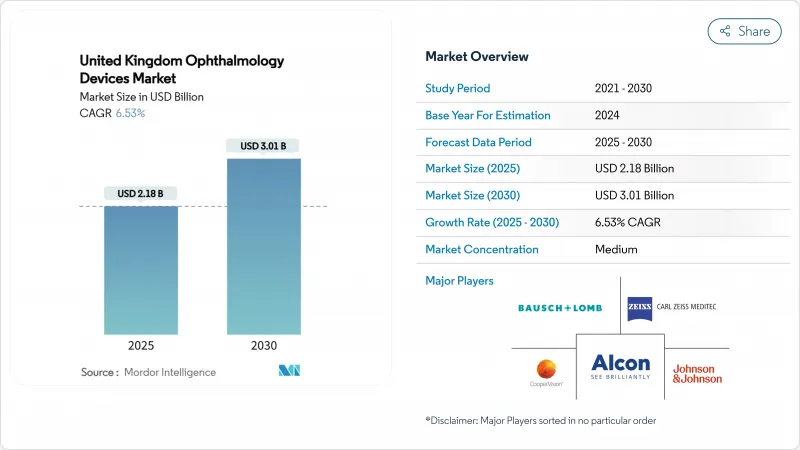

영국의 안과용 기기 시장 규모는 2025년에 21억 8,000만 달러로 평가되었고, 2030년에 30억 1,000만 달러에 이를 것으로 예측되며, 기간 중 6.53%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

시력 보존 수술에 대한 견고한 수요, 백내장 환자 풀을 확대하는 고령화 인구, 그리고 결과 기록을 보상하는 영국 국민건강보험(NHS) 프레임워크 계약이 종합적으로 영국의 안과용 의료기기 시장의 지속적인 성장을 뒷받침하고 있습니다. 시력 관리 소모품은 소매 채널을 통해 안정적인 판매량을 확보하고 있으나, 영상 및 분석 분야 지출 증가로 데이터 중심 진단으로의 점진적 전환이 가시화되고 있습니다. 사모펀드 지원 외래 수술 센터(ASC)는 모듈식 수술실을 지속적으로 도입하며, 공급업체들이 NHS 요금 체계와 상업적 자비 부담 패키지에 부합하는 가치 기반 가격 정책을 정교화하도록 유도하고 있습니다. 팬데믹 기간 동안 발생한 NHS 대기 환자 물량은 2026년 중반 이전에는 해소되지 않을 것으로 예상되어, 백내장, 녹내장, 망막 기기의 높은 기준 물량이 유지될 전망입니다.

2025년 3월 발표된 영국 인구조사 업데이트에 따르면, 65세 이상 주민은 현재 1,960만 명으로 전체 인구의 28%를 차지하며, 이는 2024년 26%에서 증가한 수치입니다. 왕립안과학회(RCOphth) 모델링에 따르면 서비스 수용 능력이 유지될 경우 2025년부터 2035년 사이 백내장 수술 건수가 50% 증가할 것으로 전망됩니다. 병원 진료 통계(HES)도 이 추세를 확인시켜줍니다. 2024/25 회계연도 백내장 적출술 건수는 47만 5천 건을 넘어섰으며, 이는 전년 대비 6.2% 증가한 수치로 2010년 전자 기록 시작 이후 가장 가파른 연간 증가율을 기록했습니다. 녹내장 진료량도 비슷한 양상을 보이고 있다; 영국 NHS 트러스트는 2024년 2023년 대비 8% 증가한 섬유주절제술을 기록했으며, 만성 개방각 녹내장 외래 진료 건수는 사상 처음으로 160만 건을 돌파했습니다. 이에 따라 파코 시스템, 녹내장 스텐트, 인공수정체 제조업체들은 위원회가 명확히 예측 가능한 인구 고령화 증가에 대비해 재고를 확보하려는 움직임 속에서 다년간 공급 계약을 체결하고 있습니다.

