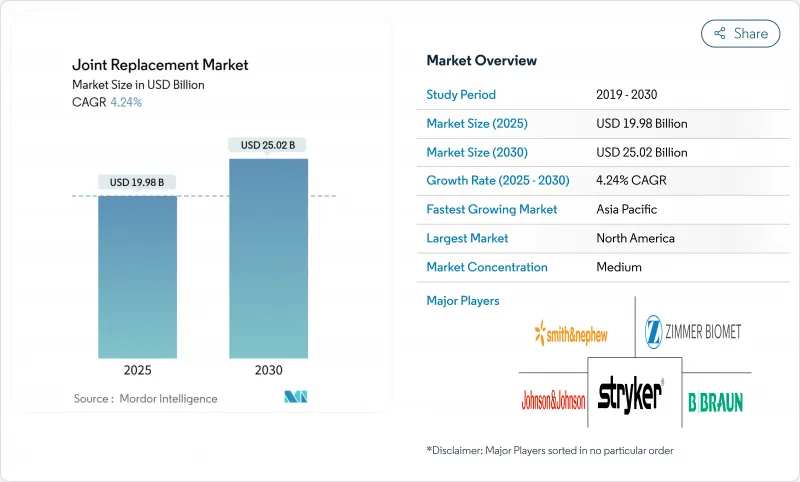

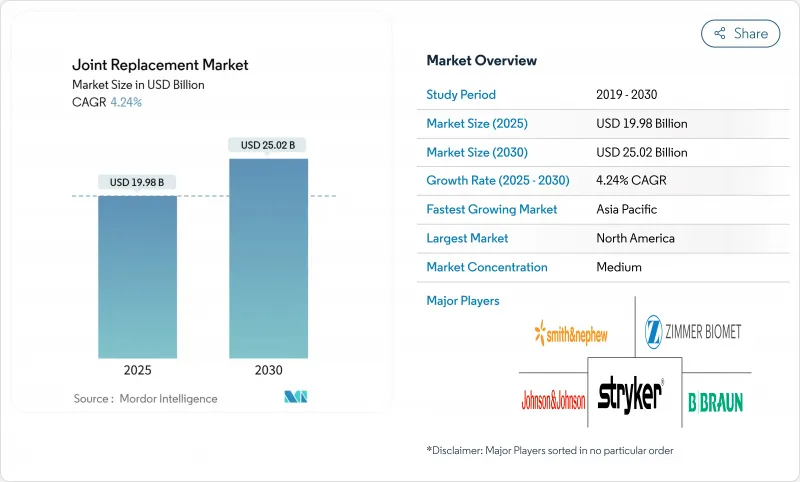

관절 치환술 시장 규모는 2025년에 199억 8,000만 달러, 예측 기간(2025-2030년)의 CAGR은 4.24%를 나타내고, 2030년에는 250억 2,000만 달러에 달할 것으로 예측됩니다.

인구동태의 고령화, 라이프스타일로 인한 변형성 관절증, 지속적인 임플란트의 기술 혁신이 혼재하는 것으로, 이 완만한 성장이 유지되는 한편, 수술 프로토콜의 급속한 전환이 강요되고 있습니다. 미국에서는 로봇 지원 시스템이 무릎 관절 전치환술의 두 자리대 점유율을 획득하여 당일 퇴원으로의 이행을 촉구하고 있습니다. 금속 인공 슬관절이 여전히 주류를 차지하고 있지만, 마모가 적고 금속 이온에 노출되지 않는 인공 슬관절을 원하는 젊은 활동적인 환자들 사이에서 세라믹 인공 슬관절의 인기가 높아지고 있습니다. 지역별로는 북미가 이용률로 선도하고 있는 반면 아시아태평양은 각국 정부가 정형외과 의료설비에 투자하고 보험상환을 확대하고 있기 때문에 가장 급속히 확대하고 있는 지역입니다.

골관절염은 미국에서 3,250만 명, 세계에서 6억 650만 명의 성인을 앓고 있습니다. 무릎 관절 질환만으로 전체 사례의 절반 이상을 차지하고 있으며, 엄청난 수의 잠재적 수술 후보자가 존재합니다. 미국에서는 변형성 무릎관절증과 직접 관련되는 약 100만 건의 무릎관절과 고관절 치환술로 연간 1,368억 달러의 경제적 부담이 발생하고 있습니다. 변형성 무릎 관절증으로 진단된 사람의 절반 이상이 결국 인공 슬관절 전치환술을 받고 있으며 임플란트의 구조적 수요 곡선을 지원합니다.

