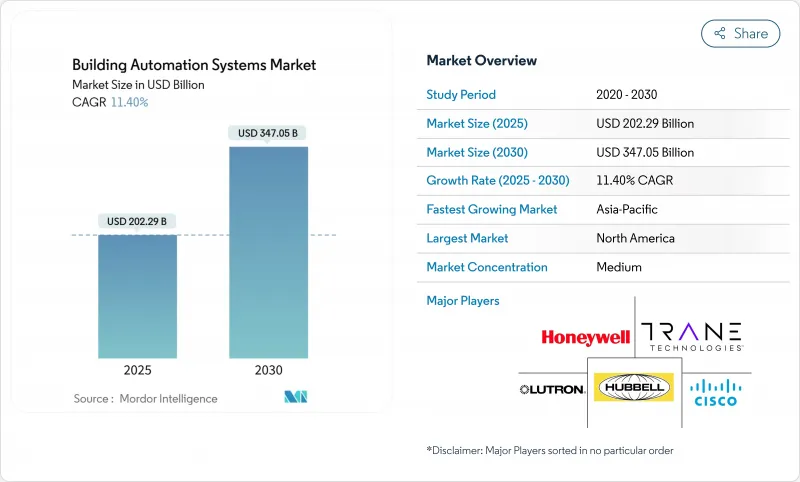

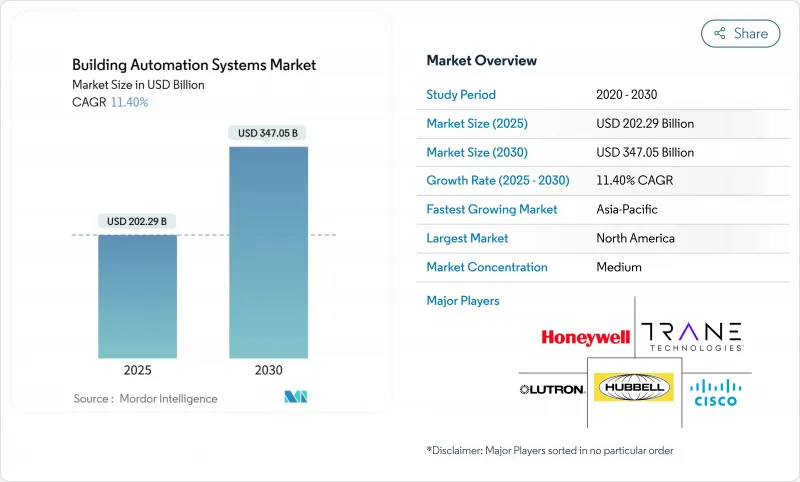

빌딩 자동화 시스템 시장 규모는 2025년에 2,022억 9,000만 달러로 평가되었고, CAGR은 11.40%를 나타낼 것으로 예측되며 2030년에는 3,470억 5,000만 달러에 달할 전망입니다.

상업 시설 에너지 비용의 50%를 차지하는 HVAC는 여전히 주요 비용 요인으로, HVAC를 조명 및 보안 시스템과 연계하는 자동화 플랫폼에 대한 투자가 우선적으로 이루어지고 있습니다. 캘리포니아주의 2025년 타이틀 24 기준에 따라 모든 신규 비주거용 프로젝트는 OpenADR 프로토콜을 따르는 수요 반응형 제어 시스템을 반드시 포함해야 합니다. 미국 에너지부는 ASHRAE 90.1-2022가 2019년판 대비 상업용 건물 효율을 9.8% 향상시킬 것으로 판단했습니다. EU와 아시아태평양 지역의 유사한 프레임워크는 정확한 탄소 배출 보고를 요구하므로, 소유주들은 자동화를 선택 사항이 아닌 필수 요소로 인식하고 있습니다. 시장 선도 기업들은 전략적 인수를 통해 제품 범위를 확대하고 장기 서비스 계약을 확보하는 한편, 무선 BACnet은 리모델링 프로젝트의 설치 시간을 70% 단축합니다.

