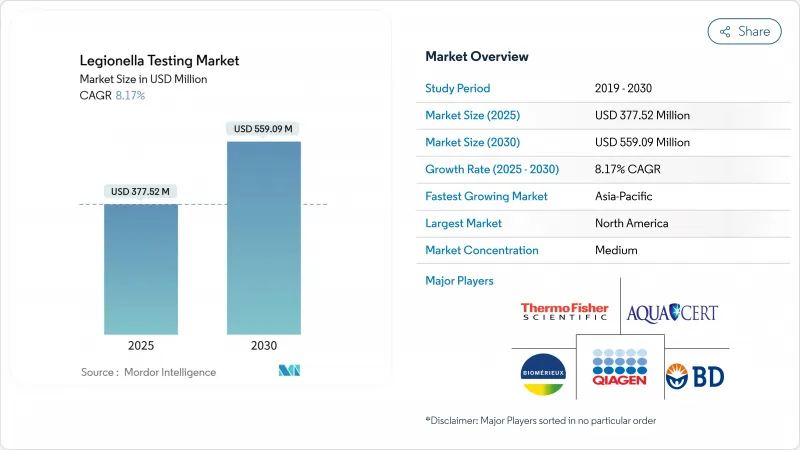

레지오넬라 검사 시장 규모는 2025년에 3억 7,752만 달러로 평가되었고, 2030년에는 5억 5,909만 달러에 이를 것으로 예측되며, CAGR은 8.17%를 나타낼 전망입니다.

건물 내 수질 규제가 강화되고, 팬데믹 이후 경계심이 높아지며, 분자 진단 기술이 급속히 발전함에 따라 두 자릿수 수요 증가세가 지속되고 있습니다. 메디케어 자금 지원을 ASHRAE 준수 수질 관리 프로그램 시행과 연계하는 의무적 CMS 규정은 병원 및 장기 요양 시설이 지속적인 검사 주기를 유지하도록 합니다. 증가하는 법적 책임과 보험 규정으로 인해 이러한 준수 의식이 호텔, 상업용 부동산, 제조 시설로 확대되었습니다. PCR 플랫폼으로의 기술 전환은 결과 도출 시간을 7-14일에서 48시간 미만으로 단축시켜 발병 규모를 제한하는 조기 개입 프로토콜을 가능하게 합니다.

미국에서 보고된 레지오넬라증 사례는 2000년부터 2011년까지 3배 증가했으며, 2024년까지 계속 상승세를 보였는데, 이는 여러 OECD 국가에서도 유사한 패턴을 보였습니다. 2024년 멜버른 발병 사례는 77건의 확진, 75건의 입원, 2명의 사망자를 발생시켜 오염된 에어로졸이 밀집된 도시 인구를 얼마나 빠르게 감염시킬 수 있는지 보여줍니다. 중증 사례의 사망률이 20-40%에 달함에 따라 의료 시스템은 정기적 감시가 전체 치료 비용을 낮춘다는 점을 인식하고 있습니다. 고용주 역시 예방적 검사가 직원의 질병을 방지함으로써 생산성 절감 효과를 얻습니다. 결과적으로 지속적인 역학적 압박은 임상 및 환경 검사에 대한 기본 수요로 이어지고 있습니다.

임상의들은 24시간 내 실행 가능한 결과를 요구합니다. 배양 검사의 7-14일 지연은 중증 폐렴 관리에 임상적으로 용납되지 않는 수준으로 인식됩니다. PCR 플랫폼은 임상적 유의한 기준에서 99.95%의 음성 예측값을 가진 당일 결과를 제공합니다. 코로나19 이후 시설 재개방 시 정체된 배관이 세균 증식을 촉진하는 사례가 드러나면서 신속 분자 패널 도입이 가속화되었습니다. 환경 관리자들 역시 신속 검사를 선호하여 세균 수치가 규제 한도를 초과하기 전에 소독 프로토콜을 조정할 수 있습니다. 따라서 48시간 미만의 처리 시간 요구는 레지오넬라 검사 시장의 핵심 특징으로 남아 있습니다.

