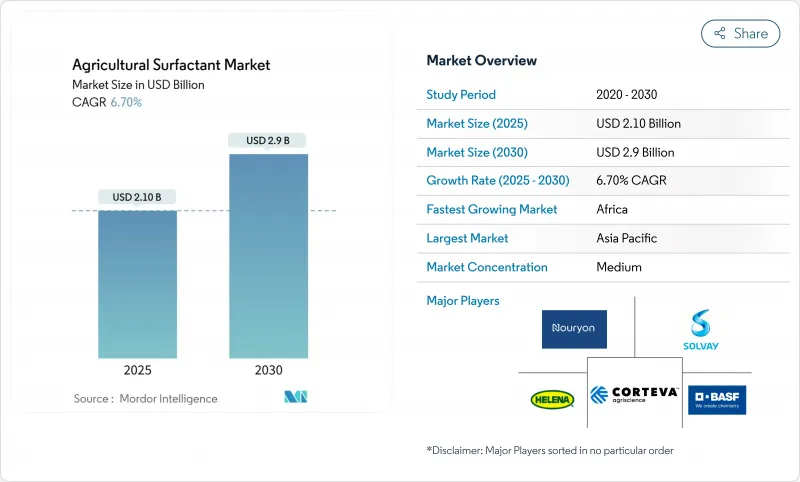

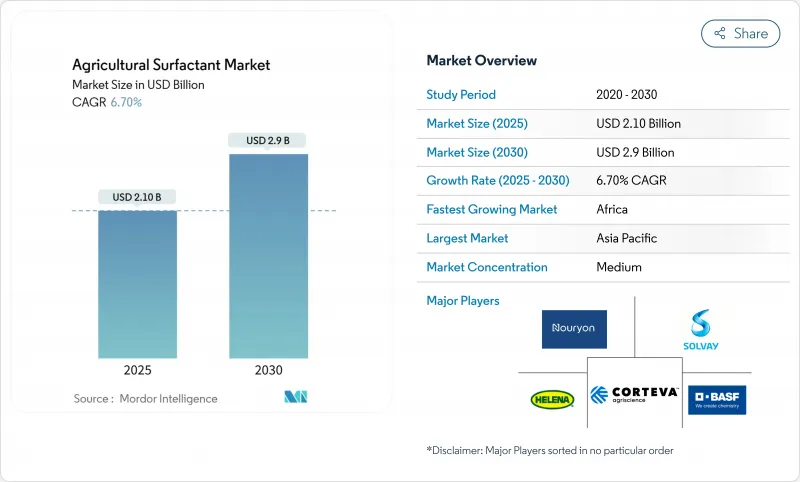

농업용 계면활성제 시장은 2025년 21억 달러, 예측 기간 동안 CAGR 6.7%로 성장하고, 2030년에는 29억 달러에 이를 것으로 예측됩니다.

시장 성장의 원동력이 되고 있는 것은 자율형 드론이나 정전 분무기 등의 정밀 농업 기기의 도입이 증가하고 있는 것으로, 액적 사이즈를 최적화하고, 드리프트를 저감하고, 현장에서의 살포 효율을 향상시키기 위해, 특정의 계면활성제 처방이 필요해지고 있습니다. 업계는 합성 화합물로부터 양성 및 유기 실리콘 제제로의 전환을 진행하고 있으며, 특히 미생물의 효능을 유지하고 흡수를 높이기 위해 계면활성제를 필요로 하는 생물학적 작물 보호 제품의 확대가 그 이유가 되고 있습니다. EU의 Farm-to-Fork 이니셔티브는 2030년까지 합성농약의 사용량을 50% 삭감하는 것을 목표로 하고 있으며, 저용량 적용을 위한 나노계면활성제 기술의 연구개발을 추진하고 있습니다. 시장이 세분화된 구조이기 때문에 전문 기업이 지역 특화형 및 작물 특화형 솔루션을 통해 시장 점유율을 획득할 기회가 있습니다. 그러나 원료가격의 상승과 잔류규제의 강화가 과제가 되고 있으며 지속가능하고 경제적으로 실행 가능한 대체물질의 개발이 중요시되고 있습니다.

