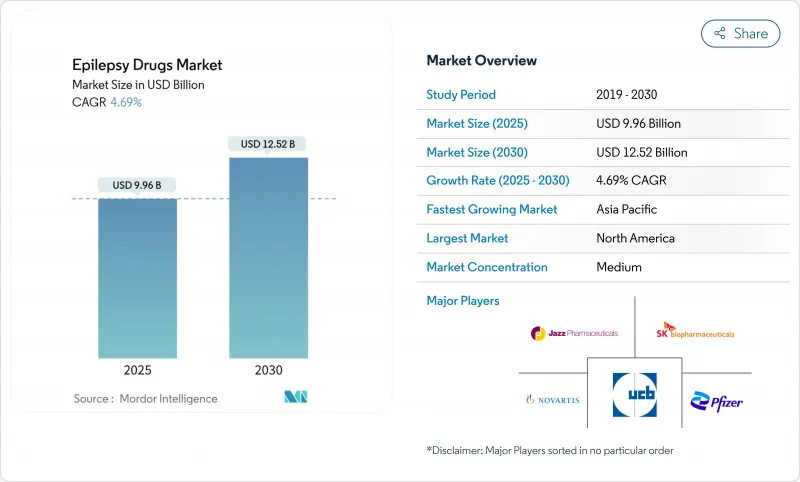

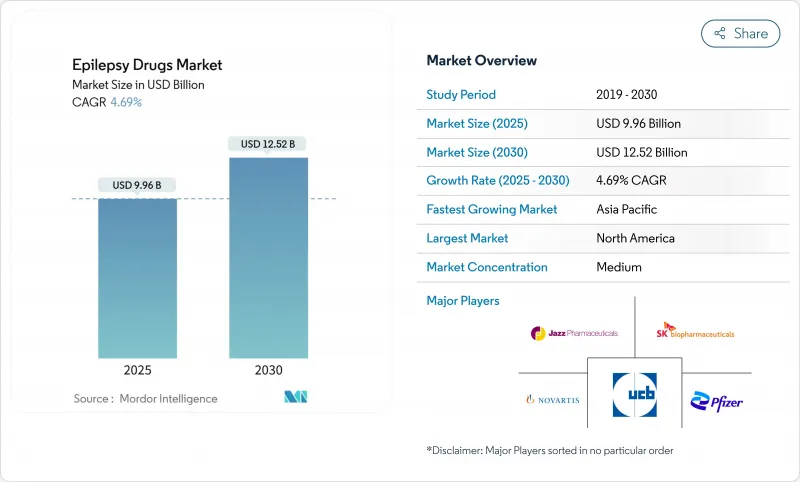

간질 치료제 시장의 2025년 시장 규모는 99억 6,000만 달러로, 2030년에는 125억 2,000만 달러에 이르고, CAGR 4.69%를 나타낼 것으로 예측됩니다.

이 성장은 3 세대 간질 약물의 상시 성공, 유전자 정밀 분석 도구의 급속한 보급, 복약 충동을 향상시키는 원격 신경학 서비스의 성장을 반영합니다. 국소 간질이나 치료제 내성 간질에 대해 의사가 보다 안전한 치료제를 요구하고 있기 때문에 수요는 증가의 일도를 따르고 있지만, 특허 부족이나 정기적인 원약 부족에 의한 가격 압력이, 매출액의 기세를 약화시키고 있습니다. 북미는 상환 범위가 넓기 때문에 리더십을 유지하고 있지만, 아시아태평양은 중국과 인도가 간질계발 캠페인에 투자하고 첨단 치료제에 대한 접근을 확대하고 있기 때문에 가장 강한 궤도를 보여주고 있습니다. 틈새 이노베이터가 희귀질환과 디지털 건강 생태계에서 점유율을 얻기 때문에 경쟁의 치열성이 커지고 있습니다.

