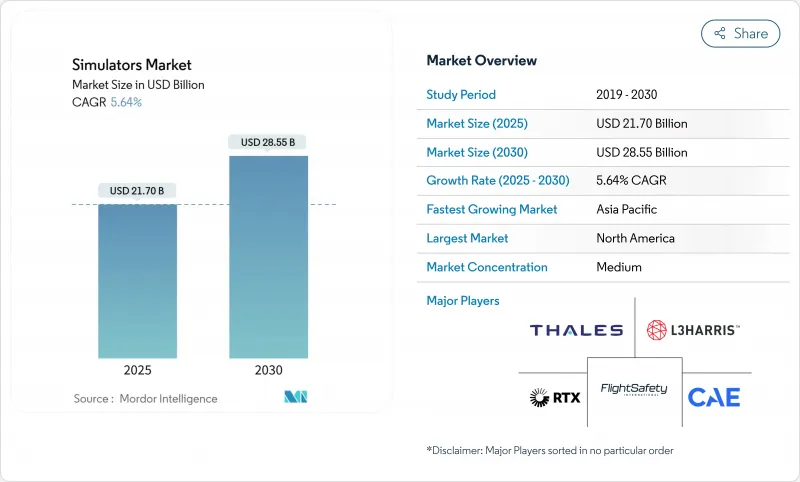

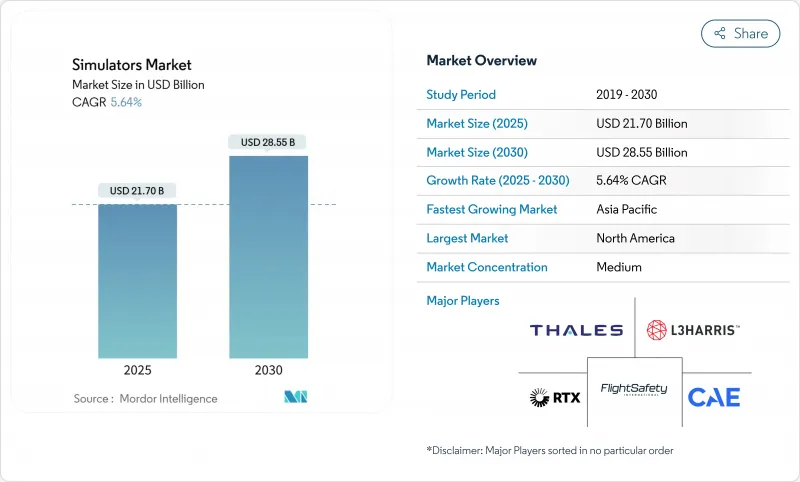

시뮬레이터 시장은 2025년에 217억 달러로 평가되었고, 2030년에는 285억 5,000만 달러에 이를것으로 예측되며, CAGR은 5.64%를 나타낼 전망입니다.

성장은 국방 현대화 주기 가속화, 항공 훈련 규정 강화, 사용자 진입 비용을 낮추는 서비스 지향적 공급 모델 채택에서 비롯되었습니다. 군 구매처가 지출을 주도했으나, 디지털 트윈 및 AI 기반 브리핑 도구의 가치가 입증되면서 상업 항공사, 드론 운영사, 공정 산업 기업들의 수요가 확대되었습니다. NATO와 미 인도태평양사령부가 의무화한 플랫폼 상호운용성 업그레이드는 교체 수요를 촉발했습니다. 동시에 정밀 서보모터와 UHD 프로젝터의 공급망 병목 현상으로 납기 기간이 연장되면서 방위 기관과 다년 계약을 체결한 대형 공급업체에 유리하게 작용했습니다. 웻리스(Wet-lease) 및 시뮬레이션 서비스(Simulation-as-a-Service) 제공은 접근성을 더욱 확대하여 중소 항공사와 신흥 시장 군대가 대규모 자본 투자 없이도 고성능 장비로 훈련할 수 있게 했습니다.

