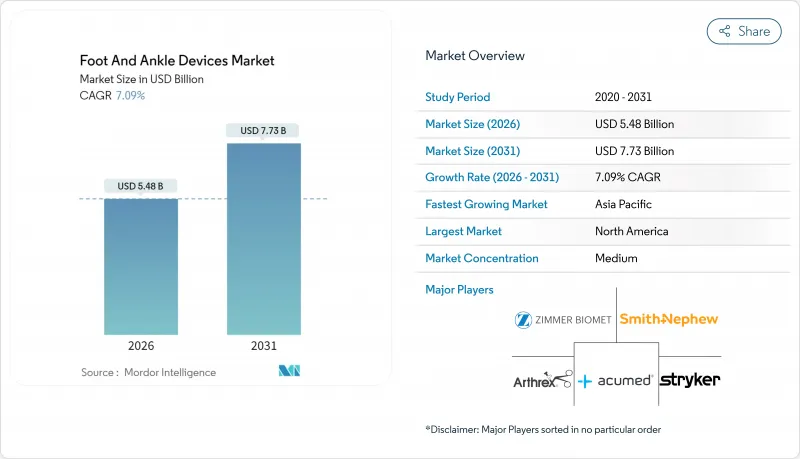

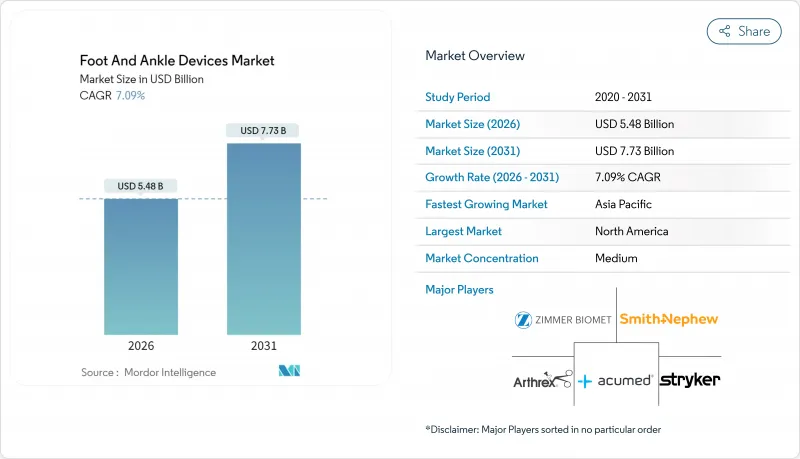

발 및 발목 기기 시장은 2025년에 51억 2,000만 달러로 평가되었고, 2026년 54억 8,000만 달러에서 2031년까지 77억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 7.09%를 나타낼 전망입니다.

환자 맞춤형 3D 프린팅 임플란트의 임상적 수용 확대, 외래 시술 건수 증가, 고정 재료의 지속적인 혁신으로 시술 건수와 평균 판매 가격이 모두 증가하고 있습니다. 자연 뼈 구조를 모방한 단일 기기 출시가 외과의사의 기대를 재편하는 한편, 스포츠 외상 및 당뇨병 관련 합병증과 연계된 강력한 수요가 단위 성장세를 안정적으로 유지하고 있습니다. 맞춤형 기기에 대한 규제 승인이 과거보다 빠르게 이루어지면서 소규모 혁신 기업들이 틈새 솔루션을 상용화하도록 장려하고 있습니다. 대형 정형외과 기업들은 발 및 발목용 기기 시장 전반에 걸쳐 종합 치료 플랫폼을 제공하기 위해 전문 기업들을 인수하며 대응하고 있습니다.

청소년 및 성인 운동선수들의 고에너지 발목 골절은 연중 수술 건수를 높게 유지합니다. 외과의들은 동반 질환 위험도에 따라 환자를 적극적으로 분류하여, 흡연자 및 만성 폐쇄성 폐질환 환자에게 조기 실패를 방지하는 강화형 고정 기기를 권장합니다. 스포츠 의학 프로그램 또한 수술 후 체중 부하 프로토콜을 표준화하여, 입원 회복에서 가정 기반 재활로의 전환을 가속화하고 간접적으로 고마진 외래 환자용 기기 판매를 촉진합니다. 종합적으로 이러한 요소들은 발 및 발목용 기기 시장 전반에 걸쳐 엄격한 운동 요구 사항을 위해 설계된 차세대 기기의 가격 결정력을 강화합니다.

