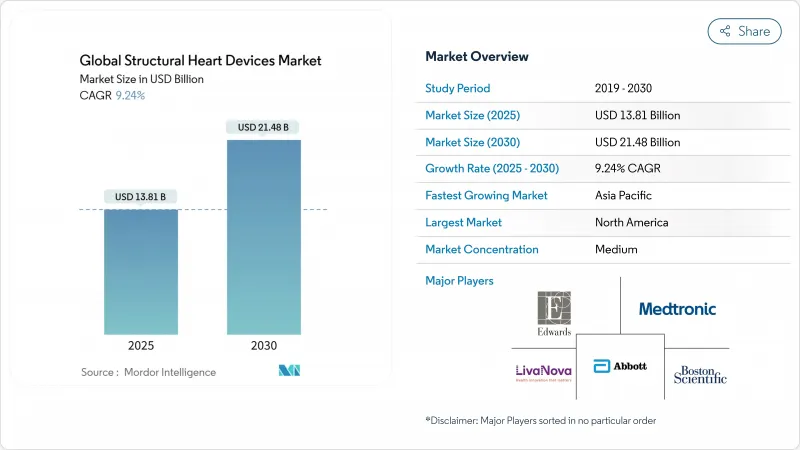

구조적 심장질환 기기 시장 규모는 2025년에 138억 1,000만 달러로 평가되었고, 2030년에 214억 8,000만 달러에 이를 것으로 예측되며, CAGR은 9.24%를 나타낼 전망입니다.

경피적 대동맥판막 교체술(TAVR)에 대한 견고한 수요, 저위험군 환자에 대한 광범위한 보험 적용 확대, 지속적인 기기 업그레이드가 단기 성장 전망을 높이고 있습니다. 전달 시스템을 단순화하는 제품 출시, 외래 수술 센터에서의 시술량 증가, 폴리머 프리 니티놀 프레임의 등장 또한 임상적 채택을 확대하고 있습니다. 기존 공급업체들이 승모판 및 삼첨판 제품군 확장에 박차를 가하는 한편, 지역 업체들은 가격 경쟁력을 바탕으로 신흥 아시아 시장에 진출하며 경쟁이 치열해지고 있습니다. 숙련된 중재적 심장 전문의의 지속적인 부족과 하이브리드 카테터실/수술실의 높은 자본 비용이 전반적인 성장세를 다소 억제하고 있으나, 구조적 심장질환 기기 시장은 여전히 견고한 확장 궤도를 유지하고 있습니다.

선진국 경제에서 기대 수명이 길어짐에 따라 석회화 대동맥 협착증 및 기능성 승모판 역류증의 위험군도 확대되었습니다. 최근 등록 데이터 업데이트에 따르면 75세 이상 환자에서의 시술 건수가 증가하고 있어 장기적 수요 곡선을 강화하고 있습니다. EARLY TAVR 임상시험의 조기 개입 증거는 무증상 중증 대동맥 협착증을 증상 발현 전에 치료할 경우 재입원률이 20% 감소함을 보여주어 잠재적 대상 환자군을 확대하고 있습니다.

저위험군 환자에 대한 5년 추적 관찰 결과 TAVR과 수술 간 전원 사망률이 유사함을 확인하여 보험사와 의료진의 신뢰도를 높였습니다. 이에 따라 상업적 초점은 판막 내구성, 판막 주변 누출 감소, 혈역학적 성능으로 전환되었습니다. 에드워즈가 약 60%의 점유율을 유지하고 있으며, 메드트로닉이 28%를 차지하고 있습니다. 애보트와 같은 신규 진입업체들은 네비터 시스템으로 입지를 넓히며 차별화 경쟁을 가속화하고 있습니다.

류마티스성 심장병은 아시아와 아프리카 저소득 지역에서 여전히 흔하나, 시술 역량은 대도시 중심지에 집중되어 있습니다. 복잡한 경피적 승모판 교체술은 신속한 확장이 불가능한 광범위한 프로크터링(지도)을 요구합니다. 업계 교육 협력은 진행 중이지만, 잠재 수요가 가장 높은 지역에서 공급 격차는 도입 모멘텀을 계속 저해하고 있습니다.

