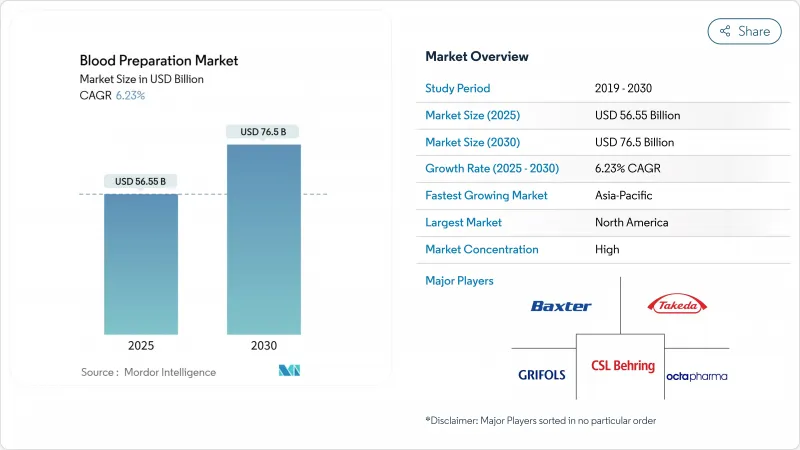

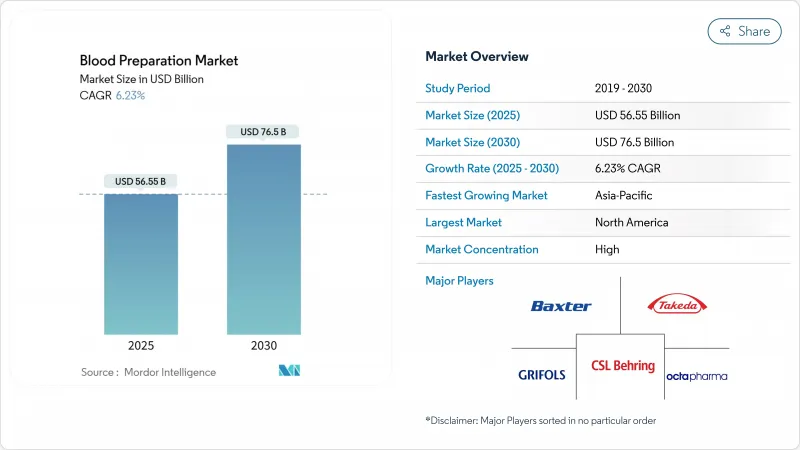

혈액제제 시장 규모는 2025년에 565억 5,000만 달러로 추정되고, 2030년에는 765억 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 6.23%로 성장할 전망입니다.

이 궤도는 자동 성분 분리의 채용 확대, 병원체 삭감 플랫폼의 보급, 수혈 수요를 높이는 수술량의 꾸준한 증가에 의해 지지되고 있습니다. 혈장 유래의 치료제, 특히 면역글로불린의 동시적인 확장은 정밀의료 및 만성 질환 관리에 대한 움직임을 뒷받침합니다. 혈장 분획자 간 통합은 리터당 비용을 낮추고 공급의 탄력성을 향상시키는 반면, 인자 XI 억제제와 같은 새로운 항응고제 부류는 임상 이용 사례를 넓히고 있습니다. 지역별로는 북미의 견고한 규제 프레임워크과 아시아태평양의 생산 능력 증강이, 혈액제제 시장의 장기적인 성장을 지지하는 균형 잡힌 수급 다이나미즘을 창출하고 있습니다.

2025년에는 선택적 수술과 외상 관련 수술이 회복되어 적혈구 농축 제제와 혈장 성분 수요를 끌어올렸습니다. 미국 병원에서는 정형외과 수술 건수가 전년 대비 8% 증가하여 성분 보존과 신속형 검사의 업그레이드를 촉구하고 있습니다. 비슷한 기세는 서유럽에서도 볼 수 있으며, 저침습 기술에 의해 외래 수술이 장려되고 있지만, 여전히 수술 전 혈액 적합이 필요합니다. 자동 교차 매칭 분석기와 디지털 혈액 은행 소프트웨어는 턴어라운드 시간을 단축하고 모든 헌혈 단위 이용률을 향상시킵니다. 이러한 개발은 혈액제제 시장의 수익 전망을 강화합니다.

