안과 장비 시장(-2030년) : 기술, 제품 유형(외과용 기기, 진단&모니터링 기기), 최종 사용자별 예측

Ophthalmic Equipment Market by Technology, Product Type (Surgical Devices, Diagnostic & Monitoring Devices ), End User - Global Forecast to 2030

상품코드:1881234

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 474 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

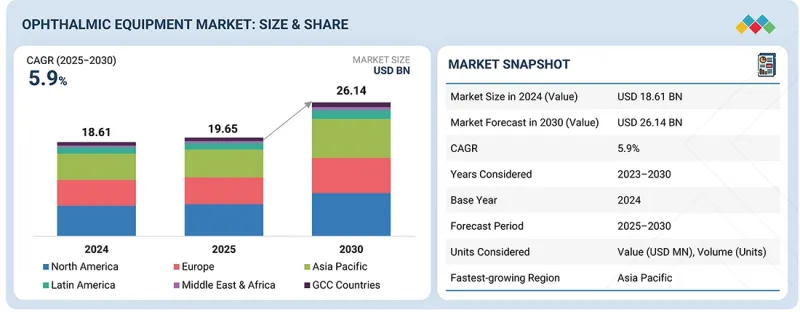

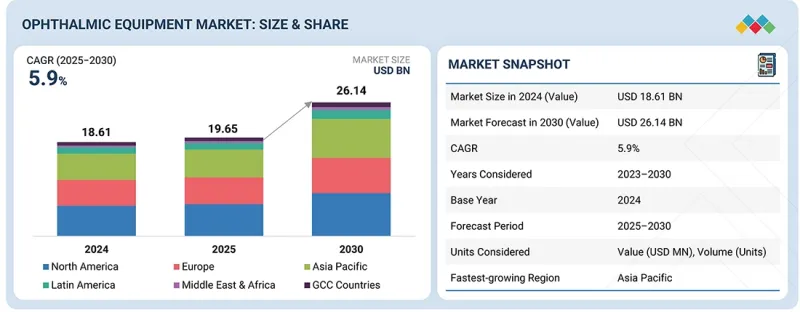

안과 장비 시장 규모는 예측 기간 동안 CAGR 5.9%를 나타내 2025년 196억 5,000만 달러에서 2030년에는 261억 4,000만 달러에 이를 것으로 전망됩니다.

조사 범위

조사 대상 기간

2024-2033년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

기술, 제품 유형, 최종 사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가

안과 장비 시장은 주로 백내장, 녹내장, 당뇨병성 망막증 등의 안질환의 유병률 증가나 세계적인 고령화에 의해 견인되고 있습니다. OCT와 안저카메라 등의 고급 진단 툴의 사용 증가, 의료비 증가, 개발도상국의 안과 의료 서비스에 대한 액세스 확대도 시장 성장을 가속하고 있습니다.

또한 저침습 및 AI 기반 안과 의료 솔루션을 지원하는 기술 혁신도 그 보급을 촉진하고 있습니다. 그러나 장비의 고비용과 숙련된 전문가의 부족은 시장 확대를 제한하고 있습니다.

제품 유형별로는 백내장 수술, 굴절 교정 수술, 녹내장 수술의 세계적인 실시 건수가 많기 때문에 외과용 기기가 시장을 독점하고 있습니다. 현미 수술 기술, 펨토초 레이저, 초음파 유화 흡입 시스템의 진보로 정밀도와 치료 성적이 향상되어 채용이 증가하고 있습니다. 게다가 노인 인구 증가와 고급 수술센터의 확대는 안과 수술 장비 수요를 더욱 밀어 올리고 있습니다.

최종 사용자별로 병원은 가장 큰 점유율을 차지합니다. 병원은 종합적인 안과 의료를 제공하는 주요 기지로서 진단 서비스와 외과 수술 서비스를 모두 제공합니다. 고급 인프라와 숙련된 안과 의사를 옹호하고 클리닉보다 더 많은 환자를 모으고 있습니다. 또한, 복잡한 치료를 위한 고기능 안과 장비에 대한 투자 능력은 시장 전반에 걸친 병원의 이점을 강화하고 있습니다.

북미는 첨단 의료 인프라, 혁신적인 진단 및 수술 기술의 보급률이 높고 주요 제조업체의 강력한 존재감으로 최대 점유율을 차지합니다. 이 지역은 다량의 의료 지출, 지원적인 상환 정책, 다수의 훈련을 받은 안과 의사의 존재로부터 혜택을 받고 있습니다. 게다가 녹내장과 노인황반변성 등 노화성 안질환의 유병률 증가가 장비 수요를 더욱 밀어 올리고 있으며, 지속적인 기술 혁신과 조기 도입이 시장의 우위성 유지에 기여하고 있습니다.

