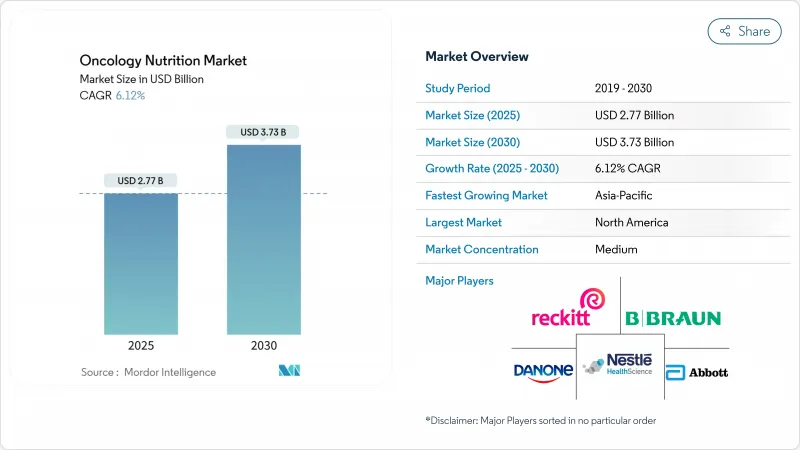

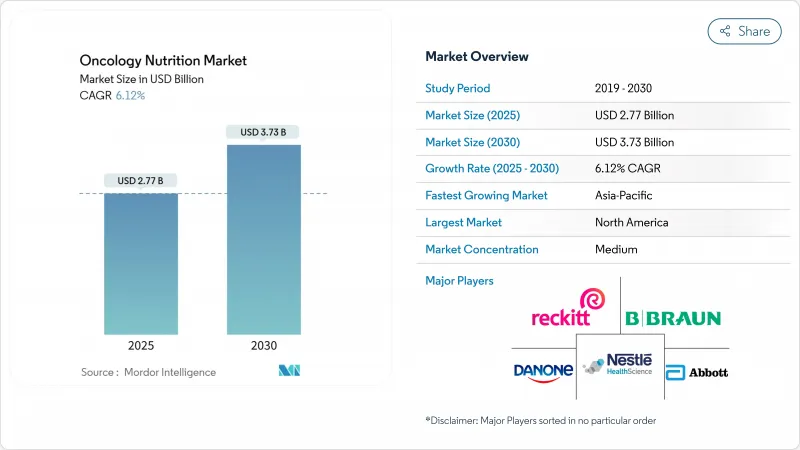

종양 영양 시장은 현재 27억 7,000만 달러로 평가되었고, CAGR은 6.12%를 나타낼 것으로 예측되며 2030년에는 37억 3,000만 달러로 성장할 전망입니다.

이러한 성장 추세는 암 발병률의 동시적 증가, 맞춤형 영양 기술의 주류화, 그리고 서비스 양보다 결과를 중시하는 가정 기반 치료 모델로의 의료 시스템 전환에 기인합니다. 미국에서만 2025년에 200만 건 이상의 신규 암 진단이 예상됨에 따라 수요가 더욱 강화되어, 치료 전 과정에 걸쳐 영양 중심적 중재의 광범위한 채택을 촉진하고 있습니다. 2024년 이미 종양 영양 시장의 71.3%를 차지하는 경장영양은 비경로적 방법에 비해 감염 위험 감소 및 치료 비용 절감에 대한 설득력 있는 임상 증거로 인해 혜택을 보고 있습니다. 두경부암은 심각한 연하곤란 합병증으로 인해 종양 영양 시장의 39.2%라는 압도적인 비중을 차지하는 반면, 혈액암은 CAR-T 세포 치료 지원 수요와 연계된 9.9%의 연평균 복합 성장률(CAGR)을 기록하며 가장 빠른 성장세를 보이고 있습니다. 북미는 50.1%의 매출 점유율을 차지하지만, 아시아태평양 지역은 급속한 의료 인프라 개발과 암 유병률 증가에 힘입어 9.2%의 CAGR로 모든 지역을 앞질렀습니다.

