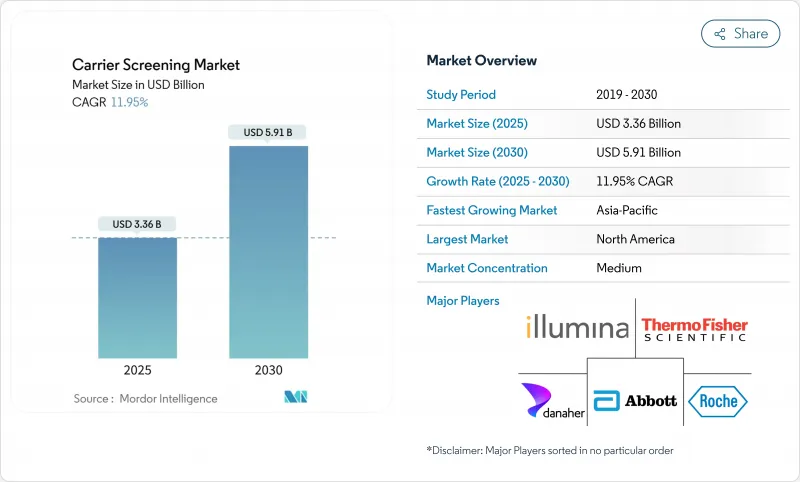

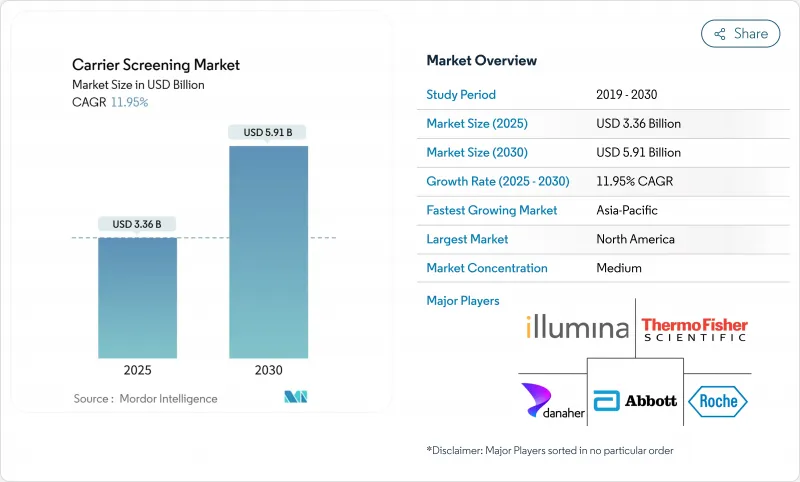

세계의 캐리어 스크리닝 시장은 2025년 33억 6,000만 달러로 평가되었고, 2030년에는 59억 1,000만 달러로 성장할 것으로 예측됩니다.

성장 촉진요인은 차세대 염기서열 분석 비용 하락, 강화되지만 명확해진 실험실 개발 검사 규정, 그리고 불임 치료 전반에 걸친 유전자 검사의 심화된 통합에서 비롯됩니다. 의료 제공자들은 이제 캐리어 스크리닝를 일상적인 생식 결정 과정에 통합하고 있으며, 고용주 유전자 혜택 프로그램, 확대된 보험 적용 범위, 인구 대상 시범 사업이 검사량을 촉진하고 있습니다. 참조 실험실 간 통합은 규모의 경제를 가속화하며, 다중 유전자 패널 채택은 단일 유전자 분석에서 광범위하고 비용 효율적인 유전체 검사로의 전환을 시사합니다. 동시에 훈련된 유전 상담사 부족과 불균등한 보험 적용은 단기적 확장을 제한하며, 이해관계자들에게 원격 유전학 및 AI 기반 결과 해석 도입을 촉구하고 있습니다.

보험사 및 공중보건 기관들은 포괄적 유전체 검사를 선택적 서비스가 아닌 비용 절감 방안으로 점점 더 인식하고 있습니다. 영국과 뉴욕시의 대규모 신생아 프로그램(20만 명 대상)은 예방적 유전체학으로의 전환을 더욱 부각시킵니다. 가이징거의 마이코드 프로그램은 참가자 30명 중 1명에게서 임상적 조치 가능 결과를 발견했으며, 대부분은 유전적 위험을 인지하지 못했습니다. 이러한 임상적, 재정적 가치 입증은 광범위한 다유전자 캐리어 스크리닝의 확산을 촉진하며, 예방적 유전체학을 일상적 진료로 정착시키고 있습니다.

