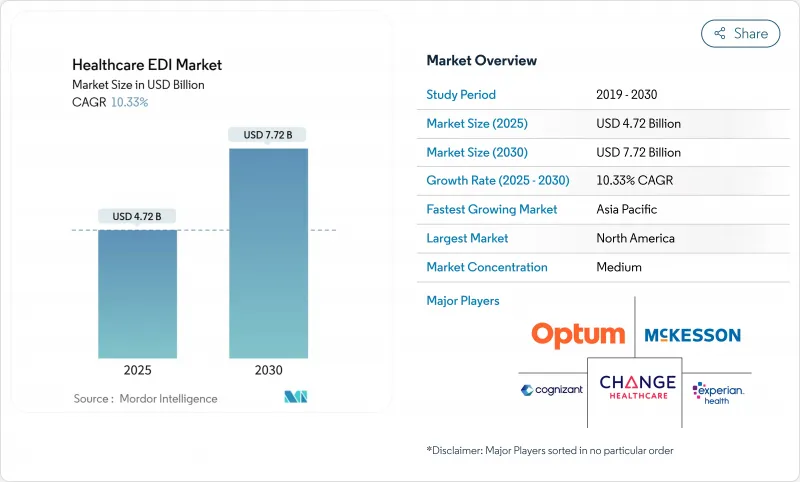

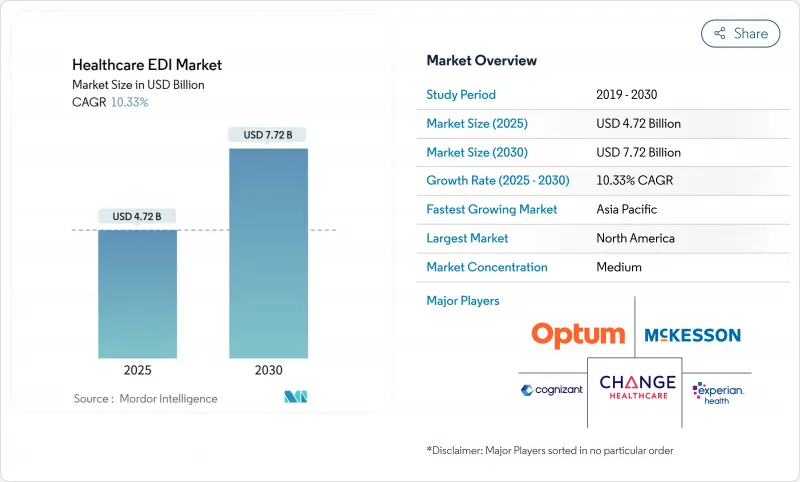

헬스케어 EDI 시장의 2025년 시장 규모는 47억 2,000만 달러로 추정되고, 2030년에는 77억 2,000만 달러에 이를 전망이며, CAGR 10.33%로 성장할 전망입니다.

디지털화의 진전, 비용 억제의 의무화, 엄격한 데이터 교환 규제에 의해 지불자, 의료 제공업체, 생명과학 기업의 채용이 가속화되고 있습니다. 클라우드로의 마이그레이션이 넓어짐으로써 도입 시의 마찰이 경감되는 한편, 밸류 베이스 케어로의 시프트가 가속됨으로써 실시간 멀티 파티 데이터 흐름에 대한 새로운 수요가 탄생하고 있습니다. 2025년 체인지 헬스케어 사건 이후 사이버 보안에 대한 인식이 높아지고 안전하고 감사 가능한 거래 플랫폼에 대한 투자가 더욱 증가하고 있습니다. 상호 운용성, 고급 분석 및 견고한 컴플라이언스 도구를 결합한 공급업체는 의료기관이 단편화된 수작업 워크플로에서 철수하는 동안 새로운 화이트 스페이스 기회를 획득했습니다.

미국에서는 HIPAA 거래가 계속 의무화되고 있으며, 공급자와 지불자는 표준화된 EDI 형식을 통해 청구, 송금, 자격 데이터를 교환할 의무가 있습니다. CMS가 버전 8010으로 직접 마이그레이션하는 것을 고려하는 것은 전통적인 모호성을 제거하고 현대화된 프레임워크의 긴급성을 강조합니다. 유럽과 아시아에서도 같은 지령이 내려져, 공통 구문에 대한 수렴이 진행되고 있으며, 다국적 기업의 구현 스케줄이 단축되어, 헬스 케어 EDI 시장의 CAGR에 약 2.8포인트 기여하고 있습니다. 수출 주도형 아시아의 의료기술 벤더, 특히 한국과 대만의 벤더는 북미와 유럽 경제 영역에서 거래 상대방에게 받아들여지기 위해 이러한 연계를 활용하고 있습니다.