1차 인공 고관절 치환술은 2030년까지 57만 2,000건, 1차 인공 슬관절 치환술은 348만 건에 이를 것으로 예측되며, 2005년 대비 174%, 673%증가한 수치입니다. 고관절과 무릎 관절의 재치환술은 노후된 임플란트가 수명을 맞이하는 것과 병행하여 증가하여 의료 시스템에 대한 부담이 증가합니다. 신흥국은 이 패턴을 반영하고 있으며, 콜롬비아에서는 2050년까지 3만 9,270건의 하지 인공관절 치환술을 실시하여 여성이 52.7%를 차지할 것으로 예측됩니다. 노인 환자는 종종 합병증이 많기 때문에 의료 제공업체는 회복 시간을 단축할 수 있는 침습이 적은 절차를 선호합니다. 또한, 지불측도 외래에서의 치료를 장려하고 있습니다. 메디케어의 인공관절 치환술의 72%는 이미 외래에서 행해지고 있어 5년전에는 거의 행해지지 않았지만, 지금은 급증하고 있습니다.

메디케어에 의한 인공 고관절 전치환술의 상환액은 계속 떨어지고 마진을 압박하고 있습니다. 프랑스는 2025년부터 정형외과용 기구의 가격을 25% 낮추도록 의무화했고, 이익이 줄어들면서 제품 부족의 위험이 있습니다. 미국에서는 위험을 분배할 수 있는 대규모 비영리 병원을 우대하고 소규모 의료 제공업체는 취약한 입장에 놓여 있습니다. 정형외과의 외상진료보상은 20년간 3분의 1로 감소했고, 인플레이션율을 크게 밑돌았습니다. 외래의료센터는 유의한 비용 절감을 실현하는 한편, 제조업체에 마진 압력을 가해 경쟁을 격화시키고 있습니다.

무릎 관절 수술은 변형성 무릎 관절증의 높은 유병률과 확립된 임상 경로에 지지되어 2024년 매출의 39.54%를 차지했습니다. 어깨 관절 성형술은 CAGR 5.50%에서 가장 급성장하고 있는 카테고리로, 60세 미만의 환자에서의 스포츠 부상 증가, 관절와의 설치 실수를 줄이는 로봇 지침의 등장이 자극이 되고 있습니다. 인공 고관절 치환술의 건수는 2023년에는 3.8% 증가한 79만 3,082건이지만, 발관절과 팔꿈치 관절의 수술은 틈새이면서 임플란트의 적응을 확대하는 3D 프린터에 의한 환자 전용 디바이스의 혜택을 받고 있습니다. Zimmer Biomet의 시멘트리스 Oxford 임플란트는 10년 생존율 94.1%를 달성했습니다. 이러한 수술의 유형은 성숙하면서도 기술 혁신에 견인되어 시장정세를 진화시키고 있습니다.

단과형 인공 슬관절 치환술의 급속한 보급은 뼈를 보존하고 재활을 가속화하려는 외과 의사의 의욕을 반영합니다. VELYS와 같은 로봇 정렬 도구는 기존의 사용을 제한했던 어려운 기술 습득 곡선의 극복을 목표로합니다. 반면에 재치환 수술 수요가 증가함에 따라 복잡한 재치환 수술에 대한 교육의 필요성이 증가하고 수술을 많이 수행하는 관절성형술 전문의에 대한 병원 의존도가 높아지고 있습니다. 이러한 역학은 2030년까지 병원의 자원 계획과 지불자 협상에 계속 영향을 미치는 내구성 있는 수술 구성을 지원하고 있습니다.

금속 임플란트는 입증된 피로 강도와 가공의 용이성으로 인해 2024년에는 47.87%의 매출을 유지했습니다. 그러나 환자들이 마모가 적고 이온 방출이 없는 소재를 선호함에 따라, 세라믹은 CAGR 10.93%로 확대될 전망입니다. 티타늄 합금은 코발트 크롬보다 효과적으로 인공 고관절 주위의 골밀도를 유지하기 때문에 1차 및 재치환 수술 수준 모두에서 티타늄 기반 시스템의 관절 치환술 시장 규모를 지원합니다. BIOLOX 델타힙 베어링은 생존율이 우수하고 알레르기 반응도 매우 적으며 세라믹에 설득력 있는 가치 제안을 제공합니다. 폴리머와 메탈의 하이브리드와 생체 흡수성 스캐폴드도 복잡한 재치환술과 젊은 성인의 외상으로 주목을 받고 있어 제품 파이프라인의 다양화를 시사하고 있습니다.