2025년 미국에서 신규 암 진단 건수가 200만 건을 넘어설 것으로 예상되며, 이는 사상 처음으로 해당 기준을 돌파하는 것입니다. 고령화 인구, 비만, 환경적 노출 요인이 계속해서 발병률을 높여 종양 영양을 선택적 지원에서 일선 치료로 전환시키고 있습니다. 자궁내막암, 간암, 유방암 등 과체중 관련 암의 증가 속도가 가장 빠르며, 이는 대사 및 면역 조절 영양 프로토콜에 대한 지속적인 수요를 창출하고 있습니다. 아시아태평양 지역에서는 1990년부터 2019년까지 17가지 암 유형에서 상당한 발병률 증가가 관찰되어 3차 병원 내 영양 부서에 대한 투자를 촉진하고 있습니다. 결과적으로 종양 영양 시장 관계자들은 영양을 주변적 서비스가 아닌 정밀 종양학의 필수 요소로 인식하고 있습니다.

여러 체계적 문헌고찰은 암 치료에서 경장 영양 공급이 비경구 방법 대비 감염 위험이 낮고 유사한 사망률을 보인다는 점을 확인했습니다. 특히 미국 메디케어 프로그램 하의 유리한 보험급여 체계는 경장 제품 쪽으로 균형을 더욱 기울여 공급업체에게 명확한 상업적 성장 기회를 제공합니다. 위장관 기능이 유지될 경우 “경장 우선”을 점점 더 강조하는 업데이트된 임상 지침은 펩타이드 기반 면역 강화 포뮬러 연구개발을 촉진하고 있습니다. 그럼에도 점막염, 폐쇄증 또는 공격적 화학요법을 받는 환자에게는 비경로적 솔루션이 여전히 필수적이어서 해당 틈새시장은 전문 제조사에게 매력적인 영역으로 남아있습니다.

전문 면역 영양제는 표준 포뮬러보다 가격대가 훨씬 높은 경우가 많으며, 이는 높은 연구개발비, 임상시험 비용, 무균 제조 비용을 반영합니다. 신흥국 병원들은 합병증 감소로 인한 장기적 비용 절감 효과에도 불구하고 이러한 비용을 감당하기 어렵습니다. 단백질 가수분해물 프로파일과 미량영양소 혼합물이 특허 및 엄격한 규제 절차로 보호받기 때문에 제네릭 제품 진입이 드물어 프리미엄 가격대가 유지되고 광범위한 채택이 저해되고 있습니다.

두경부 악성 종양은 2024년 매출의 28.5%를 차지하며 종양 영양 시장에서 가장 큰 비중을 보였습니다. 동시 화학방사선 치료를 받는 거의 모든 환자는 연하곤란, 구강건조증 또는 점막염을 겪어 예방적 영양관 삽입과 글루타민 및 오메가-3 지방산이 풍부한 질환 특화 포뮬러가 필요합니다. 결과적으로 두경부 환자군은 임상 도입 동향의 선행지표 역할을 합니다. 혈액암 시장은 연평균 4.93% 성장률로 확대되며, 복잡한 세포 기반 치료와 증가된 영양소 수요 간의 연관성을 부각시킵니다. 혈액학 의료진은 중성구 감소증 기간 동안 장 건강을 최적화하기 위해 엄격한 아미노산 및 프로바이오틱스 프로토콜을 점차 통합하고 있습니다.

위암 및 광범위한 위장관 암은 맞춤형 영양 공급 대상 환자군 중 세 번째로 큰 규모를 형성합니다. 절제술과 흡수장애 증후군은 위 배출을 촉진하는 펩타이드 기반 중쇄 트리글리세라이드(MCT) 영양제의 필요성을 높입니다. 유방암의 발생률과 생존율은 근육 보존 및 대사 지원을 목표로 하는 경구 영양 보충제의 꾸준한 사용을 주도하지만, 해당 부문은 여전히 가격에 민감합니다. 폐암 환자들은 전신 치료와 관련된 이화 작용 손실을 상쇄하기 위해 메스꺼움을 완화하는 고에너지 포뮬러에 의존합니다. 이러한 질병 군집들은 정밀 영양 연구 개발이 이제 종양 생물학과 치료 알고리즘에 어떻게 연결되어 있는지 보여줌으로써, 종양학 영양 시장이 그 자체로 하나의 치료 라인으로 성숙해가고 있음을 강화합니다.

