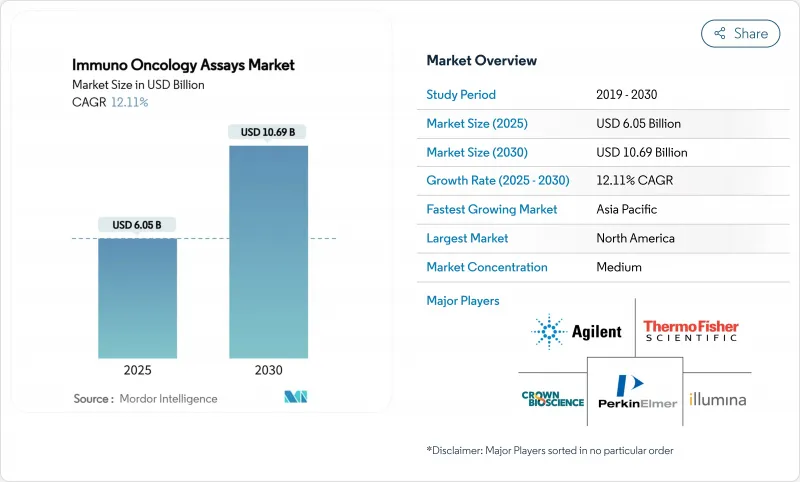

면역 종양 어세이 시장은 2025년에 60억 5,000만 달러로 추정되고, 2030년에는 106억 9,000만 달러에 이를 것으로 예측됩니다.

세계적인 암 이환율의 상승, 동반진단약에 대한 규제 당국의 꾸준한 지원, 공간 생물학적 플랫폼의 채용 가속이 함께, 세련된 면역 프로파일링 검사에 대한 수요가 높아지고 있습니다. 제약기업 및 진단제의 파트너십을 확대하면 검증 기간이 단축되고 검사 메뉴가 확대되는 한편 인공지능(AI)의 통합으로 검사 정밀도 및 처리량이 향상됩니다. 북미는 유리한 보험 상환으로 주도권을 유지하고 있지만 아시아태평양은 의료 인프라가 성숙하고 임상시험 활동이 활발해짐에 따라 가장 빠른 섭취를 기록하고 있습니다. 경쟁 전략은 멀티오믹스 통합과 실제 임상 증거 창출에 점점 더 의존하고 있으며, 민첩한 기술 공급자는 지역 암 영역에서 큰 점유율을 얻을 수 있습니다.

면역체크포인트 억제제는 치료 상황을 재형성하고 PD-L1 상태, 종양 돌연변이 부하 및 마이크로 위성의 안정성을 측정하는 컴패니언 검사의 광범위한 전개를 촉진합니다. 식도 편평상피암에 대한 tislelizumab과 화학요법의 병용, HER2 양성 위암에 대한 pembrolizumab-trastuzumab 등 2025년에 여러 FDA 승인이 이루어진 것은 견고한 예측 검정의 필요성을 강조하고 있습니다. 암 면역요법학회는 현재 일상적인 임상 판단의 지침이 되는 바이오마커 패널을 리스트업하고 있습니다. 공간 오믹스 플랫폼은 다차원적인 종양 미세환경 분석을 가능하게 하고, 분석의 특이성을 증가시킴으로써, 효능 예측을 더욱 정교하게 합니다.

인공지능 및 공간 생물학 기술을 결합하면 전통적인 접근 방식에서 보이지 않았던 세포 간 상호 작용이 드러납니다. 가번 연구소의 AAnet 도구는 치료 전략에 정보를 제공하기 위해 다섯 가지 종양 상재 세포 유형을 구별함으로써 이러한 진보를 보여줍니다. Hyperion XTi Imaging Mass Cytometer와 같은 상용 시스템은 자가 형광 노이즈 없이 40개 이상의 마커를 동시에 시각화하여 보다 깊은 바이오마커 파이프라인을 개발합니다. Molecular Cancer 잡지의 연구는 고해상도 3D 조직학이 종양 불균일성에 대한 이해를 깊게하고 분석 혁신을 가속화한다는 것을 확인했습니다.

NGS에 대한 메디케어의 청구 거부율이 2025년에는 16.8%에서 27.4%로 급상승해 미국 지급자의 감시가 엄격해지고 있음을 나타냅니다. 완전한 공간 프로파일링 설정을 위한 설비 투자는 50만 달러를 초과하며 지역 환경에서의 보급은 더욱 제한됩니다. 유럽의 의료기술평가(Health Technology Assessment)는 발매 스케줄에 12-18개월을 추가하여 소규모 개발자의 재무 리스크를 증대시킵니다. 그 결과 비용에 민감한 지역에서의 보급을 유지하기 위해서는 가격 계층화 전략이 필수적입니다.