농업용 계면활성제는 농약의 전달 효율을 높이는 것으로 농작물의 수율 증가를 서포트해, 식량 안보와 1인당 경지 면적의 감소라는 과제에 대처합니다. 인도에서는 다기능 습윤제가 농약 살포의 효과를 유지하면서 살포량을 15-20% 삭감하는 것이 실지 시험에서 입증되었습니다. 브라질의 바이오 투입 시장은 10억 달러로 평가되고 있으며 미생물제와 메틸화된 종자유를 결합하여 뿌리 영역으로의 침투성을 높이고 있습니다. 비오네마의 소일젯 BSP100의 현장 시험은 최적화된 애주번트 제제에 의해 생물학적 효과가 30% 향상되는 것을 입증하고 있습니다. 날씨와 관련된 병해충의 과제가 점점 확산되고 있기 때문에 소규모 농업 경영도 대규모 농업 경영도 비용 효율적인 작물 보호 솔루션으로 계면활성제를 채택하게 되었습니다.

농업용 드론에 의한 살포는 2024년 중에 캔자스주에서 1,030만 에이커 이상을 커버하고, 프로펠러의 난류 중에서도 액적 사이즈를 일정하게 유지하는 특수한 양성 계면활성제를 이용하고 있습니다. 잎의 뒷면에 액적을 부착할 수 있는 정전 살포 시스템은 물 소비량을 60% 줄였으나 특정 전도도 균형 첨가제가 필요했습니다. 브라질 고이아스 주에서는 가변 레이트 살포로 대두밭의 100%를 커버하고 있으며, 농학자들은 실시간으로 탱크 믹스를 조정할 때 유효 성분의 안정성을 유지하기 위해 pH 안정 제제를 선택하고 있습니다. 에보닉과 같은 기업은 무인 항공기 스프레이 시스템을 위해 특별히 설계된 브레이크 트루 MSO MAX 522와 같은 특수 제품을 개발하고 있습니다. 이러한 용도에 특화된 요건은 농업용 계면활성제 시장의 꾸준한 성장을 가속하고 프리미엄 가격을 지원하고 있습니다.

발효 또는 식물성 기름을 원료로 하는 바이오 생산 경로는 탄소 크레딧을 고려한 후에도 석유화학 대체품보다 15-30% 할인됩니다. 다우가 최근 킬란트 중간체 가격을 파운드당 0.10달러 인상했다는 것은 유도체 공급망에 영향을 미치는 인플레이션 압력을 보여줍니다. 농지의 70%를 영세농가가 소유한 신흥 시장에서는 정부 보조금 없이는 가격에 민감한 농가의 도입이 지연될 수 있습니다. 효소 촉매의 효율 개선, 반응기 용량의 확대, 제품별 이용에 의해 비용 패리티를 달성할 수 있을 가능성은 있지만, 현재의 2년간의 비용면에서의 불리가, 농업용 계면활성제에 있어서의 재생 가능 등급 시장 점유율 확대를 제약하고 있습니다.

비이온성 분자는 중성 전하, 폭넓은 pH 내성, 글리포세이트 및 페녹시계 제초제와의 적합성이 입증되었기 때문에 2024년 매출의 38%를 차지했습니다. 이러한 계면활성제는 친수성-친유성 밸런스(HLB) 값이 12-15이며, 다양한 용제의 조합을 유화하는데 효과적입니다. 비이온 계면활성제가 시장의 우위를 유지하는 한편, 양성 계면활성제는 8.2%의 성장을 이루고 있으며, 음이온 조건 하에서 열화하는 미생물 제제로의 채택이 증가하고 있습니다. 유럽의 사과원에서의 실지시험에서는 양성 계면활성제가 살포온도 범위를 넓히면서 구리의 살포량을 20% 삭감하는 것을 입증하였습니다.

