초음파 기기 시장 규모는 2025년에 91억 2,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 3.77%를 나타내, 2030년에는 109억 8,000만 달러에 달할 것으로 예상됩니다.

실시간으로 방사선을 사용하지 않는 영상 진단에 대한 일관된 수요, 영상 획득 및 해석에 있어서 인공지능(AI)의 급속한 보급, 1차 케어에서의 핸드헬드 프로브의 보급이 이 성장을 지원하고 있습니다. 임상적 증거에 따르면 AI 지침을 통해 전문가가 수행하지 않은 검사의 진단 품질은 98.3%까지 향상되어 전문의의 성능에 필적합니다. 성숙시장이 프리미엄 3D&4D 시스템의 교체 수요를 계속 견인하는 한편, 신흥국은 공중보건 프로그램을 통해 최초 구매를 뒷받침합니다. CT와 MRI에 실시간 초음파를 오버레이하는 멀티모달 퓨전 플랫폼과 결합된 저침습 절차에 대한 축족이 이 기술의 기술적 역할을 펼치고 있습니다. 동시에 미국에서는 POC(Point-of-Care) 기기에 대한 상환의 격차가 뿌리 깊고 세계적인 품질 시스템 규제의 강화로 그 기세는 약해지고 있습니다.

심혈관 질환, 종양성 질환, 호흡기 질환이 초음파 검사 소개의 대부분을 차지하고 있으며, 만성 질환 관리가 구조적인 수요 촉진요인이 되고 있습니다. 난소 종양 검출을 위한 AI 모델은 F1 점수 83.5%를 달성하고 전문 방사선과 의사를 능가했습니다. 마찬가지로, 딥러닝 툴은 수근관 스캔으로 정중 신경을 높은 정밀도로 확인합니다. 미국암협회는 2025년 미국에서 새롭게 발생하는 암 환자 수를 2024년 200만명에서 204만명으로 증가시킬 것으로 예측하고 있으며 장기적인 영상 진단 수요를 강화하고 있습니다. AI는 워크플로우를 가속하고 정확도를 높이기 위해 훈련된 초음파 검사사의 부족을 보완하고 사용자 기반을 넓히고 초음파 기기 시장을 유지합니다.

바늘 유도 생검, 국소 마취, 근골격계 주사에 대한 세계적인 축족은 초음파의 수술적 관련성을 깊게 합니다. 라이브 초음파와 CT, MRI, PET 스캔을 융합시킨 퓨전 플랫폼은 복잡한 사례에서 병변 타겟팅을 향상시키고 있습니다. 시설의 성장은 설치 기반을 강화한다 : 인도는 2024년 2월에 5,200개의 NABL 인증 실험실을 세고, 그 44%가 방사선과였습니다. 호주에서는 2023년 12월까지 4,462개의 인증된 이미지 클리닉이 나열되었으며, 81%가 인구가 많은 3개 주에 집중되었습니다. 콜롬비어 닥터스/뉴스 프레스 비테리안의 맨해튼 사이트와 같은 새로운 센터가 2025년 1월에 오픈하여 고밀도 도시에 서비스를 제공했습니다. 이러한 지리적 확산은 럭셔리 기계와 중급기 모두에 대한 안정적인 수요로 이어져 초음파 기기 시장을 강화하고 있습니다.

POC(Point-of-Care) 초음파(POCUS)에는 1 차 진료의 많은 적응증에 대한 전용 청구 코드가 없습니다. 진료 보상 모델은 외래나 재택에서의 초음파 기기 시장 성장 억제요인이 되어 폭넓은 보급을 방해하고 있습니다. 최근 CMS의 제안은 전진을 시사하는 것이지만, 민간지급자간 정책의 분단은 계속되고 있어 의료 제공업체의 투자 대 효과를 늦추고 있습니다.

2024년 초음파 기기 시장 매출의 23.3%는 방사선학 용도이 차지하고 다장기 영상 진단의 요구가 그 원동력이 되었습니다. 난소 악성 종양에 플래그를 지정하는 AI 모듈은 이제 인간의 전문 지식을 능가하고, 병원은 방사선과 워크 스테이션의 업그레이드를 강요하고 있습니다. 또한, 엘라스토그래피의 개선으로 간 섬유증의 병기 분류가 더욱 선명해지고, 비침습적 스크리닝 라이브러리의 폭이 넓어지고 있습니다.

절차 유도 마취학은 규모는 작지만 CAGR 4.9%를 나타낼 전망입니다. 신경 블록의 채택은 ScanNav Anatomy PNB와 같은 컬러 오버레이 보조기구의 혜택을 받았습니다. 마취제 사용량과 수술 후 통증 완화에 열성적인 병원은 전용 선형 프로브를 구입하여 수술기 초음파 기기 시장을 확대하고 있습니다.