본 보고서에서는 세계의 안과 장비 시장을 조사했으며, 시장 개요, 시장 성장 영향요인 분석, 기술·특허 동향, 법규제 환경, 사례연구, 시장 규모 추이와 예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요기업 프로파일 등을 정리했습니다.

The ophthalmic equipment market is projected to reach USD 26.14 billion by 2030 from USD 19.65 billion in 2025, at a CAGR of 5.9% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2033

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Technology, Product Type, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries

The ophthalmic equipment market is mainly propelled by the increasing prevalence of eye conditions such as cataracts, glaucoma, and diabetic retinopathy, along with the aging global population. Rising use of advanced diagnostic tools like OCT and fundus cameras, higher healthcare expenditures, and broader access to eye care services in developing countries also drive market growth.

Additionally, innovations in technology that support minimally invasive and AI-based eye care solutions boost adoption. However, high equipment costs and a shortage of skilled professionals limit market expansion.

By product type, surgical devices dominate the ophthalmic equipment market because of the high volume of cataract, refractive, and glaucoma surgeries worldwide. Advances in microsurgical techniques, femtosecond lasers, and phacoemulsification systems have improved precision and outcomes, increasing their adoption. Additionally, the growing elderly population and the expanding availability of advanced surgical centers further boost demand for ophthalmic surgical devices.

By end user, hospitals hold the largest share in the ophthalmic equipment market because they serve as primary centers for comprehensive eye care, providing both diagnostic and surgical services. They have advanced infrastructure and skilled ophthalmologists, and they attract more patients than clinics. Additionally, hospitals' ability to invest in high-end ophthalmic equipment for complex procedures strengthens their dominance in the overall market.

North America holds the largest share of the ophthalmic equipment market because of its advanced healthcare infrastructure, high adoption of innovative diagnostic and surgical technologies, and a strong presence of leading manufacturers. The region benefits from significant healthcare spending, supportive reimbursement policies, and a large number of trained ophthalmologists. Additionally, the increasing prevalence of age-related eye diseases like glaucoma and macular degeneration further boosts equipment demand, while ongoing innovation and early technology adoption help sustain the market dominance.

A breakdown of the primary participants (supply-side) for the ophthalmic equipment market referred to in this report is provided below:

By Company Type: Tier 1:34%, Tier 2: 38%, and Tier 3: 28%

By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Prominent players in the ophthalmic equipment market are Bausch Health Companies, Inc. (Canada), Alcon (US), Carl Zeiss Meditec AG (Germany), Johnson & Johnson Vision Care (US), HOYA Corporation (Japan), EssilorLuxottica (France), Canon Inc. (Japan), Glaukos Corporation (US), Nidek Co., Ltd. (Japan), Topcon Corporation (Japan), Staar Surgical (US), Haag-Streit (Switzerland), Visionix (France), Shanghai Mediworks Precision Instruments Co., Ltd. (China), Halma plc (UK), among others.

Research Coverage

The report assesses the ophthalmic equipment market and estimates its size and future growth potential across various segments, including technology, product type, end user, and region. It also provides a competitive analysis of the major players, featuring company profiles, product offerings, recent developments, and key market dynamics strategies.

Reasons to Buy the Report

The report will help market leaders and new entrants by providing data on approximate revenue figures for the overall market, the ophthalmic equipment sector, and its subsegments. It will assist stakeholders in understanding the competitive landscape and gaining insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report helps stakeholders grasp the market pulse by offering data on key drivers, barriers, obstacles, and opportunities in the market.

This report provides insights into the following points:

Analysis of key drivers (Increasing geriatric population, Rising prevalence of eye disorders, Technological advancements in ophthalmic devices, and Increased government initiatives to control visual impairment), restraints (High cost of ophthalmology devices, High cost and risk associated with eye surgeries and Rising adoption of refurbished ophthalmic devices), opportunities (Potential growth opportunities in emerging markets and Low adoption of phacoemulsification devices and premium IOLs in emerging markets), and challenges (Low accessibility to eye care in low-income countries, Lack of skilled professionals)

Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global ophthalmic equipment market

Market Development: Thorough knowledge and analysis of the profitable rising markets by technology, product type, end user, and region

Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global ophthalmic equipment market

Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global ophthalmic equipment market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 SEGMENTS COVERED & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY USED

1.5 STAKEHOLDERS

1.6 LIMITATIONS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 CAGR PROJECTIONS

2.2.2 TOP-DOWN APPROACH

2.3 MARKET BREAKDOWN & DATA TRIANGULATION

2.4 MARKET SHARE ESTIMATION

2.5 STUDY ASSUMPTIONS

2.6 LIMITATIONS

2.6.1 METHODOLOGY-RELATED LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 OPHTHALMIC EQUIPMENT MARKET OVERVIEW

4.2 NORTH AMERICA: OPHTHALMIC EQUIPMENT MARKET, BY COUNTRY AND END USER (2024)