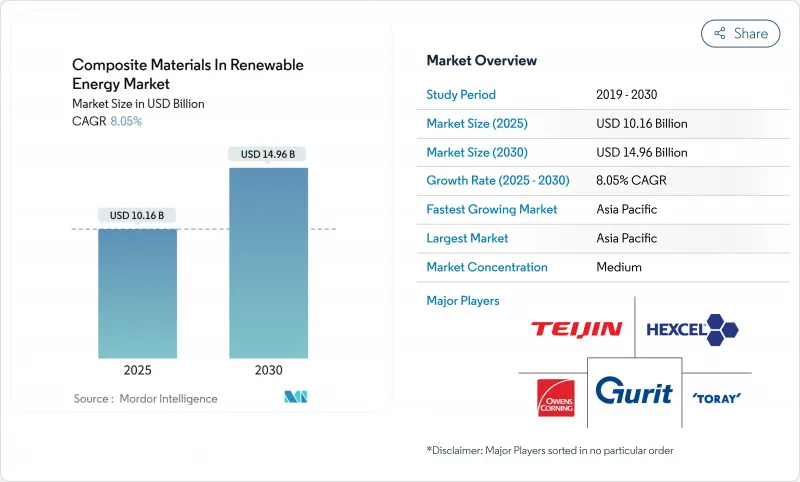

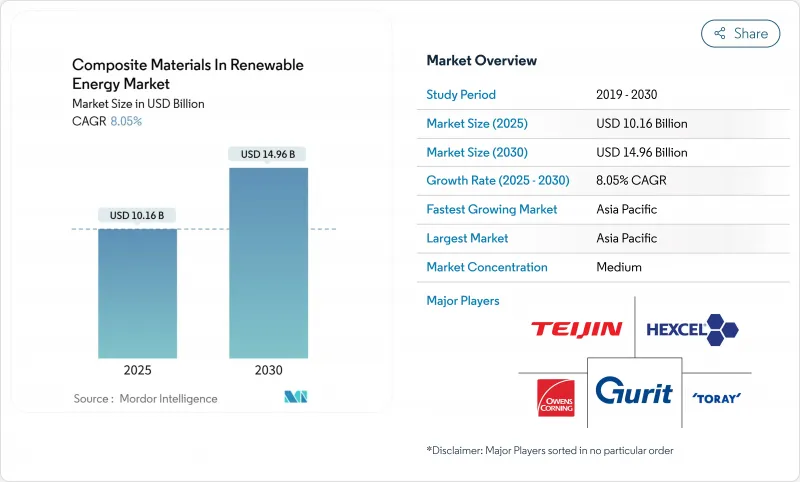

재생에너지용 복합재료 시장의 2025년 시장 규모는 101억 6,000만 달러로 평가되었고 CAGR은 8.05%를 나타낼 것으로 예측되며, 2030년에 149억 6,000만 달러로 성장할 전망입니다.

풍력, 태양광, 수소 프로젝트의 급속한 용량 증가는 부품 수명을 연장하고 탄소 발자국을 축소하는 더 가볍고 강한 구조물을 요구합니다. 정부의 청정 에너지 의무화 정책, 재활용 가능한 열가소성 플랫폼의 기술적 돌파구, 가혹한 해상 및 사막 기후를 견디는 경량 소재의 필요성이 결합되어 조달 주기를 가속화하고 있습니다. 자동 섬유 배치, 3D 프린팅 및 기타 인더스트리 4.0 공정은 생산 일정을 단축하는 동시에 제조 폐기물을 줄이고 있습니다. 동시에 수직 통합 공급업체들은 공급망 긴장 속에서 핵심 원자재를 확보하기 위해 섬유 방적, 수지 합성, 부품 제작을 통합하고 있습니다. 이러한 교차하는 힘들은 재생에너지 시장에서 복합재료가 10년간 꾸준하고 혁신 주도형 성장을 이룰 수 있는 기반을 마련하고 있습니다.