새로운 에너지 규정은 자동화를 선택적 업그레이드에서 규제 요건으로 전환시키고 있습니다. EU 건물 에너지 성능 지침은 모든 주거용 건물이 2030년까지 최소 E등급, 2033년까지 D등급을 달성하도록 의무화하여 소유주들이 조명, HVAC, 계량 시스템을 자동화하도록 강제합니다. 캘리포니아의 2025년 규정은 비주거용 HVAC 시스템에 대한 원격 설정점 조정을 요구하며, 4,000W 이상의 조명 부하에는 15% 자동 전력 감축을 제공해야 합니다. 미시간주는 ASHRAE 90.1-2022를 반영한 새로운 상업용 코드를 도입했습니다. 이러한 표준은 기존의 투자 회수 논쟁을 없애고 건물 자동화 시스템 시장의 지속적인 성장 기반을 마련합니다.

재정 정책은 초기 자본 지출을 낮춤으로써 규제를 보완합니다. 미국에서는 인프라 투자 및 일자리 법안(IIJA)과 인플레이션 감축법(IRA)이 자동화 하드웨어 및 소프트웨어를 지원하며, 슈나이더 일렉트릭의 1억 4,000만 달러 규모 테네시 공장 확장 프로젝트 등을 뒷받침합니다. 캘리포니아 대학 샌디에이고 캠퍼스의 무선 온도조절기 프로젝트 비용은 유틸리티 리베이트로 295,700달러에서 14,600달러로 절감되어 0.2년의 투자 회수 기간을 달성했습니다. 아시아태평양 지역에서는 싱가포르의 그린 빌딩 마스터 플랜이 스마트 빌딩 개조 비용의 최대 50%를 지원하는 보조금을 제공합니다. 이러한 인센티브는 건물 자동화 시스템 시장 전반에서 도입 곡선을 가속화하고 판매 주기를 단축시킵니다.

개조 프로젝트는 장비 가격을 초과할 수 있는 인건비 및 배선 비용을 극복해야 합니다. 허니웰의 '건물용 어드밴스드 컨트롤'은 기존 케이블을 활용해 개조 설치 시간을 40% 단축하지만, 소규모 시설은 여전히 자본 제약에 직면합니다. 에너지 서비스 계약(ESA)과 같은 금융 솔루션은 태양광 전력구매계약(PPA) 구조에 비해 미비하여 인센티브가 제한된 시장에서 도입 속도를 저해합니다.

하드웨어는 센서, 컨트롤러, 현장 장치를 중심으로 2024년 매출의 55.90%를 차지합니다. 그러나 소유주들이 영구 라이선스에서 구독 모델로 전환함에 따라 소프트웨어 부문은 12.40%의 연평균 성장률(CAGR)을 기록 중입니다. 빌딩 자동화 시스템 시장의 소프트웨어 규모는 2030년까지 1,320억 달러에 달할 것으로 예상되며, 이는 전체 매출의 38%에 해당하는 수치로 2024년 29%에서 증가한 것입니다. 슈나이더 일렉트릭의 SaaS 포트폴리오는 2024년 140% 성장하여 데이터 분석, 원격 진단 및 사이버 보안 서비스가 반복 수익을 창출하는 방식을 보여줍니다.

증가된 가치의 상당 부분은 서로 다른 장치를 연결하는 클라우드 API를 통해 실현됩니다. 존슨컨트롤스의 평탄화된 메타시스(Metasys) 아키텍처는 통합 시간을 절반으로 줄이고 장치 처리량을 향상시키는 반면, 허니웰의 커넥티드 솔루션(Connected Solutions)은 성과 기반 계약으로 하드웨어와 소프트웨어를 묶어 제공합니다. 그 결과, 빌딩 자동화 시스템 시장은 초기 자본 주기보다 자산 수명 전반에 걸쳐 최적화하는 소프트웨어 정의 솔루션으로 계속 이동하고 있습니다. 이러한 전환은 또한 규제 기관들이 조달 지침에 규정화하기 시작한 사이버 보안 및 데이터 주권 문제를 부각시킵니다.

보안 및 접근 제어는 2024년 매출 점유율 50.30%를 유지하며 기업의 위험 완화 우선순위를 반영했습니다. 건물 에너지 관리 시스템은 연평균 11.80% 성장률을 보이며, 건물 자동화 시스템 시장 내 점유율이 2024년 19%에서 2030년까지 24%로 상승할 전망입니다. 유틸리티 기업들은 현재 연간 kW당 60-100달러의 피크 절감 수수료를 지불하며 에너지 관리 투자 회수율을 개선하고 있으며, 수요 반응 프로그램은 동적 부하 감축에 대한 보상을 제공합니다. ABB와 삼성은 주거용 에너지 관리를 SmartThings Pro에 통합하여 상업용 자동화와 소비자 IoT 영역 간의 융합을 부각시키고 있습니다.