NATO 표준화 협정 4603호와 미 인도태평양사령부의 태평양 다중 영역 훈련 및 실험 능력(Pacific Multi-Domain Training and Experimentation Capability)은 기존에 분리된 훈련장을 연결함으로써, 공급업체들이 신규 장비에 고수준 아키텍처(High-Level Architecture) 게이트웨이와 분산형 상호작용 시뮬레이션(Distributed Interactive Simulation) 브리지를 내장하도록 강제했습니다. 캐나다, 호주, 일본도 최근 입찰에서 네트워크 지원 시뮬레이터를 의무화하며 전통적인 비행 훈련을 넘어 사이버, 해상, 우주 임무 리허설 분야로 조달 범위를 확대했습니다.

유럽연합 항공안전청(EASA)은 항공사들이 작업 목록 중심 교육에서 역량 기반 시나리오로 전환하도록 하는 증거 기반 훈련 지침을 확정했습니다. 이로 인해 기종별 레벨-D 시뮬레이터 훈련 시간이 증가했습니다. 미국 연방항공청(FAA)은 약 23억 달러 규모의 ‘시뮬레이션 및 훈련 공학 지원(STES)’ 프로그램을 통해 동일한 접근법을 도입했습니다. 이로 인해 장비 활용률이 상승하며 역량 증명을 기록하는 소프트웨어 업그레이드 및 데이터 분석 패키지에 대한 안정적인 애프터마켓 수요가 창출되었습니다.

2023년 연합군 상호운용성 시험에서 아시아태평양 연방 객체 모델과 연결 시 NATO DIS 및 HLA 트래픽이 전술 네트워크를 과부하시켜 고속 전투기 시나리오 중 정확도가 저하되는 것으로 드러났다. NATO 모델링·시뮬레이션 전문센터(M&S COE)가 새로운 연방 객체 모델을 발표했으나, 소규모 국가의 기존 시스템 개조 비용이 여전히 높아 합동 훈련 일정이 지연되고 있습니다.

항공 시뮬레이터 부문은 2024년 매출의 42.58%를 차지하며 시뮬레이터 시장의 핵심 역할을 재확인했습니다. 항공모함 조종사 부족, 증거 기반 반복 훈련, 신규 항공기 도입으로 주문량이 지속적으로 유지되었습니다. 해상 시뮬레이터 부문은 규모는 작지만 해군이 교실용 함교 훈련 장비를 연안 전투 시나리오를 지원하는 네트워크 연결형 고동작 장치로 교체함에 따라 연평균 6.42% 성장할 것으로 전망됩니다. 콩스베르그의 DP3 앵커 핸들링 시뮬레이터가 해양 고객사에 판매된 사례가 이러한 변화를 부각시켰습니다. 지상 기반 장갑차 훈련기는 미군의 합성 훈련 환경 프로그램으로 계속 혜택을 보았으나, 해상 응용 분야에 비해 성장세는 여전히 완만했습니다.

해상 구매자들은 함정이 임무를 수행하는 동안 승조원이 훈련할 수 있는 내장형 솔루션을 요구했습니다. L3해리스는 작전 센서와 통합되는 함정용 콘솔을 선보여 가동 중단 시간과 임무 차질을 줄였다. 대학 및 상선사관학교도 통합 엔진실 및 항해 장비에 투자하며 방위 분야를 넘어선 사용자 기반 확대를 시사했습니다.

실전-가상-구성(LVC) 방식은 2024년 매출 점유율 35.17%를 기록했는데, 이는 NATO와 미 공군이 전력 생성 준비 태세를 위해 다중 영역 합성 환경을 의무화했기 때문입니다. 현재 장치는 단일 연방 내에서 공중, 해상, 지상, 사이버, 우주 요소를 복제하여 구매자들이 기존 하드웨어와 미들웨어를 업그레이드하도록 유도하고 있습니다. 그러나 게임 및 시리어스 게임 하위 부문은 국방부가 경제성과 민첩성을 위해 상용 게임 엔진을 채택함에 따라 모든 기술 중 가장 높은 8.03%의 연평균 성장률(CAGR)을 기록할 전망입니다.