헬스케어 조직은 전자 거래 1건 당 종이에 비해 평균 2.7달러를 절약하고 처리 시간을 82% 줄였습니다. 진료 보수의 감액에 의해 마진이 압박되는 가운데, 수익 사이클 매니저는 풀 장비의 EDI를 양도할 수 없는 경영 요건이라고 생각하게 되어 있습니다. 승인 전 검사 및 송금 데이터의 자동 게시를 자동화하는 도입은 관리 비용 센터에서 15-30%의 비용 절감을 실현하여 헬스케어 EDI 시장의 성장 시나리오를 보다 견고하게 하고 있습니다.

2025년 2월에 발생한 체인지 헬스케어의 랜섬웨어 공격은 전국적인 보험금 청구를 방해했으며, 유나이티드 헬스 그룹은 65억 달러의 구제금을 지불해야 했습니다. 그 결과 트랜잭션 라우팅 및 암호화 계층 모니터링이 강화되어 위험을 싫어하는 공급자의 EDI 배포 속도가 느려지고 잠재적인 CAGR이 1.2% 감소했습니다.

2024년 헬스케어 EDI 시장은 클라우드 지원 클리어링 하우스 엔진이 표준화되었기 때문에 소프트웨어가 매출의 56%를 차지하고 있으며 지속적인 시장이 되고 있습니다. 그러나 서비스 부문은 2030년까지 연평균 복합 성장률(CAGR) 12.40%로 확대되어 내부 전문 지식 부족과 지속적인 진화를 위한 컴플라이언스 의무에 부응하고 있습니다. 맵핑, 파트너 온보딩, 24시간 365일 거래 모니터링을 제공하는 컨설턴트 회사는 적극적인 디지털 의제를 추구하는 중규모 시스템의 중요한 기술 격차를 채웁니다.

Managed Services에 대한 의존도가 높아지면 X12, HL7 FHIR 및 자체 API를 통합하는 복합 워크플로의 향상도 반영됩니다. 공급자는 데이터 스튜어드십, 예외 처리 및 지속적인 테스트를 위해 외부 전문가를 활용합니다. 서비스 제공 헬스케어 EDI 시장 규모는 2030년까지 30억 달러 이상에 달할 것으로 예상되는 반면, 가상화된 게이트웨이가 랙 기반 모뎀을 대체할수록 하드웨어 실적이 줄어들고 있습니다.

클레임 관리는 2024년 헬스케어 EDI 시장의 48% 매출 점유율을 차지했으며, 현금 흐름 보전에 있어 핵심적인 역할을 보여줍니다. 그러나 의료 시스템이 EDI를 활용하여 재고를 간소화하고, 장비 비용 상승을 억제하고 있기 때문에 공급망 거래는 11.10%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 자동화된 구매 주문서, ASN 피드, 위탁 재고 경고는 재고 부족을 줄이고 운전 자본을 해제하기 위해 공급망 EDI는 CFO의 전략적 테코로 자리매김하고 있습니다.

IoT 원격 측정과 EDI 메시지 세트를 함께 사용하면 온도에 민감한 생물학적 제제의 만료 시간을 실시간으로 추적하여 낭비를 줄일 수 있습니다. 이 수렴은 조달 팀과 생물 의학 엔지니어링 팀을 공동 거버넌스 협의회로 이끌어 헬스케어 EDI 시장 전반에 걸쳐 통합된 네트워크 전체의 데이터 가시성에 대한 수요를 강화하고 있습니다.

북미는 2024년 매출의 43%를 차지했으며, HIPAA의 의무화 및 성숙한 클리어링하우스 네트워크에 힘입어 선두를 유지했습니다. 거의 모든 메디케어 진료 보상 청구가 전자화되어 헬스케어 EDI 시장의 높은 기준선을 확립하고 있습니다. Interoperability and Prior Authorization Final Rule(상호 운용성 및 사전 승인에 대한 최종 규칙)은 디지털 요구 사항을 강화하고, 상업 지불자를 예외 처리의 자동화로 향하게 하며, 소규모 의료 제공업체 그룹에게도 대응할 수 있는 기회를 넓히고 있습니다.

아시아태평양은 CAGR 11.90%로 가장 빠르게 성장하고 있으며, 중국, 인도, 인도네시아 의료 보험의 급속한 확대와 정부의 대규모 클라우드 이니셔티브에 힘쓰고 있습니다. 모바일 퍼스트의 채용에 의해 클리닉은 종래의 모뎀 인프라를 우회할 수 있게 되어, 보급이 가속하고 있습니다. 한국 등에서는 전자청구서의 발행이 의무화되어 헬스케어 데이터 교환에 대한 지출이 가속되고, 이 지역의 헬스케어 EDI 시장 규모는 2030년까지 16억 달러로 확대됩니다.

유럽에서는 다양한 채용 곡선을 볼 수 있습니다. 독일은 DRG 상환의 틀 안에서 통일된 조달 교환의 규모를 확대하고 영국은 임상 이벤트를 청구 가능한 EDI 반권으로 변환하는 국경을 넘은 EHR 연계를 우선하고 있습니다. 스칸디나비아는 환자의 자격 검사를 간소화하는 전국 전자 ID 시스템의 혜택을 받고 있습니다. 이러한 노력으로 유럽은 헬스케어 EDI 시장에서 매출 2위를 차지하고 있습니다.

