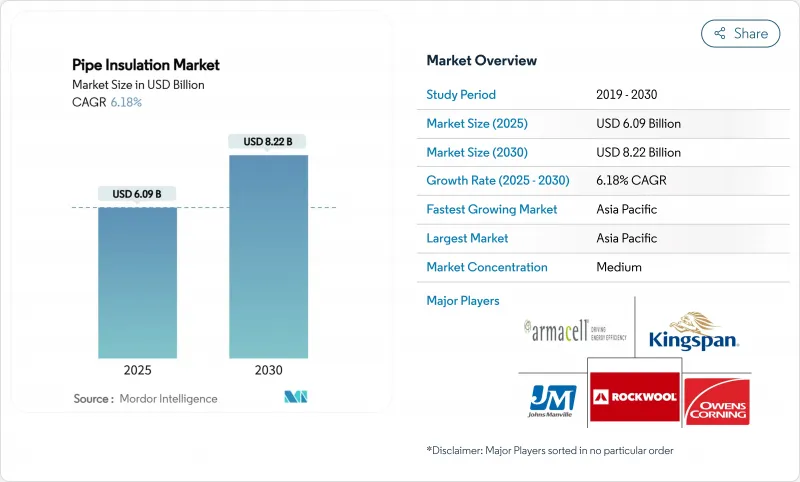

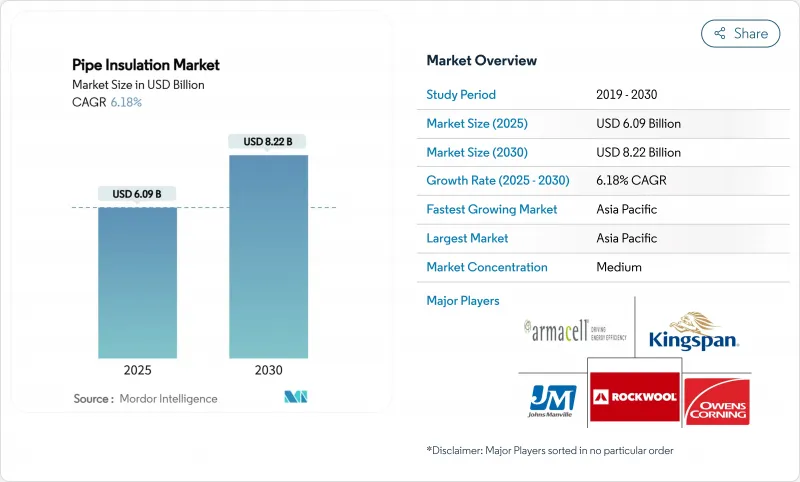

파이프 단열재 시장 규모는 2025년에 60억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.18%로 성장할 전망이며, 2030년에는 82억 2,000만 달러에 달할 것으로 예측됩니다.

건축 에너지 규제의 강화, 산업계의 탈탄소화 의무, 인프라의 잇따른 갱신에 의해 파이프 단열재 시장은 견조한 성장을 계속하고 있습니다. 북미와 유럽의 건축 규제는 보다 두껍고 고성능의 단열재를 요구하고, 아시아태평양 정부는 공공 부문에 대한 대출을 입증 가능한 에너지 절약 목표와 연결하고 있습니다. LNG 수출 능력 증대와 4세대 지역 난방 네트워크는 기존의 건물에 비해 대응 가능한 기회를 훨씬 넓히고 있습니다. 선도적인 기존 기업이 지역 기업을 통합하고 스마트 센서 플랫폼에 투자하며 고급 에어로겔 기술 라이선스를 취득함에 따라 경쟁이 치열해지고 있습니다. 석유화학 원료의 가격 변동 및 얇은 플라스틱 배관의 보급에 의해 단기적인 이익은 축소되고 있는 것, 다양한 재료 포트폴리오와 조립식 설치 솔루션을 가진 제조업체는 세계적인 탄소 중립의 스케줄이 가속하는 가운데, 상승 국면을 파악하는 입장에 있습니다.

