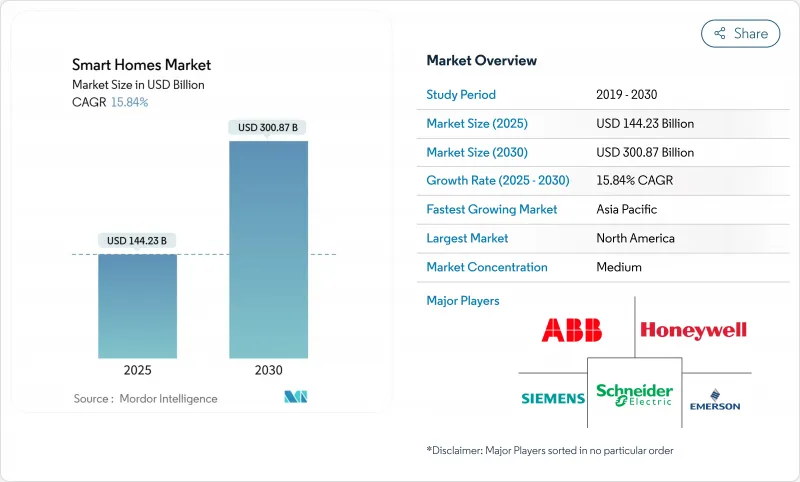

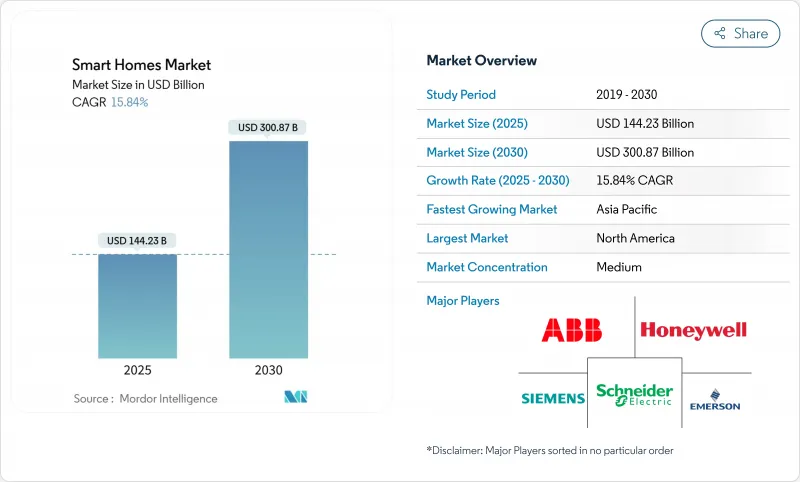

스마트홈 시장 규모는 2025년에 1,442억 3,000만 달러, 2030년에는 3,008억 7,000만 달러에 이르고, CAGR은 15.8%를 나타낼 전망입니다.

이 성장은 에너지 비용의 인플레이션, 탈탄소화 정책, 기술의 융합으로 인해 커넥티드 리빙이 프리미엄 참신함에서 기본적인 주택 인프라로 이동하고 있기 때문입니다. 대규모 연방 정부의 우대 조치가 북미의 리더십을 지원하는 반면, 아시아태평양은 도시화와 스마트 시티 프로그램을 배경으로 가장 빠르게 확대되고 있습니다. 5G, 인공지능, Matter 상호 운용성 프로토콜의 융합은 비용과 복잡성의 장벽을 침식하고 부유한 초기 사용자 외에도 채택을 넓혀줍니다. 기기의 생태계는 단편화된 상태이지만, 건설업체가 신축에 커넥티드 인프라를 도입하고, 집합 주택 사업자가 스마트 솔루션을 채택하여 물건을 차별화함에 따라 플랫폼의 통합이 가속화되고 있습니다.

