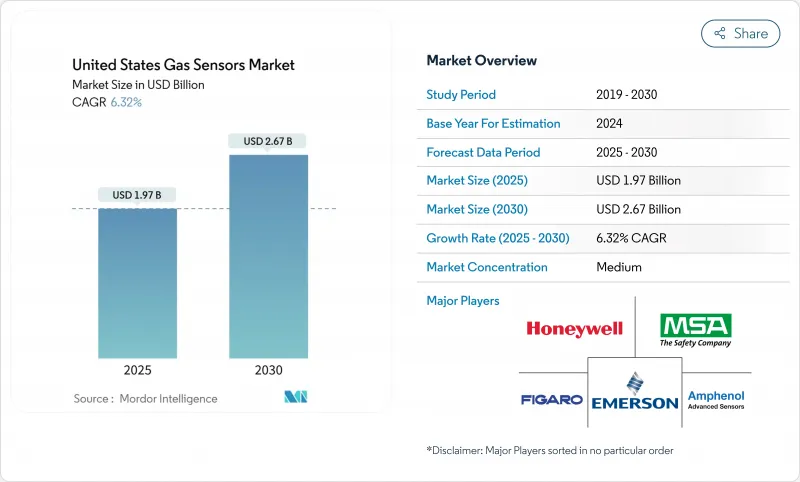

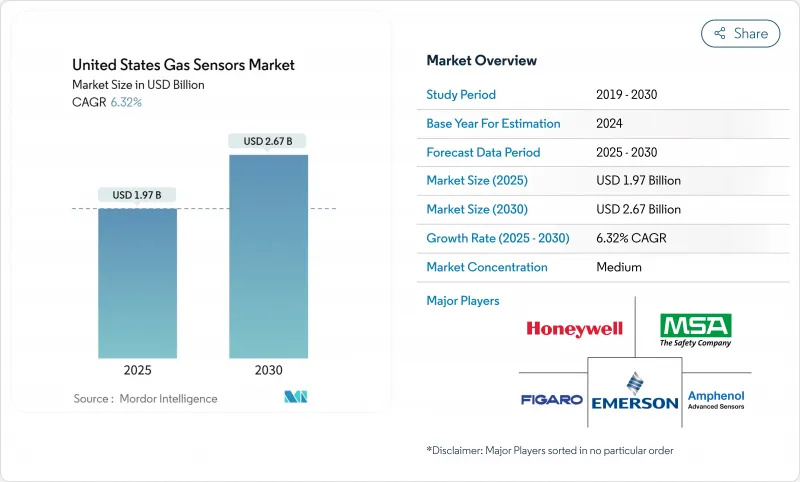

미국의 가스 센서 시장 규모는 2025년에 19억 7,000만 달러로 추정되고, 2030년에는 26억 7,000만 달러에 이르고, CAGR 6.32%를 나타낼 것으로 예측됩니다.

수요는 공장 및 정유소에 연속적인 누수 감지 시스템을 설치하도록 촉구하는 연방 안전 규정에 의해 지원되며, ASHRAE 환기 기준의 엄격화로 상업용 건물에서의 채택이 확대되고 있습니다. 저전력 네트워크가 설치 비용을 절감하고 가동 시간을 향상시키는 원격 진단을 가능하게 하기 위해 무선 및 IoT 지원 장치가 빠르게 지원을 받고 있습니다. 에지 AI 분석이 센서 노드에서 직접 실행되므로 원시 데이터를 실시간 경고로 변경하여 비용이 많이 드는 사고를 예방할 수 있습니다. 수소 인프라의 전개에 의해 초고감도 검출기의 주문이 급증하고, MEMS 기반의 설계에 의해 사이즈와 전력 요건이 저하되어, 웨어러블 기기나 휴대형 안전 기기에 새로운 용도가 확산되고 있습니다. 경쟁의 심각성은 중간 정도입니다. 다각적인 안전 리더는 여전히 중요한 프로세스 틈새 시장을 지배하고 있지만, 반도체 전문가들은 컴팩트하고 소프트웨어 중심 플랫폼에서 점유율을 확대하고 있습니다.