배양 검사는 검체 유형에 따라 70-90%의 민감도를 보이며, 비레지오넬라 세균이 배지를 과도하게 증식할 경우 재채취가 필요합니다. 요로 항원 검사는 L. pneumophila 혈청군 1형만 검출하여 다른 혈청군에 의한 8-30%의 사례를 놓칩니다. 검출 누락은 지속적인 노출과 잠재적 소송 위험을 초래하지만, 예산이 제한된 시설들은 여전히 이러한 구식 방법을 선택합니다. 따라서 기존 검사에 대한 광범위한 의존은 더 빠르고 광범위한 스펙트럼의 진단법으로의 보편적 전환을 지연시킵니다.

PCR/qPCR/ddPCR 플랫폼은 2024년 레지오넬라 검사 시장 점유율의 42.76%를 차지했는데, 이는 병원이 중증 폐렴 치료 시 24시간 내 결과 제공을 중요시하기 때문입니다. 2025년 3억 7,752만 달러 규모로 기록된 레지오넬라 검사 시장 내에서 PCR 검사는 높은 민감도와 광범위한 혈청형 커버리지를 결합하여 가장 큰 매출 비중을 차지했습니다. 실험실들은 또한 배양보다 빠르게 수처리 효과를 검증하기 위해 분자적 방법에 의존합니다. 배양은 생존력 확인 및 항생제 감수성 평가에 여전히 필수적이지만, 그 사용은 일선 검사보다는 확인 검사로 전환되고 있습니다. 직접 형광 항체 염색법은 즉각적인 시각화 니치를 채우지만 매출 기여도는 미미합니다. 요로 항원 검사는 응급실 분류 결정을 지원하는 15분 내 현장진단 결과를 제공하며 10.56%의 연평균 성장률(CAGR)로 시장을 주도하고 있습니다. 기술 개선으로 요로 항원 검사의 민감도는 95%를 넘어섰으며, 다중 검출 버전은 이제 단일 카트리지로 여러 레지오넬라 종을 동시에 검출합니다. 시약 비용이 하락함에 따라 요로 항원 검사 키트는 직업 건강 프로그램과 크루즈선 의료 부서에 확산되고 있습니다. 따라서 시장 참여자들은 다양한 최종 사용자 예산 범위를 최대한 커버하기 위해 신속 분자 검사와 분산형 항원 검사 양식을 모두 아우르는 균형 잡힌 포트폴리오를 유지하고 있습니다.

2세대 ddPCR 기기는 대규모 배관 시스템에서 검출 한계 미만의 콜로니 수를 식별함으로써 배양 검사의 시장 점유율을 더욱 잠식할 것으로 예상됩니다. 휴대용 LAMP-측류 키트를 갖춘 현장 기술자는 이제 정기 유지보수 방문 시 스파 물을 검사할 수 있어 HVAC 및 수처리 계약업체에게 새로운 수익원을 창출하고 있습니다. 시약 가격은 여전히 한천 배지보다 높지만, 대량 구매 및 시약 임대 계약으로 격차가 좁혀지고 있으며, 특히 주당 수천 건의 검체를 처리하는 지역 기준 실험실에서 두드러집니다. 예측 기간 동안 기술 융합으로 실험실들은 단일 워크플로우 내에서 ddPCR 정량화와 배양 확인을 결합할 것으로 예상되며, 이는 레지오넬라 검사 시장 전반에 걸쳐 분자 검사의 우위를 공고히 할 것입니다.

북미는 2024년 전 세계 매출의 43.43%를 차지했으며, 이는 의료 분야 CMS 규정, 작업장 OSHA 지침, 상업용 부동산 소유주를 대상으로 한 보험사 주도 감사 등 강력한 규제 네트워크에 기반을 두고 있습니다. 미국에 본사를 둔 대형 진단 기업들이 대부분의 PCR 시약을 공급하며, 수백 개의 인증 실험실이 당일 검사 물류 서비스를 제공합니다. 캐나다 공중보건 기관들은 미국 기준을 반영하고 있으며, 멕시코의 민간 병원 확장은 이에 맞춰 조달 정책을 조정 중입니다. 높은 소송 위험도 의료비 전반적 압박 속에서도 정기 검사 예산을 유지하게 합니다.

