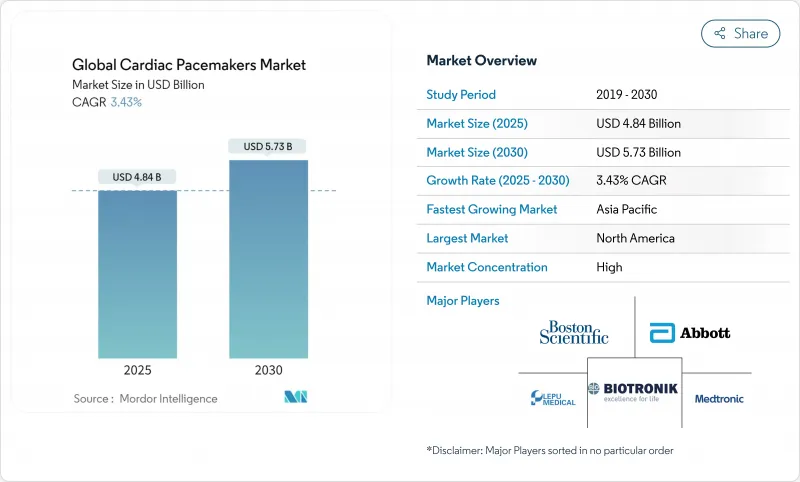

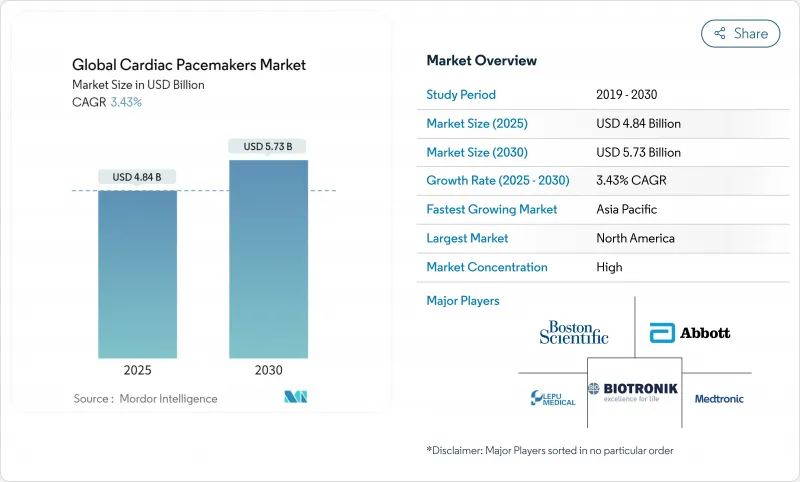

심장 페이스메이커 시장은 2025년에 48억 4,000만 달러로 추정되고, CAGR 3.43%로 성장할 전망이며, 2030년에는 57억 3,000만 달러에 이를 것으로 예측됩니다.

성장의 배경으로는 노인 인구의 꾸준한 증가, 서맥성 부정맥 및 심장 블록 발생률 증가, 하드웨어 주도 수량 증가, 리드리스 설계, MRI 지원 플랫폼, AI 가이드 프로그래밍을 중시한 소프트웨어 지원 성능 업그레이드로의 결정적인 변화가 있습니다. 북미는 프리미엄 기술의 채용을 촉진하는 견고한 상환 제도에 의해 심장 페이스메이커 시장을 선도하고 있습니다. 듀얼 챔버 시스템은 여전히 임상 주력 제품이지만, 리드리스 장치와 생리적 페이싱 컨셉이 급속히 현존의 우위를 침식하고 있으며, 저침습으로 탁월한 솔루션에 의해 시장이 진화하고 있음을 보여줍니다. 경쟁 포지셔닝은 장치, 원격 모니터링, 분석 및 사이버 보안 안전 가드를 결합한 엔드 투 엔드 생태계에 달려 있습니다. 반면 탄탈과 마이크로칩 공급망 부족은 FDA의 까다로운 사이버 보안 규정과 함께 탄력성이 있는 수요 환경에 복잡성 및 비용 압력을 가져다 줍니다.