보조생식술은 이제 양측 배우자에 대한 유전자 검사를 기본으로 합니다. 존스홉킨스 불임센터는 조상 배경과 무관하게 모든 환자에게 400개 이상의 열성 질환을 포괄하는 확장 패널 검사를 권고합니다. 비침습적 배아 검사는 생검 관련 생존 가능성 우려 없이 착상 전 유전자 평가를 가능하게 하여 환자의 수용성을 높입니다. 호주의 메디케어(Medicare)가 생식 캐리어 스크리닝에 대한 비용을 보상하는 것은 이러한 사전 계획에 대한 공식적 지지를 강조합니다. 부부들은 이제 임신 전 유전체적 명확성을 원하며, 이는 클리닉들이 캐리어 스크리닝를 일상적인 불임 치료 워크플로우에 통합하도록 촉구하고 캐리어 스크리닝 시장 내 검사량을 증가시키고 있습니다.

유나이티드헬스케어는 메디케어 어드밴티지 보장 범위에서 보균자 검사를 명시적으로 제외하며, 제한된 CPT 코드는 새로운 패널에 대한 청구 절차를 복잡하게 만듭니다. 벨기에에서는 신생아 유전체 검사당 365유로가 기록되어 기존 검사보다 훨씬 높아 보건 시스템 예산에 부담을 주고 있습니다. 정책의 파편화는 저소득 지역에서의 포괄적 검사 확산을 지연시킵니다.

분자 검사는 2024년 매출의 63.18%를 차지했으며, 13.36%의 연평균 성장률(CAGR)로 발전 중이며, 민감도와 다중 검사 범위 측면에서 생화학적 방법을 능가하고 있습니다. 이러한 우위는 공급자들이 간접적인 대사 산물 대리인보다 직접적인 변이 검출을 선호함에 따라 보인자 선별 시장을 주도하고 있습니다. 중국 남부의 지중해성 빈혈 대립 유전자 프로토콜에 대한 포괄적인 분석은 보인자 유병률이 16%를 초과하는 초고속 시퀀싱의 효능을 보여줍니다.

생화학적 검사는 여전히 효소 또는 단백질 질환에 중요하며, 벨기에의 BabyDetect와 같은 신생아 프로그램에서 유전체 검사와 잘 결합됩니다. 경제성 분석은 특정 대사 질환 시나리오에서 탠덤 질량 분석법의 가치를 확인하여, 분자 검사 확대와 함께 다양한 검사 메뉴가 지속될 것임을 보장합니다.

낭포성 섬유증은 보편적인 지침과 보험사들의 친숙함 덕분에 2024년 59.46%의 점유율을 유지하며, 캐리어 스크리닝 시장 점유율의 큰 부분을 차지했습니다. 확장된 100개 변이 CFTR 패널은 다민족 집단에서 검출률을 높입니다.

연골근위축증은 12.73%의 연평균 복합 성장률(CAGR)이 예상되며, 혁신적 치료법과 대부분의 신생아 패널 포함으로 혜택을 봅니다. 테이-삭스병, 고셔병, 겸상적혈구증에 대한 혈통 기반 프로그램은 지속되는 한편, 시퀀싱 비용 하락으로 희귀 상염색체 열성 질환이 주목받고 있습니다.

북미는 고용주 유전자 혜택, 강력한 상담 네트워크, 감독과 혁신의 균형을 맞춘 FDA 프레임워크의 강점을 바탕으로 2024년 매출의 44.18%를 차지했습니다. 가이징거의 마이코드(MyCode) 등록자가 17만 5,000명을 넘어 인구 유전체학에 대한 수요를 입증했습니다. 사우스캐롤라이나의 ‘우리 DNA 속으로(In Our DNA)’ 프로젝트는 10만명 목표 중 5만명의 참가자를 모집하며 주 차원의 추진력을 강화했습니다.

아시아태평양 지역은 13.83%의 연평균 성장률(CAGR)로 가장 강력한 성장세를 보입니다. 중국의 iHope 프로젝트는 2024년 중반까지 513개 희귀질환 가정을 지원했으며, 2026년까지 1,800개 가정 지원을 목표로 합니다. 한편, 전국적 지중해빈혈 검진은 남부 지방의 최대 24%에 달하는 보인자 비율 문제를 해결하고 있습니다. 호주의 메디케어 지원 패널은 지역 내 보험 적용 선례를 마련했습니다.

유럽은 균형 잡힌 확장을 기록 중입니다. 영국은 신생아 유전체 10만 건 시퀀싱을 목표로 하며, 벨기에의 유전체 신생아 선별검사 부모 동의율 90%는 공공 신뢰를 입증합니다. 이스라엘 보건부는 290개 유전자로 구성된 650개 변이 프로그램에 자금을 지원하며 광범위한 패널에 대한 정부 지원을 강조합니다.

