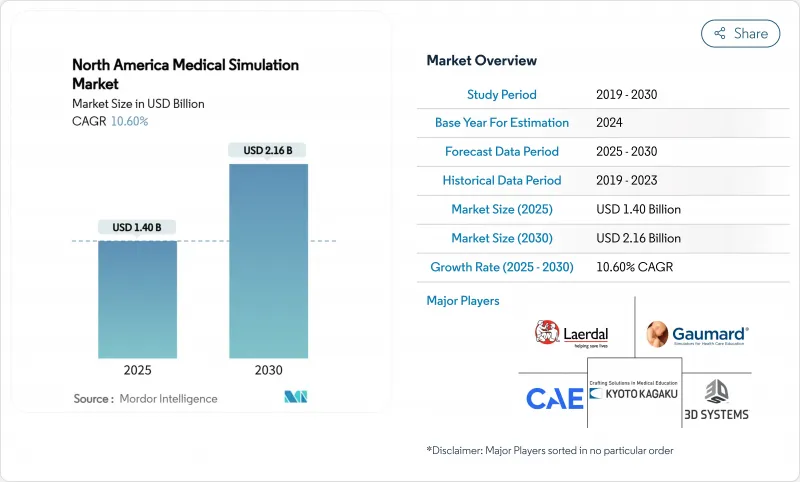

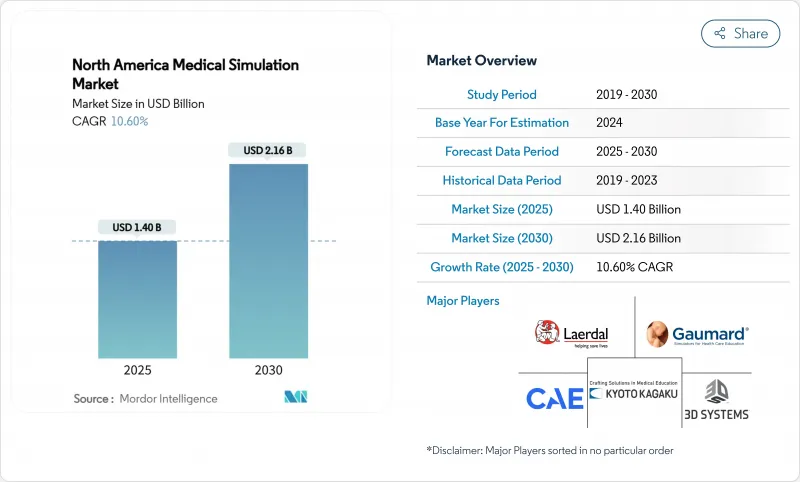

북미의 의료 시뮬레이션 시장은 2025년에 11억 4,000만 달러로 평가되었고, 2030년에 21억 6,000만 달러에 이를 것으로 예측되며, CAGR은 13.56%를 나타낼 전망입니다.

이 표제의 수치는 현재 의료 시뮬레이션 시장 규모를 나타내며, 교수진 부족, 환자 안전 의무화, 확장 현실 하드웨어의 급속한 발전에 힘입어 활발한 성장 궤도를 강조합니다. 수요 압박은 의과대학이 제한된 임상실습 자리를 마주하고, 규제 기관이 측정 가능한 역량 증명을 요구하며, 가상 현실 헤드 마운트 디스플레이가 마침내 임상 등급의 시각적 충실도를 제공할 때 가장 강합니다. 결과적으로 교육자와 병원들이 확장 가능하고 반복적이며 데이터가 풍부한 훈련 모델을 추구함에 따라 의료 시뮬레이션 시장은 선택적 지출에서 핵심 인프라 투자로 전환되고 있습니다. FDA 제출 시 계산 모델링에 대한 규제 강조, AI 기반 적응형 분석의 확산, 비용 효율적인 서비스 계약은 모두 시장 성장 모멘텀을 강화합니다.

복강경, 로봇, 내시경 기술은 기존 견습 모델로는 대규모로 제공할 수 없는 정신운동 기술을 요구합니다. 약 8,400달러 수준의 합리적인 가격의 로봇 수술 인터페이스는 자원이 제한된 학교에서도 고급 기술 실습 접근성을 확대했습니다. 햅틱 기능이 탑재된 가상 현실은 훈련생이 실제 수술실에 들어가기 전에 근육 기억을 형성하고 시술 자신감을 높이며, 이러한 도구를 사용하는 프로그램은 수술 중 오류율의 상당한 감소를 기록합니다. 외과의사 부족을 상쇄하기 위한 로봇 플랫폼의 성장은 시뮬레이션을 최전선 훈련 방식으로 더욱 공고히 합니다. 커리큘럼이 고반복, 무위험 연습 세션을 핵심 학습에 포함시키면서 이 촉진요인은 예측 연평균 성장률(CAGR)에 2.8% 포인트를 추가합니다.