심장 판막 장치는 2024년 매출의 60.0%를 차지하며 구조적 심장질환 기기 시장에서 핵심 역할을 확인했습니다. TAVR의 전 세계 매출은 미국에서 연간 10.0% 성장에 힘입어 70억 달러에 근접하고 있습니다. 밸브 개발사들은 장기 내구성을 향상시키는 저프로파일 전달 기술, 항석회화 판막, 그리고 심방판막 접합부 정렬 기술에 주력하고 있습니다. 밸브 플랫폼의 구조적 심장질환 기기 시장 규모는 2025년 CE 인증을 획득한 최초의 경대퇴동맥 경유 승모판 교체 시스템인 Edwards SAPIEN M3와 같은 차세대 시스템의 출시와 함께 동조하여 성장할 것으로 전망됩니다.

폐쇄 장치 및 전달 시스템은 특히 뇌졸중 예방 분야에서 시술 적용이 급속히 확대되고 있습니다. 애보트의 WATCHMAN FLX 포트폴리오는 피벗 준비 프레임과 완전 원주 밀봉으로 시술자의 신뢰를 지속적으로 얻고 있습니다. 외래환자 보험급여 확대가 판매 성장을 가속화하며, 폐쇄 장치는 경피적 수리 솔루션 내 가장 빠르게 성장하는 하위 카테고리가 되었습니다. 새로운 폴리머 프리 니티놀 제품들은 더욱 짧은 입원 기간을 약속하며, 이차 예방 대상 환자군 전반에 걸쳐 채택률 상승에 추가적인 압력을 가하고 있습니다. 이러한 추세들은 종합적으로 구조적 심장질환 기기 시장을 높은 한 자릿수 성장 궤도에 유지시키고 있습니다.

북미는 2024년 전 세계 매출의 40.0%를 차지했으며, 이는 전 세계 TAVR 이식 수술의 절반 이상을 수행하고 연간 약 10.0%의 시술 증가율을 유지하는 미국이 주도했습니다. CMS 보장 범위 확대와 ASC(외래 수술 센터) 보급 확대로 인해 경피적 수리 시술 건수는 지속적인 두 자릿수 성장을 보이고 있습니다. 캐나다의 승모판 클립 시술에 대한 보험급여 개혁은 2027년까지 점진적인 상승 여력을 더합니다.

유럽은 가치 기준으로 2위를 차지하며, 중앙 집중식 조달과 범지역적 CE 인증 덕분에 신기술을 신속하게 도입하고 있습니다. 2025년 4월 SAPIEN M3의 CE 마크 획득은 대퇴동맥 경유 승모판 솔루션의 초기 상용화 허브로서 유럽의 역할을 부각시킵니다. 독일과 프랑스의 병원 네트워크는 클립 시술실을 확대하고 환자를 최소 침습적 경로로 분류함으로써, 인구 고령화로 인한 정체에도 불구하고 유럽 구조적 심장질환 기기 시장 규모가 중간 단일 자릿수 성장을 유지하도록 지원하고 있습니다.

아시아태평양 지역은 중국, 호주, 인도의 시술량 증가로 2030년까지 11.1%의 가장 빠른 연평균 복합 성장률(CAGR)을 기록할 전망입니다. 2024년 1,240만 달러에 불과했던 인도의 구조적 심장 부문은 국내 OEM 기업과 2차 민간 병원의 카테실 확장 추진으로 31% CAGR을 달성할 것으로 예상됩니다. 다양한 질병 프로필은 농촌 지역의 류마티스성 관련 승모판 수리 수요부터 도시 중심부의 퇴행성 대동맥 협착증에 이르기까지 차별화된 시장 진출 전략을 요구하는 다양한 임상적 우선순위를 창출합니다. 일본의 고령화 인구는 꾸준한 TAVR 성장을 지속적으로 뒷받침하는 반면, 한국의 3차 의료기관들은 승모판 중재술을 위한 AI 기반 크기 측정 기술을 시범 운영 중입니다.

The structural heart devices market size stands at USD 13.81 billion in 2025 and is forecast to reach USD 21.48 billion by 2030, reflecting a 9.24% CAGR.