The Healthcare EDI market is valued at USD 4.72 billion in 2025 and is on course to reach USD 7.72 billion by 2030, advancing at a 10.33% CAGR.

Growing digitization, cost-containment mandates, and stringent data-exchange regulations are reinforcing adoption across payers, providers, and life-science firms. Widespread cloud migration lowers implementation friction, while the accelerating shift to value-based care creates fresh demand for real-time, multi-party data flows. Heightened cybersecurity awareness following the 2025 Change Healthcare breach further elevates investment in secure, auditable transaction platforms. Vendors that combine interoperability, advanced analytics, and robust compliance tooling are capturing new white-space opportunities as healthcare entities retire fragmented, manual workflows.

HIPAA transactions remain obligatory in the United States, compelling providers and payers to exchange claims, remittances and eligibility data through standardized EDI formats. CMS deliberations on skipping directly to Version 8010 underscore the urgency of a modernized framework that removes legacy ambiguities. Similar mandates in Europe and Asia are converging toward common syntaxes, compressing implementation timelines for multinationals and contributing roughly 2.8 percentage points to the Healthcare EDI market CAGR. Export-driven Asian health-tech vendors, particularly in South Korea and Taiwan, leverage this alignment to gain trading-partner acceptance in North America and the European Economic Area.

Healthcare organizations save an average of USD 2.7 per electronic transaction versus paper, trimming 82% of processing time. With reimbursement erosion squeezing margins, revenue-cycle managers increasingly view full-suite EDI as a non-negotiable operating requirement. Deployments that automate pre-authorization validation and auto-post remittance data deliver 15-30% cost reductions in administrative cost centers, reinforcing the Healthcare EDI market growth narrative.

The February 2025 Change Healthcare ransomware attack disrupted claims nationwide and forced UnitedHealth Group to advance USD 6.5 billion in relief payments. Fallout heightened scrutiny of transaction routing and encryption layers, denting EDI rollout velocity among risk-averse providers and shaving 1.2% points from potential CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software remained the backbone of the Healthcare EDI market in 2024, generating 56% of total revenue as organizations standardized on cloud-ready clearinghouse engines. The services sub-segment, however, is expanding at a 12.40% CAGR through 2030, propelled by scarce in-house expertise and ever-evolving compliance mandates. Consultancies providing mapping, partner onboarding, and 24/7 transaction monitoring fill critical skill gaps for midsize systems pursuing aggressive digital agendas.

Growing reliance on managed services also reflects the rising sophistication of composite workflows that merge X12, HL7 FHIR, and proprietary APIs. Providers are turning to external specialists for data stewardship, exception handling, and continuous testing. The Healthcare EDI market size for service offerings is forecast to eclipse USD 3 billion by 2030, while the hardware footprint contracts as virtualized gateways replace rack-based modems.

Claims management held 48% revenue share of the Healthcare EDI market in 2024, underlining its centrality in cash-flow preservation. Nevertheless, supply-chain transactions are registering an 11.10% CAGR as health systems exploit EDI to rationalize inventory and tame rising device costs. Automated purchase orders, ASN feeds, and consignment stock alerts trim stock-outs and free working capital, positioning supply-chain EDI as a strategic lever for CFOs.

Interlacing IoT telemetry with EDI message sets offers real-time expiry tracking for temperature-sensitive biologics, reducing waste. This convergence is nudging procurement and biomedical engineering teams into joint governance councils, intensifying demand for integrated network-wide data visibility across the Healthcare EDI market.

Healthcare Electronic Data Interchange Market Report is Segmented by Component (Software, Hardware, and Services), by Transaction Type (Claims Management (837/835) and More), by Mode of Delivery (Web- and Cloud-Based EDI and More), by End User (Healthcare Providers and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained leadership with 43% of 2024 revenue, underpinned by HIPAA mandates and mature clearinghouse networks. Nearly all Medicare fee-for-service claims flow electronically, establishing a high baseline for the Healthcare EDI market. The Interoperability and Prior Authorization Final Rule intensifies digital requirements, nudging commercial payers toward automated exception handling and widening the addressable opportunity across smaller provider groups.

Asia-Pacific delivers the fastest growth at 11.90% CAGR, buoyed by rapid health-insurance expansion and extensive government cloud initiatives in China, India, and Indonesia. Mobile-first adoption allows clinics to bypass legacy modem infrastructure, accelerating penetration. Mandatory e-invoicing rules in economies such as South Korea cascade into accelerated healthcare data-exchange spending, lifting the regional Healthcare EDI market size toward USD 1.6 billion by 2030.

Europe showcases diverse adoption curves. Germany scales unified procurement exchanges within its DRG reimbursement framework, while the United Kingdom prioritizes cross-border EHR linkages that convert clinical events into billing-ready EDI stubs. Scandinavia benefits from nationwide electronic ID systems that streamline patient eligibility checks. Collectively, these initiatives maintain Europe's role as the second-largest regional contributor to the Healthcare EDI market revenue.