시뮬레이션 기반 카테터 삽입 교육 과정은 시설당 연간 9.95건의 혈류 감염을 감소시켜 70만 달러 이상을 절감하고 7:1의 투자 수익률(ROI)을 제공합니다. 이러한 증거는 시뮬레이션을 교육적 부대비용에서 재정적 필수 요소로 재정의합니다. 합동위원회(Joint Commission)와 같은 인증 기관은 이제 문서화된 역량 지표를 요구하며, 시뮬레이션은 표준화된 시나리오와 자동화된 채점을 통해 이를 유일하게 제공합니다. 병원들은 이러한 지표를 활용해 가치 기반 보상 제도를 충족시키며 의료 과실 위험을 줄이고 치료 품질을 높입니다.

학장들의 84%가 인턴십 부족을 지적하며, 학교들이 시뮬레이션 할당량을 늘릴 수밖에 없다고 밝혔습니다. 현대식 센터에서는 적응형 시나리오와 분석 대시보드를 통해 한 명의 강사가 여러 학습자를 감독할 수 있어 교육 범위가 확대됩니다. 코로나19 사태는 시뮬레이션이 보조 도구가 아닌 교육 과정의 핵심 축으로서 역할을 입증했습니다. 따라서 장기적인 교수진 공백은 팬데믹 압박을 훨씬 넘어선 높은 수요를 지속시킬 전망입니다.

제품은 학술 및 병원 실험실의 물리적 기반으로서 2024년 매출의 53.6%를 차지했습니다. 이 중 중재 및 수술 시뮬레이터가 핵심을 이루며, 작업 훈련기와 생리학적 마네킹이 보조 역할을 합니다. 그러나 서비스 부문은 자본 지출보다 턴키 구독을 선호하는 기관들의 수요에 힘입어 연평균 13.67% 성장률을 기록하며 확장 중입니다. 클라우드 라이선싱, 커리큘럼 설계, 관리형 실험실 서비스는 일회성 구매를 예측 가능한 운영 예산으로 전환하며 의료 시뮬레이션 시장의 중대한 전환점을 마련하고 있습니다.

중재 시뮬레이터 수요는 로봇 및 복강경 시술 증가와 연동되며, 환자 시뮬레이터는 실제 모니터링 장치와 연동되는 무선 방식의 생리학적 기능이 풍부한 모델로 진화하고 있습니다. 서비스 성장세는 3B Scientific의 e Sono 같은 SaaS 초음파 플랫폼에서 가장 두드러지며, 이는 종량제 접근 방식이 고급 훈련을 대중화하는 방식을 보여줍니다. 반복 수익이 증가함에 따라 의료 시뮬레이션 산업은 고충실도 하드웨어 부문에서 가격 부담으로 배제되었던 중소 규모 기관까지 대상 고객층을 확대하고 있습니다.

저충실도 도구는 경제성과 신속한 배포 덕분에 2024년 지출의 47.35%를 차지합니다. 그럼에도 고충실도 시뮬레이터는 현실감과 측정 가능한 학습 성과 간의 연관성을 입증한 실증 연구로 인해 13.99%의 연평균 복합 성장률(CAGR)을 기록 중입니다. 고충실도 제품군에는 이제 Gaumard의 HAL S3201과 같은 마네킹이 포함되며, 동적 폐 순응도와 약물 인식 기능을 통해 시뮬레이션 실과 실제 중환자실 병상 간의 격차를 해소합니다. 기관들은 오류 감소로 인한 비용 절감을 정량화하여 높은 지출을 정당화함으로써 의료 시뮬레이션 시장 규모에서 이 비중을 확대하고 있습니다.

중간 충실도 시스템은 핵심 기술 훈련에 여전히 중요하지만, 고급 프로그램들은 생체 신호, 영상, 전자 기록을 동기화하는 고몰입형 경험으로 빠르게 전환하고 있습니다. 이러한 전환은 점점 더 복잡해지는 환자 집단에 대비하도록 임상의들을 더 잘 준비시키는 초현실주의로 조달 예산이 장기적으로 전환될 것임을 시사합니다.