복합재료 대체는 해상 풍력, 수소 탱크, 조력 장치의 구조적 질량을 줄여 적재 효율을 높이고 운송 물류를 간소화합니다. 조력 블레이드의 13.76% 무게 절감은 강철 대비 출력을 46.1% 향상시켰습니다. 항공우주 분야에서는 라이너 없는 V형 탄소 복합재료 탱크 개발이 액체 수소 추진 전환을 지원하며, 재생 에너지 등급 섬유 수요를 간접적으로 증가시킵니다. 미쓰비시 화학의 C/SiC 세라믹 매트릭스 복합재료는 1,500°C를 견뎌 헬리오스태트 수신기 및 핵융합로 하드웨어 적용을 가능케 합니다. 이러한 진전은 재생에너지 시장에서 복합재료가 고온·부식성 환경에서 알루미늄과 강철을 지속적으로 대체하는 이유를 보여줍니다.

로터 직경 276m의 지멘스 에너지 21MW 프로토타입은 150m에 육박하는 블레이드 길이가 유리섬유만으로는 달성 불가능한 강성 대 중량 목표를 위해 탄소섬유 스파 캡을 필요로 함을 보여줍니다. 고강도 에폭시 접합으로 구현된 분할형 블레이드 구조는 공기탄성적 무결성을 유지하면서 운송을 용이하게 합니다. ZEBRA 컨소시엄은 아르케마의 엘리움 수지를 사용해 세계 최대 규모의 완전 재활용 가능 열가소성 블레이드를 완성하며 폐쇄형 플랫폼의 산업적 준비를 알렸습니다. 천연 섬유와 합성 섬유를 혼합한 하이브리드 레이업은 내충격성을 향상시키고 내재 탄소량을 낮춰, 2050년까지 150GW를 목표로 하는 EU 해상 풍력 계획과 부합하며 이는 글로벌 탄소섬유 수요를 두 배로 증가시킬 수 있습니다.

자동 섬유 배치 라인은 개당 500-1,000만 달러, 100m 이상 블레이드 금형은 세트당 200만 달러 이상으로, 투자 회수 전까지 수년간 자본을 묶어둡니다. 인증 프로그램은 보통 5-7년 소요되어 중견 혁신 기업의 운영 자금 수요를 확대시킵니다. 헥셀(Hexcel)의 2025년 3억 달러 채권 발행은 공정 기술 리더십 유지를 위해 필요한 재정적 역량을 보여줍니다. 열가소성 소재 도입은 비용을 가중시키는데, 열경화성 라인과 오븐, 프레스, 용접 장비가 달라 병렬 자산 공간을 창출하여 중소 제조업체의 경쟁력을 저해하기 때문입니다.

2024년 재생에너지 시장 내 복합재료 점유율에서 GFRP가 55.25%를 차지하며 최대 매출 기여도를 기록했습니다. 탄소 섬유의 8.62% CAGR은 120m를 초과하는 로터 직경에서 강성과 피로 성능이 5-10배의 비용 프리미엄을 정당화함을 반영합니다. SGL Carbon의 80m 이상 블레이드 공급 계약은 항공우주 산업에서 에너지 분야로의 수직적 진출을 보여줍니다. 현무암 섬유와 천연 섬유를 혼합한 하이브리드 섬유 레이업은 내재 탄소를 줄이면서도 필요한 계수를 유지하여 중형 터빈 클래스에 대한 옵션을 확대합니다. 독일의 바이오 기반 리그닌 섬유 연구는 상업적 규모는 제한적이지만 향후 비용 절감 수단이 될 전망입니다. 기계적 재활용으로 원래 인장 강도의 60-70%를 유지하는 재활용 탄소섬유는 2차 구조물에 꾸준히 통합되며 원료 공급원을 다각화하고 원자재 가격 변동성을 완화합니다.

에폭시는 성숙한 공급망과 높은 피로 저항성 덕분에 2024년 매출 점유율 45.86%를 유지했습니다. 그러나 바이오 수지와 재활용 수지는 OEM 업체들이 순환 경제 의무를 충족하기 위해 경쟁하면서 연평균 8.04%의 성장률을 보이고 있습니다. 다우(Dow)와 베스타스(Vestas)는 층간 내구성을 높이는 동시에 신속한 인발 성형을 가능하게 하는 폴리우레탄 스파 캡(spar-cap) 화학 물질을 인증받았습니다. 시코민의 SGi 128 바이오 에폭시 겔 코트는 35% 재생 가능 성분으로 화재 안전 솔루션을 입증합니다. 엘리움과 같은 열가소성 매트릭스는 수리 가능성과 용융 재활용이라는 추가 이점을 제공하여 재생 에너지 시장의 복합재료가 폐쇄형 순환 경제로 전환되도록 합니다.