북미는 명확한 보험급여 체계와 확고한 영양 지원 팀을 바탕으로 2024년 매출의 50.1%를 차지했습니다. 메디케어, 메디케이드 및 민간 보험사는 경장영양 및 비경장영양 방식을 보험급여하지만, 외래 환경에서의 경구 보충제에는 공백이 존재합니다. 미국 암 센터들은 증거 기반 프로토콜 준수를 강화하기 위해 실시간 영양 결핍 경보를 EHR에 자동 입력하는 AI 기반 식단 계획 도구를 점점 더 많이 도입하고 있습니다. 캐나다는 의료용 식품에 대해 보편적 보장을 제공하지만 프리미엄 포뮬러에 대한 보상을 제한하여 조달 위원회가 물량 기반 할인을 협상하도록 유도합니다. 멕시코의 중산층 확대와 민간 병원 성장은 중가대 시장 기회를 열어주지만 공공 부문 예산은 여전히 제한적입니다.

아시아태평양 지역은 연평균 9.2% 성장률로 암 영양 시장 최대 성장 지역입니다. 중국 1급 병원들은 공식 영양과 신설을 시작했으며, 국가급여의약품목록에 의료용 식품이 주기적으로 추가되며 접근성이 개선되고 있습니다. 일본은 고령화로 지속적인 수요가 발생하며, 세계 최고 수준의 영양사 밀집도로 정교한 프로토콜이 용이합니다. 인도의 암 부담은 급증하고 있으며, 대도시 지역 암 연구소의 역량 강화로 지역별 입맛 선호도에 맞춘 현지 제조 포뮬러의 채택이 촉진됩니다. 규제 일정은 크게 달라 현지 임상 증거와 유통사 파트너십을 통합한 시장 진출 전략이 필요합니다.

유럽은 ‘유럽 암 퇴치 계획(European Beating Cancer Plan)’ 하에 포괄적 암 치료에 영양 관리를 지속적으로 통합하고 있으나, 회원국별 실행 방식은 상이합니다. 독일과 영국은 입원 시 필수적인 영양실조 검진을 의무화하여 필요한 제품에 대한 보험 적용을 촉발합니다. 프랑스와 이탈리아는 지중해식 식단 원칙을 장려하며, 이는 식물성 포뮬러 트렌드와 부합합니다. 동유럽 시장은 예산 제약으로 뒤처지고 있으나, EU의 국경 간 암 치료 지원 프로그램이 교육 및 조달을 강화하고 있습니다. 지역 전반의 지속가능성 의무화는 식물성 중심 영양제로의 전환을 가속화하며, 탄소 절감 데이터를 제시할 수 있는 공급업체에게 병원 입찰에서 경쟁 우위를 제공합니다.

The oncology nutrition market is currently valued at USD 2.77 billion and is forecast to advance to USD 3.73 billion by 2030, reflecting a 6.12% CAGR.

This growth trajectory is rooted in the simultaneous rise of cancer incidence, the mainstreaming of personalized nutrition technologies, and the healthcare system's shift toward home-based care models that reward outcomes rather than service volume. Demand is reinforced by more than 2 million new cancer diagnoses expected in 2025 in the United States alone, spurring widespread adoption of nutrition-centric interventions throughout the treatment continuum. Enteral nutrition, already responsible for 71.3% of the oncology nutrition market share in 2024, benefits from compelling clinical evidence of reduced infection risk and lower treatment costs compared with parenteral methods. Head and neck cancers hold a dominant 39.2% slice of the oncology nutrition market thanks to severe dysphagia complications, while blood cancers post the fastest expansion, riding a 9.9% CAGR linked to CAR-T cell therapy support needs. North America secures a 50.1% revenue share, but the Asia-Pacific region outpaces all geographies with a 9.2% CAGR, underpinned by rapid healthcare infrastructure development and rising cancer prevalence.

New cancer diagnoses are expected to exceed 2 million cases in the United States in 2025, marking the first time this threshold is crossed. Aging populations, obesity, and environmental exposures continue to lift incidence rates, pushing oncology nutrition from optional support to frontline therapy. Excess-weight-related cancers such as endometrial, liver, and breast malignancies are climbing fastest, creating persistent demand for metabolic and immune-modulating nutrition protocols. In Asia-Pacific, longitudinal data show substantial incidence jumps across 17 types of cancer between 1990 and 2019, driving investments in nutrition departments within tertiary hospitals.As a result, oncology nutrition market stakeholders view nutrition as an indispensable element of precision oncology rather than a peripheral service.