POC(Point-of-Care) 스캐너에 대한 병원 예산 증가는 오피오이드 온존 진통을 장려하는 국가 수준의 지침과 함께 마취과에서 두 자릿수의 장비 업데이트율을 유지할 가능성이 높습니다. AI가 사전 설정된 이미지 프로토콜을 만들게 되면 임상의는 초음파 가이드 하단 블록을 정형외과뿐만 아니라 응급 및 집중 치료 환경으로 확장할 수 있다고 확신하게 됩니다. 이러한 부문 횡단적인 파급효과로 이용률이 향상되고 스캔당 비용이 절감되고 보다 광범위한 초음파 기기 시장에서 첨단 플랫폼 투자의 경제적 근거가 강화됩니다.

3D와 4D 체계는 2024년 초음파 기기 시장 점유율의 45.6%를 차지했습니다. 3D 및 4D 시스템은 산과, 소아과, 순환기과 같은 부피 시각화가 필요한 경우에 사용됩니다. 이들은 태아의 얼굴 특징을 실시간으로 자동 렌더링하는 머신러닝 알고리즘에 의해 지원됩니다. 이러한 자동화를 통해 임상의는 노보로지보다 상담에 집중할 수 있습니다.

HIFU는 자궁근종에서 췌장 종양에 이르기까지 틈새이지만 급속히 확대되는 치료 영역에 해당하며 CAGR 5.1%를 나타낼 것으로 예측됩니다. 학술 시험은 최소한의 회복 시간으로 의미있는 증상 완화를 나타내며, 중국과 유럽의 지불자가 상환의 틀을 평가하도록 촉구하고 있습니다. 수술 부문이 HIFU를 종양판에 통합함에 따라 방사선과 예산 내에 들어가면서 수익원이 다양해지고 초음파 기기 시장의 궤도가 강화됩니다.

절제 구역을 즉시 정량화하는 통합 AI 대시보드는 수술 중 불확실성을 줄입니다. 이 정확도는 신속한 턴오버와 감염 위험의 감소가 중시되는 외래 데이 케어 모델로 종양학의 변화를 보완합니다. 그 결과, 높은 프레임 레이트 이미징과 치료 빔을 융합시키는 기술 벤더는 초음파 기기 시장에서 자본 지출 증가의 압도적 점유율을 획득할 가능성이 높습니다.

북미는 2024년에 38.1%의 매출 점유율을 유지했는데, 이는 강력한 페이어 커버리지, 높은 만성 질환 부담, 꾸준한 기술 갱신 사이클에 의한 것입니다. Vave Health의 전신 무선 기기와 GE 건강 관리의 자동 유방 초음파 프리미엄 등의 출시는 AI를 통합한 혁신에 대한 국내 의욕을 보여줍니다. 규정의 명확화와 유방 밀도 스크리닝의 CPT 코드는 이러한 솔루션의 신속한 도입을 지원합니다. 병원에서는 구급 부문에 핸드헬드 프로브를 장비하는 케이스가 늘어나고 있으며, 트리아지 시간을 단축하고 침대 흐름을 개선함으로써 초음파 기기 시장의 활성화로 이어지고 있습니다.

아시아태평양은 CAGR 4.8%로 가장 빠르게 성장하는 지역입니다. 중국은 Mindray의 Consona 시리즈와 같은 국산 콘솔을 선호하는 조달 프로그램을 통해이 지역의 수를 독점하고 있습니다. Wipro GE의 Versana Premier R3은 벵갈루로 조립된 AI 지원 시스템입니다. 과밀한 프라이머리 케어 센터에서의 POC(Point-of-Care) 초음파의 채용에 의해 최초회 구입이 가속하고 있지만, PCPNDT법에 의해 산과의 대수는 억제되고 있습니다. 그럼에도 불구하고 공공 보험 회사에 의한 간 검사 및 심장 검사 환불이 증가하고 있으며 초음파 기기 시장의 지역 상승을 지원합니다.

유럽은 여전히 기술 중심 시장입니다. 유럽 의약품청(European Medicines Agency)과 같은 기관은 확실한 임상 데이터를 요구하고 있으며, 공급업체는 무선량 이미지와 전자 의료 기록과의 상호 운용성에 대한 증거를 제시하도록 요청받고 있습니다. 본태성 진전에 대한 Insightec의 MRgFUS는 독일에서 NUB 상태를 획득하고 상환을 받습니다. WONCA 유럽은 일반 개업의를 대상으로 한 체계적인 초음파 훈련을 전개하여 지역 의료의 밑단을 넓히고 있습니다. 이러한 역학을 종합하면 유럽은 초음파 기기 시장에 중요한 공헌자로 계속되고 있습니다.