당뇨병 유병률 증가로 사지 보존용 의료기기에 대한 장기적 수요가 촉진되고 있습니다. 당뇨병 환자의 15-25%가 당뇨병성 족부 궤양을 경험하며, 치료 비용은 1건당 최소 8,000달러에서 63,100달러 이상까지 치솟습니다. 임상 추적조사에 따르면 당뇨병 환자의 34%가 평생 궤양 발생 위험에 직면하며, 이 동반질환은 미국에서 비외상성 절단의 주요 원인으로 자리매김했습니다. 골감소증 뼈를 견디는 특수 잠금판, 원형 외부 고정기, 티타늄 융합 케이지는 현재 샤르코 재건술의 표준 치료법입니다. 데이터에 따르면 조기 고정술이 입원 기간 단축과 중증 감염 발생 억제에 효과적임이 입증되면서, 보험사들은 예방적 수술 개입을 점점 더 지지하고 있습니다. 이는 발 및 발목용 기기 시장의 꾸준하고 장기적인 성장을 촉진하고 있습니다.

보험 적용 범위는 과학적 발전 속도를 따라가지 못하고 있습니다. 기존 금속 나사와 플레이트는 명확한 청구 코드의 혜택을 받지만, B-삼칼슘인산염을 포함한 새로운 생분해성 복합재는 보험사들의 일관된 인정을 받지 못하고 있습니다. 결과적으로 환자가 추가 보험이나 자비 부담 능력이 없는 한 외과의들은 종종 이러한 임플란트 사용을 포기합니다. 지연된 보험급여가 극히 낮은 외래 환자 마진을 위협하기 때문에 병원들은 여전히 신중한 태도를 유지합니다. 무작위 대조 시험을 통해 생분해성 구조물이 후속 제거 수술을 없애고 감염 위험을 줄인다는 사실이 확인되었음에도 정책 불확실성으로 인해 시장 확대 속도가 더뎌지고 있습니다. 이 격차를 해소하려면 발 및 발목용 기기 시장 전반에 걸쳐 지속 가능한 도입을 보장하기 위한 조직적인 로비 활동과 강력한 비용 효율성 데이터가 필요합니다.

2025년 발 및 발목용 기기 시장 점유율에서 플레이트 부문은 20.68%를 차지했으며, 외상실에서 골절 치료 건수가 주를 이루기 때문에 여전히 매출의 핵심을 이루고 있습니다. 그러나 기반이 더 작았던 발목 치환술 코호트는 9.29%의 연평균 복합 성장률(CAGR)을 기록할 것으로 예상되어 다른 모든 기기 클래스를 앞지를 전망입니다. 9년 생존율이 약 88.3%에 달한다는 지속적인 발표는 외과의사들에게 전체 발목 관절 치환술이 고관절 및 무릎 치환술의 성공을 모방할 수 있다는 확신을 심어주고 있습니다. 엑서텍(Exactech)이 골격골을 모방하도록 설계된 3D 프린팅 경골 임플란트를 출시한 것은 이러한 생체모방 기술로의 전환을 상징합니다. 이 디자인은 조기 고정화를 촉진하여 과거 발목 구성품 수명을 제한했던 미세 운동을 줄이고, 발 및 발목용 기기 시장 전반에 걸친 채택률을 높입니다.

공급업체들은 현재 격자 구조 설계 최적화, 주기적 하중 하의 피로 시험, 골유착을 촉진하는 표면 처리 기술에 연구개발 예산을 집중하고 있습니다. 플레이트 기술도 진화 중으로, 고위험 동반질환 사례에서 관찰된 감염 위험을 억제하기 위해 니티놀 스테이플과 항생제 코팅이 표준 키트에 포함되기 시작했습니다. 하이브리드 플레이트-네일 시스템은 노인성 골절에서 발생하는 복잡한 발목 주위 골절을 해결하여 외상 등록부에 기록된 치료 격차를 해소합니다. 활동적인 은퇴자들이 조기 체중 부하와 골프, 하이킹, 저충격 스포츠로의 빠른 복귀를 요구함에 따라 높은 내구성 지표가 중요합니다. 일반 나사 세트 시장에서는 가격 경쟁이 지속되지만, 프리미엄 발목 교체 시스템은 차별화된 가치를 유지하며 마진을 확보하고 있습니다. 이러한 역학은 재건 임플란트의 수익 기여도를 확대하면서도 발 및 발목용 기기 시장에 플레이트가 제공하는 기존 기반을 훼손하지 않도록 지원합니다.

2025년 발 및 발목용 기기 시장 수익의 35.74%를 북미가 차지합니다. 이는 높은 수술 실시 밀도와 병원, 외래수술센터(ASC) 쌍방에서 선진 임플란트를 상환하는 까다로운 보험 적용 정책에 지지되고 있습니다. 미국은 외상 네트워크가 안정적인 플레이트 수요를 창출하고, 광범위한 당뇨병 관리로 샤르코 재건술 사례가 꾸준히 발생하여 단위 판매에서 압도적인 비중을 차지합니다. 환자 맞춤형 임플란트에 대한 FDA 승인은 종종 글로벌 안전 기준을 설정합니다. 예를 들어 'restor3D Total Talus Replacement'과 같은 기기가 승인되면 다수의 비미국 규제 기관이 해당 결과를 참고하여 후속 심사 주기를 단축합니다. 지역별 교육 프로그램은 해외 연수생들을 유치하여 그들이 자국 시장에 기기 선호도를 전파하게 함으로써, 북미의 세계적 소비 패턴 영향력을 강화합니다.