만성 신장병, 혈액암, 혈우병은 아시아태평양에서 증가의 일로를 걷고 있으며, 혈장 유래의 면역글로불린이나 응고 인자의 정기적인 수요가 확대되고 있습니다. 중국과 인도에서는 정부의 상환 목록에 피하 면역글로불린 요법이 포함되어 환자에 대한 접근이 가속화되고 있습니다. 다국적 기업은 분획 라인과 도너 센터의 증설로 대응하고, 국내 기업은 기술 이전을 위해 제휴하고 있습니다. 광범위한 질병 부담은 혈액제제의 장기적인 수요를 확보하고 혈액제제 시장의 지속적인 성장을 뒷받침하고 있습니다.

우간다 조사에서 기증자의 수혈 감염의 유병률은 13.8%로 HBV와 HCV가 특히 높다고 보고되었습니다. 병원체 감소 시스템은 말라리아 감염의 위험을 87% 줄이지만, 예산 제한은 위협이 가장 큰 곳에서의 채용을 방해합니다. 국제 공여 기관은 파일럿 프로그램에 자금을 제공하고 있지만, 그 확장성은 감염 증가에 뒤처져 있습니다. 이 지속적인 격차는 저렴한 멸균의 필요성을 강조하고 혈액제제 시장의 절대 성장을 억제합니다.

혈액 유도체는 2024년 매출의 48.45%를 차지했으며, 면역글로불린과 응고 인자의 왕성한 수요에 지지되고 있습니다. 폐색전증 분야는 2024년 시장 세분화에서 27.56%의 점유율을 차지했으며, 급성기에서 유도체 소비를 지원하고 있습니다. CSL 베린은 면역글로불린의 매출을 20% 늘렸는데, 이는 리터당 혈장 채취 비용이 22% 감소한 것으로 기여하고 있으며, 대규모 분획 시설이 유리한 스케일 메리트를 나타내고 있습니다. Reveos와 같은 자동화 시스템이 혈액 성분 CAGR을 8.56% 밀어 올려 단위당 혈소판과 적혈구 수율을 높여 낭비를 줄이고 과냉각 보존에 의해 보존 기간을 42일에서 63일로 연장했습니다. 병원에서의 성분별 수혈 프로토콜 채용 증가가 혈액제제 시장의 확대를 지지하고 있습니다.

파생상품 파이프라인은 여전히 호조입니다. 그리포르스는 FDA 승인 후 7년간 Yimmugo의 누적 매출액 10억 달러를 전망하고 있습니다. 유럽 정부는 2030년까지 알부민의 자급률 80% 달성을 목표로 하고 있으며, 국내 분획 수탁 제조 프로그램을 자극하고 있습니다. 전혈 로봇 공학과 인공 대체물의 병행 진보는 장기적인 선택을 제공하지만 기존 유도체를 대체하는 데는 시간이 걸릴 것으로 보입니다. 그 결과, 성분의 혁신이 혈액제제 시장의 효율성과 수익성을 높여도 유도체가 주도권을 유지하게 됩니다.

항응고제는 2024년 매출의 61.45%를 차지했으며, 임상 지침의 정착과 의사의 정통도를 반영하고 있습니다. 인자 XI 억제제인 아베라시맙은 심방세동의 임상시험에서 리버록사반에 대한 출혈을 67% 감소시켜 혈소판응집 억제제의 CAGR 8.73% 성장을 가속했습니다. 아픽사반은 호주에서 가장 처방된 경구 항응고제로 지속되었으며, 2024년에는 의료 시스템에 5억 달러의 손실을 가져왔습니다. 폐색전증은 시장 세분화에서 27.56%의 점유율을 차지했으며, 응급 및 만성 질환 영역에서 항응고제의 처방량이 증가했습니다.