전기 요금 상승과 기후 변화 목표로 소비자는 소비량을 최적화하고 까다로운 세액 공제를받을 수있는 연결 장치로 향하고 있습니다. 미국에서는 인플레이션 억제법에 따라 대상인 히트펌프, 온수기, 에너지 절약제어기기의 구입비용의 30%가 공제되어 투자회수기간이 대폭 단축됩니다. GE 어플라이언스의 EcoBalance 플랫폼은 옥상 태양광 발전, 축전지, EV 충전기를 통합하여 가정 전체의 오케스트레이션을 가능하게 함으로써 전력 사용량을 20-35% 줄이고 연방정부의 효율화 프로그램을 통해 주택 소유자에게 최대 4,000달러의 리베이트를 얻을 수 있습니다. 송전망의 불안정성에 직면하고 있는 전력회사는 수요 대응 이벤트에의 참가에 대해 커넥티드 어플라이언스의 소유자에게 지불하는 것이 늘고 있어, 키친이나 HVAC 시스템을 분산형 에너지 자산으로 바꾸고 있습니다. 그 결과 얻은 수입원은 부하 삭감의 기회를 예측하고 가전의 평생 가치를 높이는 AI를 통합하는 동기부여가 됩니다.

고속 연결은 신뢰할 수 있는 장비 성능을 지원합니다. 5G 고정 무선 액세스는 이미 미국에서 400만 가구 이상으로 서비스를 제공하고 있으며 실시간 보안 피드와 음성 어시스턴트를 유지하는 파이버 클래스의 속도를 제공합니다. 5G 에지 처리는 안전하고 중요한 기능의 대기 시간을 줄이고 저렴한 IoT 센서의 보급을 가능하게 합니다. 지역 커뮤니티가 가장 혜택을 받는 것은 비용이 많이 드는 마일 파이버를 피하고 전통적으로 남아 있던 층을 위한 스마트 홈 시장을 확보하는 것입니다. 인도와 브라질에서 주파수 대역 경매가 가속화됨에 따라 신흥 시장 전체에서 스마트 홈에 대한 액세스가 확대될 것으로 예측됩니다.

총 홈 시스템은 보통 15,000-4만 달러이며, 평생 에너지 절약 효과가 있음에도 불구하고, 중간 소득층에 있어서는 도입의 허들이 되고 있습니다. 오래된 주택에서는 패널 업그레이드 및 배선 변경이 필요하며 프로젝트 예산이 늘어납니다. 전기나 에어컨의 기술 노동자 부족은 비용을 더욱 상승시킵니다. 리베이트는 저소득 가구에 대해서는 80%의 상쇄가 가능하지만, 사무처리의 복잡성과 환불의 지연은 유효성을 제한하고 있습니다. 송장에 의한 상환과 그린 모기지와 같은 자금 조달의 혁신은 초기 지출을 완화시켜 스마트 홈 시장에의 침투를 가속시킵니다.

액세스 제어, 안전 및 보안은 2024년 매출의 22.1%를 차지하며 주택 소유자가 도난 억제 및 보험료 절약을 우선시하는 동안 스마트 홈 시장을 지원합니다. 스마트락은 현재 생체인증 정보를 통합하고 배달원의 감사 추적을 생성하고 있습니다. 헬스케어 컴포넌트의 스마트홈 시장 규모는 만성질환 관리가 주택으로 전환됨에 따라 CAGR 16.2%로 상승하여 가장 빠르게 확대될 것으로 예측됩니다. 음성 제어 허브는 복약 지도를 겸하고 연결된 청진기는 임상의에게 실시간 생명력을 전달합니다. 유틸리티 기업은 자동화된 수요 반응에 대한 청구 크레딧을 제공함으로써 에너지 관리 시스템을 홍보하고 스마트 HVAC는 그리드 상황을 전달하는 AI 최적화 히트 펌프를 통해 견인력을 늘리고 있습니다. 컨트롤러와 허브는 공급업체 간의 페어링을 가능하게 하는 Matter 인증을 통해 상품화에 직면하며, 차별화는 유지보수를 예측하고 편안함 알고리즘을 개선하는 임베디드 분석으로 축족을 옮깁니다.

