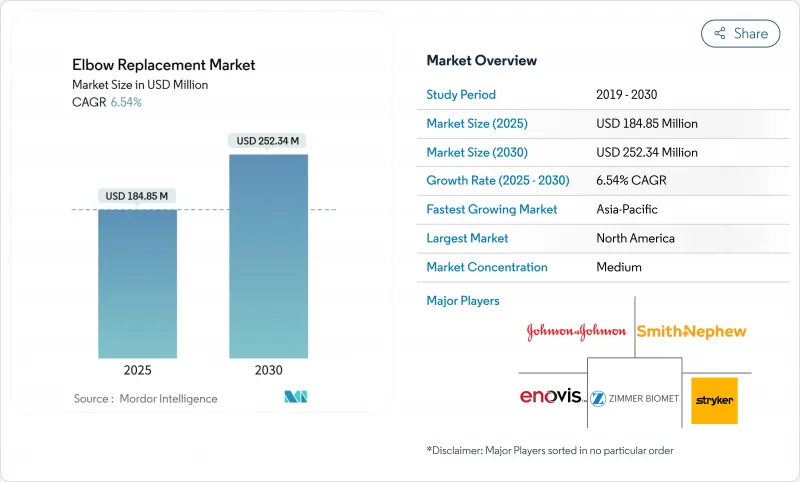

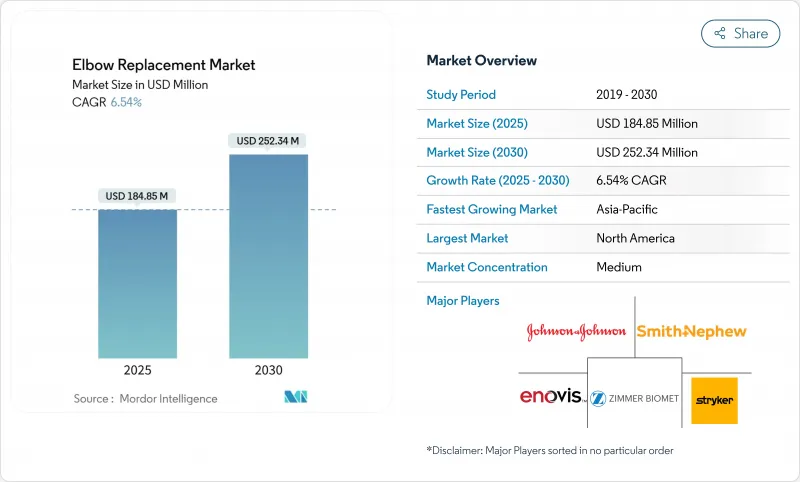

주관절 치환술 시장 규모는 2025년에 1억 8,485만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.54%로 성장할 전망이며, 2030년에는 2억 5,234만 달러에 달할 것으로 예측됩니다.

말기 주관절 증례 증가, 주관절 전치환술에 익숙한 외과 증가, 3D 프린팅된 환자에 적합한 임플란트의 꾸준한 개량이 이 확대를 지원하고 있습니다. 외래 수술 인프라가 급속히 정비되고 복잡한 사지 수술에 유리한 진료 보상 조정과 함께 환자의 접근이 더욱 확산되고 있습니다. 링크드 힌지 인공관절은 재치환이 없는 생존 기간에 초기 설계를 능가하고, 항균성 표면 기술은 심부 감염 위험을 감소시키며, 임플란트의 장기적인 성공을 뒷받침하고 있습니다. 주관절 치환술 시장은 또한 병원이 정형외과 수술실을 근대화하고 현지 제조업체가 규제 당국의 허가를 취득함에 따라 아시아태평양에서 수술 건수가 증가하고 있는 것도 추풍이 되고 있습니다.

골관절염 및 류마티스 관절염이 만연하기 때문에 주관절 치환술의 수술 대기 목록이 계속 증가하고 있습니다. 임상 등록에 따르면 인공관절 전치환술 후 Mayo Elbow Performance Scores는 39에서 95로 개선되었으며 수술이 내구성있는 통증 완화 전략임이 입증되었습니다. 고령화가 진행되고 노인들의 활동에 대한 기대치가 높아지기 때문에 장기적으로 안정된 후보자가 확보됩니다. 안코노네우스 반사 하퇴 삼두근 텅 접근법과 같은 새로운 노출을 줄이는 절차는 연조직 손상을 줄이고 더 빠른 재활을 지원합니다. 이러한 진보는 모든 주요 지역에서 수술 건수를 유지하고 주관절 치환술 시장의 궤도를 강화하고 있습니다.

반구속형 링크드 힌지 인공관절은 기존의 비구속형 인공관절보다, 특히 뼈 결손이 큰 주관절에 대해 더 나은 류측-류측 안정성을 제공합니다. 메타분석에 따르면 염증성 관절염의 경우에는 비링크형에 비해 이완이 적고 10년 생존율이 높다고 보고되었습니다. 임상 커리큘럼이 이러한 기술을 통합함에 따라 외과 의사의 선호도가 변화하고 북미와 서유럽의 리퍼럴 센터 임플란트 수요를 밀어 올리고 있습니다. 제조업체 각사는 수술중의 얼라인먼트를 용이하게 해, 또한 본래의 운동학적 특성을 유지하는 모듈러 스템 및 테이퍼 플랜지를 개량하고 있습니다.

