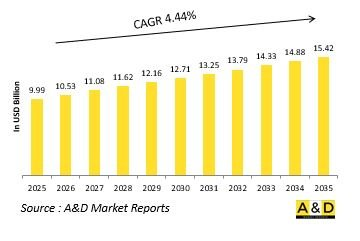

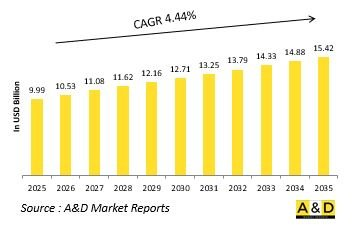

전 세계 소구경 탄약 시장 규모는 2025년 99억 9,000만 달러에서 예측 기간 동안 4.44%의 CAGR로 2035년에는 154억 2,000만 달러로 성장할 것으로 예상됩니다.

국방용 소구경 탄약 시장은 군사 화력의 기반을 형성하고 있으며, 소총, 권총, 기관총, 저격 시스템 등 다양한 보병용 무기를 뒷받침하고 있습니다. 소구경 탄약은 근접전, 전술 작전, 훈련 훈련에 필수적이며, 개별 병사 및 특수부대원에게 주요한 도구가 될 수 있습니다. 신뢰성, 정확성, 범용성으로 인해 평시전, 대반란 작전, 평화유지 활동에 필수적인 존재입니다. 전 세계 국방 전략이 비대칭 위협과 하이브리드형 분쟁 대응으로 진화하는 가운데, 성능이 향상된 소구경 탄약에 대한 수요는 지속적으로 증가하고 있습니다. 군대는 도시부터 험준한 전장까지 다양한 환경에서 정확도 향상, 살상력 증대, 성능 최적화를 요구하고 있습니다. 또한, 소구경 탄약의 역할은 전투에 국한되지 않고 법집행기관, 국내 치안, 국경 경비 임무에도 확대되고 있습니다. 비용 효율성과 적응성은 지속적인 작전 대응력과 신속한 전개 능력을 뒷받침하는 중요한 요소이기도 합니다. 병력 현대화와 전장 기동성을 중시하는 군대에 있어 소구경 탄약은 전술적 우위, 전력 효율성, 그리고 점점 더 복잡해지는 세계 방위 시나리오에서 임무 성공을 달성하는 데 있어 핵심적인 역할을 하고 있습니다.

기술의 발전은 국방용 소구경 탄약 시장을 크게 변화시켜 성능, 안전성, 운용 효율성을 높이고 있습니다. 재료과학의 혁신으로 더 가볍고 강도가 높으며 관통력과 종말 탄도 성능이 우수한 탄체가 개발되고 있습니다. 추진제 및 뇌관 구성의 개선은 사거리, 일관성, 신뢰성을 향상시키고 다양한 환경 조건에서 우수한 성능을 발휘합니다. 정밀 엔지니어링과 제조 공차의 엄격화는 정확도 향상과 탄도 편차 감소로 이어져 정밀 사격이 결정적인 현대전에서 매우 중요합니다. 또한, 프로그래밍 가능한 탄약, 전자신관 등 스마트 탄약 기술이 등장하여 특정 표적에 대한 효과를 최적화할 수 있게 되었습니다. 환경적 측면에 대한 고려도 설계에 영향을 미치고 있으며, 훈련 및 전투에서의 환경 부하를 줄이기 위해 무연 및 저독성 탄약의 도입이 진행되고 있습니다. 또한, 부가 제조 기술은 생산 효율을 높이고, 신속한 시제품 제작 및 커스터마이징을 가능하게 합니다. 첨단 화기 관제 시스템 및 탄도 계산기와 통합되어 전장에서의 효과도 더욱 최적화되어 있습니다. 이러한 기술 동향은 소구경 탄약을 보다 고성능, 다재다능하고 지속가능한 현대전 도구로 진화시키고 있으며, 병사의 치사율 향상, 작전 유연성, 다양한 임무에 대한 즉각적인 대응이라는 목표에 부합하고 있습니다.