역학 조사에서는 방실 블록의 증례 수가 41% 증가하고, 2020년 37만 8,816명에서 2060년에는 53만 5,076명이 될 것으로 예측되고 있습니다. 완전한 심장 블록은 임상 등록에서 영구 페이스메이커 적응증의 76%를 차지하며 모든 제품 클래스에서 지속적인 수요를 보장합니다. 2000-2022년 심방세동의 평생 위험이 24.2%에서 30.9%로 상승했기 때문에 페이싱 치료의 적응이 되는 심방세동이 더욱 증가했습니다. 시크 사이너스 증후군과 관련된 사망률도 노인들 사이에서 상승하고 있으며, 적시 개입의 필요성을 강조하고 있습니다. 생존율의 데이터는 심박 조율기의 유용성을 뒷받침하고 있으며, 중증 서맥 코호트에서는 페이싱을 받은 환자의 생존율은 치료되지 않은 환자의 2.7배가 되고 있습니다.

심혈관 질환은 2050년까지 미국 성인의 61%에 영향을 미칠 것으로 예상되며, 심장 맥박 조정기 시장의 구조적 돌풍을 강화하고 있습니다. 85세 이상의 노인층은 이미 미국에서의 이식의 40% 이상을 차지하고 있으며, 2060년까지 3배로 증가할 전망입니다. 치료 성적 분석을 통해 전도계 페이싱은 연령층을 넘어 동등한 효능을 유지하는 것으로 밝혀졌고, 노인 치료 위험에 대한 우려는 부인되었습니다. 의료 시스템은 노년 순환기 병동을 건설하고 허약한 환자를 위한 장치의 선택을 개선함으로써 대응합니다. 장기간의 케어에 대한 배려로부터, 장수명으로 유지관리의 필요성이 낮은 시스템을 선택하는 의료 기관이나 임상가가 늘고 있습니다.

2,500-3,000달러라는 단가는 신흥국에서 많은 환자가 치료를 받을 수 없는 상황을 낳고 있으며, 이들 국가에서의 이식형 의료기기의 장착율은 인구 100만 명당 4대에 그치고 있는 것에 비해 선진국인 프랑스에서는 100만 명당 782대가 되고 있습니다. 이러한 비용 면에서 장벽은 매년 예상 100만 명의 예방 가능한 사망으로 이어지고 있으며, 자원이 제한된 지역에서는 치료가 필요한 환자의 27%가 치료를 받을 수 없는 상태로 남아 있습니다. 장치 재사용 프로그램에서 안전성은 새로운 임플란트와 동등하다고 보고되었지만 규제 망설임 및 문화적 저항에 직면하고 있습니다. 정부 입찰, 자선 기부, 단계적 가격 설정으로 어느 정도의 구제가 이루어지고 있지만, 지속 가능한 솔루션은 근본적인 비용 혁신, 현지 조립, 공급망 합리화에 달려 있습니다. 범아프리카 심장병학회(Pan-African Society of Cardiology)의 장비 재사용 이니셔티브는 규제, 임상, 업계 이해관계자들이 마음을 맞추면 무엇을 달성할 수 있는지를 밝혔습니다.

이식형 시스템은 2024년에 64.23%의 매출을 획득해 폭넓은 임상적응증에서 확고한 지위를 구축하고 있습니다(ihrs.co.in). 그러나 리드리스 모델의 CAGR은 4.45%로 가장 높고 의사가 합병증 프로파일의 저침습 옵션에 끌려가면서 점유율을 저하시키고 있습니다. 단순한 서맥에는 단일 챔버 이식형이 여전히 표준적이지만, 복잡한 방실 조건에서는 듀얼 챔버 이식형이 주류입니다. 양심실 재동기화 페이싱은 전도 지연이 있는 심부전 환자를 대상으로 하며 특수한 그룹이면서 점점 컴팩트한 하드웨어 설계의 혜택을 누리고 있습니다. 임시 페이스메이커와 체외식 페이스메이커는 수술 후 또는 응급 시 급성 심부전을 보완하여 영구적인 이식이 가능할 때까지 치료의 연속성을 확보합니다.