시리어스 게임 플랫폼 도입은 언리얼 또는 유니티 프레임워크를 라이선스하고 군사 콘텐츠를 층화하는 초급 공급업체의 공급망을 창출하여 가격을 낮추었습니다. 이러한 변화는 풀모션 LVC 장비가 여전히 비용 부담이 큰 신흥 경제국에서의 접근성을 개선했습니다.

북미는 2024년 전 세계 매출의 37.42%를 차지했으며, 이는 미국 국방부가 2025 회계연도에 시뮬레이터 대량 구매 및 연구개발(R&D) 자금을 포함해 총 8,330억 달러를 배정한 데 따른 결과입니다. 캐나다의 P-8A 순찰기 및 코모란트 헬리콥터 중간 수명 연장 프로그램은 번들 시뮬레이터 구매를 통해 추가 물량을 창출했습니다. 연방항공청(FAA) 계약은 민간 부문 성장을 지원했으며, 록히드 마틴의 THAAD 및 F-35 업그레이드 노력으로 인해 미사일 방어 및 스텔스 전투기 훈련기 제작사들이 바쁜 모습을 보였습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 6.28%를 기록하며 가장 빠르게 성장하는 시장으로 부상했습니다. 일본의 2025 회계연도 국방 예산은 가상 시험대에 의존하는 무인 시스템, 인공지능(AI), 사이버 분야를 우선시했습니다. 시마에로(Simaero)의 창사(長沙) 6베이 센터 사례에서 보듯, 중국의 민간 항공 확장은 지속되었습니다. 대만의 eVTOL 의료 이니셔티브와 호주의 AUKUS 잠수함 훈련 파이프라인은 특수 해군 및 회전익기 수요를 추가하며 지역 솔루션 구성을 확대했습니다.

유럽은 NATO 상호운용성 의무에 힘입어 안정세를 유지했습니다. EASA의 증거 기반 훈련 규정은 항공사 시뮬레이터 운용 시간을 증가시켰으며, 루마니아 등 회원국들은 국가 방위 전략에 모델링 및 시뮬레이션 목표를 포함시켰습니다. 영국 국방부는 조달 비용 리스크 완화를 위해 개방형 표준 채택을 장려한 반면, 독일은 해군 및 회전익 훈련기를 현대화하여 거시경제적 역풍 속에서도 주문 파이프라인을 안정적으로 유지했습니다.

The simulators market stood at USD 21.70 billion in 2025 and is forecast to reach USD 28.55 billion by 2030, advancing at a 5.64% CAGR.

Growth stemmed from accelerating defense-modernization cycles, tightening aviation-training rules, and adopting service-oriented delivery models that lower user entry costs. Military buyers continued to dominate spending, yet commercial airlines, drone operators, and process-industry firms broadened demand as digital-twin and AI-powered debrief tools proved their value. Platform interoperability upgrades mandated by NATO and the US Indo-Pacific Command created a replacement wave. At the same time, supply-chain bottlenecks in precision servomotors and UHD projectors prolonged lead times, favoring larger vendors that hold multi-year contracts with defense agencies. Wet-lease and simulation-as-a-service offerings further democratized access, enabling smaller air carriers and emerging-market militaries to train on high-fidelity devices without large capital outlays.

The NATO Standardization Agreement 4603 and the US Indo-Pacific Command's Pacific Multi-Domain Training and Experimentation Capability linked previously isolated ranges, forcing vendors to embed High-Level Architecture gateways and Distributed Interactive Simulation bridges inside new devices.Canada, Australia, and Japan followed suit by stipulating network-ready simulators in recent tenders, expanding a procurement pool beyond traditional flight training into cyber, maritime, and space mission rehearsal.