양쪽성 계면활성제 제조업체는 베타인과 이미다졸린 구조를 이용하고, 저발포성과 생분해성을 제공하며, 슈퍼마켓의 컴플라이언스 감사에 있어서의 잔류물 제로의 요건을 충족하고 있습니다. 양성 계면활성제의 농업용 계면활성제 시장은 2030년까지 두배로 될 것으로 예상되며, 드론으로 조작하는 포도원 용도에서의 초기 채택이 예상됩니다. 비이온성 서브카테고리인 유기 실리콘은 표면 장력을 20 mN/m 이하로 저하시킴으로써 성능을 향상시켜 5초 이내에 기공에 침투할 수 있습니다. 프리미엄 가격에도 불구하고, 이러한 특수 실록산은 높은 산포량에서 식물 독성의 가능성이 있기 때문에 선택적으로 사용됩니다.

제초제는 2024년 농업용 계면활성제 시장 수익의 40.2%를 차지했습니다. 세계적인 저항성 관리 전략은 잎의 얼룩에 침투하는 효과적인 습윤제를 필요로 하는 접촉 및 침투 잡초 방제 솔루션에 계속 의존하기 때문입니다. 미국 중서부에서의 농장 시험에서는 사플루페나실과 메틸화 종자유를 조합한 탱크 혼합제로 벨벳 리프를 95% 방제할 수 있었습니다는 것이 입증되어 기술의 진보가 나타났습니다. 시장 성장을 뒷받침하는 것은 새로운 활성 성분의 라벨이 최적의 성능을 보장하기 위해 보조제의 요구 사항을 자주 지정한다는 것입니다.

살균제 분야는 시장 규모가 작은 것, 따뜻한 계절에 의한 병원균의 라이프 사이클의 연장에 의해 CAGR 7.4%로 성장하고 있습니다. 브라질 연구 결과, 유기 실리콘 습윤제는 기존의 비이온성 계면활성제와 비교하여 대두 녹병의 중증도를 30% 감소시키는 것으로 나타났습니다. 양성 캐리어를 이용한 새로운 나노구리 제제는 EU의 규제 심사를 받고 있으며, 금속 잔류물의 감소의 이점을 기대할 수 있습니다. 살충제 부문은 소포성과 침투성을 겸비한 특수 계면활성제를 필요로 하는 나노캡슐화 피레스로이드로 구성되어 있습니다.

아시아태평양은 2024년 시장 수익의 32%를 차지하며, 이는 중국의 광범위한 벼농사와 옥수수 재배, 인도의 확대하는 콩과 면화의 윤작 관행이 견인하고 있습니다. 중국의 조사에서는 정전 드론 살포가 92.1%의 해충 방제 효과를 달성하여 물의 사용량을 90% 삭감한 것이 실증되어 전하 적합 보조제 수요가 높아지고 있습니다. 인도에서는 농약 시장이 10.3% 성장하여 구자라트주나 마디야 프라데시주에서 보급되고 있는 경수 조건 하에서 글리포세이트의 안정성을 유지하는 습윤제의 요구가 높아지고 있습니다. 일본에서는 정부가 지원하는 스마트 농업 구상으로 로봇 농기의 센서 간섭을 막는 초저 발포 실리콘의 사용이 증가하고 있습니다.

아프리카 시장 규모는 작지만 나이지리아, 케냐, 남아프리카가 토양 검사와 가변 시용 매핑을 통해 정밀 농업 능력을 확대함에 따라 CAGR은 7.9%를 나타낼 것으로 예측됩니다. 남아프리카의 감귤류 수출은 EU의 잔류 농약 기준을 준수하기 때문에 내풍성과 팩 하우스 가공시 쉽게 제거를 양립하는 보조제가 필요합니다. 나이지리아의 온실 개발은 생물학적 살충제와 연동하는 pH 완충 살포제가 필요하며, 지역적인 제조 사업 기회를 창출하고 있습니다.