Abot의 AVEIR DR 시험에서 98.3%의 수술 성공률과 97%의 동기화율이라는 데이터도 뒷받침하고 있습니다. 또한 노스 웨스턴 대학의 용해 가능한 장치는 미래의 어린이 및 단기 기회를 제안합니다. 밸류 베이스 케어의 압력이 강해지고 있는 가운데, 지불자는 포켓이나 리드에 관련된 개정의 배제를 환영해, 리드리스 기술을 평생에 걸쳐 비용 효율적인 옵션으로서 자리매김하고 있습니다.

본 보고서는 세계의 심장 페이스메이커 시장 기업을 망라하여 제품 유형별(이식형 페이스메이커, 리드리스 페이스메이커, 기타), 기술별(싱글 챔버 기술, 듀얼 챔버 기술, 기타), 최종 사용자별(병원 및 심장 센터, 외래수술센터(ASC) 등), 지역별(북미, 유럽, 아시아태평양, 기타)로 세분화하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년에 38.50%의 점유율을 차지했고, 여전히 주요 수익원이며, 정교한 지불자 프레임워크, 높은 대중 인지도, AI 기반 원격 모니터링 cms.gov 의 조기 도입으로 지지되고 있습니다. 페이싱 리드 및 실시간 모니터링에 대한 메디케어의 개별 지불은 기술 도입을 유지하고 있으며, FDA의 고속 트랙 패스웨이는 듀얼 챔버 리드리스 시스템 및 예측 분석 엔진과 같은 획기적인 제품의 신속한 상업화를 촉진하고 있습니다. 캐나다와 멕시코 공중 보건 프로그램은 가치 기반 조달을 지원하는 일괄 입찰을 통해 액세스를 확대하고 제조업체에게 스티커 가격뿐만 아니라 수명주기의 경제성을 제시하도록 촉구합니다.

유럽에서는 유럽 심장병학회(European Society of Cardiology) 등에 의한 일관된 상환 제도와 강력한 임상 가이드라인의 영향력을 활용하여 진료 기준의 균질화를 추진하고 있습니다. 독일, 프랑스, 영국은 견고한 전기 생리학적 네트워크와 1인당 진단률이 높아 이식 건수를 선도하고 있습니다. 브렉시트(EU 이탈)에 의해 무역 문서상의 마찰이 생겼지만, 병행하는 규제 프레임워크는 계속 CE 마크가 붙은 페이스메이커를 승인하고 있어 환자의 접근을 확보하고 있습니다. 중기적으로 EU 의료기기 규제(MDR)는 보다 깊은 시판 후 감시를 요구하며, 중소기업은 컴플라이언스 오버헤드를 이유로 제휴 및 철수를 강요받게 됩니다.

아시아태평양에서 2030년까지 연평균 복합 성장률(CAGR) 5.67%로 가장 빠른 성장이 전망되며, 인구동태의 고령화, 도시의 생활 습관병, 심장 의료기기의 상환을 확대하는 정부의 대처가 이를 뒷받침합니다. 중국의 개혁 국가 의료 제품 관리국(NMPA) 프로세스는 외국에서 만든 장치의 승인을 가속화하는 반면, 그 수량 기준 조달 프로그램은 가격을 협상하고 설치 기반의 확산을 확대합니다(cisema.com). 인도에서는 비용 문제에 직면해 있지만, 특히 Tier2 도시 pubmed.ncbi.nlm.nih.gov에서 민간 파트너십을 통한 난치병 의료 지원을 통해 임플란트 수가 증가하고 있습니다. 일본과 한국은 국민 모두 보험제도와 기술에 정통한 전문의가 있기 때문에 국민 1인당 임플란트 임베디드률이 높고, 호주와 싱가포르는 AI 주도 스크리닝 프로그램의 지역 테스트 베드로 기능하고 있습니다.

