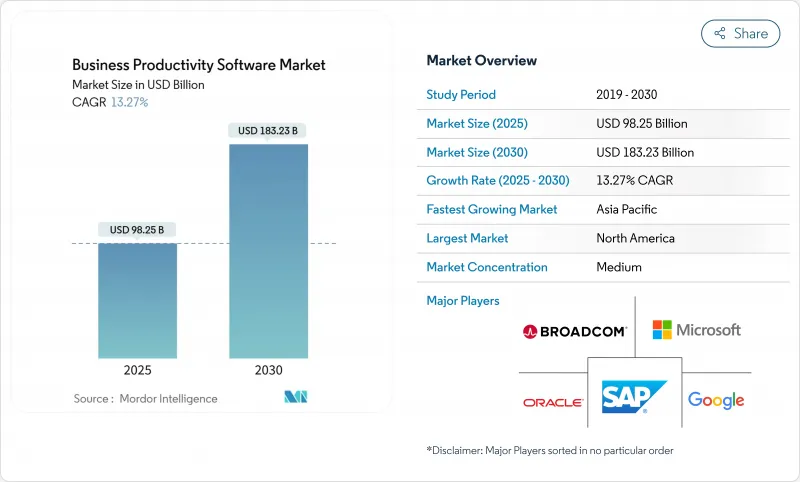

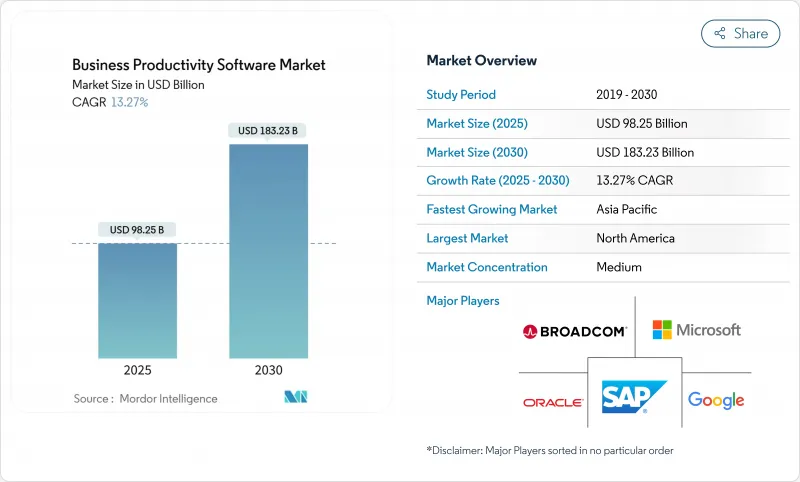

비즈니스 생산성 소프트웨어 시장은 2025년에 982억 5,000만 달러, 2030년에는 1,832억 3,000만 달러에 이를 전망이며, 예측 기간의 CAGR은 13.3%로 견조하게 성장할 전망입니다.

생성형 AI는 현재 최신 생산성 제품군의 핵심을 차지하고 있으며, Microsoft는 Copilot의 배포 후 개별 작업의 완료 속도가 75% 향상되었다고 밝혔고 기업의 조기 채용자의 3년간의 ROI가 112%로 나타났습니다. 하이퍼스케일러를 통한 클라우드 인프라 커미트먼트, 새로운 하이브리드 워크 의무화, 보다 엄격한 데이터 거버넌스 법률이 플랫폼 업데이트 사이클을 가속화하고 있습니다. 많은 업계에서는 기밀성이 높은 워크로드를 사내에서 관리해야 하기 때문에 현재도 On-Premise의 도입이 매출의 대부분을 차지하고 있지만, 지출의 기세가 가장 빠른 분야는 소버린 클라우드 지역과 소비 기반의 가격 모델입니다. 플랫폼 공급업체의 보고에 따르면 임베디드 컴플라이언스 자동화, 지역별 데이터 레지던시 관리, 그리고 비기술 직원이 루틴 워크를 효율화할 수 있는 로우코드 툴킷에 대한 요구가 급증하고 있습니다. 동시에 협업 트래픽도 폭발적으로 증가하고 있습니다. Microsoft Teams의 일일 액티브 사용자는 3억 명을 돌파했으며, 기업은 Teams와 Slack을 병렬로 활용하여 팀의 다양한 취향을 충족시키는 경우가 늘고 있습니다.