새로운 카테고리로는 AI가 식사의 목표나 재고에 맞춘 레시피를 추천하는 스마트 키친 등이 있습니다. GE 어플라이언스의 Flavorly 서비스는 식료품 주문과 가전제품 설정을 연결하여 식품 소매와 주택 IoT의 융합을 보여줍니다. 조명은 일루미네이션뿐만 아니라, 서커디안 친화적인 스펙트럼, 전지 없이 동작하는 에너지 수확 스위치로 이행하고 있어, 대규모 주택의 유지관리 비용을 인하하고 있습니다.

단독주택 부동산은 개별 주택 소유자가 자유롭게 기기 에코시스템을 선택하고 전호 패키지를 도입하기 때문에 2024년에는 64.5%의 수익을 지배합니다. 스마트 미터, 옥상 태양열 및 축전지는 EV 충전기와 동기화되어 자체 완성형 에너지 노드를 형성합니다. 집합 주택의 보급은 CAGR16.9%로 그 차이를 줄이고 있으며, 입주율의 향상과 운영 효율의 향상을 요구하는 자산 관리 회사가 뒷받침하고 있습니다. 스마트락은 주택 교체를 간소화하고 에너지 대시보드는 서브미터 데이터를 공개하여 임차인에게 청구의 투명성을 향상시킵니다. 하이테크 설비를 갖춘 아파트 임대 프리미엄은 5-25%로 지속적인 투자 동기 부여가 되고 있습니다. 입주자가 관리하는 액세스 로그와 같은 개인 정보 보호는 입주자에게 허용되는 핵심 요소입니다. 중앙 관리 대시보드를 통해 운영자는 전체 포트폴리오를 시각화할 수 있어 예측 유지 보수가 가능하므로 운영 비용을 줄일 수 있습니다.

스마트홈 시장 보고서는 컴퍼넌트별(가전, 입퇴실 관리, 안전, 시큐리티, 조명, 에너지 관리, 스마트 HVAC/공조 제어, 컨트롤러/허브, 스마트 홈 헬스 케어, 스마트 키친), 주택 유형별(단독주택, 집합 주택), 설치 유형별(신축, 개수), 판매 채널별(온라인, 오프라인), 지역별로 분류되어 있습니다.

북미는 2024년 매출액의 36.4%를 차지했으며, 정책적 인센티브와 광대역 보급에 지지되었습니다. 커넥티드 컨트롤을 포함한 에너지 효율적인 리노베이션에는 1세대당 최대 1만 4,000달러가 회수 가능해 주류로의 흡수를 뒷받침하고 있습니다. 캐나다 주 프로그램은 연방 정부의 지원을 반영하고 연결형 히트 펌프와 모니터링 대시보드를 선호하는 1만 캐나다 달러 보조금과 제로 금리 대출을 발행합니다. 삼성의 SmartThings Energy와 같은 전기자동차와 홈 그리드의 균형을 연결하는 생태계 제휴는 생태계 전체 통합의 지역 리더십을 보여줍니다.

아시아태평양은 급속한 도시화와 정부 주도의 스마트 시티의 청사진에 견인되어 CAGR 16.5%로 가장 급성장하고 있는 분야입니다. 샤오미와 같은 중국의 국산 브랜드는 저렴한 가격의 가정용 번들 제품을 제공하여 대중 시장으로의 보급을 촉진하고 있습니다. 인도에서는 광섬유와 5G의 도입으로 대응 가능한 가구가 확대되고, 싱가포르에서는 간병인에게 이상을 알리는 앰비언트 센싱 기능을 갖춘 고령자용 간병 아파트를 시험적으로 건설하고 있습니다. 이 지역에 제조 거점이 집중되어 있기 때문에 재료비가 억제되고, 엔트리 레벨 솔루션이 신흥 중산 계급에서도 이용 가능하게 되어 스마트 홈 시장의 밑단이 퍼지고 있습니다.