중동 및 아프리카는 심장 질환의 부담이 증가하고 공중 보건 정책이 비전염성 질환 관리에 축족을 옮기고 있기 때문에 건수에서는 뒤쳐지고 있지만 잠재적인 기회를 제공합니다. 사우디아라비아와 아랍에미리트(UAE)에서는 정부 주도 입찰에 의해 최신 페이싱 기술에 예산이 할당되고 자선 사업에 의한 기기 재이용 프로그램에 의해 사하라 이남 지역에서는 심장 대기 환자가 감소하고 있습니다. 라틴아메리카에서는 브라질과 멕시코가 전기 생리학적 치료 능력을 근대화하는 한편, 경제 규모가 작은 국가는 수입 자금 조달을 복잡하게 하는 통화 변동과 격투하고 있으며, 그 진전은 엇갈리고 있습니다.

The cardiac pacemaker market generated USD 4.84 billion in 2025 and is forecast to post a 3.43% CAGR, achieving USD 5.73 billion by 2030.

Growth stems from a steadily enlarging elderly population, rising incidence of bradyarrhythmia and heart block, and a decisive shift from hardware-driven volume gains to software-enabled performance upgrades that emphasize leadless designs, MRI-conditional platforms, and AI-guided programming . North America continues to lead the cardiac pacemaker market through robust reimbursement schemes that accelerate adoption of premium technology, while Asia-Pacific shows the quickest uptake as governments fund wider access and local manufacturers enter value tiers. Dual-chamber systems remain the clinical workhorse, yet leadless devices and physiologic pacing concepts are rapidly eroding the incumbent's dominance, marking the market's evolution toward minimally invasive, extraction-free solutions. Competitive positioning hinges on end-to-end ecosystems that combine devices, remote monitoring, analytics, and cybersecurity safeguards. Meanwhile, supply chain shortages in tantalum and microchips, combined with stringent FDA cybersecurity rules, add complexity and cost pressures to an otherwise resilient demand landscape.

Epidemiological studies project atrioventricular block cases to climb 41%, moving from 378,816 individuals in 2020 to 535,076 by 2060, propelled by an aging global population and widespread cardiovascular risk factors. Complete heart block constitutes 76% of permanent pacemaker indications in clinical registries, ensuring persistent demand across all product classes. Concomitant rises in atrial fibrillation-from a 24.2% to 30.9% lifetime risk between 2000 and 2022-further expand the candidate pool for pacing therapy as conduction disorders supervene. Mortality tied to sick sinus syndrome has also climbed among seniors, highlighting the need for timely intervention. Survival data underscore pacemaker benefit, with paced patients experiencing 2.7-fold higher survival than untreated counterparts in severe bradycardia cohorts.

Cardiovascular disease is forecast to affect 61% of US adults by 2050, reinforcing the structural tailwind behind the cardiac pacemaker market. The >=85-year cohort already represents over 40% of US implants and is on track to triple by 2060. Outcome analyses reveal that conduction-system pacing maintains equivalent efficacy across age groups, debunking concerns over geriatric procedural risk. Health systems respond by building geriatric cardiology units and refining device selection for frail patients, with leadless options showing particular appeal in reducing infection risk. Long-term care considerations increasingly guide payer and clinician preference toward systems offering longevity and low maintenance demands.