북미에서는 유전자 변형 작물과 엄격한 드리프트 방지 대책을 통해 프리미엄 시장의 지위를 유지하고 있으며, 미국의 농가는 풍동 테스트를 거친 드리프트 저감 제품을 이용하고 있습니다. 캐나다의 캐놀라 농부는 봄의 번다운 살포에 메틸화 씨앗 오일을 사용하고 액체 계면 활성제 시장의 성장을 지원합니다. 유럽 시장은 Farm-to-Fork 정책에 따라 바이오 에톡실레이트 및 비-APE 제제로의 전환을 추진하고 있습니다. 남미에서는 브라질의 대두 산업이 가변 속도 무인 항공기 기술을 채택하고 있으며 다양한 물 조건에 적합한 신속하게 녹는 보조제 포드가 필요합니다. 중동 시장에서는 관개 시스템의 제한된 수자원을 최적화하기 위한 토양 습윤제가 주목받고 있습니다.

The agricultural surfactants market, valued at USD 2.1 billion in 2025, is projected to reach USD 2.9 billion by 2030, growing at a CAGR of 6.7% during the forecast period.

The market growth is driven by the increased adoption of precision farming equipment, including autonomous drones and electrostatic sprayers, which require specific surfactant formulations to optimize droplet size, reduce drift, and improve field application efficiency. The industry is transitioning from synthetic compounds to amphoteric and organosilicone formulations, particularly due to the expansion of biological crop protection products that require surfactants to maintain microbial effectiveness and enhance absorption. The European Union's Farm-to-Fork initiative, which aims to reduce synthetic pesticide usage by 50% by 2030, is driving research and development in nano-surfactant technologies for low-dose applications. The market's fragmented structure provides opportunities for specialized companies to gain market share through region-specific and crop-focused solutions. However, increasing raw material prices and stricter residue regulations present challenges, emphasizing the importance of developing sustainable and economically viable alternatives.

Agricultural surfactants support increased crop yields by enhancing the delivery efficiency of agrochemicals, addressing challenges of food security and declining arable land per capita. In India, field trials demonstrate that multifunctional wetters reduce spray volume by 15-20% while maintaining effectiveness in agrochemical applications. Brazil's bio-inputs market, valued at USD 1 billion, combines microbial agents with methylated seed oils to enhance root-zone penetration. Field trials of Bionema's Soil-Jet BSP100 demonstrate that optimized adjuvant formulations increase biological effectiveness by 30%. The increasing prevalence of weather-related pest and disease challenges has led both small-scale and large agricultural operations to adopt surfactants as a cost-effective crop protection solution.

Agricultural drone operations covered more than 10.3 million acres in Kansas during 2024, utilizing specialized amphoteric surfactants that maintain consistent droplet size in propeller turbulence. Electrostatic spraying systems, which enable droplets to adhere to leaf undersides, reduced water consumption by 60% but require specific conductivity-balanced additives. In Brazil's Goias state, where variable-rate application covers 100% of soybean fields, agronomists select pH-stable formulations to maintain active ingredient stability during real-time tank mix adjustments. Companies such as Evonik have developed specialized products, such as BREAK-THRU MSO MAX 522, designed specifically for drone spray systems. These application-specific requirements drive steady growth and support premium pricing in the agricultural surfactants market.

Bio-based production routes using fermentation or plant-oil feedstocks remain 15-30% more expensive than petrochemical alternatives, even after factoring in carbon credits. Dow's recent USD 0.10 per pound price increase for chelant intermediates demonstrates the inflationary pressures affecting derivative supply chains. In emerging markets, where smallholder farmers operate 70% of agricultural land, price sensitivity may slow adoption without government subsidies. While efficiency improvements in enzymatic catalysis, expanded reactor capacity, and co-product utilization could achieve cost parity, the current two-year cost disadvantage constrains market share growth for renewable grades in agricultural surfactants.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Nonionic molecules accounted for 38% of 2024 revenue due to their neutral charge, wide pH tolerance, and proven compatibility with glyphosate and phenoxy herbicides. These surfactants offer hydrophile-lipophile balance (HLB) values between 12 and 15, making them effective for emulsifying various solvent combinations. While nonionics maintain market dominance, amphoteric surfactants are experiencing 8.2% growth and increasing adoption in microbial formulations that deteriorate under anionic conditions. Field trials in European apple orchards demonstrated that amphoteric surfactants reduce copper application rates by 20% while expanding the temperature range for spraying.