건축기준법은 파이프 단열재를 재량적인 항목에서 법적 요건으로 바꾸고 있습니다. 2024년 국제 에너지 절약 기준(IECC)에서는 온수 파이프라인에 최대 5인치의 두께를 의무화하고 있으며, 이 규칙에 따라 미국에서는 주택 용지의 에너지 사용량이 7.80% 삭감될 것으로 예상되고 있습니다. 캘리포니아의 Title 24와 유사한 유럽 지침은 최저 R값을 규정하고 있으며, 저성능 랩은 사실상 제외됩니다. 미국에서는 이미 14개 주가 2024년 IECC로 가는 길을 걷고 있으며, Northeast Energy Efficiency Partnerships는 조기 채용자에 대해 6.80%의 소스 에너지 절감을 예측했습니다. 상업 시설은 이러한 요구 사항을 반영하여 소유자가 초기 비용보다 라이프사이클의 에너지 절약을 우선하도록 촉구합니다.

미국 멕시코 걸프를 따라 액화 천연 가스 수출 터미널은 19,800 마일 이상의 신규 또는 교체 배관이 필요하며, 대부분은 -160°C 작동 온도용으로 설계되었습니다. 상압 에어로겔 파이프 인 파이프 설계는 수축 응력을 허용 범위 내로 유지하면서 설치 비용을 절감합니다. 아시아태평양에서 부체식 LNG 허브가 가동됨에 따라 장기적인 해저 절연 마일에 대한 수요가 높아지고 프리미엄 재료의 가격도 상승하고 있습니다. 극저온 등급 폴리우레탄과 다공질 유리 제품 라인을 갖춘 제조업체는 마진 상승을 즐길 수 있으며, 다년간의 메가 프로젝트에서 조기 계약을 받았습니다.

스프레이 폴리우레탄 폼과 다층 자켓팅의 현장 시공에는 자격을 갖춘 작업자와 특수 설비가 필요하며, 대도시 시장에서는 시공비가 선형 피트당 15달러를 초과합니다. 리노베이션 후 에너지 비용은 30% 감소할 수 있지만, 베터 빌딩스 네이버후드(Better Buildings Neighborhood)의 데이터에 따르면 1달러를 투자해도 첫해 절약 효과는 불과 0.08달러로 주택 소유자의 투자 회수 기간이 연장됩니다. 조립식 파이프 스풀은 기술 격차를 부분적으로 해소하지만, 12인치를 초과하는 직경에서는 운송의 제한이 보급의 방해가 되고 있습니다. 노동력 부족이 가장 심각한 것은 북유럽이며, 고령화한 장인들은 견습생들이 직업훈련 프로그램에 들어가는 것보다 빨리 퇴직해 버립니다. 생산자는 현장 노동력을 최대 40% 절감하는 스냅 핏식 광물 섬유 쉘이나 자기 점착성 에어로겔 랩으로 대응하고 있지만, 보급은 늦어지고 있습니다.

유리 섬유는 저비용과 0.04W/(m*K)에 가까운 λ값에 지지되어 2024년 파이프 단열재 시장 점유율 39.65%의 선두를 유지했습니다. Rockwool 브랜드는 고유의 내화성 및 순환성의 주장을 활용하여 2023년 매출을 평생 예상 에너지 절약량 818TWh로 환산했습니다. 실리케이트는 600℃ 이상의 틈새 정유소 및 발전소 라인에서 사용되며, 경질 폴리우레탄 폼은 바이오의 배합으로 0.02W/(m*K) 이하의 도전율을 실현하고 있습니다. 고무 발포체는 열 사이클에 의해 구부러지기 때문에 HVAC의 스테디셀러로 계속되고 있습니다.