메탄 가스 및 독성 가스 배출에 관한 규제의 갱신으로 인해 공장은 낮은 임계값으로 누출을 확인해야 하며, 하루에 2만 5,000달러에 달하는 처벌이 부과될 수 있습니다. 따라서 시설은 10억분의 1 농도를 검출하는 멀티 가스 어레이에 투자하고 컴플라이언스를 넘어서는 공정 제어의 가치를 부가하고 있습니다. 엔지니어링 팀은 현재 위험 수준이 발생할 때 셧다운을 자동화하는 안전 계장 시스템과 통합되는 검출기를 지정합니다. 텍사스, 루이지애나, 펜실베니아의 석유, 가스 및 화학 클러스터는 컴플라이언스 지출이 가장 많으며 공급업체에게 확실한 수익원이되었습니다. 선도적인 구매자는 규제 당국에 대한보고를 단순화하는 교정 프로그램과 클라우드 기반 감사 추적에 지원되는 제품 라인을 선호합니다.

2024년 ASHRAE 62.1의 업데이트로 CO2 미터의 정확도 목표가 엄격해지면서 빌딩 사업자는 오래된 하드웨어를 고급 광학 또는 전기화학 장치로 교체하게 되었습니다. 사무실 타워, 병원, 학교는 현재 가스 측정을 공기 처리 장치에 연결하는 가동률 기반 환기 제어를 통합하고 에너지 절약과 건강 기준의 균형을 맞추고 있습니다. 포트폴리오 소유자는 실내 공기 데이터를 테넌트 유지를 지원하는 어메니티로 간주하고 가스 센서를 후방 설비에서 웰니스 브랜딩의 눈에 보이는 부분으로 승화시키고 있습니다. 가장 도입이 진행되고 있는 것은 북동부와 캘리포니아주로, 주로부터의 장려금과 지속가능성의 의무화가 조합되고 있습니다. 시스템 통합자는 센서를 분석 대시보드에 번들하여 고장 경고 및 환기 스코어 카드를 단일 보기로 제공합니다.

분기별 교정 프로토콜은 특수 테스트 가스, 훈련된 직원 및 장비의 평생 소유 비용을 40%로 끌어올리는 다운타임이 필요합니다. 소규모 플랜트의 경우 서비스 간격이 지연되는 경우가 많아 안전에 대한 투자를 훼손할 수 있는 오보 및 미검출 누출의 위험이 있습니다. 제조업체는 자체 교정 셀과 원격 진단을 통해 대응하지만 자본 가격은 상승하고 구매자는 선행적인 절약과 경상적인 노동을 비교 검토해야합니다. 농촌 지역의 기술 부족은 부담을 증가시키고 일부 사업자는 센서, 서비스 및 컴플라이언스 문서 작성을 번들로 유지 보수 계약을 아웃소싱해야 합니다.

2024년 미국의 가스 센서 시장에서는 무정전전원과 페일세이프 통신을 필요로 하는 공정산업에 지지되어 유선 카테고리가 54%의 포지션을 유지했습니다. 이러한 설비는 일반적으로 분산 제어 시스템에 직접 연결되어 위험 지역에서의 컴플라이언스를 보장합니다. 그러나 무선 노드는 배터리 수명을 5년 이상으로 늘리는 저전력 광역 기술에 힘입어 CAGR 11.5%를 나타낼 전망입니다. 시설 관리자는 턴어라운드 시나 케이블 배선이 비용이 적게 드는 레거시 빌딩에 일시적인 배치를 가능하게 하는 메쉬 네트워크를 도입하고 있습니다. 무선 유연성은 세밀한 센서 배치를 지원하고 더 나은 환기 인사이트를 요구하는 다층 학교와 병원에서의 커버리지를 향상시킵니다. 통합자는 무선 가스 데이터를 가동률 및 에너지 지표와 결합하여 안전뿐만 아니라 운영 효율성에도 가치를 제공합니다.