아시아태평양 지역은 2024년 재생 에너지 시장 규모에서 복합재료의 44.68%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 8.12%를 기록할 전망입니다. 중국은 종단간 공급망으로 지역을 주도하지만, 2024년 도입된 재활용 기준은 통합형 현지 선도기업에 유리한 규정 준수 비용을 증가시킵니다. 인도의 24억 달러 규모 수소 미션과 방위산업용 탄소섬유 확대는 국내 생산 유인을 강화합니다. 일본의 페로브스카이트 로드맵은 유연한 복합 기판을 통해 2040년까지 38.3GW 달성을 목표로 하며, 이는 글로벌 태양광 모듈 구조를 재편할 수 있는 전환점입니다. 한국은 조선 기술력을 활용해 해상풍력 복합재료 시장에 진출하는 한편, 호주는 내륙 저수지에 부유식 태양광을 시험하며 최종 사용 사례의 지역적 다양성을 보여줍니다.

북미는 3,690억 달러 규모의 인플레이션 감축법(IRA) 자금의 혜택을 받으며, 텍사스·뉴욕·온타리오에서 국내 생산 보너스가 공장 확장을 촉진합니다. GE 버노바의 6억 달러 규모 제조 시설 확장은 태평양 횡단 물류 위험을 줄이는 리쇼어링 움직임을 보여줍니다. 캐나다 항공우주 복합재료 클러스터는 오토클레이브 외 공정 기술을 조력 터빈 외피로 이전하는 데 기여하며, 멕시코의 비용 경쟁력 있는 노동력은 태양광 지지대 수출용 풀트루더 업체를 유치합니다. 이 지역의 과제는 수입 의존도 과잉을 방지하기 위한 섬유 생산 규모 확대이며, 여러 합작 기업들이 2027년까지 이 격차를 해소할 계획입니다.

유럽은 재활용성과 내재 탄소에 관한 글로벌 규범을 주도하는 규제 영향력을 행사합니다. ZEBRA 프로젝트의 열가소성 블레이드 성공은 유럽 대륙을 기술 선도자로 자리매김하게 했습니다. 독일의 리그닌 섬유 파일럿 라인은 연구개발 리더십을 상징하는 반면, 프랑스는 항공우주 유산을 활용해 고탄성 프리프레그를 정제합니다. 영국 국립 복합재료 센터의 SusWIND 프로그램은 다양한 재활용 경로를 검증하여 OEM에 설계 유연성을 제공합니다. 북해와 발트해의 해상풍력 확대는 지속적인 섬유 수요를 창출하지만, 높은 에너지 비용은 마진 방어를 위한 자동화를 촉진합니다.

The composite materials in the renewable energy market were valued at USD 10.16 billion in 2025 and are forecast to expand at an 8.05% CAGR, reaching USD 14.96 billion by 2030.

Rapid capacity additions in wind, solar, and hydrogen projects demand lighter, stronger structures that extend component lifetimes and shrink carbon footprints. Government clean-energy mandates, breakthroughs in recyclable thermoplastic platforms, and the need for lightweight materials that endure harsh offshore and desert climates combine to accelerate procurement cycles. Automated fibre placement, 3D printing, and other Industry 4.0 processes are compressing production timelines while trimming manufacturing scrap. At the same time, vertically integrated suppliers are consolidating fibre spinning, resin synthesis, and part fabrication to secure critical inputs amid supply-chain tension. These intersecting forces position the composite materials in the renewable energy market for a decade of steady, innovation-driven growth.

Composite substitution cuts structural mass in offshore wind, hydrogen tanks, and tidal devices, boosting payload efficiency and easing transport logistics. Weight savings of 13.76% on tidal blades have lifted power output by 46.1% versus steel alternatives. In aerospace, the development of liner-less Type V carbon-composite tanks supports the transition to liquid-hydrogen propulsion, indirectly increasing demand for renewable-grade fibres. Mitsubishi Chemical's C/SiC ceramic matrix composite endures 1,500 °C, opening paths for heliostat receivers and fusion-reactor hardware. These advances underline why the composite materials in the renewable energy market continue to displace aluminum and steel in high-temperature, corrosive environments.