세계 규제 당국은 세노바메이트, 브리바라세탐, 칸나비디올, 디아제팜 비강제 등 기존 약물보다 높은 발작 억제율과 적은 부작용을 보이는 차세대 약물을 차례로 승인하고 있습니다. SK Biopharmaceuticals는 2025년 1분기 Xcopri 매출이 전년 동기 대비 46.6% 증가한 1억 240만 달러로 급증했다고 보고했습니다. 2025년 미국 신경학회에서 발표된 실제 데이터에서는 세노바메이트로 치료한 성인의 초점 발작의 발작 중앙값이 84% 감소한 반면, 이스라엘의 관찰 연구에서는 같은 분자를 사용한 약물 저항성 환자의 발작 자유도가 27.5%였습니다. FDA는 2025년 4월, 디아제팜 점비약을 2-5세의 어린이에게도 확대하기로 결정해, 구조의 선택지가 퍼졌습니다. 이러한 진보를 종합하면 장기적인 결과 개선에 대한 기대가 높아지고 치료 저항성 사례를 새로운 요법으로 전환시키는 임상의가 박차를 받습니다.

인공지능 알고리즘이 수백만 건의 임상 기록을 분석하고, 전형적인 진단의 몇년전에 단발성 간질을 신고함으로써 보다 조기적이고 적절한 치료가 가능해졌습니다. 필라델피아 소아 병원은 3만 2,000명의 환자에서 얻은 8,900만 건의 주석을 스크리닝하고 유전성 간질을 3.6년 빨리 발견하는 모델을 검증했습니다. 전체 엑솜 시퀀싱에 의한 진단 적중률은 14%로, 그 중 59%가 정밀 치료와 일치하지만, 실제 도입은 상환 및 접근상의 이유로 아직 32%로 뒤처져 있습니다. 보험 상환의 범위가 확대되고, AI가 규제 당국의 먹이를 얻으면서, 임상의는 유전자형에 관한 지견과 제3세대의 치료제를 조합해 간질 치료제 시장 전체에서 맞춤형 치료의 길을 강화할 것으로 기대됩니다.

UCB의 빈팻을 비롯한 오랜 유력 제품은 독점적 보호의 해지와 함께 가파른 가격 하락에 직면해 있습니다. 연방거래위원회는 제네릭 의약품의 진입을 저지하거나 늦추는 업계의 수법을 조사하고, 절약분이 환자에게 도달하도록 주장하고 있습니다. 특허실효 후 1년 이내에 약가가 70% 이상 하락할 가능성도 있지만, 특허가 아직 유효한 혁신적인 치료제를 시험하도록 처방의를 촉구하고 풍부한 후기 파이프라인을 유지하는 기업으로 약가가 이동하고 있습니다.

3세대 화합물은 뛰어난 안전성과 듀얼 메커니즘 작용으로 2024년 간질 치료제 시장에서 39.64%의 점유율을 차지했습니다. 세노바메이트의 3상 데이터에서는 다양한 용량으로 12개월간의 발작 프리율이 25.8%였습니다. 이러한 진전으로 이 부문은 2030년까지 리드를 넓히는 반면, 2세대 치료제는 실제 사회에서의 폭넓은 익숙성과 양호한 부작용 프로파일을 배경으로 CAGR 6.32%를 나타낼 것으로 예측됩니다.

향후 3세대 약물과 정밀진단의 시너지 효과로 난치성 환자의 치료전환이 가속화되어 혁신자의 수익원이 될 가능성이 높습니다. 그럼에도 불구하고 자원이 제한된 환경에서는 잘 알려진 약동학과 저비용의 1세대 클래식 약물이 여전히 기축이며, 간질 치료제 시장에는 다층적인 상황이 유지되고 있습니다.

2024년 간질 치료제 시장 규모에서 차지하는 국소발작의 비율은 61.34%로 세계적으로 부분발작의 유병률이 높은 것을 반영했습니다. 첫 번째 선택 약물에는 라모트리긴과 레베티라세탐이 포함되며, 카르바마제핀은 비용에 민감한 지역에서 널리 받아들여집니다.

