.

분석, 키트, 시약은 2024년 감염증 진단 시장 규모의 53.45%를 차지했습니다. 소프트웨어와 인포매틱스는 규모가 작고 실험실 워크플로우가 디지털화됨에 따라 CAGR이 가장 빠른 5.66%를 나타낼 것으로 보입니다. 검사 장비는 현재 원시 처리량뿐만 아니라 자동화 깊이, 샘플에서 응답까지의 속도, AI와의 협력으로 경쟁하고 있습니다.

병원이 복잡한 시퀀싱과 약물 내성 패널을 외주하면 위탁 검사 서비스가 성장합니다. 클라우드 기반의 애널리틱스는 원시 데이터를 실용적인 보고서에 연결하여 검사별 가치를 높입니다. 감염증 진단 시장 전체에서 하드웨어의 이폭이 축소해도 시약과 인포매틱스를 번들하는 공급업체는 점유율을 유지했습니다.

북미는 확립된 상환규칙, 신속한 FDA 승인, 루틴 스크리닝량이 많아지면서 2024년에는 세계 매출의 45.26%를 차지했습니다. 그러나 이 지역에서는 COVID-19 검사의 수익이 감소함에 따라 예산의 압축에 직면하고 있으며, 검사 시설은 메뉴의 확대와 자동화의 가속을 강요하고 있습니다.

아시아태평양은 인프라 투자와 감염 부담 증가로 인해 2030년까지 연평균 복합 성장률(CAGR) 5.36%를 나타낼 것으로 예측됩니다. 중국, 인도, 일본의 정부 프로그램은 신속 뎅기열, mpox, 항균제 내성 패널에 보조금을 내고 도입주기를 단축하고 있습니다. 디지털 헬스 파일럿은 원격 키트를 원격 진단에 연결하여 지역에서의 보급을 촉진합니다.

유럽은 안정적인 수요를 유지하고 신드로믹 멀티플렉스의 채용을 선도. 그러나 항균제 관리에 관한 이니셔티브는 신속한 진단제를 도입하기 위해 병원에 계속 압력을 가하고 있습니다. 중동 및 아프리카 시장은 여전히 작지만 기증자 자금으로 업그레이드가 진행되고 있으며 감염증 진단 시장 내에서 지리적 다양화를 목표로하는 공급업체의 발판입니다.

The infectious disease diagnostics market stands at USD 46.81 billion in 2025 and is on course to reach USD 55.55 billion by 2030, growing at a 3.48% CAGR.

This steady trajectory shows how the infectious disease diagnostics market is moving from pandemic-driven demand toward long-term growth anchored in endemic disease management, climate-linked outbreaks, and ongoing technology upgrades. Spending is broadening beyond respiratory tests to include vector-borne, antimicrobial-resistant, and emerging pathogens, helping laboratories offset lower COVID-19 volumes. Reagent sales remain the revenue backbone, yet software-enabled workflow tools are scaling fast as labs seek automation efficiencies. Competitive intensity is rising because new entrants armed with CRISPR, isothermal, and AI capabilities are challenging incumbents for share in the infectious disease diagnostics market.

Vector-borne illnesses are climbing, with dengue cases running 15% above the five-year average in early 2025.Climate change is widening mosquito habitats, so providers now test for pathogens once restricted to the tropics. The World Health Organization classified mpox as a grade 3 emergency in August 2024, prompting a 160% jump in test demand over the prior year. Antimicrobial resistance adds pressure: the WHO's 2024 priority list highlights 15 resistant bacterial families that need rapid diagnostics. As new threats surface, laboratories must refresh menus frequently, creating recurring revenue for firms across the infectious disease diagnostics market.

Regulators are green-lighting consumer tests at pace. In August 2024 the FDA cleared the first OTC syphilis assay, ushering retail diagnostics into mainstream practice. Syphilis incidence rose 80% from 2018 to 2022, so community pharmacies and e-commerce portals now stock rapid kits. Cepheid's finger-stick hepatitis C test adds same-visit viral confirmation, closing care gaps in primary clinics. Payers value earlier therapy starts that reduce downstream costs, so reimbursement processes are catching up, even as coding complexity persists.

Payers insist on stringent coding before honoring claims, and the added paperwork stretches cash cycles for smaller labs. Government fee schedules, especially in low- and middle-income countries, rarely cover the full cost of advanced molecular platforms, limiting uptake. Laboratories in such settings rely on donor programs, slowing commercial momentum despite clear clinical need. Harmonized payment models would unlock wider adoption across the infectious disease diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Respiratory panels held 20.13% of infectious disease diagnostics market share in 2024, yet vector-borne and emerging pathogens are set to climb at a 5.78% CAGR to 2030. A record 13 million dengue cases in 2024-2025 forced hospitals to expand test menus. Mpox, hepatitis, HIV self-tests, and AI-assisted tuberculosis assays broaden the clinical mix. The infectious disease diagnostics market size attached to vector-borne testing will keep rising as global mobility and climate change alter transmission zones.

Growth relies on rapid antimicrobial susceptibility tools for hospital-acquired infections and FDA OTC clearances for STI home kits. Laboratories value platforms that update quickly when the WHO adds bacteria to its resistance list; such flexibility strengthens vendor stickiness inside the infectious disease diagnostics market.

Assays, kits, and reagents contributed 53.45% of infectious disease diagnostics market size in 2024 because consumables drive recurring revenue. Software and informatics, though smaller, will post the quickest 5.66% CAGR as labs digitize workflows. Instruments now compete on automation depth, sample-to-answer speed, and AI tie-ins rather than raw throughput alone.

Contract-testing services grow when hospitals outsource complex sequencing or drug-resistance panels. Cloud-based analytics link raw data to actionable reports, enhancing value per test. Vendors bundling reagents with informatics maintain share even as hardware margins tighten across the infectious disease diagnostics market.

The Infectious Disease Diagnostics Market Report is Segmented by Application (Hepatitis, HIV, and More), by Product & Service (Assays, Kits, & Reagents, and More), by Technology (PCR & QPCR, and More), End User (Hospital & Clinical Laboratories, and More), Test Setting (Laboratory-Based Testing, and More), Sample Type(Urine, Stool and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 45.26% of global revenue in 2024, supported by established reimbursement rules, fast FDA clearances, and high routine screening volume. However, the region is now confronting budget compression as COVID-19 testing revenues fade, prompting labs to broaden menus and accelerate automation.

Asia-Pacific is projected to grow at a 5.36% CAGR to 2030 owing to infrastructure investment and rising infectious-disease burdens. Government programs in China, India, and Japan subsidize rapid dengue, mpox, and antimicrobial-resistance panels, which shortens adoption cycles. Digital health pilots link remote kits to teleconsults, increasing reach in rural regions.

Europe maintains steady demand and leads syndromic multiplex adoption. Fragmented reimbursement and data-privacy legislation slow cross-border digital-health scaling, yet antimicrobial-stewardship initiatives keep pressure on hospitals to deploy rapid diagnostics. Middle East and Africa markets remain smaller but are receiving donor-funded upgrades that create footholds for suppliers seeking geographic diversification within the infectious disease diagnostics market.