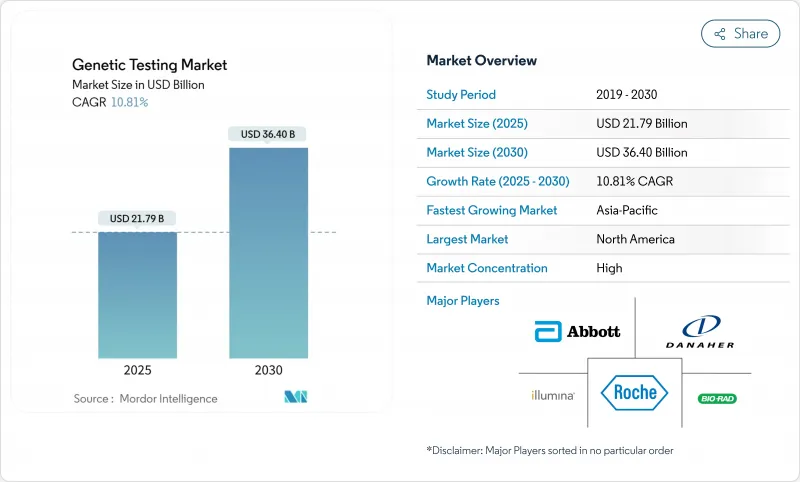

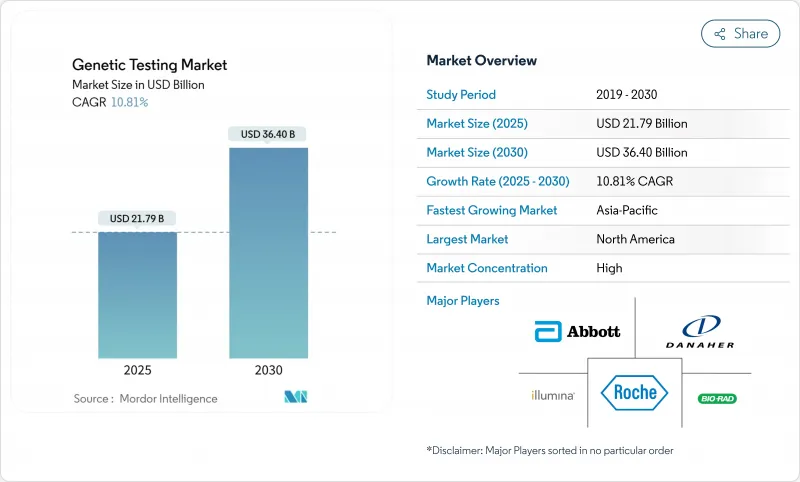

유전자 검사 시장은 2025년에 217억 9,000만 달러에 이르고, 2030년에는 364억 달러에 이를 것으로 예상되며, CAGR은 10.81%를 나타낼 전망입니다.

최근 획기적인 보고 사이클을 7-9시간으로 단축하는 AI를 활용한 해석과 100USD 이하의 전체 유전체 시퀀싱에 의해 임상 비용의 패러다임이 재정의되어 세계적인 보급이 가속화되고 있습니다. 2025년 6월에 발표된 영국 신생아 DNA 검사 프로그램(6억 5,000만 파운드)에서 볼 수 있듯이, 국가 의료 시스템은 유전체 서비스를 일상 진료에 통합하려고 합니다. 규제의 무결성, 특히 종양학에 대한 FDA의 새로운 동반진단의 의무화는 전문 분야 간의 검사 요청을 더욱 정상화합니다. 유전자 검사 시장은 현재 기록적인 벤처기업의 자금 조달, 플랫폼 인수의 물결, 고용자의 의료 보험 적용 범위의 확대 등의 혜택을 받고 있으며, 이들은 공동으로 검사에 대한 접근성을 확대하는 동시에 가격 압축을 촉진하고 있습니다.

의료기관은 출생 전 검사를 전문적인 소개 서비스에서 루틴 스크리닝으로 전환하고 있습니다. 2025년 6월 영국 이니셔티브에서는 모든 신생아의 순서에 6억 5,000만 파운드를 할당하고 출생 시 200개 이상의 희귀질환의 검출을 목표로 했습니다. 비침습적 출생 전 및 초음파 검사는 복잡한 염색체 이상에 대해 88.24%의 민감도를 달성하고 기존 프로토콜을 훨씬 웃도는 것이 파일럿 연구에서 나타났습니다. 실용적인 소견을 보다 조기에 발견함으로써, 의료 시스템은 평생에 걸친 치료의 절약과 발달상의 결과의 개선을 기대하고 있습니다. 이 접근법은 동시에 참조 유전체을 강화하고 하류 연구 협력을 촉진하는 집단 데이터 뱅크를 축적합니다. 각국의 보험사가 진료보상체계를 성문화함에 따라 출생전 유전체 패널이 신흥경제국에서 산과진료의 디폴트가 될 가능성이 높습니다.