2024년, 시약 및 항체는 면역 종양 어세이 시장의 40.12%를 차지했으며, 면역 검사 워크플로우가 소모품에 치우치고 있는 것을 증명했습니다. 병원 및 레퍼런스 실험실은 SITC가 권장하는 바이오마커의 요구사항을 충족하기 위해 유효한 항체 패널을 사용합니다. 검사 장비는 40가지 이상의 마커를 감지할 수 있는 이미징 매스사이트 메트리 플랫폼으로 업그레이드되어 안정적인 수요를 누리고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 12.67%로 예측되는 소프트웨어 및 애널리틱스는 세포 표현형 매핑과 클라우드 기반 데이터 공유를 자동화하는 AI 모듈로부터 혜택을 받습니다. 가반 연구소의 AAnet과 유사한 솔루션은 분석 시간을 단축하고 디지털 병리 공급업체에게 새로운 수익원을 창출합니다. 이 소프트웨어의 급속한 성장은 면역 종양 어세이 시장의 수익 구성을 다양화하고 있습니다.

차세대 시퀀서는 2024년에 면역 종양 어세이 시장에서 37.67%의 점유율을 유지하고 광범위한 돌연변이 스캔에 필수적인 존재로 남아있습니다. 고심도 패널 시퀀싱은 종양 돌연변이 부하의 계산을 지원하고 체크포인트 억제제의 사용을 직접 유도합니다.

CAGR 12.71%를 보일 것으로 예측되는 Multiplex Spatial Profiling은 온전한 조직 내의 단백질과 RNA 마커의 단일 셀 분해능 매핑을 가능하게 합니다. 일루미나의 모든 트랜스크립트 공간 플랫폼은 컨텍스트가 풍부한 해석으로의 변화를 돋보이게 합니다. Immunoassay, PCR 및 Flow Cytometry 방법은 표적 및 고처리량 용도 분야에서 보완적인 역할을 하며, 면역 종양 어세이 시장에서 기술의 다양성을 유지합니다.

북미는 유리한 상환, 조기 AI 도입, 종합암 센터의 치밀한 네트워크를 통해 2024년 세계 매출의 42.34%를 창출하였습니다. 메디케어의 NGS 진단제에 대한 적용 범위의 확대는 단기적인 상환 불확실성을 초래하지만, 강력한 민간부담의 틀이 전체적인 성장을 유지합니다.

유럽에서는 의료기술평가(Health Technology Assessment)에서 임상적 유용성이 검증된 후 널리 전개되기 때문에 균형 잡힌 진전이 유지되고 있습니다. EMA에 의한 tislelizumab과 같은 약물의 승인은 면역 요법의 확대에 대한 지역의 헌신을 보여줍니다. 여러 국가의 승인이 진단 약의 출시를 지연시킬 수 있지만 EU의 IVDR을 준수하는 간소화 된 패스웨이는 2026년 이후 시장 출시까지의 기간을 단축할 것으로 기대됩니다.

아시아태평양은 CAGR 12.86%로 성장을 이끌고 있는데, 이는 중국이 국가적인 암 검진 프로그램을 도입하고 일본이 유전체 검사를 조성하고 있기 때문입니다. 인도와 한국에서는 정밀의료 허브가 상승하고 수요를 더욱 자극합니다. 혁신적인 검사 장비에 대한 규제의 간소화로 접근성이 향상되었으며, 면역 종양 어세이 시장에서 국제적인 공급업체는 대응 가능한 기반을 획득하고 있습니다.

중동 및 아프리카에서는 걸프 국가들이 암 연구센터에 투자하고 멀티플렉스 플랫폼을 조달하고 있기 때문에 수요가 증가하고 있습니다. 남미에서는 브라질의 관민 종양 파트너십과 아르헨티나의 국가 가이드라인에 대한 유전체 검사 도입에 견인되어 꾸준한 진전을 기록하고 있습니다. 진료 보상 적용 범위에 차이가 있기 때문에 검사 건수는 아직 제한되어 있지만 장기적인 이환 동향은 잠재적인 수요를 지원하고 있습니다.

The immuno Oncology assays market stands at USD 6.05 billion in 2025 and is forecast to reach USD 10.69 billion by 2030, reflecting a healthy 12.11% CAGR.

Rising global cancer incidence, steady regulatory support for companion diagnostics, and accelerating adoption of spatial biology platforms combine to spur demand for sophisticated immune profiling tests. Growing pharma-diagnostic partnerships shorten validation timelines and expand test menus, while artificial intelligence (AI) integration strengthens assay accuracy and throughput. North America maintains leadership through favorable reimbursement, but Asia-Pacific records the fastest uptake as healthcare infrastructure matures and clinical trial activity rises. Competitive strategies increasingly hinge on multi-omics integration and real-world evidence generation, positioning agile technology providers to capture sizeable share in community oncology settings.