엔터프라이즈 구매 패턴은 클라우드 네이티브 서비스를 선호하며 핵심 IT뿐만 아니라 재무, 인사 및 운영 팀에도 확산되어 있습니다. Microsoft Azure는 2024년 전년 대비 30%의 매출 증가를 기록했으며 Google Cloud는 Workspace 배포와 직접 관련된 Vertex AI 사용이 20배로 급증했다고 밝혔습니다. 맞춤형 On-Premise 모듈을 표준화된 SaaS 제품군으로 대체한 조직에서는 총 소유 비용이 두 자리 감소하였고 릴리스 사이클이 현저히 빨라졌다는 보고가 일상적으로 이루어지고 있습니다. 점점 더 엄격해지는 데이터 거버넌스의 법적 규제도 그 기세를 약화시키지 못했습니다. 대신 공급자는 지역별 인스턴스, 자동화된 감사 추적 및 고객이 관리하는 암호화 키를 통해 주권에 대한 수요를 처리합니다. 그 결과, 이전에는 오프 프리미어 스토리지를 양도할 수 없다고 생각했던 업계에서도 클라우드 구독 수익에 결정적으로 기울고 있음이 드러나고 있습니다.

일반 AI는 실험적인 파일럿에서 일상적인 작업 환경으로 전환했습니다. Microsoft의 코파일럿은 요약 초안, 프레젠테이션 생성, 긴 이메일 스레드를 수초 안에 캡처할 수 있으며 앞서 언급한 75%의 작업 시간 절감을 지원합니다. 구글은 Gemini를 도입한 작업공간 계획에 대해 AI 기능을 기본 구독 요금에 통합하여 광범위한 롤아웃 비용 장벽을 낮춥니다. Oracle은 Fusion Data Intelligence에 대화형 분석을 통합하여 재무 사용자가 평이한 단어로 원장을 쿼리할 수 있도록 합니다. 이렇게 코파일럿이 성숙함에 따라 구매자는 오피스 스위트의 핵심 기능보다 모델 투명성, 거버넌스 도구 및 프롬프트 엔지니어링의 용이성으로 공급업체를 평가하게 되었습니다.

각국 정부는 해외공급자에게 국내에서의 정보의 보존과 처리를 의무화하는 현지화의 의무화를 강화하고 있습니다. EU 데이터 법의 역외 적용은 시행이 시작되면 미국의 디지털 서비스 수출 총액을 2% 줄일 수 있습니다. 중국과 인도에서도 비슷한 규제가 있으며, 클라우드 사업자는 물리적으로 독립적인 시설을 설치하고 국내 감사를 받을 의무가 있습니다. 생산성 향상 제품군은 실시간 협업과 세계 AI 모델 교육에 크게 의존하기 때문에 데이터 아일랜드를 분할하는 것은 자본 비용과 운영 복잡성을 모두 증가시킵니다.

On-Premise 비즈니스 생산성 소프트웨어 시장의 규모는 2024년 매출의 68.4%를 차지하였으며, 근본적으로 금융, 방위 및 행정에 엄격한 데이터 위치 정책이 적용되고 있습니다. 그러나 클라우드 구독은 하이퍼스케일러가 대규모 언어 모델(LLM) 워크로드용으로 설계된 고성능 GPU 클러스터를 추가함에 따라 CAGR 15.0%로 모든 배포 모델 중 가장 빠른 속도로 성장하고 있습니다. 조직은 하이브리드 아키텍처를 선택하는 경향이 강해지고, 보호된 데이터 세트를 프라이빗 클러스터에 저장하는 한편, 클라우드 AI를 활용하여 실시간 번역, 문서 요약을 실시했습니다. 클라우드 급 실리콘 및 관리형 ML 도구를 로컬로 복제하는 것은 경제적이지 않으므로 CIO는 예측 기간 동안 순수한 On-Premise 규모가 축소될 것으로 예상했습니다.

