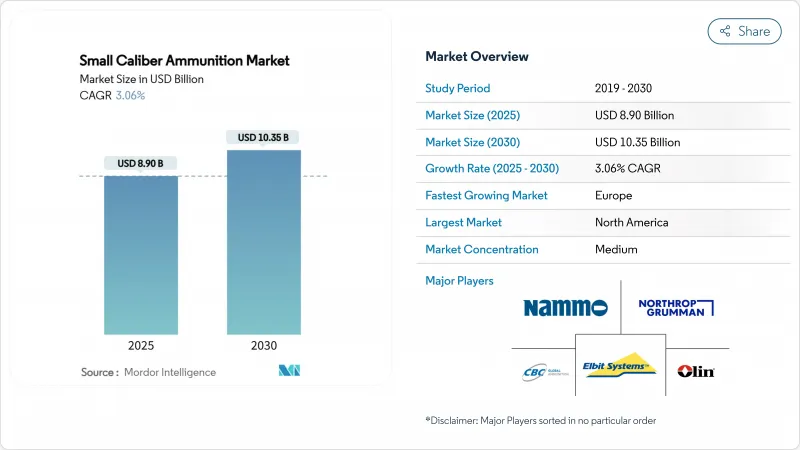

소구경 탄약 시장 규모는 2025년에 89억 달러로 평가되었고, 2030년에 CAGR은 3.06%를 나타낼 것으로 예측되며, 103억 5,000만 달러에 달할 전망입니다.

현재의 성장은 꾸준한 방위 물자 조달, 증가하는 민간 사격 기반, 그리고 미군의 5.56mm 탄약에서 6.8mm 탄약으로의 전환 결정에 기반하고 있습니다. 이러한 전환은 이미 NATO 동맹국들과 글로벌 공급망에 영향을 미치고 있습니다. 단기 수요는 북미와 유럽의 증가한 군수 예산에 의해 뒷받침되는 반면, 인도 및 기타 지역 군대의 자급자족 추구로 아시아태평양 지역의 수요가 가장 빠르게 증가하고 있습니다. 미국 내 지속적인 사냥 및 사격 참여로 민간 소비는 탄력성을 유지하고 있습니다. 그러나 니트로셀룰로오스와 안티몬에 대한 중국의 수출 통제로 원자재 부족에 직면한 생산은 서방 제조사들에게 조달 다각화 압박을 가하고 있습니다. 환경 정책은 또 다른 구조적 촉진요인으로, 생산자들을 무연탄환과 폴리머 탄피로 전환하도록 촉진하고 있습니다.

세계적인 국방비 지출 증가로 전투용 및 훈련용 탄약 수요가 유지되고 있습니다. 미국 국방부는 2025 회계연도에 탄약 구매를 위해 298억 달러(탄약 구매 전용 59억 달러 포함)를 배정했습니다. 많은 유럽 정부들은 우크라이나 분쟁에서 얻은 소비 교훈에 대응하여 생산 능력 확장을 위해 2021년 이후 55억 유로(63억 8천만 달러)의 신규 자금을 추가했습니다. 다년간 계약이 이제 군사 조달을 지배하여 생산자들이 자신 있게 자본 투자를 계획할 수 있게 합니다. 중동에서는 1,000억 달러 규모의 사우디 무기 패키지가 지역적 긴장이 전통적인 NATO 고객들로부터 수요를 어떻게 다각화하는지 보여줍니다.

레크리에이션 및 사냥 활동은 민간 유통 채널을 활성화합니다. 국가 즉각 범죄 배경 조사 시스템(NICS)은 4년 연속 매월 100만 건 이상의 조회를 처리하며 지속적인 총기 취득과 이에 따른 탄약 소비를 보여줍니다. 제조사들은 SHOT 쇼 같은 무역 행사에서 신규 프리미엄 라인을 선보이며, 야생동물 보호구역에서 무연탄환 사용을 장려하는 규제 시범 사업은 규정을 준수하는 생산자들에게 새로운 기회를 제공합니다. 인구 밀집 지역의 실내 사격장 증가 역시 제한된 공간에서 사용하기 위해 설계된 탄약에 대한 꾸준한 수요를 창출합니다.

국가 안보 심사는 구매 기간을 연장하고 국경 간 통합을 제약하고 있습니다. 미국 당국은 공급망 위험을 위해 모든 주요 거래를 면밀히 조사하며, 유럽 허가 기관들도 유사한 엄격함을 적용합니다. 이러한 통제는 국내 생산자를 보호하지만 수출업체의 해외 확장을 제한하여 대규모 내수 시장을 보유한 업체들에게 경쟁 우위를 제공합니다.