2025년 2월 런던대학(UCL)이 발표한 동료 검토 연구에 따르면, 영국 18-24세 인구 중 근시 비율이 2020년 28%에서 현재 34%로 증가했으며, 이는 팬데믹 봉쇄 기간 동안 지속된 화면 노출이 원인이라고 분석했습니다. 부츠 안경점은 2024년 한 해 동안 근시 진행 억제 콘택트렌즈 주문량이 전년 대비 22% 증가했다고 보고했으며, 스펙세이버스는 조기 개입 수요에 대응하기 위해 2024년 12월까지 650개 매장에 축거리 측정 서비스를 도입했습니다. 이 데이터는 영국 안과 의사 협회(College of Optometrists)의 2024년 설문조사 결과와도 일치하는데, 실무자의 61%가 “경력 중 어느 때보다 많은 청소년 근시 처방을 하고 있다”고 답했습니다. 기기 공급업체들은 산소 투과성 일회용 렌즈와 안경 렌즈 디자인으로 축축장 지연을 유도하며 수십 년에 걸친 평생 가치를 지닌 시장 부문을 공략하고 있습니다. 이에 따라 기존에 노인 질환에 집중하던 제조사들도 부모와 대학을 대상으로 마케팅을 재편하며 은퇴 후 소비자층을 넘어 수익 기반을 확대하는 연쇄 효과가 발생하고 있습니다.

2025년 5월 발표된 영국 의학위원회(GMC) 인력 통계에 따르면 안과 전문의 공석률은 9.4%로, 2024년 8.7%에서 상승했으며 목표치인 7%를 크게 상회합니다. 영국안과전문의협회(RCOphth)의 2025년 인구조사에 따르면 현재 수요를 충족하려면 즉시 234명의 추가 전문의가 필요하며, 이 수치는 훈련 인원이 급격히 증가하지 않는 한 2030년까지 두 배로 증가할 것으로 예상됩니다. 인력 부족은 수술실 활용도 저하로 이어집니다. GIRFT 감사 자료에 따르면 2024년 예약된 백내장 수술 목록의 17%가 외과의사 부족으로 취소되거나 단축되었습니다. 따라서 기기 활용률은 설치 기반 성장에 미치지 못해 교체 주기를 억제하고 공급업체의 자본 장비 투자 수익률(ROI)을 끌어내리고 있습니다.

비전 케어 기기는 2024년 영국의 안과용 의료기기 시장 점유율의 약 60.11%를 차지하며 안정적인 콘택트렌즈 판매로 반복 수익을 지속 견인할 전망입니다. 반면 진단 및 모니터링 기기는 프리미엄 가격에 분석 서비스를 묶어 제공하는 NHS 계약의 지원으로 8.81%의 연평균 성장률(CAGR)을 기록하며 시장 성장률을 앞지를 것으로 예상됩니다. 1초 미만 스캔이 가능한 상호운용성 OCT 플랫폼은 검사 주기를 단축시켜 추가 장비 투자 없이도 클리닉이 더 많은 환자를 처리할 수 있게 합니다. 당뇨성 망막병증 진단 감도가 80% 이상으로 보고된 컴퓨터 지원 망막 분석(CARA) 시스템은 임상 검증이 도입을 가속화하는 사례를 보여줍니다. 공급업체들은 AI 호환성을 위해 하드웨어 동등성이 요구될 때만 기존 안저 카메라를 개조하며, 이는 단기 단위 판매는 위축시키지만 애프터마켓 액세서리 수익을 끌어올리는 지속적인 개조 파이프라인을 시사합니다.

전안부 모듈을 통합한 공급업체들은 공간을 추가로 차지하지 않으면서 굴절 및 각막 수술을 모두 처리할 수 있어 공간이 제한된 도시 수술실에 매력적입니다. 산소 투과성 소재를 활용한 콘택트렌즈 혁신은 소매 모멘텀을 유지하지만, 가격 경쟁으로 인한 마진 압박으로 절대적 매출 성장은 완만합니다. 진단 장비 공급업체들은 NHS 지불 주기에 맞춘 리스 계획을 제공함으로써 일회성 자본 지출에 대한 우려를 상쇄합니다. 이러한 계약에는 고마진 소프트웨어 수익을 확대하는 서비스 계약이 포함되어 제품 개발 주기를 연장하는 데 기여합니다. 데이터 기반 모니터링 기능은 MHRA의 강화된 증거 요구 사항도 충족시켜 연결 플랫폼 주변에 규정 준수 장벽을 구축합니다.

The United Kingdom Ophthalmic Devices market size is USD 2.18 billion in 2025 and is projected to climb to USD 3.01 billion by 2030, advancing at a 6.53%CAGR throughout the period.