금속 과민증은 니켈 프리 및 코발트 프리 대체품과 이온 방출을 억제하는 고급 코팅의 연구 개발을 뒷받침하고 있습니다. 스미스 앤 네퓨사의 옥시늄 표면 치환형 솔루션은 20년 생존율이 94.1%로 기존 합금보다 재치환이 35% 적다는 것을 입증했습니다. 공급자는 수술 부위의 감염과 싸우기 위해 항균성은 코팅을 골절 플레이트 및 기구 트레이에 추가합니다. 이러한 기술 혁신은 재료 선호의 계층을 재정의하고 미래 관절 치환술 시장 점유율의 궤적에 영향을 미칠 것으로 보입니다.

북미는 2024년 매출의 41.11%를 차지했으며 연간 215만 건 이상의 인공 고관절 치환술과 인공 슬관절 치환술에 지지되고 있습니다. 그러나 44% 이상의 진료 보상의 하향 조정으로 병원은 수술실의 효율화와 임플란트의 가격 협상에 두 발을 밟고 있습니다.

유럽에서는 규제 환경이 정비되어 적용 범위도 넓지만, 특히 프랑스에서는 2025년부터 기기 가격이 25% 인하되는 등 상환 가격 인하가 수익성을 압박하고 있습니다. 독일, 영국, 이탈리아는 높은 수술 건수를 기록하고 있지만, 원재료의 주권에 관한 EU의 폭넓은 논의가 티타늄과 코발트의 리쇼어링에 박차를 가하고 있습니다. 세라믹 베어링과 고관절 부분 표면 치환술에 대한 외과의의 쾌적성이 높은 것이 유럽의 임상 실천을 차별화하고 있습니다.

아시아태평양은 CAGR 9.92%로 가장 급속히 확대되고 있는 지역입니다. 중국의 티타늄 산업 허브인 다카이케는 세계 생산의 33%에 기여해 국내 임플란트의 성장을 지지하고 있습니다. 일본의 센터가 로봇의 도입을 리드하는 한편, 인도는 생산 연동 인센티브 제도에 의해 제조와 수술 건수를 가속시키고 있습니다. 공립병원에서의 로봇인공무릎관절 전치환술의 시험에서는 안전성을 손상시키지 않고 환자의 재원일수가 단축되어 자원계층을 넘은 기술 도입이 입증되었습니다. 호주와 한국은 성숙한 상환의 틀과 신속한 기술 혁신의 보급을 추가하여 이질적이지만 활기찬 지역상을 완성하고 있습니다.

The Joint Replacement Market size is estimated at USD 19.98 billion in 2025, and is expected to reach USD 25.02 billion by 2030, at a CAGR of 4.24% during the forecast period (2025-2030).

A mix of demographic ageing, lifestyle-related osteoarthritis, and continuous implant innovation is sustaining this moderate growth while forcing rapid shifts in surgical protocols. Robotic-assisted systems have captured a double-digit share of total knee cases in the United States and have catalysed the transition to same-day discharge pathways. Metallic devices still dominate, yet ceramics are gaining traction among younger, active recipients who want low wear and no metal ion exposure. Regionally, North America leads on utilisation, whereas Asia-Pacific is the fastest expanding zone as governments invest in orthopaedic capacity and broaden reimbursement.

Osteoarthritis affects 32.5 million adults in the United States and 606.5 million people worldwide. Knee disease alone accounts for more than half of all cases, creating a vast pool of potential surgical candidates. In the United States the economic burden is USD 136.8 billion a year, driven by nearly 1 million knee and hip replacements linked directly to osteoarthritis. More than half of those diagnosed with knee osteoarthritis ultimately undergo total knee arthroplasty, anchoring a structural demand curve for implants.

Primary hip arthroplasties are forecast to hit 572,000 cases by 2030 and primary knee arthroplasties 3.48 million, marking 174% and 673% jumps from 2005 volumes. Revision hip and knee surgeries will rise in parallel as ageing implants reach the end of their life, intensifying the load on health systems. Emerging nations mirror this pattern; Colombia expects 39,270 lower-limb arthroplasties by 2050, with women representing 52.7% of procedures. Older patients often present multiple comorbidities, so providers prioritise less invasive techniques that shorten recovery time. Payers also encourage ambulatory settings: 72% of Medicare joint replacements already occur in outpatient facilities, up sharply from virtually none five years earlier.