저침습성 관절경 수술은 연골의 박리와 활막 절제술을 통해 최종 인공 관절 치환술을 연기 할 수 있으며 특히 젊은 선수에게는 매력적입니다. 주관절 고정술은 육안적인 불안정성과 감염에 대한 예비 수단으로 일상 작업에 가장 적합한 위치에서 90% 이상의 고정율을 달성합니다. 다혈소판 혈장과 줄기세포를 이용한 재생주사도 조기 변성에 틈새 위치를 차지하고 있습니다. 이러한 대체 경로는 적응증이 제한되지만, 총체로, 주관절 치환술 시장에서 수술 후보자의 상당 부분을 벗어나고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

인공 주관절 전치환술은 2024년 매출의 68.17%를 차지했으며, 심각한 관절 파괴에 대한 종합적인 솔루션으로서의 역할을 강조합니다. 이 우위는 Mayo 점수의 중앙값이 수술 후 40점대 전반에서 90점대 중반으로 급상승한 수십년에 걸친 결과 데이터를 반영합니다. 반관절 성형술과 인공 요골두를 다루는 부분 시스템은 젊은 층의 외상 환자에게 적합하기 때문에 2030년까지 연평균 복합 성장률(CAGR)은 6.80%로 상승할 전망입니다. 외과의사는 염증성 질환이나 말기 변성 질환에 대해서는 전치환술을 선택하는 한편, 복잡한 골절에 대해서는 뼈를 온존하는 부분치환술을 선택하게 되어 있어 주관절 치환술 시장의 저변이 넓어지고 있습니다.

임상 등록은 이러한 동향을 뒷받침하고, 부분 임플란트는 수술 후 체중 제한이 존중되는 경우 주관절의 엄격한 생체 메카닉을 고려하면 허용되는 17%의 재수술률을 달성하고 있습니다. 두 범주 모두 수술 중 3D 내비게이션으로 구성요소 정렬이 더욱 선명해진다는 장점이 있습니다. 이와 병행하여, 모듈형 척골 줄기는 골다공증의 관을 만날 때 외과의사가 고정의 크기를 늘릴 수 있고 조기 느슨함을 더욱 줄일 수 있습니다. 이러한 다양성과 증거 유지의 융합은 주관절 치환술 시장에서 두 제품 라인의 꾸준한 수량 성장을 보장합니다.

코발트 크롬은 입증된 내마모성으로 인해 51.59%의 점유율을 유지하지만 티타늄 합금의 CAGR은 7.13%로 성장할 전망입니다. 나사산 티타늄 줄기는 해면골의 구매를 촉진하고 응력 차폐를 줄입니다. 새로운 다공성 탄탈 슬리브와 PEEK 복합재는 틈새 역할을 하지만 골량이 부족한 재치환술의 경우에는 주목받고 있습니다.

레이저로 텍스처링된 표면과 하이드록시아파타이트 코팅은 티타늄의 골전도성을 증폭시켜 조기 기능적 부하를 가능하게 합니다. 동시에, 항균성 코팅의 성막은 매우 중요한 고장 모드인 인공 관절 주위 감염을 표적으로 합니다. 이러한 개선이 성숙함에 따라 재료 구성은 수요가 높은 용도에서 크롬 코발트의 자리를 빼앗지 않고 서서히 티타늄으로 기울어 갈 것으로 보입니다. 따라서, 티타늄 기반 주관절 치환술 시장 규모는 예측 기간 동안 유의미하게, 그러나 서서히 상승할 것으로 예측됩니다.

북미는 2024년 매출의 39.81%를 차지하며 선두를 유지했습니다. 이는 견고한 상환의 틀과 휄로우십 훈련을 받은 상지 외과의의 치밀한 네트워크가 있기 때문입니다. 메디케어의 진료 보상 안정성과 명확하게 정의된 CPT 코드는 꾸준한 절차의 보급을 지원합니다. 유럽은 임플란트의 안전성을 임상가에게 안심시키는 엄격한 MDR 기준을 뒷받침하면서 3D 프린팅의 신속한 승인을 통해 기술 혁신을 장려하고 있습니다.

아시아태평양은 중국, 인도, 한국이 사회보험을 확대하고 국내 임플란트 제작을 육성하고 있기 때문에 CAGR 7.55%로 예측되어 가장 빠르게 성장하고 있습니다. 국가 조달은 단가를 낮추고 복잡한 재건을 위한 병원 예산을 확대합니다. 라틴아메리카와 중동 및 아프리카는 후진을 숭배하고 있지만 도시의 사립 병원이 고급 화상 처리와 층류 극장을 도입하면 큰 상승을 나타냅니다. 이러한 패턴을 종합하면 주관절 치환술 시장은 지리적으로 분산된 성장을 이루고 있습니다.

The Elbow Replacement Market size is estimated at USD 184.85 million in 2025, and is expected to reach USD 252.34 million by 2030, at a CAGR of 6.54% during the forecast period (2025-2030).