클라우드 도입의 2차적인 장점으로는 재해 복구 시간의 단축, 계절적인 수요 급증시에 라이선스를 재이용할 수 있는 것 등을 들 수 있습니다. 공급업체는 현재 컴플라이언스 대시보드, 테넌트 수준의 암호화 관리 및 제로 트러스트 액세스 제어를 번들로 제공하여 주권에 대한 이전의 반대 의견을 완화하고 있습니다. 더 많은 규제 프레임워크가 공인 클라우드 영역을 공식적으로 받아들일수록 미래를 기대하는 조달 정책은 '클라우드 우선'으로 이동하고 베어 메탈 설치는 레거시 에지 케이스에 머무르고 있습니다.

대기업은 방대한 시트 수와 다중 스위트 계약 갱신으로 2024년 총 지출액의 70.5%를 창출했습니다. 그럼에도 불구하고 중소기업층은 14.7%의 연평균 복합 성장률(CAGR)을 보였으며 다른 모든 고객층을 능가하고 기존 기업의 엔터프라이즈 편중 수익 구성을 점차 잠식하고 있습니다. 중소기업의 비즈니스 생산성 소프트웨어 시장의 규모는 사용량에 연동된 과금으로부터 직접 이익을 얻고 있으며, 팀은 매월 약간의 AI 어시스트로 시작하여 ROI가 증가함에 따라 확대할 수 있습니다.

중소기업은 또한 레거시 부담을 최소화할 수 있으므로 최첨단 AI를 보다 빠르게 도입할 수 있습니다. 소매업의 신흥기업은 수주 내에 상품 카탈로그 전체에 대화형 검색을 통합할 수 있지만 세계 소매업체는 먼저 병렬 데이터 레이크를 조정해야 합니다. 이러한 차이에 민감한 공급업체는 재고 매칭, 시프트 스케줄, 비용 승인 등 거의 설정이 필요하지 않은 턴키 템플릿을 제공합니다. 이 "최소한 관리"라는 아이디어는 주로 전임 IT 지원이 부족한 중소기업에게 매력적입니다.

비즈니스 생산성 소프트웨어 시장 보고서는 배포(On-Premise 및 클라우드), 조직 규모(대기업 및 중소기업), 최종 사용자 업계(은행, 금융서비스 및 보험(BFSI), 통신 및 IT 등), 솔루션 유형(컨텐츠 협업 및 문서 관리, 통신 및 통합 커뮤니케이션 등) 및 지역별로 분류됩니다.

북미는 2024년 세계 매출의 36.4%를 차지하였습니다. 풍부한 클라우드 인프라, 성숙한 SaaS 조달 문화, 기록적인 하이퍼스케일러 설비 투자(마이크로소프트만으로 2026년까지 800억 달러를 AI 데이터센터에 투자할 예정)에 의해 이 지역이 새로운 기능의 주요 시험장으로 유지되고 있습니다. 공공 부문의 디지털 근대화 보조금은 주와 지방 기관을 위한 안전한 협업을 조성함으로써 리드를 더욱 확대하고 있습니다. 캐나다와 멕시코는 국경을 넘는 공급망 프로그램이 공유 문서 워크플로 플랫폼에서 표준화됨에 따라 상승이 예상됩니다.

유럽은 크게 다른 규제 환경 하에서 꾸준한 성장을 유지하고 있습니다. GDPR(EU 개인정보보호규정)과 EU 데이터 규정은 세분화된 데이터 이식성 관리와 위치 기반 라우팅을 제공하도록 공급업체를 지원합니다. 컴플라이언스 오버헤드로 인해 클라우드 마이그레이션이 지연되는 경우도 있지만, 동시에 전용 거버넌스 모듈에 대한 수요도 높아지고 있습니다. 대륙의 바이어들은 오픈소스 기반과 현지 시설에 수용된 소버린 LLM에 대한 관심을 높이고 있습니다.