다른 유형(주로 에어로겔 담요 및 다공질 유리)은 거대한 프로젝트가 초저열 손실을 요구하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 7.51%에서 급성장합니다. 차세대 Si3N4 강화 에어로겔의 밀도는 0.033g/cm3로 낮아 893℃의 온도차를 견뎌냅니다. 다공질 유리는 LNG와 극저온 파이프라인에 흡수 제로와 100년의 설계 수명을 어필하고 있습니다. 높은 설비 투자는 유지 보수에 의해 상쇄되기 때문에 공정 소유자는 고급 재료를 선호하는 성능 기반 입찰을 지정합니다.

아시아태평양은 파이프 단열재 시장을 독점하고 있으며, 그 규모는 정책 지원과 결합되어 있습니다. 중국의 성 당국은 현재 건축 허가를 검증된 열에너지 모델과 연계하고 있으며, 에너지 절약을 위한 국가 3년 행동 계획에서는 배관 단열을 Tier-1 대책으로 특정하고 있습니다. 인도의 신재생에너지 통합을 추진함으로써 공정 산업은 증기라인 손실을 줄여야 하고 광물섬유 라미네이트 쉘에 대한 수요가 증가하고 있습니다. 아시아 개발 은행의 협력 대출 도구는 그린 필드 열 네트워크 프로젝트의 위험을 줄이고 안정적인 자재 인출을 보장합니다.

북미는 LNG 파이프라인의 전개와 법규제의 갱신으로부터 혜택을 받습니다. 미국 DOE가 2024년판 IECC에 의한 주택 에너지 절약률을 7.80%로 확인함으로써 각 주는 비용 효과적인 긴 논의 없이 도입에 착수할 수 있습니다. 단열재 비용의 30%를 다루는 연방 세액 공제는 투자 회수를 더욱 단축합니다. 캐나다의 각 국가는 저금리 리노베이션 대출을 활용하고, 앨버타의 산업 관계자는 연료 비용을 버퍼링하기 위해 고효율 재킷으로 전환하여 원료 변동을 헤지하고 있습니다.

유럽의 야망은 파리 같은 도시에서 2042년까지 지역 냉방 파이프를 3배로 하는 것이며, 2030년까지 3,500만 동의 건물의 개수를 목표로 하는 EU 리노베이션의 물결과 얽혀 있습니다. 스칸디나비아 시장에서는 생물 기원 바인더를 사용한 탄소 마이너스 단열재가 시험되어 전문 제조업체에게 조기 수익을 가져오고 있습니다. 유틸리티자는 단열재 계약을 히트 펌프 조달과 번들로 공급자와의 협상을 총소유비용(TCO) 메트릭으로 전환하고 있습니다.

The Pipe Insulation Market size is estimated at USD 6.09 billion in 2025, and is expected to reach USD 8.22 billion by 2030, at a CAGR of 6.18% during the forecast period (2025-2030).

Tighter building-energy codes, industrial decarbonization mandates, and a wave of infrastructure upgrades keep the pipe insulation market on a firm growth footing. North American and European building regulations demand thicker, higher-performance insulation, while Asia-Pacific governments link public-sector lending to demonstrable energy-savings targets. LNG export capacity additions and fourth-generation district heating networks extend the addressable opportunity well beyond conventional buildings. Competitive intensity has risen as large incumbents consolidate regional players, invest in smart-sensor platforms, and license advanced aerogel technologies. Although price volatility for petrochemical feedstocks and the spread of thin-wall plastic piping temper short-term margins, manufacturers with diversified materials portfolios and prefabricated installation solutions remain positioned to capture upside as global carbon-neutrality timetables accelerate.

Building codes are turning pipe insulation from a discretionary line item into a legal requirement. The 2024 International Energy Conservation Code (IECC) mandates thicknesses of up to 5 inches for hot-water pipelines, a rule expected to cut residential site-energy use by 7.80% in the United States. California's Title 24 and similar European directives specify minimum R-values, effectively sidelining low-performance wraps. With 14 U.S. states already on the 2024 IECC path, Northeast Energy Efficiency Partnerships forecasts 6.80% source-energy savings for early adopters. Commercial facilities mirror these requirements, pushing owners to favor lifecycle energy savings over upfront costs-another lever that expands the pipe insulation market.