4인자 프로트롬빈 농축 제제는 심장 수술 중 동결 혈장을 대체하여 대출혈을 50% 가까이 감소시킵니다. 선용약은 안정적인 수요를 유지하고 있지만, 주입 시간을 단축하는 유전자 재조합형 지혈약과의 경쟁이 격화되고 있습니다. XI인자 제제가 후기 개발 단계에 들어가고 처방 패턴이 변할 수 있지만, 항응고제는 예측 기간 동안 계속 혈액제제 시장의 수익의 기둥이 될 것으로 보입니다.

북미는 2024년 매출의 38.54%를 차지했으며, 350개의 CSL 혈장 기증자 센터와 헌혈 시간을 15분 단축하는 리카 수집 시스템의 급속한 보급에 힘입었습니다. 2025년에는 혈액에 특화된 5가지 지침서가 예정되어 있으며, 이 지역의 정교한 규제 과제가 기술의 승인과 채용을 가속화하고 있습니다. 미국 적십자사는 2024년 7월 폭염과 폭풍우로 재고가 25% 감소했습니다.

아시아태평양의 CAGR은 7.56%로 가장 높습니다. 테르모의 1,500만 달러를 투입한 항저우 공장은 현지 생산을 강화하고 인도네시아의 혈장 분획 프로젝트는 지역의 자급자족을 가속시킵니다. 나라현립 의과대학의 일본 인공혈액 프로그램은 2년간의 보존 기간과 보편적인 적합성으로 인해 긴급 수혈에 혁명을 일으킬 수 있습니다.

유럽은 200만 명의 공여자 추가와 회원국 공통의 품질 기준을 요구하는 새로운 SoHO 규정 하에서 자율성에 중점을 둡니다. 영국은 2025년까지 면역글로불린 자급률 25%를 목표로 하고 있습니다. 네덜란드에서 Sankin의 자동화 처리를 채택하면 기술이 증가하는 헌혈에 대한 의존도를 줄일 수 있는 방법을 보여줍니다. 이러한 지리적 역학은 혈액제제 시장의 균형 잡힌 세계적 전망을 강화합니다.

The blood preparation market size was valued at USD 56.55 billion in 2025 and is forecast to reach USD 76.50 billion by 2030, registering a 6.23% CAGR during the period.

This trajectory is supported by the growing adoption of automated component separation, the spread of pathogen-reduction platforms, and steady growth in surgical volumes that elevate transfusion demand. Parallel expansion in plasma-derived therapeutics, especially immunoglobulins, underscores a move toward precision medicine and chronic-disease management. Consolidation among plasma fractionators is lowering cost per liter and improving supply resilience, while new anticoagulant classes such as factor XI inhibitors are widening clinical use cases. Across regions, robust regulatory frameworks in North America and capacity build-outs in Asia-Pacific create a balanced demand-supply dynamic that sustains long-term growth for the blood preparation market.

Elective and trauma-related surgeries are rebounding in 2025, boosting demand for red-cell concentrates and plasma components. Hospitals in the United States increased orthopedic procedure counts by 8% year-on-year, prompting upgrades in component storage and rapid-type testing. Similar momentum is visible in Western Europe, where minimally invasive techniques encourage outpatient surgeries that still require pre-operative blood matching. Automated cross-matching analyzers and digital blood-bank software shorten turnaround times, improving utilization rates for every donated unit. These developments strengthen revenue visibility for the blood preparation market.

Chronic kidney disease, hematologic cancers, and hemophilia continue to rise across Asia-Pacific, expanding recurring demand for plasma-derived immunoglobulins and coagulation factors. Government reimbursement lists in China and India now include subcutaneous immunoglobulin therapy, accelerating patient access. Multinationals respond by adding fractionation lines and donor centers, while domestic firms partner for technology transfer. The broad disease burden ensures long-term pull for blood derivatives, reinforcing sustainable growth for the blood preparation market.