국방용 소구경 탄약 시장의 성장은 변화하는 전투 요구, 현대화 이니셔티브, 안보 환경의 변화에 의해 주도되고 있습니다. 비대칭전, 대테러 작전, 도시전투의 증가는 복잡한 환경에서도 성능을 발휘할 수 있는 정밀한 설계와 신뢰할 수 있는 탄약에 대한 수요를 증가시키고 있습니다. 병사 현대화 프로그램은 병사의 치사율과 기동성을 향상시키는 것을 목표로 하고 있으며, 차세대 탄약 조달을 촉진하고 있습니다. 특수작전부대 및 신속대응부대의 확충으로 근접전투부터 장거리 정밀사격까지 다양한 임무에 대응할 수 있는 고성능 탄약이 요구되고 있습니다. 또한, 정기적인 훈련과 즉각적인 대응태세 유지를 위한 연습도 수요를 뒷받침하고 있으며, 군은 지속적인 기술 개발 및 작전 준비를 중시하고 있습니다. 국경경비, 국토방위, 평화유지 임무도 시장 확대에 기여하고 있으며, 다양한 탄약 비축이 요구되고 있습니다. 기술 발전과 더불어 최신 무기 시스템과의 상호 운용성의 필요성으로 인해 국방 당국은 탄약 재고를 업그레이드하려는 움직임을 강화하고 있습니다. 또한, 지정학적 긴장, 영토 분쟁, 국방 예산의 증가는 조달 활동을 촉진하고 시장의 안정적인 확장을 보장하고 있습니다. 이러한 요인들은 총체적으로 소구경 탄약이 방어 능력과 전술적 효율성을 강화하는 중요한 기반임을 보여줍니다.

세계의 소구경 탄약 시장을 조사했으며, 시장 배경, 시장 영향요인 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별 상세 분석 등의 정보를 정리하여 전해드립니다.

지역별

캘리퍼

최종사용자별

북미

촉진요인, 제약, 과제

PEST

주요 기업

공급업체 계층 상황

기업 벤치마크

유럽

중동

아시아태평양

남미

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Small Caliber Ammunition market is estimated at USD 9.99 billion in 2025, projected to grow to USD 15.42 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 4.44% over the forecast period 2025-2035.

Introduction to Small Caliber Ammunition Market

The defense small caliber ammunition market forms a fundamental component of military firepower, supporting a wide range of infantry weapons, including rifles, pistols, machine guns, and sniper systems. Small caliber ammunition is essential for close-quarters combat, tactical operations, and training exercises, serving as the primary tool for individual soldiers and special forces. Its reliability, precision, and versatility make it indispensable for conventional warfare, counterinsurgency missions, and peacekeeping operations. As global defense strategies evolve to address asymmetric threats and hybrid conflicts, the demand for improved small caliber ammunition continues to rise. Military forces seek enhanced accuracy, increased lethality, and optimized performance across varied environments - from urban terrain to rugged battlefields. Additionally, the role of small caliber ammunition extends beyond active combat to include law enforcement, homeland security, and border protection missions. Its cost-effectiveness and adaptability also make it a key element in sustained operational readiness and rapid deployment capabilities. With armed forces emphasizing soldier modernization and battlefield agility, small caliber ammunition remains central to achieving tactical superiority, force effectiveness, and mission success in increasingly dynamic and complex defense scenarios across the globe.