아시아태평양 지역은 도시화와 인프라 투자에 힘입어 연평균 9.34% 성장률로 가장 빠르게 성장하는 지역입니다. 일본 2025 엑스포에서는 안전 기준의 50배에 달하는 레지오넬라균 수치가 검출되어 전국적인 인식 제고 캠페인과 더 엄격한 지방자치단체 규정이 시행되었습니다. 중국의 병원 건설 붐과 인도의 민관협력(PPP) 병원 프로젝트는 분기별 검사를 포함한 포괄적인 수질 안전 계획을 필수로 합니다. 홍콩의 냉각탑 감시 체계는 2024년 7월 한 달 동안만 115개 샘플을 분석하며 정부 주도의 경계 태세를 보여줍니다. 호주 주 보건 당국은 월간 냉각탑 점검을 지속적으로 시행하며 동남아시아 이웃 국가들에게 준수 사례를 제시하고 있습니다.

유럽은 국가별 법률과 에너지 절약 목표의 차이로 인해 분열된 양상을 보입니다. 독일의 높은 레지오넬라증 발생률은 실험실들이 ISO 배지보다 민감도가 높은 것으로 평가되는 IDEXX 레지올레르트(Legiolert) 방식으로 전환하도록 이끌었습니다. 프랑스는 요양원을 위한 UAT 키트 지원을 지속하는 반면, 영국은 HSE 지침에 따라 분기별 위험 평가를 의무화합니다. 친환경 건축 이니셔티브는 때로 온수 저장 온도를 낮추게 하여, 에너지 효율을 유지하면서도 세균 증식을 촉진하지 않는 정교한 제어 전략을 요구합니다. 다양한 규제 체계를 능숙하게 활용할 수 있는 검사 제공업체들은 유럽연합 전역에서 경쟁 우위를 점하고 있습니다.

The legionella testing market size was valued at USD 377.52 million in 2025 and is forecast to reach USD 559.09 million by 2030, advancing at an 8.17% CAGR.

Stricter building-water regulations, heightened post-pandemic vigilance, and rapid advances in molecular diagnostics are sustaining double-digit demand growth. Mandatory CMS rules that link Medicare funding to implementation of ASHRAE-compliant water management programs keep hospitals and long-term-care facilities on a continuous testing cycle. Rising legal liability and insurance stipulations have extended this compliance mindset to hotels, commercial real estate, and manufacturing plants. Technology migration toward PCR platforms has shortened result turnaround from 7-14 days to under 48 hours, enabling early intervention protocols that limit outbreak scale.

Reported U.S. Legionnaires' disease cases tripled from 2000-2011 and have continued climbing through 2024, a pattern mirrored in several OECD countries. Melbourne's 2024 outbreak produced 77 cases, 75 hospitalizations, and 2 deaths, underscoring how rapidly contaminated aerosols can infect dense urban populations. With mortality in severe cases ranging from 20-40%, health systems recognize that routine surveillance lowers overall treatment costs. Employers also see productivity savings when preventive testing keeps staff from illness. Consequently, sustained epidemiological pressure is translating into baseline demand for both clinical and environmental testing.

Clinicians seek actionable results within 24 hours; culture's 7-14-day lag is now viewed as clinically unacceptable for severe pneumonia management. PCR platforms provide same-day answers with 99.95% negative predictive value at clinically relevant thresholds. Post-COVID facility re-openings exposed stagnant pipes that intensified bacterial growth, accelerating adoption of rapid molecular panels. Environmental managers likewise favor quick tests so they can adjust disinfection protocols before bacteria levels cross regulatory limits. The push for turnaround times under 48 hours therefore remains a defining feature of the Legionella testing market.