Studies in Uganda reported 13.8% prevalence of transfusion-transmitted infections among donors, with HBV and HCV notably high. While pathogen-reduction systems cut malaria transmission risk by 87%, budget limitations hinder adoption where the threat is greatest. International-donor agencies fund pilot programs, yet scalability lags behind infection growth. The persistent gap emphasizes the need for affordable sterilization, tempering absolute growth of the blood preparation market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Blood derivatives held 48.45% of 2024 revenue, anchored by strong immunoglobulin and coagulation factor demand. The pulmonary embolism segment accounted for 27.56% share of the blood preparation market size in 2024, supporting derivative consumption in acute settings. CSL Behring logged 20% sales growth for immunoglobulins, aided by a 22% drop in plasma collection cost per liter, illustrating scale economics that favor large fractionators. Automated systems such as Reveos drive 8.56% CAGR for blood components, delivering higher platelet and red-cell yields per unit, lowering wastage, and extending storage times from 42 to 63 days through super-cooling preservation. Increasing hospital adoption of component-specific transfusion protocols sustains this expansion for the blood preparation market.

The derivatives pipeline remains buoyant. Grifols projects USD 1 billion cumulative sales for Yimmugo over seven years post-FDA approval. European governments aim to reach 80% self-sufficiency in albumin by 2030, stimulating domestic contract fractionation programs. Parallel advances in whole-blood robotics and artificial substitutes offer long-range alternatives but will take time to displace established derivatives. Consequently, derivatives retain leadership even as component innovation elevates the efficiency and profitability of the blood preparation market.

Anticoagulants represented 61.45% of 2024 revenue, reflecting entrenched clinical guidelines and physician familiarity. Abelacimab, a factor XI inhibitor, reduced bleeding by 67% versus rivaroxaban in atrial-fibrillation trials, propelling platelet-aggregation inhibitor growth at an 8.73% CAGR. Apixaban remained Australia's most prescribed oral anticoagulant, costing the health system USD 500 million in 2024. The pulmonary embolism segment captured 27.56% share of the blood preparation market, reinforcing anticoagulant volumes across emergency and chronic settings.

Four-factor prothrombin complex concentrate is displacing frozen plasma during cardiac surgery, lowering major bleeding by nearly 50%. Fibrinolytics hold steady demand but face increasing competition from recombinant hemostatic drugs that shorten infusion times. As factor XI agents enter late-stage development, prescribing patterns may pivot, but established anticoagulants will continue to anchor revenue for the blood preparation market during the forecast horizon.

The Blood Preparation Market Report is Segmented by Product Type (Whole Blood, Blood Components, and Blood Derivatives), Blood Thinning Agents (Anticoagulants, and More), Application (Thrombocytosis, and More), End User (Hospitals & Surgical Centers, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.54% of 2024 revenue, underpinned by 350 CSL Plasma donor centers and rapid uptake of the Rika collection system, which cuts donation time by 15 minutes. The region's elaborate regulatory agenda, with five blood-focused guidance documents slated for 2025, accelerates technology approval and adoption. Yet climate disruptions dent supply: the American Red Cross saw a 25% inventory drop in July 2024 during extreme heat and storms.

Asia-Pacific registers the highest 7.56% CAGR. Terumo's USD 15 million Hangzhou plant enhances local production, while Indonesia's plasma-fractionation project fast-tracks regional self-sufficiency. Japan's artificial-blood program at Nara Medical University could revolutionize emergency transfusion with two-year shelf life and universal compatibility.

Europe focuses on autonomy under the new SoHO regulation, requiring 2 million extra donors and common quality standards across member states. The United Kingdom is on track for 25% immunoglobulin self-sufficiency by 2025, aided by domestic fractionation contracts gov.uk. Sanquin's adoption of automated processing in the Netherlands demonstrates how technology reduces dependence on incremental donations. These geographic dynamics collectively reinforce a balanced global outlook for the blood preparation market.