머신 러닝 알고리즘은 현재 수백만 개의 변형을 트리어지며 몇 시간 이내에 임상적으로 중요한 소견에 주석을 달고 있습니다. 옥스포드 나노포어의 신속한 시퀀싱 파이프라인은 신생아 집중 치료와 감염 치료의 현장에 변화를 가져오는 결과를 당일 제공합니다. GeneDx가 2025년에 인수한 Fabric Genomics는 딥러닝을 통한 의사결정 지원을 통합하여 수작업으로 인한 큐레이션 비용을 절감하며 희귀질환의 엑솜 검사에서 진단 수율을 향상시킵니다. 이러한 생산성 향상으로 실험실은 인원을 늘리지 않고 검사 건수를 늘릴 수 있으며, 인증 유전 카운슬러의 세계 부족으로 인한 백로그를 완화할 수 있습니다. AI는 또한 과제 샘플의 증폭 성공률을 향상시켜 열화된 DNA의 법의학적 분석 등 롱테일의 응용을 해방합니다.

대규모 유전체 연구에 필수적인 국경을 넘어서는 데이터 흐름을 복잡하게 하는 것은 모자이크 형태로 확대하는 프라이버시법입니다. 2023년 이후 미국 각 국가의 유전자 프라이버시법에 근거하여 30개 이상의 집단 소송이 DNA 데이터의 부적절한 취급을 주장하였으며, 위반자는 고의 위반 1건당 최고 1만 5,000달러의 벌금에 노출되어 있습니다. 유럽연합(EU)의 GDPR(EU 개인정보보호규정)은 명시적인 동의를 의무화하고 데이터 최소화를 의무화하여 소비자 직접 판매 기업의 2차 분석 수익을 억제하고 있습니다. 인도의 2025년 디지털 개인 데이터 보호법은 다국적 실험실의 인프라 비용을 높이는 로컬 스토리지 요구 사항을 부과합니다. 컴플라이언스에 대한 지출은 연구 개발에서 자금을 유출시켜 여러 지역에서의 임상시험 등록을 감속시키고 유전자 검사 시장의 당면 성장 궤도를 억제합니다.

차세대 시퀀서는 현재 유전자 검사 시장 매출의 50.57%를 차지하고 있으며, 높은 처리량 임상 워크플로우에서 중심적인 역할을 명확하게 보여주고 있습니다. 이 부문은 종양 프로파일링을 한 번의 실행으로 응축시킨 일루미나 500 유전자 TruSight Oncology Comprehensive 키트와 같은 멀티플렉스 패널에서 이익을 얻습니다. 대조적으로 Seegene의 듀얼 프라이밍 올리고뉴클레오티드와 같은 혁신적인 기술에 견인되는 PCR 시스템은 병원이 80분 이내에 보고하는 신속한 호흡기 병원체 패널을 채용하기 때문에 2030년까지 11.23%를 나타낼 것으로 예측됩니다. Microarray와 Sanger Sequence는 각각 Validation과 Small Gene Target이라는 틈새 유용성을 유지하고 있으며, 실험실은 NGS 탐색과 PCR 확인을 결합한 하이브리드 워크스트림을 점점 도입하고 있습니다. 시약가격 하락과 통합분석 플랫폼이 소규모 클리닉의 원내 유전체 해석의 시작을 지원하고 자본 예산에 제약이 있어도 PCR 기반 툴의 유전자 검사 시장 규모를 확대하고 있습니다.

Sanger Sequence는 그 정밀도의 높이로부터 일 염기의 식별이 필요한 유전성 암 변이의 확인 검사에 적합합니다. Fluorescence In Situ Hybridization는 혈액 악성 종양에서 암원성 전좌의 검출에 여전히 필수적입니다. 그러나 의료 시스템이 종합적인 커버리지, 빠른 턴어라운드, 메가베이스당 비용 우위를 우선시함에 따라 장기적인 궤도는 NGS와 AI에 최적화된 PCR에 분명히 유리해지고 있습니다. 벤더의 로드맵은 업스트림 PCR 농축과 호환되는 ONT 플로우 셀 화학과 같은 수렴하는 기술 스택도 밝혀내고 있으며, 시퀀싱의 모달리티 선택이 워크플로우에 얽매이지 않는 통합된 미래를 가리킵니다.