5.56mm 소구경 탄약 시장 규모는 2024년 글로벌 매출의 26.76%를 차지했으며, 광범위한 재고와 기존 무기 시스템으로 인해 여전히 상당한 비중을 유지하고 있습니다. 그러나 6.8mm 탄약은 미국 및 동맹국 군대의 신형 소총 도입으로 2030년까지 연평균 7.89% 성장할 전망입니다. 이 성장세는 구형 구경 탄약의 점진적 감축을 상쇄합니다. 예측 기간 동안 다수 NATO 회원국이 5.56mm와 6.8mm 탄약을 이중 조달함으로써 갑작스러운 물류 전환에 대비할 것입니다.

SIG Sauer의 하이브리드 탄피 설계는 6.8mm가 미래 전투력 핵심인 이유를 보여줍니다. 과도한 무게나 발열 없이 높은 약실 압력을 구현하기 때문입니다. 북유럽 시험 프로그램과 영국군의 구경 평가는 차세대 탄도학에 대한 광범위한 관심을 입증합니다. 따라서 해당 부문은 기존 유지보수용과 미래 대비용으로 분화되어 유연한 생산자에 대한 풍부한 수요를 창출합니다.

소총 탄약은 2024년 글로벌 판매량의 32.77%를 차지했으며 보병 작전과 정밀 사격 스포츠에 여전히 필수적입니다. 그럼에도 소구경 탄약 시장은 기관단총용 소구경 탄약 주문 증가를 목격하고 있으며, 2030년까지 연평균 5.12% 성장할 전망입니다. 도시 대테러 작전과 경찰 부대는 이 플랫폼이 제공하는 짧은 총열과 기동성을 높이 평가합니다.

인도의 아스미 기관단총 도입은 치명적 제압력을 유지하면서도 소총을 보완하는 경량 무기 채택이라는 군대 간 트렌드를 시사합니다. 탄약 기업들은 짧은 총열에 맞춰 연소 속도를 최적화한 탄약을 개발하여 안정적인 작동과 종단 에너지를 보장함으로써 이에 대응하고 있습니다.

북미는 2024년 29.89%의 매출 점유율로 선두를 달렸으며, 이는 미국의 8,498억 달러 국방 예산과 활발한 민간 사격 문화에 힘입은 결과입니다. 레이크 시티 육군 탄약 공장(LCAP)만으로도 미군의 소구경 탄약 수요의 약 85%를 공급하며, 초과 생산분은 시장에 판매됩니다. 무연 사냥을 장려하는 연방 및 주 정부 프로그램으로 제품 다양성이 높아져 지역 생산자들은 무독성 포뮬러 개발에 연구개발(R&D) 자금을 할당해야 합니다.

아시아태평양 지역은 2030년까지 연평균 복합 성장률(CAGR) 4.90%로 가장 빠른 성장세를 보일 전망입니다. 인도의 ‘아트마니르바르 바라트(자립 인도)’ 정책은 국산 탄약 라인에 상당한 투자를 유도했으며, 기존 공급업체의 조달 지연으로 뉴델리는 공급업체 기반 확대를 추진 중입니다. 남중국해와 동중국해의 지역적 긴장은 국가들의 탄약 비축량 확대를 더욱 촉진합니다. 예를 들어 한국은 세계 최대 규모의 105mm 탄약 비축량을 유지하며 동맹국에 탄약을 제공할 의사를 표명했습니다.

유럽은 우크라이나 분쟁으로 드러난 공급 부족을 해결하기 위해 산업 기반을 재정비 중입니다. 라인메탈은 연간 포탄 생산량을 10배 증산했으며, 9개국 SAAT 이니셔티브는 상호운용성 확보를 위한 탄약 표준 조화를 모색하고 있습니다. 동시에 유럽화학물질청의 납 제한 로드맵으로 인해 유럽 제조사들은 구리 기반 탄환 생산을 위한 라인 개조가 불가피합니다.

The small caliber ammunition market size was valued at USD 8.90 billion in 2025 and is forecasted to reach USD 10.35 billion by 2030 at a 3.06% CAGR.

Current growth rests on steady defense procurement, a rising civilian shooting base, and the US Army's decision to move from 5.56 mm to 6.8 mm ammunition. This shift is already influencing NATO partners and global supply chains. Near-term demand is underpinned by higher munition budgets in North America and Europe, while Asia-Pacific demand rises fastest as India and other regional militaries seek self-sufficiency. Civilian consumption remains resilient thanks to sustained hunting and target-shooting participation in the United States. Production, however, faces raw-material shortages after Chinese export controls on nitrocellulose and antimony, creating pressure on Western manufacturers to diversify sourcing. Environmental policy is another structural driver, pushing producers toward lead-free bullets and polymer cases.