The European Union Aviation Safety Agency finalized Evidence-Based Training guidance that moves airlines from task-list syllabi to competency-driven scenarios, increasing the number of Level-D simulator hours per type rating. The US Federal Aviation Administration mirrored this approach through its Simulation and Training Engineering Support program, which is valued at about USD 2.3 billion.Device utilisation rates rose, creating steady aftermarket demand for software upgrades and data analytics packages documenting competency evidence.

Coalition Warrior Interoperability trials in 2023 revealed that NATO DIS and HLA traffic overloaded tactical networks when connected to Asia-Pacific Federation Object Models, degrading fidelity during fast-jet scenarios. The NATO Modelling & Simulation Centre of Excellence (M&S COE) published a new federation object model, but retrofitting legacy systems remains expensive for smaller nations, delaying joint-exercise scheduling.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The airborne segment generated 42.58% of 2024 revenue, confirming its central role in the simulators market. Carrier pilot shortages, evidence-based recurrent training, and new aircraft introductions kept order books full. The maritime segment, while smaller, is forecast to expand at a 6.42% CAGR as navies replace classroom bridge trainers with network-ready, high-motion devices that support littoral combat scenarios. Kongsberg's DP3 anchor-handling simulator sale to an offshore client highlighted this shift. Land-based armored-vehicle trainers continued to benefit from the US Army's Synthetic Training Environment program, yet growth remained moderate compared with seaborne applications.

Maritime buyers requested embedded solutions that allow crews to train while ships stay on task. L3Harris fielded on-board consoles that integrate with operational sensors, reducing downtime and mission disruption. Colleges and merchant-marine academies also invested in integrated engine rooms and navigation suites, signaling a broadening user base beyond defense.

Live-Virtual-Constructive (LVC) methods owned a 35.17% revenue share in 2024 as NATO and the US Air Force mandated multi-domain synthetic environments for force-generation readiness. Devices now replicate air, maritime, land, cyber, and space elements inside a single federation, pushing buyers to upgrade legacy hardware and middleware. However, the gaming and serious-games subset will chart a 8.03% CAGR, the strongest rate of any technique, as defense ministries adopt commercial game engines for affordability and agility.

Adopting serious-games platforms created a pipeline of entry-level suppliers that license Unreal or Unity frameworks and layer military content, driving down price points. This shift improved accessibility in emerging economies where full-motion LVC devices remain cost-prohibitive.

The Simulators Market Report is Segmented by Platform (Airborne, Land, and Maritime), Technique (Synthetic Environment Simulation, and More), Solution (Hardware, Software, and Services), Application (Commercial Pilot and Crew Training, and More), End Use (Commercial and Military), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America secured 37.42% of global revenue in 2024 after the US Department of Defense allocated USD 833 billion for FY 2025, including substantial simulator procurement and R&D funding. Canada's P-8A patrol aircraft and Cormorant helicopter mid-life programs added further volume through bundled simulator buys. Federal Aviation Administration contracts supported civil growth, and Lockheed Martin's THAAD and F-35 upgrade efforts kept device makers busy with missile defense and stealth fighter trainers.

Asia-Pacific emerged as the fastest-growing theatre, tracking a 6.28% CAGR to 2030. Japan's FY 2025 defense budget prioritised unmanned systems, AI, and cyber, all reliant on virtual testbeds.As illustrated by Simaero's six-bay centre in Changsha, China's civil aviation expansion continued. Taiwan's eVTOL medical initiative and Australia's AUKUS submarine training pipeline added specialised naval and rotorcraft demand, widening the regional solution mix.

Europe held steady on the back of NATO interoperability mandates. EASA's Evidence-Based Training rule increased airline simulator hours, and member states such as Romania embedded modelling-and-simulation targets inside national defence strategies. The UK Ministry of Defence promoted open-standards adoption to de-risk procurement cost, while Germany modernised naval and rotary-wing trainers, keeping order pipelines consistent despite macroeconomic headwinds.