유럽은 엄격한 에너지 지침과 프라이버시 중심의 규제로 안정적인 보급을 보여줍니다. 가정에 대한 스마트 홈 보급률은 2022년까지 1억 1,200만 가구를 돌파해, 2027년에는 47%에 이를 전망입니다. 슈나이더 일렉트릭의 Wiser Home 플랫폼은 AI 예측을 적용하여 요금 피크 시 소비량을 줄이고 송전망의 안정성을 중시하는 대륙을 반영합니다. GDPR(EU 개인정보보호규정)은 로컬 데이터 처리를 촉구하고 공급업체에게 에지 지능형 장비 설계를 촉구합니다. Fit-for-55 패키지의 인센티브는 태양광 발전의 잉여 전력을 수요 반응 시장에 통합함으로써 가정 소유자가 계통 연계 장비를 구입할 때 지불됩니다. 중동 및 아프리카는 아직 막 시작되었지만 사우디아라비아의 NEOM과 같은 대표적인 스마트 시티 구축의 혜택을 누리고 있습니다. 라틴아메리카는 연결 인프라가 성숙하고 브라질의 전국적인 스마트 미터가 전개됨에 따라 소비자가 연결된 생활에 익숙해지면서 발전하고 있습니다.

The smart homes market size is valued at USD 144.23 billion in 2025 and is projected to reach USD 300.87 billion by 2030, advancing at a 15.8% CAGR.

The up-swing stems from energy-cost inflation, decarbonization policies, and technology convergence that shift connected living from premium novelty to baseline residential infrastructure. Sizeable federal incentives anchor North America's leadership, while Asia-Pacific delivers the fastest expansion on the back of urbanization and smart-city programs. The convergence of 5G, artificial intelligence, and the Matter interoperability protocol is eroding cost and complexity barriers, broadening adoption beyond affluent early users. Device ecosystems remain fragmented, yet platform integration is accelerating as builders include connected infrastructure in new construction and multi-family operators adopt smart solutions to differentiate properties.

Rising electricity tariffs and climate targets are propelling consumers toward connected devices that optimize consumption and qualify for generous tax credits. Under the Inflation Reduction Act, U.S. households recoup 30% of purchase costs for qualifying heat pumps, water heaters, and energy-savvy controls, sharply lowering payback periods. GE Appliances' EcoBalance platform integrates rooftop solar, storage, and EV chargers, enabling whole-home orchestration that can trim electricity use 20-35% and earn homeowners rebates up to USD 4,000 through federal efficiency programs. Utilities, facing grid volatility, increasingly pay connected-appliance owners for participating in demand-response events, turning kitchens and HVAC systems into distributed energy assets. The resulting revenue stream motivates manufacturers to embed AI that predicts load-shaving opportunities and boosts lifetime appliance value.

High-speed connectivity underpins reliable device performance. 5G Fixed Wireless Access already serves more than 4 million U.S. households and delivers fiber-class speeds that sustain real-time security feeds and voice assistants. Edge processing over 5G cuts latency for safety-critical functions and allows inexpensive IoT sensors to proliferate. Rural communities benefit most, bypassing costly last-mile fiber and unlocking the smart homes market for demographics traditionally left behind. As spectrum auctions accelerate in India and Brazil, comparable infrastructure gains are expected to broaden smart-home accessibility across emerging markets.