The North American medical simulation market stands at USD 1.14 billion in 2025 and is forecast to climb to USD 2.16 billion by 2030, registering a 13.56% CAGR.

This headline figure represents the current medical simulation market size and highlights the brisk growth trajectory being fueled by faculty shortages, patient-safety mandates, and rapid advances in extended-reality hardware. Demand pressure is strongest where medical schools face limited clerkship slots, regulatory bodies insist on measurable competency proof, and virtual-reality head-mounted displays finally deliver clinical-grade visual fidelity. As a result, the medical simulation market is shifting from discretionary spending toward critical infrastructure investment as educators and hospitals chase scalable, repeatable, and data-rich training models. Regulatory emphasis on computational modeling in FDA submissions, rising adoption of AI-driven adaptive analytics, and cost-effective service contracting all reinforce the market's growth momentum.

Laparoscopic, robotic, and endoscopic techniques demand psychomotor skills that traditional apprenticeship models cannot deliver at scale. Affordable robotic-surgery interfaces priced near USD 8,400 have widened access to advanced skills practice for resource-constrained schools. Haptic-enabled virtual reality fosters muscle memory and boosts procedural confidence before trainees enter live theaters, and programs using these tools record significant declines in intra-operative error rates. Growth of robotic platforms to offset surgeon shortages further cements simulation as a frontline training modality. The driver adds 2.8 percentage points to forecast CAGR as curricula embed high-repetition, risk-free practice sessions into core learning.

Simulation-based catheter insertion curricula cut 9.95 bloodstream infections per facility each year, saving more than USD 700,000 and delivering a seven-to-one ROI. Such proof reframes simulation from educational overhead to financial imperative. Accrediting bodies like the Joint Commission now require documented competency metrics, which simulation uniquely provides through standardized scenarios and automated scoring. Hospitals leverage these metrics to satisfy value-based reimbursement schemes, shrinking malpractice exposure while elevating care quality.

Eighty-four percent of deans cite clerkship shortages, forcing schools to raise simulation quotas. Modern centers let one instructor oversee multiple learners via adaptive scenarios and analytics dashboards, multiplying teaching reach. The COVID-19 disruption validated simulation's role as curricular backbone rather than ancillary tool. Long-term faculty gaps therefore sustain elevated demand well beyond pandemic pressures.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Products commanded 53.6% of 2024 revenue as the physical backbone of academic and hospital labs. Within that total, interventional and surgical simulators remain the cornerstone, supplemented by task trainers and physiologic manikins. Yet the services category is expanding at a 13.67% CAGR, propelled by institutions favoring turnkey subscriptions over capital outlay. Cloud licensing, curriculum design, and managed-lab services convert episodic purchases into predictable operating budgets, a pivotal shift for the medical simulation market.

Interventional simulator demand mirrors the growth of robotic and laparoscopic procedures, while patient simulators evolve toward wireless, physiology-rich models that integrate with real monitoring devices. Services momentum is most evident in SaaS ultrasound platforms such as 3B Scientific's e Sono, which illustrates how pay-as-you-go access democratizes advanced training. As recurring revenue rises, the medical simulation industry expands its addressable audience to smaller institutions once priced out of the high-fidelity hardware segment.

Low-fidelity tools hold 47.35% of 2024 spend thanks to affordability and quick deployment. Nevertheless, high-fidelity simulators are logging a 13.99% CAGR as empirical studies tie realism to measurable learning gains. The high-fidelity cohort now includes manikins like Gaumard's HAL S3201 with dynamic lung compliance and drug recognition, bridging the gap between simulation suites and real ICU beds. Institutions justify higher outlays by quantifying error-reduction savings, thereby growing this share of the medical simulation market size.

Medium-fidelity systems remain important for core skills drills, but advanced programs are fast-tracking toward high-immersion experiences that synchronize vitals, imaging, and electronic records. That migration signals a long-run pivot of procurement budgets toward ultra-realism that better prepares clinicians for increasingly complex patient populations.

The North American Medical Simulation Market Report is Segmented by Products & Services (Products, Services & Software), Fidelity (High-Fidelity, Medium-Fidelity, and More), End User (Academic & Research Institutes, Hospitals & Surgical Centers, and More), Delivery Mode (On-Premise Simulation Labs, Cloud-Based), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).