Liquefied-natural-gas export terminals along the U.S. Gulf Coast require more than 19,800 miles of new or replacement piping, much of it designed for -160 °C operating temperatures. Ambient-pressure aerogel pipe-in-pipe designs cut installation costs while keeping contraction stresses within allowable limits. As Asia-Pacific commissions floating LNG hubs, demand for long-run subsea insulation miles pushes premium material pricing. Manufacturers with cryogenic-grade polyurethane or cellular glass lines enjoy margin upside and early-mover contracts on multi-year megaprojects.

Field application of spray polyurethane foam and multi-layer jacketing requires certified crews and specialized rigs, pushing installation charges above USD 15/linear foot in large metro markets. Although energy bills can drop 30% post-retrofit, Better Buildings Neighborhood data show that every USD 1 invested yields only USD 0.08 in first-year savings, stretching homeowner payback horizons. Prefabricated pipe spools partially solve the skills gap, yet transport limits hamper uptake for diameters above 12 inches. Labor scarcity is most acute in Northern Europe, where aging tradespeople retire faster than apprentices enter vocational programs. Producers respond with snap-fit mineral-fiber shells and self-adhesive aerogel wraps that cut site labor by up to 40%, but widespread adoption lags.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fiberglass maintained the leading 39.65% pipe insulation market share in 2024, underpinned by low cost and a λ-value near 0.04 W/(m*K). Rockwool leverages inherent fire resistance and circularity claims; the brand's 2023 sales translated to anticipated lifetime energy savings of 818 TWh. Silicate wraps own niche refinery and power-plant lines above 600 °C, while rigid polyurethane foams post sub-0.02 W/(m*K) conductivities in bio-based formulations. Rubber foams remain HVAC staples because they flex with thermal cycling.

Other Types-primarily aerogel blankets and cellular glass-grow fastest at 7.51% CAGR through 2030 as mega-projects demand ultra-low heat loss. Next-gen Si3N4-reinforced aerogels come in at densities as low as 0.033 g/cm3 withstanding 893 °C differentials. Cellular glass appeals to LNG and cryogenic pipelines for zero water absorption and 100-year design life. Higher capex is offset by maintenance savings, leading process owners to specify performance-based tenders that favor premium materials.

The Pipe Insulation Market Report is Segmented by Type (Fiberglass, Rockwool, Silicates, Polyurethane, Rubber Foams, Other Types), End-User Industry (Buildings and Construction, Oil and Gas, Transportation, General Industrial, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominates the pipe insulation market, pairing volume scale with policy support. Chinese provincial authorities now tie building permits to verified thermal-energy models, and the national Three-Year Action Plan for energy conservation identifies pipework insulation as a Tier-1 measure. India's renewable-integration drive requires process industries to cut steam line losses, sending demand toward laminated mineral-fiber shells. The Asian Development Bank's blended-financing tools de-risk greenfield heat-network projects, assuring steady material off-take.

North America benefits from LNG pipeline rollouts and code updates. The U.S. DOE's confirmation of 7.80% residential energy savings from the 2024 IECC emboldens states to adopt without lengthy cost-effectiveness debates. Federal tax credits covering 30% of insulation spend further shorten paybacks. Canadian provinces tap low-interest retrofit loans, while industrial players in Alberta hedge feedstock volatility by switching to higher-efficiency jacketing to buffer fuel bills.

Europe's ambition is to treble district cooling pipes by 2042 in cities like Paris, intertwining with the EU Renovation Wave that targets 35 million building upgrades by 2030. Scandinavian markets trial carbon-negative insulation made with biogenic binders, providing early revenue for specialty manufacturers. Utilities bundle insulation contracts with heat-pump procurement, shifting supplier negotiations toward total-cost-of-ownership metrics.