북미는 충분한 자금을 갖춘 건강 관리 시스템, 정교한 지불자의 틀, 활발한 M&A 환경을 통해 유전자 검사 시장을 지원합니다. 고용주 부담의 유전학적 복리후생은 현재 미국 기업의 44% 가족력 검사를 다루고 있으며, 그중에서도 종양학 패널의 이용이 가장 증가하고 있습니다. 캐나다에서는 국민 모두 보험의 시행이 진행되고, 멕시코에서는 민간 보험사가 유전성 암 검진의 적용 범위를 서서히 넓히고 있습니다. 그러나 노동력 부족은 여전히 심각하고, 공인 유전 카운슬러가 차로 30분 이내에 있는 농촌 주민들은 불과 6%로 공정한 확대를 제한하는 격차가 되고 있습니다.

유럽에서는 강력한 공적 자금과 엄격한 데이터 보호 모니터링이 결합되어 있습니다. 영국 신생아 시퀀싱에 대한 투자 금액은 6억 5,000만 파운드로 임상 개발에 자금을 제공할 뿐만 아니라 이미 세계 최대의 페놈 유전체 데이터 세트 nhs.uk에 연결된 UK 바이오뱅크의 자원을 강화하고 있습니다. 독일과 프랑스는 다 유전자 종양학 패널을 법정 보험에 통합하고 이탈리아는 PNRR 회수 자금을 지역 유전체 실험실로 돌리고 있습니다. GDPR(EU 개인정보보호규정)의 동의 의무화는 컴플라이언스상의 장애물을 초래하지만, 동시에 종단적 연구에 시민들의 참여를 촉구하는 높은 신뢰성의 환경도 만들어 냅니다.

아시아태평양은 유전자 검사 시장에서 가장 급성장하는 지역으로 중국, 인도, 싱가포르, 호주 인구 유전체 프로그램이 그 원동력이 되고 있습니다. 중국의 병원 네트워크에서는 생식계열과 체세포를 조합한 분석이 일상적으로 도입되고 있으며, 그 예로 전체 엑솜 시퀀싱에서 65.2%의 진단률을 달성한 768명의 난청 환자 연구를 들 수 있습니다. 인도의 10,000 유전체 데이터 세트는 변형의 병원성 결정을 크게 향상시키는 조상 서열 참조를 제공합니다. 싱가포르의 2025년 중반 가족성 고콜레스테롤혈증의 전국 스크리닝은 컴팩트한 국가들이 유전체학를 예방 순환기학 워크플로우에 통합할 수 있음을 보여줍니다. 일본과 한국은 첨단 어세이 개발로 지역의 능력을 보충하고 있지만, 호주는 임상의의 교육 격차에 시달리고 있으며, 3차 시설 이외의 종합적인 도입이 늦어지고 있습니다.

The genetic testing market is valued at USD 21.79 billion in 2025 and is projected to reach USD 36.40 billion by 2030, advancing at a robust 10.81% CAGR.

Recent breakthroughs-AI-powered interpretation that compresses reporting cycles to 7-9 hours and sub-USD 100 whole-genome sequencing-are redefining clinical cost paradigms and accelerating global uptake. National health systems are embedding genomic services into routine care, as shown by the United Kingdom's GBP 650 million newborn DNA-testing program announced in June 2025 . Regulatory alignment, especially new FDA companion-diagnostic mandates for oncology, further normalizes test ordering across specialties. The genetic testing market now benefits from record venture funding, a wave of platform acquisitions, and widening employer health-plan coverage that jointly expand test accessibility while driving price compression.

Healthcare agencies are moving prenatal testing from a specialized referral service to routine screening. The June 2025 UK initiative allocates GBP 650 million to sequence every newborn, aiming to detect more than 200 rare disorders at birth nhs.uk. Pilot studies show that non-invasive prenatal testing plus ultrasound reaches 88.24% sensitivity for complex chromosomal anomalies, far surpassing conventional protocols. By flagging actionable findings earlier, health systems expect lifetime treatment savings and improved developmental outcomes. The approach simultaneously amasses population databanks that enrich reference genomes and fuel downstream research collaborations. As national insurers codify reimbursement pathways, prenatal genomic panels will likely become default obstetric practice in developed economies.