분류되지 않은/복합형 발작 부문은 예측 기간 동안 5.98%의 성장률을 보일 것으로 예측됩니다. 유전체 조사는 국소 간질과 일반 간질의 아키텍처가 다르다는 것을 밝혀내고 파이프라인 개발자에게 새로운 목표를 제공합니다. 정밀 스크리닝이 일상적으로 이루어지면 임상의는 초점 간질의 서브그룹 내에서도 치료를 미세 조정할 수 있게 되어, 간질 시장 전체에서의 판매량 증가와 복약 준수의 향상이 기대됩니다.

북미는 종합적인 보험 적용, 전문의 밀도, 3세대 제품의 급속한 보급으로 2024년 간질 시장에서 40.02%의 점유율을 차지했습니다. 2025년 1분기에 46.6%의 매출을 기록한 Xcopri는 이 지역의 차별화 치료에 대한 의욕을 뒷받침하고 있습니다. 규제의 유연성은 어드히어런스를 향상시키는 원격 의료 처방 업데이트를 지원하지만 비용 억제 정책이 가격 하락 압력을 낳고 2030년까지의 CAGR은 3.96%를 나타낼 전망입니다.

아시아태평양은 정부가 공중 보건 예산을 확대하고 진단 인프라를 확충하기 때문에 CAGR 가장 빠른 5.98%를 나타낼 전망입니다. 큰 진전에도 불구하고, 중국의 치료 격차는 여전히 계속되고 있으며, 브랜드 제품과 품질 보증 된 제네릭 의약품에 잠재적인 비즈니스 기회가 있음이 돋보입니다. 일본에서는 칸나비디올 제제의 후기 임상시험이, 인도에서는 현지 제조를 위한 대처가 이 지역의 제품 라인업을 다양화하여 간질 치료제 시장의 성장을 가속시키고 있습니다.

유럽은 기술 혁신과 엄격한 비용 관리의 균형을 유지하고 CAGR은 4.35%를 나타낼 전망입니다. SK Biopharmaceuticals는 Angelini사를 통해 유럽 23개국에서 세노바메이트를 판매하고 있으며, 난치성 사례로의 침투를 도모하고 있습니다. 남미와 중동, 아프리카는 규모가 작고 원격 의료 파일럿과 자원이 제한된 환경에 맞는 실용적인 진단 가이드라인을 추진하고 있습니다. 이러한 이니셔티브는 인지도 향상, 스티그마 완화, 신흥국 간질 시장의 확대를 기대합니다.

The anti-epileptic drugs market is valued at USD 9.96 billion in 2025 and is forecast to reach USD 12.52 billion by 2030, expanding at a 4.69% CAGR.

This advance reflects the successful launch of third-generation antiseizure medicines, fast adoption of genetic precision tools, and the growth of tele-neurology services that improve adherence. Demand keeps rising as physicians seek safer agents for focal seizures and drug-resistant epilepsy, yet pricing pressure from patent expirations and periodic API shortages temper topline momentum. North America retains leadership through deep reimbursement coverage, while Asia-Pacific shows the strongest trajectory as China and India invest in epilepsy awareness campaigns and broaden access to advanced therapies. Competitive intensity is sharpening because niche innovators are winning share in orphan indications and digital-health ecosystems.

Global regulators are clearing a steady stream of next-wave agents such as cenobamate, brivaracetam, cannabidiol and diazepam nasal formulations that demonstrate higher seizure-reduction rates and fewer adverse reactions than legacy drugs. SK Biopharmaceuticals reported a 46.6% year-on-year jump in Xcopri sales to USD 102.4 million during Q1 2025. Real-world data presented at the 2025 American Academy of Neurology meeting showed an 84% median seizure cut in focal-seizure adults treated with cenobamate, while an Israeli observational study cited 27.5% seizure freedom among pharmaco-resistant patients using the same molecule. The FDA's April 2025 decision to extend diazepam nasal spray to children aged 2-5 broadens rescue options. Collectively these advances raise expectations for better long-term outcomes and spur clinicians to transition treatment-resistant cases onto newer regimens.