Siemens Energy's 21 MW prototype with a 276 m rotor diameter illustrates how blade lengths nearing 150 m require carbon-fibre spar caps for stiffness-to-weight targets unattainable with glass fibre alone. Segmented blade architectures, enabled by high-toughness epoxy joints, ease transport while maintaining aeroelastic integrity. The ZEBRA consortium completed the world's largest fully recyclable thermoplastic blade using Arkema's Elium resin, signalling industrial readiness for closed-loop platforms. Hybrid lay-ups that mix natural and synthetic fibres improve impact resistance and lower embodied carbon, aligning with EU offshore wind targets of 150 GW by 2050 that could double global carbon-fibre demand.

Automated fibre-placement lines cost USD 5-10 million each, while molds for >100 m blades exceed USD 2 million per set, tying up capital for years before payback. Certification programs often run 5-7 years, stretching working-capital needs for mid-tier innovators. Hexcel's USD 300 million bond issue in 2025 exemplifies the financial firepower required to retain process-technology leadership. Thermoplastic adoption compounds costs, since ovens, presses, and welding equipment differ from thermoset lines, creating parallel asset footprints that hamper small manufacturers' competitiveness.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The segment generated the largest revenue contribution in 2024, when GFRP held 55.25% of composite materials in the renewable energy market share. Carbon fibre's 8.62% CAGR reflects rotor diameters that eclipse 120 m, where stiffness and fatigue performance justify its 5-10X cost premium. SGL Carbon's supply agreements for 80 m-plus blades illustrate vertical moves into energy from aerospace. Fibre-hybrid lay-ups blending basalt and natural fibre reduce embodied carbon yet maintain required modulus, expanding options for mid-range turbine classes. Bio-based lignin fibre research in Germany offers a future cost-reduction lever, although commercial volumes remain limited. Recycled carbon fibre is steadily integrating into secondary structures as mechanical recycling preserves 60-70% original tensile strength, further diversifying feedstocks and tempering raw material price swings.

Epoxy maintained a 45.86% revenue share in 2024 thanks to mature supply chains and high fatigue resistance. Yet bio-resins and recycled resins are expanding at an 8.04% CAGR as OEMs race to satisfy circular-economy mandates. Dow and Vestas have qualified polyurethane spar-cap chemistries that enable rapid pultrusion while elevating interlaminar toughness. Sicomin's SGi 128 bio-epoxy gel coat demonstrates fire-safe solutions with 35% renewable content. Thermoplastic matrices such as Elium offer the added benefit of repairability and melt recycling, pivoting the composite materials in the renewable energy market toward closed-loop economics.

The Composite Materials in Renewable Energy Market Report Segments the Industry by Fibre Type (Glass-Fibre-Reinforced Plastics (GFRP), and More), Resin Matrix (Epoxy, Polyester, and More), Manufacturing Process (Vacuum Infusion, Prepreg/Autoclave, and More), Application (Wind Power, Solar Power, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 44.68% of the composite materials in the renewable energy market size in 2024 and is on track for an 8.12% CAGR through 2030. China anchors the region with end-to-end supply chains, yet its 2024 recycling standards raise compliance costs that favor integrated local champions. India's USD 2.4 billion Hydrogen Mission and defense-sector carbon-fibre push reinforce domestic production incentives. Japan's perovskite roadmap aims for 38.3 GW by 2040 via flexible composite substrates, a pivot that may recalibrate global solar module architectures. South Korea leverages shipbuilding know-how to enter offshore wind composites, while Australia tests floating solar on inland reservoirs, showcasing regional diversity in end-use cases.

North America benefits from USD 369 billion of Inflation Reduction Act funding, with domestic-content bonuses catalyzing plant expansion in Texas, New York, and Ontario. GE Vernova's USD 600 million manufacturing buildout exemplifies reshoring moves that cut trans-Pacific logistics risk. Canada's aerospace-composite cluster supports the transfer of out-of-autoclave methods to tidal-turbine shells, while Mexico's cost-competitive labor pool draws pultruders for solar-rack exports. The region's challenge is scaling fibre production to prevent over-dependence on imports, a gap several joint ventures aim to close by 2027.

Europe wields regulatory clout, steering global norms on recyclability and embodied carbon. The ZEBRA project's thermoplastic blade success positions the continent as a technology frontrunner. Germany's lignin-fibre pilot lines symbolize R&D leadership, whereas France leverages aerospace heritage to refine high-modulus prepregs. The UK National Composites Centre's SusWIND program validates multiple recycling routes, giving OEMs design flexibility. Offshore wind buildout in the North Sea and Baltic drives sustained fibre demand, though high energy costs compel automation to defend margins.