Robust demand for transcatheter aortic valve replacement (TAVR), wider reimbursement for low-risk patients, and continuous device upgrades lift near-term growth prospects. Product launches that simplify delivery systems, rising procedure volumes in ambulatory surgical centers, and the entry of polymer-free nitinol frames also widen clinical adoption. Competition is sharpening as established suppliers race to expand mitral and tricuspid portfolios, while regional players use price advantages to penetrate emerging Asian markets. Persistent shortages of skilled interventional cardiologists and high capital costs for hybrid cath-lab/OR suites temper the overall trajectory, yet the structural heart devices market remains on a solid expansion path.

Longer life expectancy in developed economies has expanded the at-risk pool for calcific aortic stenosis and functional mitral regurgitation. Recent registry updates show escalating procedure volumes in patients aged >=75 years, reinforcing a long-run demand curve. Early-intervention evidence from the EARLY TAVR trial indicates a 20% reduction in rehospitalizations when asymptomatic severe aortic stenosis is treated before symptom onset, broadening the potential candidate base.

Five-year follow-up of low-risk patients confirms comparable all-cause mortality between TAVR and surgery, accelerating payer and clinician confidence. Commercial focus has therefore moved to valve durability, paravalvular leak reduction, and hemodynamic performance. Edwards maintains roughly 60% share, Medtronic 28%, and newer entrants such as Abbott are gaining traction with the Navitor system, intensifying differentiation battles.

Rheumatic heart disease remains common in lower-income parts of Asia and Africa, yet procedure capacity is locked in metropolitan hubs. Complex transcatheter mitral replacement requires extensive proctoring that cannot be scaled quickly. Industry training collaborations are underway, but the supply gap continues to dampen adoption momentum in regions with the highest latent demand.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Heart valve devices captured 60.0% of 2024 revenue, confirming their anchor role in the structural heart devices market. TAVR's worldwide revenue is approaching USD 7.0 billion, supported by 10.0% annual growth in the United States. Valve developers focus on lower profile delivery, anti-calcification leaflets, and commissural alignment technologies that improve long-term durability. The structural heart devices market size for valve platforms is projected to advance in lockstep with the rollout of next-generation systems such as Edwards SAPIEN M3, the first transfemoral mitral replacement to secure a CE Mark in 2025.

Occluders and delivery systems are witnessing rapid procedural expansion, particularly in stroke-prevention applications. Abbott's WATCHMAN FLX portfolio continues to gain operator confidence due to pivot-ready frames and full-circumference sealing. Sales growth is amplified by favorable outpatient reimbursement, making occluders the quickest expanding sub-category within transcatheter repair solutions. New polymer-free nitinol iterations promise even shorter in-hospital stays, placing additional upward pressure on adoption curves across secondary prevention populations. Collectively, these trends maintain the structural heart devices market on its high-single-digit trajectory.

The Structural Heart Devices Market Report is Segmented by Product (Heart Valve Devices, Occluders & Delivery Systems, Annuloplasty & Support Rings, and More), Procedure (Replacement Procedures and Repair Procedures), End User (Hospitals & Cardiac Centers, Ambulatory Surgical Centers, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 40.0% of global revenue in 2024, anchored by the United States, which performs more than half of all TAVR implants worldwide and maintains roughly 10.0% annual procedure growth. CMS coverage expansion and ASC penetration underpin continued double-digit growth in transcatheter repair volumes. Canadian reimbursement reforms for mitral clip procedures add incremental upside through 2027.

Europe ranks second in value and adopts new technologies swiftly because of centralized procurement and pan-regional CE approvals. The April 2025 CE Mark of the SAPIEN M3 highlights the region's role as an early commercialization hub for transfemoral mitral solutions. Hospital networks in Germany and France are broadening clip labs and triaging patients into minimally invasive pathways, helping the structural heart devices market size in Europe maintain mid-single-digit growth despite demographic plateauing.

Asia-Pacific posts the fastest CAGR at 11.1% through 2030 as procedure volumes accelerate in China, Australia, and India. India's structural heart segment, only USD 12.4 million in 2024, is on track for 31% CAGR, driven by domestic OEMs and tier-two private hospitals expanding cath-lab capacity. Diverse disease profiles create varied clinical priorities, from rheumatic-related mitral repair demand in rural areas to degenerative aortic stenosis in urban centers, requiring differentiated go-to-market strategies. Japan's aging population continues to underpin steady TAVR growth, while South-Korean tertiary centers pilot AI-guided sizing for mitral interventions.