아시아태평양은 인도, 인도네시아, 필리핀의 디지털 공공 인프라 구상으로 수백만의 중소기업이 새롭게 온라인화되기 때문에 2030년까지의 CAGR이 14.0%가 될 것으로 예측되며 가장 급성장하고 있는 지역입니다. 한국의 기업은 모바일 퍼스트의 워크플레이스 도입의 선두를 달리고 있으며 이동이 많은 팀을 위해 메시징 클라이언트에 AI 트랜스크립션을 포함하고 있습니다. 일본의 첨단 로봇 산업은 AI를 활용한 스프레드시트 스크립트로 생산 데이터를 ERP 시스템과 융합시켜 다운타임을 절감합니다. 중국은 우대 조달과 엄격한 데이터 수출 규제를 통해 국내 벤더를 계속 장려하고 있으며, 그 결과 다국적 기업이 견인력을 얻기 위해서는 현지 클라우드 사업자와 제휴해야 하는 이중구조 시장이 되고 있습니다.

남미에서는 현재 절대 투자가 감소하고 있지만 미래 가치는 높습니다. 브라질 정부는 보안 문서 교환을 의무화하는 오픈 뱅킹과 전자 송장의 표준화에 투자하고 있으며 간접적으로 협업 스위트의 도입에 박차를 가하고 있습니다. 아르헨티나는 환율 변동이 심하고, 자본 설비의 구입에는 높은 헤지 리스크가 수반하기 때문에 달러형 SaaS에 대한 의욕이 높아지고 있습니다. 마지막으로 중동 및 아프리카에서는 국가 주도의 스마트 시티 계획에 원격 워크의 허브가 포함되어 있는 사우디아라비아와 UAE, 모바일 광대역의 보급에 의해 경량으로 대역폭을 절약할 수 있는 생산성 앱이 장려되고 있는 남아프리카와 나이지리아의 회랑 주변에 수요가 집중되고 있습니다.

The business productivity software market stood at USD 98.25 billion in 2025 and is on track to reach USD 183.23 billion by 2030, reflecting a solid 13.3% CAGR over the forecast period.

Generative AI now sits at the core of modern productivity suites, with Microsoft recording 75% gains in individual task completion speeds after Copilot roll-outs and modelling a 112% three-year ROI for early enterprise adopters. Cloud infrastructure commitments from hyperscalers, fresh hybrid-work mandates, and stricter data-governance laws collectively accelerate platform refresh cycles. On-premise deployments still dominate revenue today because many sectors must keep sensitive workloads in-house, yet the fastest spending momentum clearly tilts toward sovereign-ready cloud regions and consumption-based pricing models. Platform vendors report a sharp rise in requests for built-in compliance automation, regional data-residency controls, and low-code toolkits that let non-technical staff streamline routine work. At the same time, collaboration traffic is exploding: Microsoft Teams has surpassed 300 million daily active users while enterprises increasingly run Teams and Slack side-by-side to satisfy diverse team preferences.

Enterprise buying patterns now prioritise cloud-native services, extending well beyond core IT into finance, HR, and operations teams. Microsoft Azure posted 30% year-on-year revenue growth in 2024, and Google Cloud highlighted a 20-fold jump in Vertex AI usage tied directly to Workspace deployments. Cost advantages remain compelling: organisations that replace bespoke on-premise modules with standardised SaaS suites routinely report double-digit reductions in total ownership costs and noticeably faster release cycles. Increasingly stringent data-governance statutes have not slowed momentum; instead, providers answer sovereignty demands with region-specific instances, automated audit trails, and customer-managed encryption keys. The upshot is a decisive tilt toward cloud subscription revenue even inside industries that once viewed off-prem storage as non-negotiable.

Generative AI has moved from experimental pilots to the day-to-day work fabric. Microsoft's Copilot can draft summaries, generate presentations, and ingest long e-mail threads in seconds, underpinning the 75% task-time reduction noted above. Google counters with Gemini-infused Workspace plans that wrap AI functionality into the base subscription fee, removing a cost barrier for broad roll-outs. Oracle has embedded conversational analytics inside Fusion Data Intelligence so finance users can query ledgers in plain language. As these copilots mature, buyers increasingly evaluate vendors on model transparency, governance tooling, and ease of prompt engineering rather than on core office-suite features.