Technological advancements are significantly reshaping the defense small caliber ammunition market, enhancing its performance, safety, and operational efficiency. Innovations in materials science have led to the development of lighter, stronger projectiles with improved penetration and terminal ballistics. Enhanced propellants and primer compositions are boosting range, consistency, and reliability, ensuring superior performance in varied environmental conditions. Precision engineering and tighter manufacturing tolerances contribute to greater accuracy and reduced deviation, vital for modern combat where precision engagements are often decisive. Smart ammunition technologies, including programmable rounds and electronic fuzes, are emerging to deliver tailored effects against specific targets. Environmental considerations are also influencing design, with lead-free and reduced-toxicity ammunition gaining traction to minimize ecological impact during training and combat. Additive manufacturing techniques are streamlining production, enabling rapid prototyping and customization. Integration with advanced fire control systems and ballistic calculators is further optimizing effectiveness on the battlefield. Together, these technological trends are transforming small caliber ammunition into more effective, versatile, and sustainable tools of modern warfare, aligning with the broader goals of enhanced soldier lethality, operational flexibility, and readiness for diverse mission profiles.

The growth of the defense small caliber ammunition market is driven by evolving combat needs, modernization initiatives, and changing security dynamics. The rise of asymmetric warfare, counterterrorism operations, and urban combat scenarios has heightened the demand for precision-engineered, reliable ammunition capable of performing in complex environments. Soldier modernization programs aimed at increasing individual lethality and mobility are pushing armed forces to procure next-generation ammunition with enhanced performance characteristics. Expanding special operations units and rapid deployment forces require high-performance rounds optimized for diverse missions, from close-quarters engagements to long-range precision strikes. Additionally, regular training and readiness exercises fuel sustained demand, as military forces prioritize continuous skill development and operational preparedness. Border security, homeland defense, and peacekeeping missions also contribute to market growth, requiring significant stockpiles and varied ammunition types. Technological advancements, coupled with the need for interoperability with modern weapon systems, are prompting defense agencies to upgrade their ammunition inventories. Geopolitical tensions, territorial disputes, and rising defense budgets further amplify procurement activities, ensuring steady market momentum. Collectively, these factors underscore the strategic importance of small caliber ammunition as a critical enabler of defense capability and tactical effectiveness.

Regional trends in the small caliber ammunition market reflect a balance between modernization priorities, strategic requirements, and evolving security challenges. North America leads in innovation and procurement, driven by advanced infantry programs, frequent training operations, and continuous upgrades to ammunition stockpiles. Europe is witnessing increased demand as nations modernize their forces, enhance rapid reaction capabilities, and strengthen collective defense initiatives. The Asia-Pacific region is experiencing robust growth, fueled by expanding military forces, rising territorial tensions, and investments in indigenous ammunition production capabilities. Middle Eastern countries are focusing on improving counterterrorism and internal security capacities, resulting in significant procurement of specialized and high-performance ammunition. Latin America and Africa, while smaller markets, are increasingly prioritizing ammunition acquisition for border protection, peacekeeping operations, and counterinsurgency missions. Across regions, collaboration between domestic manufacturers and international defense contractors is driving technology transfer and enhancing local production capabilities. Additionally, growing emphasis on self-reliance and strategic autonomy is encouraging indigenous development initiatives. These regional dynamics underscore the universal importance of small caliber ammunition as a foundational element of defense preparedness, supporting diverse operational requirements and strengthening the tactical effectiveness of armed forces worldwide.

The Swedish Defence Materiel Administration (FMV) has awarded a contract valued at Skr1.8 billion ($185.8 million) to Norwegian-Finnish defense company Nammo for the supply of small-calibre ammunition. In addition, FMV placed an order with Norma worth Skr1.4 billion for fine-calibre ammunition. Both framework agreements with Nammo and Norma are set for a ten-year duration, including an initial three-year procurement period. Deliveries under these contracts are planned between 2026 and 2028. The 10-year agreement with Nammo is part of a broader framework recently established with FMV and represents Sweden's largest procurement of small-calibre ammunition from Nammo to date.

By Region

By Caliber

By End User

The 10-year Small Caliber Ammunition Market analysis would give a detailed overview of Small Caliber Ammunition Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Small Caliber Ammunition Market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional Small Caliber Ammunition Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.