Artificial-intelligence algorithms now parse millions of clinical records to flag monogenic epilepsies years before typical diagnosis, enabling earlier and more appropriate therapy. Children's Hospital of Philadelphia validated a model that detects genetic epilepsies 3.6 years sooner by screening 89 million annotations from 32,000 patients. Whole-exome sequencing yields a 14% diagnostic hit rate, and 59% of those findings align with precision therapies, though real-world uptake still lags at 32% for reimbursement and access reasons. As payer coverage widens and AI achieves regulatory endorsement, clinicians are expected to pair genotype insights with third-generation drugs, reinforcing personalized care pathways across the anti-epileptic drugs market.

UCB's Vimpat and several other long-standing leaders face steep price drops as exclusive protections lapse. The Federal Trade Commission is scrutinizing industry tactics to block or delay generic entry and insists that savings reach patients. While erosion can exceed 70% within the first year post-expiry, it also pushes prescribers to experiment with innovative agents still under patent, shifting volume toward companies that maintain rich late-stage pipelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Third-generation compounds dominated with 39.64% share of the anti-epileptic drugs market in 2024 thanks to superior safety and dual-mechanism action. Cenobamate's phase 3 data showed 25.8% seizure freedom over 12 months across varied doses. This progress underpins a forecast in which the segment broadens its lead through 2030, while second-generation agents grow at 6.32% CAGR on the back of extensive real-world familiarity and favorable side-effect profiles.

Moving forward, synergy between third-generation drugs and precision diagnostics will likely speed therapy switches for refractory patients, anchoring revenue streams for innovators. Even so, first-generation staples remain cornerstones in resource-limited settings because of well-known pharmacokinetics and low cost, preserving a multi-tier landscape within the anti-epileptic drugs market.

Focal seizures accounted for 61.34% of anti-epileptic drugs market size in 2024, a position that mirrors the higher prevalence of partial-onset conditions globally. First-line choices include lamotrigine and levetiracetam, while carbamazepine retains broad acceptance in cost-sensitive regions.

Unclassified/Combined Seizures segment is anticipated to record a 5.98% growth rate during the forecast period. Genomic research reveals distinct architectures for focal versus generalized epilepsies, giving pipeline developers fresh targets. As precision screening becomes routine, clinicians expect to fine-tune therapy even within the focal subgroup, yielding incremental volume growth and higher adherence across the anti-epileptic drugs market.

The Epilepsy Drugs Market Report is Segmented by Drug Generation (First Generation Anti-Epileptics and More), Seizure Type (Focal Seizures and More), Patient Type (Adult and Pediatric), Route of Administration (Oral and More), Distribution Channel (Hospital Pharmacy and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America held a 40.02% share of the anti-epileptic drugs market in 2024 due to comprehensive insurance coverage, specialist density, and rapid uptake of third-generation products. Xcopri's 46.6% sales surge in Q1 2025 underscores the region's appetite for differentiated therapies. Regulatory flexibility supports tele-health prescription renewal programs that improve adherence, yet cost-containment policies create downward price pressure and keep CAGR at 3.96% through 2030.

Asia-Pacific exhibits the fastest 5.98% CAGR as governments scale public health budgets and widen diagnostic infrastructure. Despite sizable progress, China's treatment gap persists, underscoring latent opportunity for branded and quality-assured generics. Japan's late-stage trials for cannabidiol formulations and India's push toward local manufacturing diversify the regional offer set and accelerate growth within the anti-epileptic drugs market.

Europe balances innovation against stringent cost controls, producing a steady 4.35% CAGR. SK Biopharmaceuticals markets cenobamate in 23 European countries via Angelini, seeking higher penetration of refractory cases. South America and the Middle East & Africa, while smaller, advance on telemedicine pilots and pragmatic diagnostic guidelines tailored to resource-limited settings. These efforts collectively raise awareness, reduce stigma, and expand the anti-epileptic drugs market footprint across emerging economies.