Machine-learning algorithms now triage millions of variants and annotate clinically significant findings within hours. Oxford Nanopore's rapid sequencing pipeline delivers same-day results-transformative for neonatal intensive-care and infectious-disease settings. GeneDx's 2025 purchase of Fabric Genomics integrates deep-learning decision support that trims manual curation costs and lifts diagnostic yields in rare-disease exome testing. These productivity gains permit laboratories to scale volumes without proportional staffing increases, easing backlogs created by the global shortage of certified genetic counselors. AI also unlocks long-tail applications-such as forensic analysis of degraded DNA-by improving amplification success rates in challenging samples.

A growing mosaic of privacy statutes complicates cross-border data flows essential for large-scale genomic research. Since 2023, more than 30 class actions have alleged improper DNA data handling under state genetic-privacy laws in the United States, exposing offenders to penalties up to USD 15,000 per deliberate breach. The European Union's GDPR obliges explicit consent and mandates data-minimization, curbing secondary analytics revenue for direct-to-consumer firms. India's 2025 Digital Personal Data Protection Act imposes local-storage requirements that raise infrastructure costs for multinational labs. Compliance spending diverts capital from R&D and slows multi-regional clinical-trial enrollment, tempering the genetic testing market's immediate growth trajectory.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Next-Generation Sequencing currently accounts for 50.57% of genetic testing market revenue, underscoring its central role in high-throughput clinical workflows. The segment benefits from multiplexed panels such as Illumina's 500-gene TruSight Oncology Comprehensive kit, which condenses tumor profiling into a single run. In contrast, PCR systems, led by innovations like Seegene's dual-priming oligonucleotides, are projected to grow at 11.23% through 2030 as hospitals adopt rapid respiratory-pathogen panels that report within 80 minutes. Although microarrays and Sanger sequencing retain niche utility-validation and small gene targets respectively-laboratories increasingly deploy hybrid workstreams that pair NGS discovery with PCR confirmation. Falling reagent prices and integrated analytics platforms help smaller clinics launch in-house genomics, pushing the genetic testing market size for PCR-based tools wider even where capital budgets are constrained.

Sanger sequencing's accuracy keeps it relevant in confirmatory testing for hereditary cancer variants that require single-nucleotide discrimination. Fluorescence in situ hybridization remains indispensable for detecting oncogenic translocations in hematological malignancies. Yet the long-term trajectory clearly favors NGS and AI-optimized PCR as health systems prioritize comprehensive coverage, faster turnaround, and cost per megabase advantages. Vendor roadmaps also reveal converging technology stacks, such as ONT flowcell chemistries compatible with upstream PCR enrichment, pointing to an integrated future where sequencing modality choices become workflow agnostic.

The Genetic Testing Market Report Segments the Industry Into by Technology (Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR) and More ), by Application (Cancer Diagnosis & Prognosis, Cardiovascular Disease Diagnosis, and More), by End User (Hospitals & Clinics, Diagnostic Laboratories and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

North America anchors the genetic testing market through well-funded healthcare systems, sophisticated payer frameworks, and an active M&A environment. Employer-sponsored genetic benefits now cover 44% of U.S. firms for family-history testing, with oncology panels seeing the strongest utilization uptick. Canada advances universal reimbursement pilots, while Mexico's private insurers slowly broaden coverage for hereditary cancer screens. Workforce shortages, however, remain acute: just 6% of rural residents live within a 30-minute drive of a certified genetic counselor, a distribution gap that limits equitable expansion.

Europe combines strong public-sector funding with rigorous data-protection oversight. The United Kingdom's GBP 650 million newborn sequencing investment not only funds clinical roll-out but also augments the UK Biobank resource-already the world's largest linked phenome-genome dataset nhs.uk. Germany and France integrate multigene oncology panels into statutory insurance, whereas Italy channels PNRR recovery funds into regional genomic labs. GDPR's consent mandates pose compliance hurdles, yet they also create a high-trust environment that encourages citizen participation in longitudinal research.

Asia-Pacific is the fastest-growing territory for the genetic testing market, driven by population genomics programs across China, India, Singapore, and Australia. China's hospital networks routinely deploy combined germline and somatic assays, exemplified by a 768-patient hearing-loss study that achieved a 65.2% diagnostic yield with whole-exome sequencing. India's 10,000-genome dataset supplies ancestry-aligned references that significantly improve variant pathogenicity calls. Singapore's mid-2025 nationwide screen for familial hypercholesterolemia demonstrates how compact nations can integrate genomics into preventive cardiology workflows. Japan and South Korea supplement regional capacity with advanced assay development, while Australia grapples with clinician education gaps that slow comprehensive uptake outside tertiary centers.