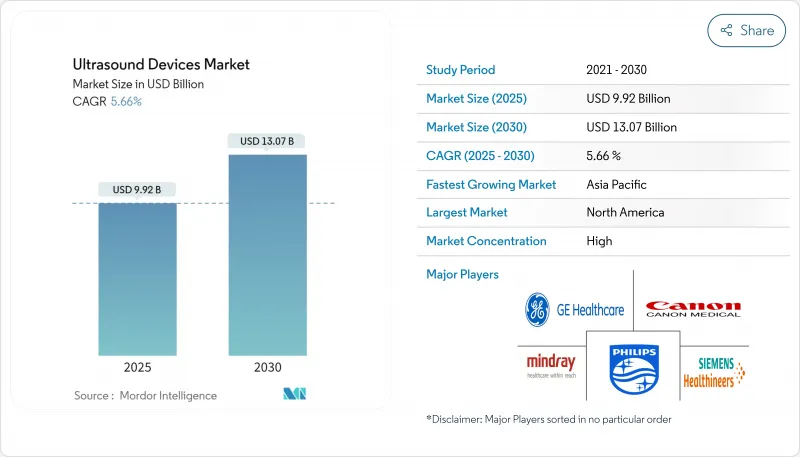

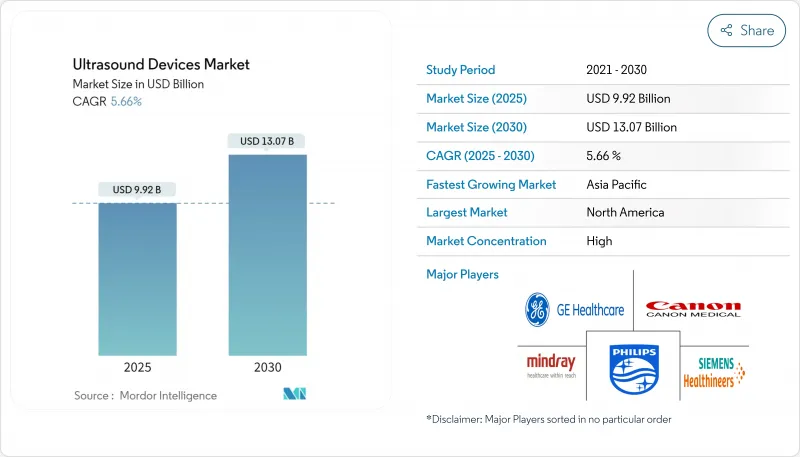

The Ultrasound Devices Market size is estimated at USD 9.12 billion in 2025, and is expected to reach USD 10.98 billion by 2030, at a CAGR of 3.77% during the forecast period (2025-2030).

Consistent demand for real-time, radiation-free imaging, rapid uptake of artificial intelligence (AI) in image acquisition and interpretation, and widening use of handheld probes in primary care underpin this growth. Clinical evidence shows AI guidance can lift the diagnostic quality of scans performed by non-experts to 98.3%, matching specialist performance. Mature markets keep driving replacement demand for premium 3D & 4D systems, while emerging economies propel first-time purchases through public health programs. A pivot toward minimally invasive procedures, combined with multimodal fusion platforms that overlay real-time ultrasound on CT or MRI, broadens the technology's procedural role. At the same time, persistent reimbursement gaps for point-of-care devices in the United States and tightening global quality-system regulations temper momentum.

Cardiovascular, oncologic, and respiratory disorders account for most ultrasound referrals, making chronic-disease management a structural demand catalyst. An AI model for ovarian-tumor detection achieved an F1 score of 83.5%, surpassing expert radiologists. Similarly, deep-learning tools pinpoint the median nerve in carpal-tunnel scans with high accuracy. The American Cancer Society projects 2.04 million new cancer cases in the United States in 2025, up from 2.00 million in 2024, reinforcing long-term imaging demand. As AI accelerates workflow and elevates accuracy, it compensates for shortages of trained sonographers, broadening the user base and sustaining the ultrasound devices market.

A global pivot toward needle-guided biopsies, regional anesthesia, and musculoskeletal injections is deepening ultrasound's procedural relevance. Fusion platforms that marry live ultrasound with CT, MRI, or PET scans are improving lesion targeting in complex cases. Facility growth reinforces the installed base: India counted 5,200 NABL-accredited labs in February 2024, 44% of which were radiology units. Australia listed 4,462 accredited imaging practices by December 2023, 81% clustered in three populous states. New centers such as ColumbiaDoctors/NY-Presbyterian's Manhattan site opened in January 2025 to serve high-density urban catchments. This geographic spread of facilities feeds steady demand for both premium and mid-range ultrasound consoles, bolstering the ultrasound devices market.