Culture yields 70-90% sensitivity depending on sample type and requires repeat sampling when non-Legionella flora overgrow plates. Urinary antigen assays detect only L. pneumophila serogroup 1, missing the 8-30% of cases caused by other serogroups. Each missed detection invites continued exposure and potential litigation, yet budget-limited facilities still opt for these older methods. Widespread reliance on legacy tests therefore slows universal migration to faster, broader-spectrum diagnostics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PCR/qPCR/ddPCR platforms captured 42.76% Legionella testing market share in 2024 because hospitals value 24-hour turnaround when treating severe pneumonia. Within the USD 377.52 million Legionella testing market size logged in 2025, PCR assays generated the largest revenue slice by combining high sensitivity with broad serotype coverage. Laboratories also rely on molecular methods to validate water treatment efficacy faster than culture. Culture remains essential for viability confirmation and antimicrobial susceptibility, but its use is shifting toward confirmatory rather than frontline testing. Direct fluorescent antibody staining fills immediate visualization niches yet accounts for a modest revenue contribution. Urinary antigen tests lead growth at a 10.56% CAGR by offering 15-minute point-of-care results that support emergency-department triage decisions. Technology refinements have pushed UAT sensitivity past 95%, and multiplex versions now detect several Legionella species in a single cartridge. As reagent costs fall, UAT kits are penetrating occupational health programs and cruise-ship medical units. Market participants therefore maintain balanced portfolios that cover both rapid molecular and decentralized antigen formats to maximize reach across diverse end-user budgets.

Second-generation ddPCR instruments are expected to erode culture share further by identifying sub-detectable colony counts in large plumbing systems. Field technicians equipped with portable LAMP-lateral-flow kits can now screen spa water during routine maintenance visits, creating new revenue lines for HVAC and water-treatment contractors. Although reagent pricing remains higher than agar media, volume purchasing and reagent rental contracts are narrowing the gap, especially for regional reference labs processing thousands of samples weekly. Over the forecast period, technology convergence will likely see labs combine ddPCR quantification with culture confirmation in a single workflow, cementing molecular dominance across the Legionella testing market.

The Legionella Testing Market Report is Segmented by Test Type (Culture Method, Urinary Antigen Test (UAT), Direct Fluorescent Antibody (DFA), Polymerase Chain Reaction (PCR/QPCR/DdPCR), and More), End-User (Hospitals & Clinics, Diagnostic Laboratories, and Other End Users), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 43.43% of global revenue in 2024, underpinned by a robust regulatory network that spans CMS rules for healthcare, OSHA guidelines for workplaces, and insurer-driven audits for commercial property owners. Large diagnostic firms headquartered in the United States supply most PCR reagents, while hundreds of accredited laboratories offer same-day test logistics. Canada's public-health agencies have mirrored U.S. standards, and Mexico's private hospital expansions are aligning procurement policies accordingly. High litigation exposure also keeps routine testing budgets intact, even during broader healthcare cost pressures.

Asia-Pacific is the fastest-growing region at a 9.34% CAGR, propelled by urbanization and infrastructure investment. Japan's Expo 2025 detected Legionella counts 50-times above safety limits, prompting nationwide awareness campaigns and stricter municipal codes. China's hospital-building boom and India's PPP hospital projects necessitate comprehensive water-safety plans that incorporate quarterly testing. Hong Kong's cooling-tower surveillance, which analyzed 115 samples in July 2024 alone, showcases government-led vigilance. Australia's state health departments continue to enforce monthly cooling-tower checks, setting a compliance example for Southeast Asian neighbors.

Europe presents a fragmented picture shaped by differing national laws and energy-conservation goals. Germany's high legionellosis incidence has moved laboratories toward the IDEXX Legiolert method, regarded as more sensitive than ISO plates. France continues to subsidize UAT kits for nursing homes, whereas the United Kingdom mandates quarterly risk assessments under HSE guidance. Green-building initiatives sometimes reduce hot-water storage temperatures, requiring sophisticated control strategies that maintain energy efficiency without fostering bacterial growth. Testing providers capable of navigating multiple regulatory frameworks enjoy a competitive edge across the European Union.