유럽은 신소재에 대한 증거 생성 속도를 높이는 견고한 임상 연구 인프라를 보유합니다. 독일, 영국, 프랑스는 각각 잘 지원되는 정형외과 등록 시스템을 운영하여 임플란트 생존율을 실시간으로 모니터링하고 외과의들이 적응증을 정교화하는 데 도움을 줍니다. 관절 보존형 솔루션에 대한 환자 옹호는 관절 등록제가 오랫동안 고관절 및 무릎 임플란트 결과를 개선해 온 스칸디나비아 보건 시스템에서 총 발목 관절 치환술의 신속한 채택을 촉진합니다. 유럽의 엄격하지만 투명한 규제 체계는 생체 적합성과 기계적 내구성을 입증한 기업을 보상하며, 점진적 개선과 진정한 혁신적 설계 개선 사이의 경계를 재정의합니다. 이러한 요소들은 안정적인 수익 기반을 유지하면서 생분해성 나사, 항생제 코팅 플레이트, 3D 프린팅 융합 케이지의 선택적 도입을 촉진합니다.

아시아는 가처분 소득 증가와 보험 적용 범위 확대로 선택적 시술량이 증가함에 따라 2026년부터 2031년까지 연평균 9.14%의 성장률을 기록하며 가장 빠른 확장을 보입니다. 중국은 지방 정부 주도의 의약품·의료기기 대량 구매 계획에 정형수술용 하드웨어가 포함되면서 평균 가격은 하락했으나 잠재적 수요층이 확대되며 임플란트 단위 성장에서 선두를 달리고 있습니다. 인도는 서양 환자들을 대상으로 비용 효율적인 발목 관절 치환술을 제공하면서 현지 외과의사들에게 고급 임플란트 시술법을 교육하는 의료 관광의 부양으로 그 뒤를 잇고 있습니다. 그러나 의료기기 기업들은 절약형 소비 습관과 인프라 격차에 맞춰 판매 전략을 조정해야 합니다. 예를 들어 소규모 지역 병원들은 복잡한 수술 도구 트레이를 처리할 수 있는 오토클레이브가 부족한 경우가 많아, 공급사들은 일회용 멸균 세트를 우선적으로 공급합니다. 일본의 PMDA부터 중국의 NMPA, 인도의 CDSCO에 이르는 규제 다양성은 지역별 출시를 복잡하게 만들지만, 규제 조화 노력은 진전을 보이고 있습니다. 이러한 어려움에도 불구하고 인구학적 추세는 아시아가 발 및 발목용 기기 시장의 장기적 확장에 핵심적 역할을 지속할 것임을 보장합니다.

The Foot And Ankle Devices Market was valued at USD 5.12 billion in 2025 and estimated to grow from USD 5.48 billion in 2026 to reach USD 7.73 billion by 2031, at a CAGR of 7.09% during the forecast period (2026-2031).

Growing clinical acceptance of patient-matched 3D-printed implants, rising volumes of outpatient procedures, and continued innovation in fixation materials are expanding both procedure counts and average selling prices. Singular device launches that mimic natural bone architecture are reshaping surgeon expectations, while strong demand linked to sports trauma and diabetes-related complications keeps unit growth steady. Regulatory clearances for customized devices now arrive faster than in the past, encouraging smaller innovators to commercialize niche solutions. Large orthopedic companies are responding by acquiring specialized players so they can offer end-to-end treatment platforms across the ankle and foot devices market.

High-energy ankle fractures in adolescent and adult athletes keep surgical volumes elevated year-round. Surgeons actively stratify patients by comorbidity risk, directing smokers and individuals with chronic obstructive pulmonary disease toward reinforced fixation constructs that resist early failure. Sports medicine programs are also standardizing post-operative weight-bearing protocols, which accelerates the transition from in-hospital recovery to home-based rehabilitation and indirectly boosts higher-margin outpatient device sales. Collectively, these factors strengthen pricing power for next-generation devices designed for rigorous athletic demands across the ankle and foot devices market.

Rising diabetes prevalence drives long-term demand for limb-saving hardware. Diabetic foot ulcers strike 15-25% of all diabetes patients, with treatment outlays that start at USD 8,000 and climb beyond USD 63,100 per case. Clinical follow-up confirms that 34% of diabetic patients face a lifetime risk of ulceration, positioning this comorbidity as a leading cause of non-traumatic amputations in the United States. Specialized locking plates, circular external fixators, and titanium fusion cages that tolerate osteopenic bone are now standard for Charcot reconstructions. Payers increasingly support preventive surgical interventions because data show earlier fixation shortens hospital stays and limits severe infection episodes, feeding steady, long-duration growth for the ankle and foot devices market.