The global carrier screening market stood at USD 3.36 billion in 2025 and is forecast to climb to USD 5.91 billion by 2030, registering an 11.95% CAGR over the period.

Growth stems from falling next-generation sequencing prices, tightening but clearer Laboratory Developed Test rules, and deeper integration of genetic screening across fertility medicine. Providers now weave carrier testing into routine reproductive decision-making, while employer genetic-benefit programs, wider insurance coverage, and population pilots boost test volumes. Consolidation among reference laboratories accelerates scale advantages, and multi-gene panel uptake signals a shift from single-gene assays toward broad, cost-effective genomic screens. At the same time, shortages of trained genetic counselors and uneven reimbursement temper near-term expansion, pressing stakeholders to adopt tele-genetics and AI-supported result interpretation.

Payers and public-health agencies increasingly see comprehensive genomic screening as a cost-saving path rather than a discretionary service. Australia's microsimulation of 569 recessive disorders predicted 2,067 affected births avoided at 50% test uptake, dwarfing outcomes from limited panels.Large newborn initiatives in the United Kingdom and New York City covering 200,000 infants further spotlight the pivot toward preventive genomics.Geisinger's MyCode program found clinically actionable results in 1 in 30 participants, most of whom were unaware of inherited risks. These demonstrations of clinical and fiscal value propel wider adoption of broad multi-gene carrier screening, cementing preventive genomics as routine care.

Assisted reproduction now defaults to genetic scrutiny for both partners. Johns Hopkins Fertility Center recommends expanded panels covering more than 400 recessive conditions for every patient regardless of ancestry. Non-invasive embryo assays allow preimplantation genetic assessment without biopsy-related viability concerns, easing patient acceptance. Australia's Medicare reimbursement for reproductive carrier screening underscores official endorsement of such proactive planning. Couples now desire genomic clarity before pregnancy, pushing clinics to embed carrier testing into routine fertility workflows and lifting test volumes within the carrier screening market.

UnitedHealthcare explicitly excludes carrier tests from Medicare Advantage coverage, and limited CPT codes complicate claims for novel panels. Belgium recorded EUR 365 per newborn genomic test, well above conventional screens, challenging health-system budgets. Fragmented policies slow the spread of comprehensive screening in lower-income regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Molecular assays commanded 63.18% of 2024 revenue and are advancing at 13.36% CAGR, eclipsing biochemical methods in sensitivity and multiplexing scope. This dominance propels the carrier screening market as providers prefer direct variant detection over indirect metabolite proxies. The Comprehensive Analysis of Thalassemia Alleles protocol in southern China illustrates the efficacy of ultra-high-throughput sequencing where carrier prevalence exceeds 16%.

Biochemical screens still matter for enzyme or protein conditions and blend well with genomic assays in newborn programs such as Belgium's BabyDetect. Economic analyses confirm tandem mass spectrometry's value in certain metabolic scenarios, ensuring that diversified testing menus persist alongside molecular expansion.

Cystic fibrosis retained 59.46% share in 2024 thanks to universal guidelines and payer familiarity, securing a large slice of the carrier screening market share. Expanded 100-variant CFTR panels raise detection rates in multiethnic populations.

Spinal muscular atrophy, projected at 12.73% CAGR, benefits from transformative therapies and inclusion in most newborn panels. Ancestry-driven programs for Tay-Sachs, Gaucher, and sickle cell disease continue, while rare autosomal recessive conditions gain traction as sequencing costs fall.

Carrier Screening Market Report is Segmented by Test Type (Molecular Screening Test and Biochemical Screening Test), Disease Type (Cystic Fibrosis, Tay-Sachs Disease and More), Panel Type (Targeted Single-Gene Panels, Ethnicity-Specific Panels and More), Technology (NGS, PCR and More), End User (Hospitals & Clinics, Diagnostic Laboratories and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America secured 44.18% revenue in 2024 on the strength of employer genetic benefits, robust counseling networks, and an FDA framework that balances oversight with innovation. Geisinger's MyCode enrollment surpassed 175,000 individuals, evidencing appetite for population genomics. South Carolina's In Our DNA initiative recruited 50,000 participants toward a 100,000 goal, reinforcing state-level momentum.

Asia-Pacific exhibits the strongest growth at 13.83% CAGR. China's iHope project assisted 513 rare-disease families by mid-2024 and targets 1,800 by 2026, while national thalassemia screening addresses carrier rates up to 24% in southern provinces. Australia's Medicare-funded panels set a regional precedent for reimbursement.

Europe records balanced expansion. The UK aims to sequence 100,000 newborn genomes, while Belgium's 90% parental acceptance rates for genomic newborn screening prove public trust. Israel's Ministry of Health funds a 650-variant program comprising 290 genes, underlining governmental support for broad panels.