Robust demand for sight-saving surgery, an ageing population that expands the cataract pool, and National Health Service (NHS) framework contracts that reward outcome documentation collectively underpin sustained growth in the United Kingdom Ophthalmic Devices market. Vision-care consumables secure stable volumes through retail channels, yet heightened spending on imaging and analytics indicates a gradual pivot toward data-rich diagnostics. Private equity-funded ambulatory surgery centres (ASCs) continue to roll out modular theatres, nudging suppliers to refine value-based pricing compatible with NHS tariffs and commercial self-pay packages. NHS backlogs created during the pandemic are not expected to clear before mid-2026, locking high baseline volumes for cataract, glaucoma, and retina devices.

United Kingdom census updates published in March 2025 show that residents aged >=65 now account for 19.6 million people, or 28% of the total population, up from 26% in 2024. Royal College of Ophthalmologists (RCOphth) modelling projects that cataract operations will rise by 50% between 2025 and 2035 if service capacity keeps pace. Hospital Episode Statistics confirm the trend: cataract extractions exceeded 475,000 in financial-year 2024/25, marking a 6.2% jump on the previous year and the steepest annual increase since electronic records began in 2010. Glaucoma workload is following suit; English NHS trusts recorded 8% more trabeculectomies in 2024 than in 2023, while outpatient visits for chronic open-angle glaucoma surpassed 1.6 million for the first time. Device makers selling phaco systems, glaucoma stents and intraocular lenses are therefore locking in multiyear supply agreements as commissioners try to ring-fence inventory against a clearly visible demographic bulge.

A peer-reviewed study released by University College London in February 2025 found that 34% of British 18- to 24-year-olds are now myopic, compared with 28% in 2020, attributing the acceleration to sustained screen exposure during pandemic lockdowns. Boots Opticians reported a 22% year-on-year rise in orders for myopia-control contact lenses during calendar-year 2024, while Specsavers introduced axial-length measurement in 650 stores by December 2024 to meet demand for earlier intervention. The data resonate with the College of Optometrists' 2024 survey in which 61% of practitioners cited "more teenage myopia fittings than at any time in their careers". Device suppliers are responding with oxygen-permeable daily disposables and spectacle-lens designs that slow axial elongation, targeting a market segment with decades of lifetime value. The cascading effect is that manufacturers traditionally focused on geriatric indications are now re-tooling marketing to parents and universities, broadening the revenue base beyond post-retirement consumers.

General Medical Council workforce statistics released in May 2025 reveal that the ophthalmology consultant vacancy rate sits at 9.4%, up from 8.7% in 2024 and comfortably above the 7% target threshold. RCOphth's 2025 census concludes that 234 additional consultants are needed immediately to meet present demand, a figure projected to double by 2030 unless training numbers rise sharply. Workforce strain translates into theatre under-utilisation: GIRFT audit data show that 17% of cataract lists booked in 2024 were cancelled or cut short due to surgeon unavailability. Device utilisation rates therefore lag installed base growth, dampening replacement cycles and tugging down capital-equipment ROI for providers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Vision Care Devices hold roughly 60.11% of United Kingdom Ophthalmic Devices market share in 2024 and continue to anchor recurring revenue with stable contact-lens sales. Diagnostic & Monitoring Devices, however, are set to outpace with an 8.81%CAGR, aided by NHS contracts that bundle analytics services at premium prices. Interoperable OCT platforms capable of sub-second scans shorten examination cycles, letting clinics process more patients without extra chair investment. The Computer-Assisted Retinal Analysis (CARA) system's reported sensitivity above 80% for referable diabetic retinopathy exemplifies how clinical validation accelerates uptake. Suppliers retrofit legacy fundus cameras only when AI compatibility demands hardware parity, indicating a sustained refurbishment pipeline that dampens short-term unit sales but lifts aftermarket accessory revenue.

Suppliers integrating anterior-segment modules address both refractive and corneal surgery without increasing footprint, appealing to space-constrained urban theatres. Contact-lens innovation around oxygen-permeable materials sustains retail momentum but margin pressure from price competition keeps absolute revenue growth moderate. Diagnostic device vendors offset lump-sum capital expenditure concerns by offering leasing plans matched to NHS payment cycles. Such arrangements embed service contracts that expand high-margin software revenue, supporting longer product-development timelines. Data-driven monitoring functions also satisfy the MHRA's heightened evidence requirements, creating a compliance moat around connected platforms.

The United Kingdom Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).