무선 옵션의 상승은 서비스 모델의 형태도 바꾸고 있습니다. 공급업체는 현재 하드웨어, 네트워크 연결 및 분석 대시보드를 하나의 계약으로 결합한 구독 패키지를 제공합니다. 이 변화는 자본 예산을 줄이고 새로운 센서가 등장할 때 항상 업그레이드할 수 있습니다. 무선 설비와 관련된 미국의 가스 센서 시장 규모가 증가함에 따라 조달 팀은 평생 가치와 소프트웨어 기능에 중점을 둔 총 비용 평가로 축 발을 옮깁니다. 위험도가 높은 지역에서는 유선 시스템이 표준인 것으로 변함이 없지만, 클래스 I 디비전 1의 존에서는 상설의 유선 검출기와, 위험도가 낮은 스페이스에서는 무선 기기를 조합해, 비용을 최적화하는 하이브리드 아키텍쳐가 출현하고 있습니다.

전기화학 전지는 CO, H2S, NO2에 대한 정확성이 입증되었기 때문에 2024년 미국의 가스 센서 시장 점유율의 31.5%를 차지했습니다. 촉매 비드 설계는 클래스 i 환경에서 가연성 가스에 대한 유력한 옵션으로 지속되었으며, NDIR 광학계는 HVAC 제어에서 CO2용으로 인기를 끌었습니다. PID는 위험물 대응 및 산업 위생 캠페인에서 VOC를 모니터링하는 틈새 역할을 수행했습니다.

MEMS MOS 기기는 반도체 생산이 유닛당 비용을 절감하고 코인 사이즈 패키지로 여러 가스의 식별을 가능하게 하기 때문에 2025년부터 2030년에 걸쳐 13.2%의 연평균 복합 성장률(CAGR)로 성장을 이룰 전망입니다. 머신러닝 알고리즘은 교차 감도를 보정하여 단일 다이로 메탄, 수소 및 휘발성 유기물을 컨텍스트에 맞는 정확도로 식별할 수 있습니다. 혼자 작업하는 사람의 안전을 보장하기 위한 웨어러블 기기 및 소비자용 전자 기기는 이러한 칩을 통합함으로써 위험한 환경을 실시간으로 사용자에게 경고할 수 있습니다. 또한 MEMS로의 전환은 전력 소비를 줄이고, 무선 노드의 배터리 수명을 연장하고, 빈번한 배터리 교체를 억제하는 지속가능성 목표에 부합합니다.

미국의 가스 센서 시장은 유형별(유선, 무선), 가스 유형별(산소, 일산화탄소 등), 기술별(전기화학, 광이온화 검출기(PID) 등), 용도별(의료 및 헬스케어, 빌딩 오토메이션 등)으로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

The United States gas sensors market size is estimated at USD 1.97 billion in 2025 and is projected to reach USD 2.67 billion by 2030, advancing at a 6.32% CAGR.

Demand is sustained by federal safety rules that push factories and refineries to install continuous leak-detection systems, while stricter ASHRAE ventilation standards extend adoption across commercial buildings. Wireless and IoT-ready devices are rapidly gaining favour as low-power networks cut installation costs and enable remote diagnostics that improve uptime. Edge-AI analytics now run directly on the sensor node, turning raw data into real-time alerts that help prevent costly incidents. Hydrogen infrastructure rollouts are creating a surge of orders for ultra-sensitive detectors, and MEMS-based designs are lowering size and power requirements, opening new uses in wearables and portable safety gear. Competitive intensity is moderate: diversified safety leaders still dominate critical-process niches, but semiconductor specialists are carving out share with compact, software-driven platforms.