Immune-checkpoint inhibitors reshape the therapeutic landscape, prompting wider deployment of companion tests that gauge PD-L1 status, tumor mutational burden, and microsatellite stability. Multiple FDA approvals in 2025, such as tislelizumab plus chemotherapy for esophageal squamous cell carcinoma and pembrolizumab-trastuzumab for HER2-positive gastric cancer, emphasise the need for robust predictive assays. The Society for Immunotherapy of Cancer lists biomarker panels that now guide routine clinical decision-making. Spatial omics platforms further refine response prediction, enabling multidimensional tumour micro-environment analysis that elevates assay specificity.

Coupling AI with spatial biology technology uncovers cellular interactions previously hidden by conventional approaches. The Garvan Institute's AAnet tool exemplifies this progress by differentiating five tumour-resident cell types to inform therapeutic strategies. Commercial systems such as the Hyperion XTi Imaging Mass Cytometer visualise 40+ markers simultaneously without autofluorescence noise, fostering deeper biomarker pipelines. Research in Molecular Cancer confirms that high-resolution 3D histology enhances understanding of tumour heterogeneity, accelerating assay innovation.

Sharp increases in Medicare claim denial rates for NGS-from 16.8% to 27.4% in 2025-illustrate tightening US payer scrutiny. Capital investment exceeding USD 500,000 for full spatial-profiling setups further limits diffusion in community settings. Health technology assessments in Europe add 12-18 months to launch timelines, increasing financial risk for smaller developers. Consequently, price-tiering strategies become essential to sustain uptake in cost-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Reagents & Antibodies captured 40.12% of the immuno-oncology assays market in 2024, evidencing the consumable-heavy nature of immune testing workflows. Hospital and reference laboratories turn to validated antibody panels to meet SITC-endorsed biomarker requirements. Instruments enjoy steady demand as labs upgrade to imaging-mass-cytometry platforms capable of 40-plus marker detection.

Software & Analytics, projected to post a 12.67% CAGR through 2030, benefits from AI modules that automate cell-phenotype mapping and cloud-based data sharing. The Garvan Institute's AAnet and similar solutions lower analysis times, creating new revenue streams for digital pathology vendors. This software upsurge diversifies revenue composition within the immuno-oncology assays market.

Next-Generation Sequencing retained 37.67% share of the immuno-oncology assays market in 2024, remaining indispensable for broad mutational scans. High-depth panel sequencing supports tumour mutational burden calculation, directly guiding checkpoint inhibitor use.

Multiplex Spatial Profiling, forecast to grow at 12.71% CAGR, permits single-cell resolution mapping of protein and RNA markers within intact tissues. Illumina's whole-transcriptome spatial platform highlights this shift toward context-rich analytics. Immunoassay, PCR, and flow cytometry modalities maintain complementary roles for targeted or high-throughput applications, collectively sustaining technology diversity inside the immuno-oncology assays market.

The Global Immuno-Oncology Assays Market Report is Segmented by Product (Reagents & Antibodies, Instruments, and More), Technology (Immunoassay, PCR, and More), Assay Type (CDx, Ldts, RUO), Indication (Lung, Colorectal, Melanoma, Breast, Other Cancers), Sample Type (Tissue, Liquid Biopsy), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.34% of 2024 global revenue through favourable reimbursement, early AI adoption, and dense networks of comprehensive cancer centres. Medicare's evolving coverage for NGS diagnostics still poses short-term reimbursement uncertainty, but strong private-payer frameworks keep overall growth intact.

Europe maintains balanced progress as health technology assessments verify clinical benefit before wide rollout. EMA's approval of agents such as tislelizumab shows regional commitment to immunotherapeutic expansion. Although multiple national approval layers can delay diagnostics launches, streamlined EU IVDR-compliant pathways promise to shorten time-to-market after 2026.

Asia-Pacific leads growth at a 12.86% CAGR as China deploys national cancer screening programs and Japan subsidises genomic testing. Emerging precision-medicine hubs in India and South Korea further stimulate demand. Simplified regulatory fast-tracks for innovative devices improve access, giving international suppliers a sizeable addressable base in the immuno-oncology assays market.

Middle East & Africa witnesses incremental uptake as Gulf states invest in oncology centres of excellence and procure multiplex platforms. South America records steady progress, led by Brazil's public-private oncology partnerships and Argentina's inclusion of genomic testing in national guidelines. Varying reimbursement coverage still restricts volume but long-term incidence trends underpin latent demand.