Coverage pathways lag behind the science. Traditional metallic screws and plates benefit from well-defined billing codes, but newer bioresorbable composites incorporating B-tricalcium phosphate lack consistent payer recognition. As a result, surgeons often forgo these implants unless patients have supplemental insurance or self-pay capacity. Hospitals remain cautious because delayed reimbursement jeopardizes razor-thin outpatient margins. Policy uncertainty slows volume ramp-up even though randomized trials confirm that resorbable constructs eliminate later removal procedures and reduce infection risk. Bridging this gap requires coordinated lobbying and robust cost-effectiveness data to ensure sustainable uptake across the ankle and foot devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The plates segment secured 20.68% of the ankle and foot devices market share in 2025 and remains the revenue anchor because fracture repair volumes dominate trauma rooms. However, the ankle replacement cohort, which held a smaller base, is projected to register a 9.29% CAGR, outpacing every other device class. The continued publication of 9-year survivorship rates of nearly 88.3% fuels surgeon confidence that total ankle arthroplasty can emulate hip and knee replacement success. Exactech's roll-out of its 3D-printed tibial implant, built to replicate trabecular bone, embodies this shift toward biomimicry. The design promotes early fixation, reducing micromotion that historically limited ankle component longevity and bolstering adoption rates throughout the ankle and foot devices market.

Suppliers now allocate R&D budgets toward lattice design optimization, fatigue testing under cyclic load, and surface treatments that accelerate osseointegration. Plates still evolve, with nitinol staples and antibiotic coatings entering standard kits to combat infection risk observed in high-risk comorbidity cases. Hybrid plate-nail systems address complex peri-ankle fractures in geriatric bones, closing treatment gaps documented by trauma registries. High durability metrics matter because active retirees demand earlier weight bearing and rapid return to golf, hiking, and low-impact sports. Competitive pricing wars persist in commodity screw sets, but premium ankle replacement systems continue to command margin because they remain differentiated. These dynamics support expanding revenue contribution from reconstruction implants without eroding the established foundation that plates provide to the ankle and foot devices market.

The Foot and Ankle Devices Market Report Segments the Industry Into by Device Type (Ankle Replacement Systems, Plates, Screws and More), Procedure (Osteotomy, Fracture Repair, Fusion / Arthrodesis, Other Procedures), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America contributes 35.74% of the ankle and foot devices market revenue in 2025, anchored by high procedure density and generous coverage policies that reimburse advanced implants in both hospital and ASC settings. The United States drives an outsized share of unit sales because strong trauma networks feed reliable plate demand, and widespread diabetes management creates steady Charcot reconstruction case flow. FDA clearances for patient-specific implants frequently set global safety benchmarks; once the agency approves a device such as the restor3D Total Talus Replacement, many non-US regulators reference those findings, shortening subsequent review cycles. Regional training programs also attract international fellows who carry device preferences back to their home markets, reinforcing North American influence on worldwide consumption patterns.

Europe commands a robust clinical research infrastructure that speeds evidence generation for new biomaterials. Germany, the United Kingdom, and France each maintain well-supported orthopedic registries, enabling real-time surveillance of implant survivorship and helping surgeons refine indications. Patient advocacy for motion-preserving solutions spurs rapid endorsement of total ankle replacements in Scandinavian health systems, where joint registries have long improved outcomes for hip and knee implants. Europe's rigorous but transparent regulatory framework rewards companies that demonstrate biocompatibility and mechanical endurance, pushing the line between incremental and truly novel design improvements. These factors maintain a steady revenue base while stimulating selective adoption of bioresorbable screws, antibiotic-coated plates, and 3D-printed fusion cages.

Asia records the fastest expansion, with an 9.14% CAGR projected from 2026 to 2031 as rising disposable incomes and broader insurance coverage lift elective procedure volumes. China leads implant unit growth after provincial drug-device bulk procurement schemes begin to include orthopedic hardware, lowering average prices yet creating larger addressable populations. India follows, boosted by medical tourism that draws Western patients seeking cost-effective ankle replacement while training local surgeons on premium implants. Nonetheless, medtech firms must tailor sales tactics to frugal spending habits and infrastructure gaps; for instance, small community hospitals often lack autoclaves capable of processing complex instrument trays, prompting suppliers to prioritize single-use sterile sets. Regulatory diversity, stretching from Japan's PMDA to China's NMPA and India's CDSCO, complicates regional launches, though harmonization initiatives show progress. Despite these challenges, demographic momentum ensures Asia remains pivotal to the long-term expansion of the ankle and foot devices market.