에너지 규정은 HVAC, 조명, 플러그 부하에서 데이터를 수집하는 지속적인 커미셔닝 대시보드를 점점 더 요구하고 있습니다. 따라서 소유주들은 에너지 관리를 추가 옵션이 아닌 기본 건축 사양에 포함시키고 있습니다. 50개 이상 사이트를 보유한 상업용 포트폴리오에서는 포트폴리오 분석을 통해 공과금을 12% 절감하고 기업 배출량 기준선을 축소하여 환경 및 사회 및 지배구조(ESG) 보고를 지원합니다. 이러한 혜택을 프로포마에 반영하는 개발사는 그린론 할인 혜택을 받을 수 있어, 건물 자동화 시스템 시장에 자생적 성장 사이클을 창출합니다.

빌딩 자동화 시스템 시장은 컴포넌트(하드웨어, 소프트웨어, 서비스), 시스템 유형(HVAC 제어 시스템, 조명 제어 시스템, 보안 및 출입 관리 시스템 등), 통신 기술(유선, 무선), 최종 사용자(주거, 상업, 산업, 시설 및 정부), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 38.00%의 매출 점유율을 차지하며, 연방 탈탄소화 의무화 정책에 따라 2029년까지 연방 시설에서 화석 연료 사용을 90% 단계적으로 폐지해야 하므로 2030년까지 선두를 유지할 것으로 전망됩니다. GSA(미국 연방총무청)의 오클라호마시티 연방 건물은 그리드 연동 제어 시스템을 통해 41%의 에너지 절감 효과를 입증하여 다른 기관들의 벤치마크가 되었습니다. 캘리포니아와 미시간주의 주 차원 규정은 민간 프로젝트의 기준을 높이며, 풍부한 세액 공제는 리모델링 포트폴리오의 순비용을 절감합니다.

아시아태평양 지역은 12.20%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국의 제14차 5개년 계획은 스마트 시티 예산에 건물 자동화를 포함시켰으며, 싱가포르의 그린 빌딩 마스터 플랜은 성과 기반 리모델링을 지원합니다. ABB와 삼성은 에너지 분석을 주류 소비자 플랫폼에 통합하기 위해 협력하여 고급 사무실에서 대중 시장 아파트로 수요 가능 영역을 확장하고 있습니다. 신흥 아세안 경제권은 국가 에너지 마스터 플랜이 공공 부문 사용 사례를 지원함에 따라 연간 8.1% 성장을 기록하고 있습니다.

유럽은 2033년까지 점진적 리모델링 목표를 설정하는 '건물 에너지 성능 지침(EPBD)'의 혜택을 받고 있습니다. 독일의 AI 경제는 연간 15% 성장하며 고급 자동화를 뒷받침하는 인재 풀과 R&D 기반을 제공합니다. 북유럽 국가들은 탄소중립 호텔 및 복합 개발을 선도하고 있으며, 덴마크의 알식 호텔(Alsik Hotel)은 고객 예약 시스템과 HVAC를 통합해 지속적인 효율성을 구현한 사례입니다.

The building automation systems market size reached a value of USD 202.29 billion in 2025 and is forecast to reach USD 347.05 billion by 2030, reflecting an 11.40% CAGR.

At 50% of a commercial facility's energy bill, HVAC remains the primary cost driver, so automation platforms that link HVAC with lighting and security are receiving priority investment. California's 2025 Title 24 standards now oblige every new non-residential project to include demand-responsive controls that follow OpenADR protocols. The U.S. Department of Energy has determined that ASHRAE 90.1-2022 will lift commercial building efficiency by 9.8% over the 2019 edition. Similar frameworks in the EU and Asia-Pacific require precise carbon reporting, so owners see automation as essential, not optional. Market leaders are using strategic acquisitions to widen product scope and lock in long-term service contracts, while wireless BACnet cuts installation time by 70% for retrofit projects.

New energy codes are turning automation from a discretionary upgrade into a regulatory requirement. The EU Energy Performance of Buildings Directive obliges every residential building to reach at least an E-rating by 2030 and a D-rating by 2033, forcing owners to automate lighting, HVAC, and metering. California's 2025 rules demand remote set-point adjustment for non-residential HVAC systems, while lighting loads above 4,000 W must provide a 15% automated power reduction. Michigan has joined with a new commercial code that mirrors ASHRAE 90.1-2022. These standards remove the traditional payback debate and establish a durable growth floor for the building automation systems market.