Average hip or knee implants cost USD 5,139 in 2023, while Medicare reimbursement for total hip arthroplasty kept falling, squeezing hospital margins. France exemplifies reimbursement pressure after mandating a 25% price cut on orthopaedic devices from 2025, risking product shortages as margins tighten. Bundled payment pilots in the United States favour large, not-for-profit hospitals that can spread risk, leaving smaller providers vulnerable. Orthopaedic trauma reimbursement eroded by one-third over two decades, well below inflation, reinforcing price sensitivity in device selection. Ambulatory centres deliver meaningful cost savings yet cascade margin pressure onto manufacturers, fomenting greater competition.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Knee surgeries accounted for 39.54% of revenue in 2024, anchored by the high prevalence of knee osteoarthritis and well-established clinical pathways. Shoulder arthroplasty is the fastest-growing category at a 5.50% CAGR, stimulated by rising sports injuries among patients under 60 and the arrival of robotic guidance that reduces glenoid placement error. Hip replacement volumes increased 3.8% to 793,082 in 2023, while ankle and elbow procedures stay niche yet benefit from 3-D printed, patient-specific devices that extend implant indications. The partial-knee option is regaining relevance thanks to Zimmer Biomet's cementless Oxford implant that delivers a 94.1% 10-year survival rate. This array of procedure types outlines a maturing yet innovation-driven landscape that keeps the joint replacement market evolving.

Rapid adoption of unicompartmental knee arthroplasty also reflects surgeon willingness to preserve bone and hasten rehabilitation. Robotic alignment tools such as VELYS aim to overcome the steep technical learning curve that traditionally constrained utilisation. Meanwhile, rising revision demand amplifies training needs for complex reconstructions, reinforcing hospital reliance on high-volume arthroplasty specialists. These dynamics underpin a durable procedure mix that will continue to influence hospital resource planning and payer negotiations through 2030.

Metallic implants retained 47.87% revenue in 2024 due to proven fatigue strength and ease of machining. However, ceramics are expanding at a 10.93% CAGR as patients seek lower wear and no ion release. Titanium alloys preserve periprosthetic bone mineral density more effectively than cobalt-chromium, supporting the joint replacement market size for titanium-based systems at both primary and revision level. BIOLOX delta hip bearings show excellent survivorship and negligible allergic response, giving ceramics a persuasive value proposition. Polymer-metal hybrids and bioresorbable scaffolds are also gaining attention for complex revisions and young-adult trauma, signalling a diversified product pipeline.

Metal hypersensitivity has pushed R&D towards nickel-free or cobalt-free alternatives and advanced coatings that cut ion release. Smith + Nephew's OXINIUM resurfacing solution demonstrated a 94.1% 20-year survivorship and 35% fewer revisions than conventional alloys. Suppliers are adding antimicrobial silver coatings to fracture plates and instrument trays to fight surgical-site infection. Together these innovations will redefine material preference hierarchies and influence future joint replacement market share trajectories.

The Joint Replacement Market Report is Segmented by Procedure (Hip Replacement, Knee Replacement, and More), Product (Implants [Metallic, and More], Bone Grafts and Substitutes [Allograft, and More], and More), Technology (Conventional, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 41.11% of revenue in 2024, supported by more than 2.15 million hip and knee replacements annually. Yet downward reimbursement revision exceeding 44% obliges hospitals to double down on operating-room efficiency and implant price negotiation.

Europe presents a seasoned regulatory environment and broad coverage, but reimbursement cuts, notably France's 25% device-price reduction from 2025, pressure profitability. Germany, the United Kingdom, and Italy post high procedural volumes, while broader EU discussions on raw-material sovereignty have spurred titanium and cobalt reshoring initiatives. Higher surgeon comfort with ceramic bearings and partial hip surface replacements differentiates European clinical practice.

Asia-Pacific is the fastest expanding zone at a 9.92% CAGR. China's titanium-industry hub in Baoji contributes 33% of global output, underpinning domestic implant growth. Japanese centres lead robot uptake, while India accelerates manufacturing and procedure counts via the Production Linked Incentive scheme. Robotic total knee arthroplasty trials in public hospitals reduced patient stay without compromising safety, evidencing technology adoption across resource tiers. Australia and South Korea add mature reimbursement frameworks and fast innovation diffusion, rounding out a heterogeneous but buoyant regional picture.