Governments are tightening localisation mandates that obligate foreign providers to store and process information domestically. The EU Data Act's extraterritorial reach could shave 2% off total US digital-services exports once enforcement begins. Similar frameworks in China and India require cloud operators to set up physically separate facilities and subject them to in-country audits. Productivity suites rely heavily on real-time collaboration and global AI model training, so splitting data islands drives both capital costs and operational complexity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The business productivity software market size for on-premise installations commanded 68.4% of 2024 revenue, a share rooted in strict data-location policies inside finance, defence, and public administration. Yet cloud subscriptions are progressing at a 15.0% CAGR, the fastest of any deployment model, as hyperscalers add high-performance GPU clusters designed for large language model (LLM) workloads. Organisations increasingly select hybrid architectures, keeping protected datasets in private clusters while exploiting cloud AI for real-time transcription, translation, and document summarisation. Over the forecast window, CIOs expect purely on-premise estates to shrink because replicating cloud-grade silicon and managed ML tooling locally is uneconomical.

Cloud adoption's second-order benefits include faster disaster-recovery times and pooled license reuse during seasonal demand spikes. Vendors now bundle compliance dashboards, tenant-level encryption management, and zero-trust access controls, alleviating earlier objections around sovereignty. As more regulatory frameworks formally accept certified cloud regions, forward-looking procurement policies pivot to "cloud-preferred," relegating bare-metal installs to legacy edge cases.

Large enterprises generated 70.5% of the total 2024 spend thanks to expansive seat counts and multi-suite contract renewals. Nevertheless, the SME cohort demonstrates a 14.7% CAGR that outpaces every other customer tier, gradually eroding incumbents' enterprise-heavy revenue mix. The business productivity software market size for SMEs benefits directly from usage-linked billing, where teams can start with a handful of AI assists per month and expand as ROI becomes visible.

Smaller firms also adopt bleeding-edge AI faster because they carry minimal legacy baggage. A retail start-up can embed conversational search across its product catalogue within weeks, whereas a global retailer must reconcile parallel data lakes first. Vendors attuned to these differences now ship turnkey templates-inventory reconciliations, shift scheduling, expense approvals-that require almost no configuration. This "minimal-admin" ethos appeals to SMEs that often lack dedicated IT support.

The Business Productivity Software Market Report is Segmented by Deployment (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, Telecommunications and IT, and More), Solution Type (Content Collaboration and Document Management, Communication and Unified Communications, and More), and Geography.

North America generated 36.4% of global revenue in 2024. Deep cloud-infrastructure footprints, a mature SaaS procurement culture, and record hyperscaler capex-Microsoft alone is funnelling USD 80 billion into AI datacentres through 2026-ensure the region remains the primary launchpad for new functionality. Public-sector digital-modernisation grants further widen the lead by subsidising secure collaboration for state and local agencies. Canada and Mexico contribute incremental upside as cross-border supply-chain programmes standardise on shared document-workflow platforms.

Europe maintains steady growth under a vastly different regulatory climate. GDPR and the EU Data Act together push vendors to provide granular data-portability controls and location-based routing. While compliance overhead slows some cloud migrations, it simultaneously catalyses demand for purpose-built governance modules. Continental buyers also show heightened interest in open-source underpinnings and sovereign LLMs housed in local facilities.

Asia-Pacific is the fastest-rising territory, projected at a 14.0% CAGR through 2030 as digital-public-infrastructure initiatives across India, Indonesia, and the Philippines bring millions of new small businesses online. Korean organisations spearhead mobile-first workplace adoption, embedding AI transcription inside messaging clients for on-the-move teams. Japan's advanced robotics sector uses AI-enhanced spreadsheet scripts to blend production data with ERP systems, trimming downtime. China continues to encourage domestic vendors through preferential procurement and strict data-export rules, resulting in a dual-track market where multinationals must partner with local cloud operators to gain traction.

South America registers lower absolute spend today, but has a robust runway. Brazil's government is investing in open banking and e-invoicing standards that mandate secure document exchange, indirectly spurring collaboration-suite deployments. Argentina's currency volatility increases the appetite for SaaS denominated in US dollars because capital equipment buys carry higher hedging risk. Finally, the Middle East and Africa cluster demand around Saudi Arabia and the UAE, where state-sponsored smart-city plans incorporate remote-working hubs, and around South Africa-Nigeria corridors, where mobile broadband growth encourages lightweight, bandwidth-frugal productivity apps.