Regulatory updates on methane and toxic gas emissions require plants to verify leaks at lower thresholds and carry penalties that can reach USD 25,000 per day. Facilities therefore invest in multi-gas arrays that detect parts-per-billion concentrations, adding process-control value beyond compliance. Engineering teams are now specifying detectors that integrate with safety-instrumented systems to automate shutdowns when hazardous levels arise, a capability that shortens response time and limits liability exposure. Compliance spending is heaviest in oil, gas, and chemical clusters across Texas, Louisiana, and Pennsylvania, securing a reliable revenue stream for suppliers. Large buyers prefer product lines supported by calibration programs and cloud-based audit trails that simplify regulatory reporting.

The 2024 update to ASHRAE 62.1 tightened accuracy targets for CO2 meters, prompting building operators to swap older hardware for advanced optical or electrochemical devices. Office towers, hospitals, and schools now integrate occupancy-based ventilation controls that link gas readings to air-handling units, balancing energy savings with health criteria. Portfolio owners see indoor-air data as an amenity that supports tenant retention, elevating gas sensors from back-of-house equipment to a visible part of wellness branding. Strongest adoption is in the Northeast and California, where state incentives pair with sustainability mandates. System integrators bundle sensors with analytics dashboards to provide fault alerts and ventilation scorecards in a single view.

Quarterly calibration protocols require specialty test gas, trained staff, and downtime that can push lifetime ownership costs to 40% of equipment spend. Smaller plants often delay service intervals, risking false alarms or undetected leaks that undermine safety investments. Manufacturers respond with self-calibrating cells and remote diagnostics, yet capital prices rise, forcing buyers to weigh upfront savings against recurring labour. Skill shortages in rural regions worsen the burden, prompting some operators to outsource maintenance contracts that bundle sensors, service, and compliance documentation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The wired category maintained a 54% position in the United States gas sensors market during 2024, anchored by process industries that require uninterrupted power and fail-safe communication. These installations typically connect directly to distributed control systems, ensuring compliance in hazardous zones. However, wireless nodes are growing at an 11.5% CAGR, propelled by low-power wide-area technologies that stretch battery life to more than five years. Facility managers deploy mesh networks that allow temporary placement during turnarounds or in legacy buildings where cabling is cost prohibitive. Wireless flexibility supports granular sensor placement, elevating coverage in multi-story schools and hospitals that seek better ventilation insight. Integrators combine wireless gas data with occupancy and energy metrics, bundling value propositions that extend beyond safety into operational efficiency.

The rise of wireless options also reshapes service models. Vendors now offer subscription packages that wrap hardware, network connectivity, and analytics dashboards in single agreements. This shift reduces capital budgets and enables evergreen upgrades when new sensors emerge. As the United States gas sensors market size relevant to wireless installations climbs, procurement teams pivot toward total-cost evaluations that emphasize lifetime value and software functionality. While wired systems will remain standard in high-risk areas, hybrid architectures emerge, pairing permanent wired detectors in Class I Division 1 zones with wireless devices in less hazardous spaces to optimize spend.

Electrochemical cells held 31.5% of the United States gas sensors market share in 2024 due to their proven accuracy for CO, H2S, and NO2. Catalytic-bead designs persisted as the go-to choice for combustible gases in Class I environments, while NDIR optics gained popularity for CO2 in HVAC controls. PIDs served niche roles monitoring VOCs during hazmat response and industrial hygiene campaigns.

MEMS MOS devices are on track to post 13.2% CAGR growth between 2025 and 2030 as semiconductor production reduces per-unit costs and enables multi-gas identification in coin-sized packages. Machine-learning algorithms compensate for cross-sensitivity, letting a single die discriminate among methane, hydrogen, and volatile organics with contextual accuracy. Wearables for lone-worker safety and consumer electronics integrate these chips to alert users to hazardous environments in real time. The migration to MEMS also lowers power draw, extending battery life in wireless nodes and aligning with sustainability objectives that discourage frequent battery swaps.

The US Gas Sensors Market Segmented by Type (Wired, Wireless), Gas Type (Oxygen, Carbon Monoxide and More), Technology (Electrochemical, Photo-Ionisation Detector (PID) and More), Application (Medical and Healthcare, Building Automation and More). The Market Forecasts are Provided in Terms of Value (USD).