Fiscal policy complements regulation by lowering the initial capital outlay. In the United States, the Infrastructure Investment and Jobs Act and the Inflation Reduction Act subsidize automation hardware and software, supporting projects such as Schneider Electric's USD 140 million Tennessee plant expansion. Utility rebates cut the University of California, San Diego's wireless thermostat project cost from USD 295,700 to USD 14,600, delivering a 0.2-year payback. In Asia-Pacific, Singapore's Green Building Master Plan offers grants that cover up to 50% of smart-building retrofit expenses. Such incentives accelerate adoption curves and shorten sales cycles across the building automation systems market.

Retrofit projects must overcome labor and wiring expenses that can outstrip equipment prices. Honeywell's Advance Control for Buildings leverages existing cabling to cut retrofit installation time by 40%, yet smaller properties still face capital constraints. Financing solutions such as energy-service agreements remain underdeveloped compared with solar PPA structures, creating a drag on deployment velocity in markets where incentives are limited.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware still provides 55.90% of 2024 revenue, primarily through sensors, controllers, and field devices. Software, however, is growing at a 12.40% CAGR as owners shift from perpetual licenses to subscription models. The building automation systems market size for software is projected to reach USD 132 billion by 2030, equal to 38% of total revenue, up from 29% in 2024. Schneider Electric's SaaS portfolio climbed 140% in 2024, showing how data analytics, remote diagnostics, and cybersecurity services create recurring revenue.

Much of the incremental value is unlocked through cloud APIs that link disparate devices. Johnson Controls' flattened Metasys architecture halves integration time and boosts device throughput, while Honeywell's Connected Solutions bundles hardware and software in an outcome-based contract. As a result, the building automation systems market continues to migrate toward software-defined solutions that optimize over the asset life rather than the initial capital cycle. That migration also elevates cybersecurity and data-sovereignty questions that regulators are starting to codify in procurement guidelines.

Security and access control retained a 50.30% revenue share in 2024, reflecting corporate risk mitigation priorities. Building energy management systems are expanding at an 11.80% CAGR, and their share of the building automation systems market size is set to rise from 19% in 2024 to 24% by 2030. Utilities now pay peak-shaving fees of USD 60-100 per kW per year, improving energy management payback, while demand-response programs reward dynamic load shedding. ABB and Samsung are integrating residential energy management into SmartThings Pro, highlighting convergence between commercial automation and the consumer IoT domain.

Energy codes increasingly require continuous commissioning dashboards that pull data from HVAC, lighting, and plug loads. Owners, therefore, bundle energy management into base-build specifications rather than treating it as an add-on. In commercial portfolios above 50 sites, portfolio analytics reduce utility bills by 12% and shrink corporate emissions baselines, supporting environmental, social, and governance reporting. Developers who factor these benefits into pro-formas gain access to green loan discounts, creating a self-reinforcing cycle for the building automation systems market.

Building Automation and Control System Market is Segmented by Component (Hardware, Software, Services), System Type (HVAC Control Systems, Lighting Control Systems, Security and Access Control Systems, and More), Communication Technology (Wired, Wireless), End-User (Residential, Commercial, Industrial, and Institutional/Government), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America holds a 38.00% revenue share and is projected to preserve its lead through 2030 as federal decarbonization mandates require a 90% fossil-fuel phase-out in federal facilities by 2029. The GSA's Oklahoma City Federal Building validated a 41% energy cut through grid-interactive controls, creating a benchmark for other agencies. State-level codes in California and Michigan raise the baseline for private projects, and generous tax credits reduce net costs for retrofit portfolios.

Asia-Pacific is the fastest-growing territory with a 12.20% CAGR. China's 14th Five-Year Plan embeds building automation in smart city budgets, while Singapore's Green Building Master Plan underwrites performance-based retrofits. ABB and Samsung have teamed up to integrate energy analytics into mainstream consumer platforms, expanding addressable demand from high-end offices to mass-market apartments. Emerging ASEAN economies post 8.1% annual growth as national energy master plans fund public-sector use cases.

Europe benefits from the Energy Performance of Buildings Directive, which sets progressive renovation targets through 2033. Germany's AI economy is expanding at 15% per year, providing a talent pool and R&D base that underpins advanced automation. Northern European countries lead on net-zero hotel and mixed-use developments, exemplified by Denmark's Alsik Hotel, which integrates guest-booking systems with HVAC for continuous efficiency.