Escalating end-stage elbow arthritis cases, wider surgeon familiarity with total elbow arthroplasty, and steady improvements in 3D-printed, patient-matched implants anchor this expansion. Rapid gains in outpatient surgical infrastructure, coupled with favorable reimbursement adjustments for complex extremity procedures, further widen patient access. Linked-hinge prostheses are outperforming earlier designs on revision-free survival, while antimicrobial surface technologies cut deep infection risk and drive long-term implant success. The elbow replacement market also benefits from rising procedure volumes in Asia-Pacific as hospitals modernize orthopedic theaters and local manufacturers secure regulatory clearances.

Widespread osteo- and rheumatoid arthritis continues to swell the surgical waitlist for elbow reconstruction. Clinical registries show Mayo Elbow Performance Scores improving from 39 to 95 after total arthroplasty, validating surgery as a durable pain-relief strategy. Population aging and higher activity expectations among seniors lock in a steady flow of candidates over the long term. New exposure-sparing techniques such as the anconeus-reflected triceps tongue approach lessen soft-tissue disruption, supporting faster rehabilitation. These advances collectively sustain procedure volumes in all key geographies and reinforce the elbow replacement market trajectory.

Semi-constrained linked-hinge prostheses deliver greater varus-valgus stability than earlier unconstrained devices, especially for elbows with extensive bone loss. Meta-analyses report lower loosening and higher 10-year survivorship in inflammatory arthritis cases relative to non-linked systems. As clinical curricula integrate these techniques, surgeon preference is shifting, boosting implant demand across referral centers in North America and Western Europe. Manufacturers are refining modular stems and tapered flanges that ease intraoperative alignment while safeguarding native kinematics.

Minimally invasive arthroscopy offers cartilage debridement and synovectomy that defers definitive joint replacement, especially attractive to younger athletes. Elbow fusion remains a fallback for gross instability or infection, achieving fusion rates above 90% at set positions optimal for daily tasks. Regenerative injections using platelet-rich plasma and stem cells have also carved a niche in early-stage degeneration. These substitute pathways, though serving selected indications, collectively divert a measurable slice of surgical candidates away from the elbow replacement market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Total elbow replacement generated 68.17% of 2024 revenue, underlining its role as a comprehensive solution for severe articular destruction. This dominance reflects decades of outcome data showing median Mayo scores jumping from the low 40s to the mid-90s post-surgery. Partial systems, covering hemi-arthroplasty and radial head prostheses, are climbing at a 6.80% CAGR through 2030 as they better suit younger trauma patients. Surgeons increasingly reserve total systems for inflammatory or end-stage degenerative conditions while opting for bone-preserving partial options in complex fractures, expanding the elbow replacement market addressable base.

Clinical registries corroborate these trends, noting partial implants achieve 17% reoperation rates-acceptable given the elbow's demanding biomechanics-when postoperative weight limits are respected. Both categories benefit from intraoperative 3D navigation that sharpens component alignment. In parallel, modular ulnar stems let surgeons upsize fixation when encountering osteoporotic canals, further reducing early loosening. This blend of versatility and evidence retention secures steady volume growth across both product lines within the elbow replacement market.

Cobalt-chrome retained 51.59% share owing to its proven wear resistance, yet titanium alloys are notching a 7.13% CAGR. Threaded titanium stems boost cancellous purchase and reduce stress shielding, qualities that resonate with surgeons focused on long-term bone preservation. Novel porous tantalum sleeves and PEEK composites continue in niche roles but command interest for revision cases with compromised bone stock.

Laser-textured surfaces and hydroxyapatite coatings amplify titanium's osteoconductivity, enabling earlier functional loading. Concurrently, antimicrobial film deposition targets periprosthetic infection, a pivotal failure mode. As these enhancements mature, material mix is likely to tilt incrementally toward titanium without displacing chrome-cobalt's seat in high-demand applications. The elbow replacement market size for titanium-based systems is therefore expected to climb meaningfully yet progressively over the forecast horizon.

The Elbow Replacement Market Report is Segmented by Product Type (Partial Elbow Replacement, Total Elbow Replacement), Implant Material (Titanium Alloys, Cobalt-chrome Alloys, Tantalum & Others), Fixation Technique (Cemented, Cement-Less), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America preserved leadership with 39.81% of 2024 turnover, thanks to robust reimbursement frameworks and a dense network of fellowship-trained upper-extremity surgeons. Medicare fee stability and clearly defined CPT codes underpin steady procedural uptake. Europe follows, buoyed by stringent MDR standards that reassure clinicians of implant safety while still encouraging innovation through fast-track 3D printing approvals.

Asia-Pacific is the fastest riser, projected at 7.55% CAGR, as China, India, and South Korea broaden social insurance and cultivate domestic implant fabrication. National procurement drives lower unit prices, expanding hospital budgets for complex reconstructions. Latin America and the Middle East & Africa trail but show meaningful upside where urban private hospitals install advanced imaging and laminar-flow theaters. Collectively, these patterns support geographically diversified growth for the elbow replacement market.