Manufacturers of amphoteric surfactants utilize betaine and imidazoline structures, which offer low foaming properties and biodegradability, meeting zero-residue requirements in supermarket compliance audits. The agricultural surfactants market for amphoterics is anticipated to double by 2030, with initial adoption in drone-operated vineyard applications. Organosilicones, a nonionic subcategory, enhance performance by reducing surface tension to below 20 mN/m, allowing stomatal penetration within five seconds. Despite their premium pricing, these specialized siloxanes see selective implementation due to potential plant toxicity at higher application rates.

Herbicides accounted for 40.2% of the agricultural surfactants market revenue in 2024, as global resistance management strategies continue to rely on contact and systemic weed control solutions that require effective wetters to penetrate leaf cuticles. Field trials in the US Midwest demonstrated that tank mixtures combining saflufenacil with methylated seed oils achieved 95% velvetleaf control, indicating technological advancement. The market growth is supported by new active ingredient labels that frequently specify adjuvant requirements to ensure optimal performance.

The fungicide segment, while smaller in market value, is growing at a 7.4% CAGR due to extended pathogen lifecycles caused by warmer seasons. Research in Brazil showed that organosilicone wetters reduced soybean rust severity by 30% compared to conventional nonionic surfactants. New nano-copper formulations utilizing amphoteric carriers are undergoing EU regulatory review, with potential benefits of reduced metallic residues. The insecticide segment comprises nano-encapsulated pyrethroids requiring specialized surfactants that combine antifoam and penetrant properties.

The Agricultural Surfactants Market Report is Segmented by Product Type (Anionic, and More ), by Application (Insecticide, and More), by Substrate (Synthetic, and Bio-Based), by Crop Application (Crop-Based, and More), by Form (Liquid, and Powder/Granular), by Function (Wetting Agent, and More), and by Geography (North America, Europe, Asia-Pacific, More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 32% of market revenue in 2024, driven by China's extensive rice and maize cultivation and India's expanding soybean and cotton crop rotation practices. Research in China demonstrated that electrostatic drone spraying achieved 92.1% pest control effectiveness while reducing water usage by 90%, increasing the demand for charge-compatible adjuvants. India's agrochemical market growth of 10.3% has increased the need for wetting agents that maintain glyphosate stability in the hard water conditions prevalent in Gujarat and Madhya Pradesh. In Japan, the government-supported Smart Agriculture initiative is increasing the use of ultra-low-foam silicones to prevent sensor interference in robotic farming equipment.

Africa's market, while smaller, projects a 7.9% CAGR as Nigeria, Kenya, and South Africa expand their precision agriculture capabilities through soil testing and variable-rate application mapping. South African citrus exports require adjuvants that provide both wind resistance and easy removal during pack-house processing to comply with EU residue standards. Nigeria's greenhouse developments require pH-buffered spreading agents that work with biological insecticides, creating opportunities for regional manufacturing operations.

North America maintains its premium market position through genetically modified crops and strict drift control measures, with U.S. farmers utilizing wind tunnel-tested drift reduction products. Canadian canola farming relies on methylated seed oils for spring burn-down applications, supporting liquid surfactant market growth. European markets are transitioning toward bio-based ethoxylates and non-APE formulations in alignment with Farm-to-Fork policies. In South America, Brazil's soybean industry employs variable-rate drone technology and requires rapidly dissolving adjuvant pods suitable for diverse water conditions. Middle Eastern markets focus on soil-wetting agents to optimize limited water resources in irrigation systems.