A global rise in defense spending is sustaining demand for combat and training ammunition. The US Department of Defense has earmarked USD 29.8 billion for munitions in fiscal-year 2025, including USD 5.9 billion allocated specifically to ammunition purchases. Many European governments have added EUR 5.5 billion (USD 6.38 billion) in new funding since 2021 to expand output capacity, responding to consumption lessons from the Ukraine conflict. Multi-year deals now dominate military procurement, allowing producers to plan capital investments confidently. In the Middle East, a USD 100 billion Saudi arms package underscores how regional tensions diversify demand away from traditional NATO customers.

Recreational and hunting activity keeps the civilian channel buoyant. The National Instant Criminal Background Check System has processed more than 1 million checks every month for over four straight years, signaling consistent firearm acquisition and underlying ammunition consumption. Manufacturers showcase new premium lines at trade events such as the SHOT Show, while regulatory pilots incentivizing lead-free rounds at wildlife refuges offer compliant producers fresh opportunities. Growth in indoor ranges in densely populated areas also creates steady demand for ammunition engineered for confined-space shooting.

National-security reviews are lengthening acquisition timelines and constraining cross-border consolidation. US authorities scrutinize every major transaction for supply-chain risk, and European licensing bodies apply similar rigor. These controls shield domestic producers yet limit overseas expansion for exporters, tilting competition toward players with large home markets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The small caliber ammunition market size for 5.56 mm stood at 26.76% of global revenue in 2024 and remains significant due to widespread inventory and legacy weapon systems. However, 6.8 mm cartridges will expand at 7.89% CAGR through 2030 as US and allied militaries field new rifles. This growth layer compensates for the tapering procurement of older calibers. Over the forecast window, many NATO members will dual-source 5.56 mm and 6.8 mm ammunition, cushioning any abrupt logistical shift.

SIG Sauer's hybrid-case design illustrates why 6.8 mm is central to future lethality, offering higher chamber pressures without excessive weight or heat. Nordic testing programs and the British Army's caliber evaluations exemplify broader interest in next-generation ballistics. The segment, therefore, splits into legacy-maintenance and future-proof lines, creating rich demand for flexible producers.

Rifle ammunition formed 32.77% of 2024 global sales and remains indispensable for infantry operations and precision sport shooting. Even so, the small caliber ammunition market notices rising orders for compact rounds used in sub-machine guns, projected at a 5.12% CAGR to 2030. Urban counter-terror missions and police units value the shorter barrels and agility these platforms offer.

India's adoption of the Asmi machine-pistol signals the trend among militaries to complement rifles with lighter weapons that retain lethal stopping power. Ammunition companies respond by engineering cartridges with optimized burn rates to match shorter barrels, ensuring reliable cycling and terminal energy.

The Small Caliber Ammunition Market Report is Segmented by Caliber (5. 56 Mm, 6. 8 Mm, 7. 62 Mm, 9 Mm, 12. 7 Mm, and Other Calibers), Weapon Platform (Handguns, Rifles, Light Machine Guns, Sub-Machine Guns, and Shotguns), Bullet Type (Brass, Copper, and More), Lethality (Lethal and Less Lethal), End-Use (Military, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led with a 29.89% revenue share in 2024, powered by the United States' USD 849.8 billion defense budget and a vibrant civilian shooting culture. Lake City Army Ammunition Plant alone supplies about 85% of the US military's small-caliber requirements while selling commercial overruns to the market. Federal and state programs promoting lead-free hunting keep product diversity high, forcing local producers to allocate R&D funds toward non-toxic formulas.

Asia-Pacific shows the fastest trajectory at a 4.90% CAGR to 2030. India's Atmanirbhar Bharat policy has directed substantial investment toward indigenous ammunition lines, and procurement delays from traditional suppliers push New Delhi to widen its vendor base. Regional flashpoints in the South and East China Seas further motivate nations to expand stockpiles. South Korea, for instance, maintains one of the world's largest 105 mm inventories and has signaled its willingness to provide ammunition to partners.

Europe is retooling its industrial base after the Ukraine conflict exposed supply shortfalls. Rheinmetall has raised annual artillery shell output by an order of magnitude, and the nine-country SAAT initiative seeks a harmonized ammunition standard to safeguard interoperability. At the same time, the European Chemicals Agency's lead-restriction roadmap compels European manufacturers to retrofit lines for copper-based bullets.