Point-of-care ultrasound (POCUS) lacks dedicated billing codes for many primary-care indications. Fee-for-service models discourage broad deployment, constraining the ultrasound devices market in outpatient and home settings. Recent CMS proposals hint at progress, yet policy fragmentation across private payers persists, delaying return-on-investment for providers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Radiology applications generated 23.3% of the ultrasound devices market revenue in 2024, fueled by multi-organ imaging needs. AI modules that flag ovarian malignancies now surpass human expertise, pushing hospitals to upgrade radiology workstations. Elastography refinements have also sharpened liver-fibrosis staging, widening non-invasive screening libraries.

Procedure-guided anesthesiology is fleetingly smaller but expanding at a 4.9% CAGR. Nerve-block adoption benefits from color-overlay aids such as ScanNav Anatomy PNB, which simplifies landmark recognition for trainees. Hospitals keen to cut anesthetic drug volumes and postoperative pain are buying specialized linear probes, scaling the ultrasound devices market in perioperative suites.

Growing hospital budgets for point-of-care scanners, together with national-level guidance encouraging opioid-sparing analgesia, will likely sustain double-digit equipment refresh rates in anesthesia departments. As AI curates preset imaging protocols, clinicians gain confidence to extend ultrasound-guided blocks beyond orthopedics into emergency and intensive-care environments. This cross-departmental spillover lifts utilization rates, reducing per-scan costs and reinforcing the economic case for investing in advanced platforms within the broader ultrasound devices market.

3D and 4D systems contributed 45.6% of the ultrasound devices market share in 2024. They are favored for obstetrics, pediatrics, and cardiology cases that need volumetric visualization. They are supported by machine-learning algorithms that auto-render fetal facial features in real time. Such automation frees clinicians to focus on counseling rather than knobology.

HIFU addresses niche but fast-scaling therapeutic areas from uterine fibroids to pancreatic tumors and is projected to grow at 5.1% CAGR. Academic trials indicate meaningful symptom relief with minimal recovery time, prompting payers in China and Europe to evaluate reimbursement frameworks. As surgical departments integrate HIFU into tumor boards, they diversify revenue streams while staying within radiology budgets, reinforcing the ultrasound devices market trajectory.

Integrated AI dashboards that quantify ablation zones instantaneously reduce intraoperative uncertainty. This precision complements oncology's shift to outpatient day-care models, where rapid turnover and reduced infection risk are premiums. Consequently, technology vendors that meld high-frame-rate imaging with therapy beams will likely capture outsized share of incremental capital spending within the ultrasound devices market.

The Ultrasound Devices Market Report Segments the Industry Into by Application (Anesthesiology, Cardiology, and More), Technology (2D Ultrasound Imaging and More), Portability (Stationary Ultrasound, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

North America retained a 38.1% revenue share in 2024 owing to strong payor coverage, a high chronic-disease burden, and steady technology refresh cycles. Launches such as Vave Health's whole-body wireless device and GE HealthCare's Automated Breast Ultrasound Premium illustrate the domestic appetite for AI-embedded innovation. Regulatory clarity and CPT codes for breast density screening underpin the quick onboarding of these solutions. Hospitals increasingly equip emergency departments with handheld probes, trimming triage times and improving bed flow, thus lifting the ultrasound devices market.

Asia-Pacific ranks as the fastest-growing region at a 4.8% CAGR. China dominates regional volume through procurement programs favoring domestically made consoles like Mindray's Consona series. India's "Make in India" ethos echoes through Wipro GE's Versana Premier R3, an AI-ready system assembled in Bengaluru. Adoption of point-of-care ultrasound in overcrowded primary-care centers accelerates first-time purchases, though the PCPNDT Act restrains obstetric volumes. Nevertheless, public insurers increasingly reimburse liver and cardiac scans, sustaining the ultrasound devices market's regional ascent.

Europe remains a technology-focused market. Agencies such as the European Medicines Agency require robust clinical data, prompting vendors to showcase evidence on dose-free imaging and interoperability with electronic health records. Focused-ultrasound milestones Insightec's MRgFUS for essential tremor winning NUB status 1 reimbursement in Germany highlight innovation's role in neurology and oncology insightec.com. WONCA Europe is rolling out structured ultrasound training for general practitioners, widening the community-care footprint. Collectively, these dynamics keep Europe a vital contributor to the ultrasound devices market.