Multiple systematic reviews confirm that enteral feeding confers lower infection risk and similar mortality outcomes versus parenteral methods in cancer care. Favorable reimbursement schedules especially under the United States Medicare program further tilt the balance toward enteral products, offering suppliers a clear commercial runway. Updated clinical guidelines increasingly dictate "enteral first" when the gastrointestinal tract remains functional, sparking R&D in peptide-based, immune-enhancing formulas. Even so, parenteral solutions remain vital for patients facing mucositis, obstruction, or aggressive chemotherapy, keeping that niche attractive for specialized manufacturers.

Specialized immunonutrition often prices well above standard formulas, reflecting elevated R&D, clinical-trial, and aseptic-manufacturing expenses. Hospitals in emerging economies struggle to absorb these costs despite long-term savings from reduced complications. Generic entrants are scarce, as protein hydrolysate profiles and micronutrient blends are protected by patents and stringent regulatory pathways, preserving premium price points and dampening widespread adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Head and neck malignancies generated 28.5% of revenue in 2024, the largest share within the oncology nutrition market. Nearly every patient treated with concurrent chemoradiation endures dysphagia, xerostomia, or mucositis, necessitating prophylactic feeding-tube placement and disease-specific formulas rich in glutamine and omega-3 fatty acids. As a result, the head and neck cohort functions as a bellwether for clinical adoption trends. Blood cancers are expanding at a 4.93% CAGR, underscoring the link between complex cell-based therapies and heightened nutrient demands. Hematology providers increasingly integrate stringent amino-acid and probiotic protocols to optimize gut integrity during neutropenia episodes.

Stomach and broader gastrointestinal cancers collectively form the third-largest pool of candidates for tailored nutrition. Resection procedures and malabsorption syndromes elevate the need for peptide-based, medium-chain triglyceride formulas that accelerate gastric emptying. Breast cancer's incidence and survivorship drive steady use of oral nutritional supplements targeting muscle preservation and metabolic support, though the segment remains price-sensitive. Lung cancer patients lean on nausea-mitigating, high-energy formulas to counter catabolic losses linked to systemic therapy. Together, these disease clusters reveal how precision-nutrition R&D is now tethered to tumor biology and treatment algorithms, reinforcing the oncology nutrition market's maturation into a therapy line in its own right.

The Oncology Nutrition Market Report is Segmented by Cancer Type (Head & Neck Cancer, Stomach & Gastrointestinal Cancers, Blood Cancer, Breast Cancer, and More), Nutrition Type (Enteral Nutrition, Parenteral Nutrition), End-User (Hospitals, Home Care, Specialty Oncology Clinics), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America delivered 50.1% of 2024 revenue, anchored by well-defined reimbursement pathways and entrenched nutrition support teams. Medicare, Medicaid, and private insurers reimburse enteral and parenteral modalities, albeit with gaps for oral supplements in outpatient settings. United States cancer centres increasingly deploy AI-based diet planning tools that populate EHRs with real-time nutrient-gap alerts, strengthening adherence to evidence-based protocols. Canada presents universal coverage for medical foods but caps reimbursement on premium formulas, pushing procurement committees to negotiate volume-based discounts. Mexico's middle-class expansion and private hospital growth open mid-price opportunities, though public-sector budgets remain constrained.

Asia-Pacific is the oncology nutrition market's most dynamic geography, forecast at a 9.2% CAGR. China's tier-1 hospitals have begun incorporating formal nutrition departments, while its National Reimbursement Drug List periodically adds medical foods, lifting access. Japan's aging population drives sustained demand, with dietitian density among the world's highest, facilitating sophisticated protocols. India's oncology burden rises sharply, and capacity building in metro-region cancer institutes fosters uptake of locally manufactured formulas tailored to regional palate preferences. Regulatory timelines vary widely, requiring go-to-market strategies that integrate local clinical evidence and distributor partnerships.

Europe continues to embed nutrition into comprehensive cancer care under the European Beating Cancer Plan, yet execution differs by member state. Germany and the United Kingdom adopt mandatory malnutrition screening upon hospital admission, triggering reimbursement for necessary products. France and Italy promote Mediterranean diet principles, dovetailing with the plant-based formula trend. Eastern European markets lag due to budgetary constraints, but EU funding programs for cross-border cancer care bolster training and procurement. Sustainability mandates across the region accelerate conversion to plant-forward formulas, giving suppliers who can articulate carbon-savings data a competitive edge in hospital tenders.