Unit prices of USD 2,500-3,000 lock many patients out of treatment in emerging economies, where implant rates hover at 4 devices per million compared with 782 per million in developed France heart.. Cost barriers translate into an estimated 1 million preventable deaths each year, and 27% of indicated patients in resource-limited settings remain untreated. Device reuse programs report safety parity with new implants but face regulatory hesitancy and cultural resistance . Government tenders, philanthropic donations, and tiered pricing bring some relief, yet sustainable solutions depend on fundamental cost innovation, local assembly, and supply chain rationalization. The Pan-African Society of Cardiology's device reuse initiative highlights what can be achieved when regulatory, clinical, and industry stakeholders align heart.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Implantable systems captured 64.23% revenue in 2024, underscoring their entrenched position across broad clinical indications ihrs.co.in. However, leadless models post the highest 4.45% CAGR and are eroding share as physicians gravitate toward minimally invasive options with lower complication profiles. Single-chamber implantables remain standard for straightforward bradycardia, whereas dual-chamber configurations dominate complex atrioventricular conditions. Biventricular resynchronization pacing serves heart-failure cohorts with conduction delays, a specialized group yet one that benefits from increasingly compact hardware designs. Temporary and external pacemakers fill acute postoperative or emergency gaps, ensuring continuity of care until permanent implantation is feasible.

Leadless expansion marks a structural pivot within the cardiac pacemaker market, buoyed by data showing 98.3% procedural success and 97% synchronization in Abbott's AVEIR DR trial. Form-factor reductions, battery gains, and retrieval enhancements collectively sharpen value, while Northwestern University's dissolvable devices hint at future pediatric and short-term opportunities sciencenews.org. As value-based care pressures intensify, payers welcome the elimination of pocket- and lead-related revisions, positioning leadless technology as a cost-effective choice over a lifetime horizon.

The Report Covers Global Cardiac Pacemaker Market Companies and It is Segmented by Product Type (Implantable Pacemakers, Leadless Pacemakers and More), by Technology (Single Chamber Technology, Dual Chamber Technology and More), by End User (Hospitals & Cardiac Centers, Ambulatory Surgical Centers and More) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remains the leading revenue generator, holding 38.50% share in 2024, anchored by sophisticated payer frameworks, high public awareness, and early adoption of AI-enabled remote monitoring cms.gov. Medicare's separate payments for pacing leads and real-time monitoring sustain technology uptake, while FDA fast-track pathways foster rapid commercialization of breakthroughs such as dual-chamber leadless systems and predictive analytics engines. Canadian and Mexican public health programs are widening access through bulk tenders that favor value-based procurement, nudging manufacturers to present lifecycle economics rather than sticker price alone.

Europe leverages cohesive reimbursement systems and strong clinical guideline influence from entities such as the European Society of Cardiology, driving homogeneity in practice standards. Germany, France, and the United Kingdom lead implantation volumes thanks to robust electrophysiology networks and high per-capita diagnostic rates. Brexit has introduced trade documentation friction, but parallel regulatory frameworks continue to recognize CE-marked pacemakers, ensuring patient access. Over the medium term, EU Medical Device Regulation (MDR) will demand deeper post-market surveillance, pushing smaller manufacturers to partner or exit due to compliance overhead.

Asia-Pacific provides the fastest 5.67% CAGR to 2030, propelled by aging demographics, urban lifestyle disease, and government initiatives that expand cardiac device reimbursement. China's reformed National Medical Products Administration (NMPA) process expedites foreign device approvals, while its volume-based procurement program negotiates prices down, enlarging installed base penetration cisema.com. India confronts cost obstacles yet shows rising implant numbers as public-private partnerships fund indigent care, especially in tier-2 cities pubmed.ncbi.nlm.nih.gov. Japan and South Korea sustain high per-capita implant rates due to universal coverage and tech-savvy specialists, while Australia and Singapore act as regional testbeds for AI-driven screening programs.

The Middle East and Africa trail in volume but offer latent opportunity as cardiac disease burden climbs and public health policies pivot toward noncommunicable disease management. Government-led tenders in Saudi Arabia and the United Arab Emirates allocate budget for modern pacing technologies, and philanthropic device reuse programs are reducing waitlists in sub-Saharan regions heart. Latin America shows mixed progress as Brazil and Mexico modernize their electrophysiology capacity while smaller economies wrestle with currency volatility that complicates import financing.