Total-home systems typically range from USD 15,000-40,000, a hurdle for middle-income adopters despite lifetime energy savings. Older dwellings require panel upgrades and rewiring that inflate project budgets. Skilled-labor shortages in electrical and HVAC trades compound costs. Although rebates can offset as much as 80% for low-income households, paperwork complexity and delayed reimbursements limit efficacy. Financing innovations such as on-bill repayment and green mortgages are emerging to soften initial spend and accelerate penetration of the smart homes market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Access Control, Safety, and Security retained 22.1% of 2024 revenue, underpinning the smart homes market as homeowners prioritize burglary deterrence and insurance savings. Smart locks now integrate biometric credentials and generate audit trails for delivery personnel. The smart homes market size for healthcare components is forecast to expand fastest, climbing at 16.2% CAGR as chronic-disease management shifts into residences. Voice-controlled hubs double as medication coaches, and connected stethoscopes stream real-time vitals to clinicians. Utilities catalyze Energy-Management systems by offering bill credits for automated demand response, while Smart HVAC gains traction through AI-optimized heat pumps that communicate grid conditions. Controllers and hubs face commoditization as Matter certification allows multi-vendor pairing; differentiation is pivoting toward embedded analytics that predict maintenance and refine comfort algorithms.

Emergent categories include smart kitchens where AI recommends recipes aligned with dietary goals and inventory. GE Appliances' Flavorly service links grocery ordering to appliance settings, illustrating convergence between food retail and residential IoT. Lighting is shifting beyond illumination to circadian-friendly spectrums and energy harvesting switches that operate without batteries, lowering maintenance costs for large residences.

Single-family properties controlled 64.5% revenue in 2024 as individual homeowners freely select device ecosystems and implement whole-home packages. Smart meters, rooftop solar, and battery storage sync with EV chargers to form self-contained energy nodes. Multi-family adoption is closing the gap at a 16.9% CAGR, propelled by asset managers seeking higher occupancy and operating efficiency. Smart locks simplify unit turnover, and energy dashboards expose sub-meter data that improve tenant billing transparency. Rent premiums in tech-equipped apartments range between 5-25%, motivating continued investment. Privacy safeguards, including resident-controlled access logs, are central to tenant acceptance. Central management dashboards give operators visibility across portfolios, enabling predictive maintenance that restrains operational expenditure.

The Smart Homes Market Report is Segmented by Components (Consumer Electronics, Access Control, Safety, and Security, Lighting, Energy Management, Smart HVAC / Climate Control, Controllers / Hubs, Smart-Home Healthcare, and Smart Kitchen), Housing Type (Single-Family and Multi-Family), Installation Type (New Construction and Retrofit), Sales Channel (Online and Offline), and Geography.

North America commanded 36.4% of 2024 revenue, buoyed by policy incentives and broad broadband coverage. Up to USD 14,000 per household is now recoverable for energy-efficient retrofits that include connected controls, driving mainstream uptake. Provincial programs in Canada mirror federal support, issuing CAD 10,000 grants and zero-interest loans that prioritize connected heat pumps and monitoring dashboards. Ecosystem alliances, such as Samsung's SmartThings Energy linking electric vehicles to home-grid balancing, showcase regional leadership in whole-ecosystem integration.

Asia-Pacific is the fastest-growing arena at 16.5% CAGR, steered by rapid urbanization and government-sponsored smart-city blueprints. China's domestic brands like Xiaomi deliver affordable whole-home bundles, catalyzing mass-market adoption. India's fiber and 5G rollouts expand addressable households, while Singapore pilots senior-care apartments equipped with ambient sensing that alerts caregivers to abnormalities. Manufacturing concentration in the region compresses bill-of-materials costs, making entry-level solutions attainable for emerging middle classes and widening the smart homes market footprint.

Europe exhibits stable uptake, bolstered by stringent energy directives and privacy-centric regulations. Household penetration surpassed 112 million smart homes by 2022, and trajectories point to 47% adoption by 2027. Schneider Electric's Wiser Home platform applies AI forecasting to shave consumption during tariff peaks, reflecting continental emphasis on grid stability. GDPR prompts local data processing, pushing vendors to design edge-intelligent devices. Incentives under the Fit-for-55 package reward homeowners for grid-interactive equipment, integrating solar surplus into demand response markets. The Middle East and Africa, though nascent, benefit from flagship smart-city builds such as Saudi Arabia's NEOM. Latin America progresses as connectivity infrastructure matures and Brazil's nationwide smart-meter rollout accelerates consumer familiarity with connected living.