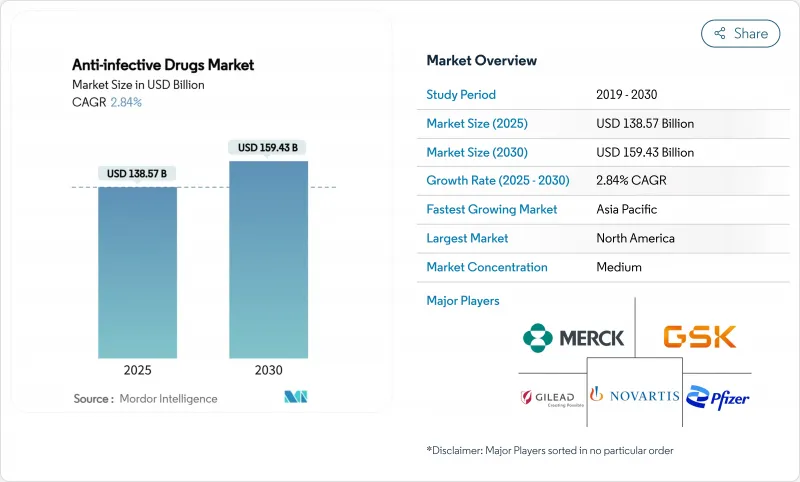

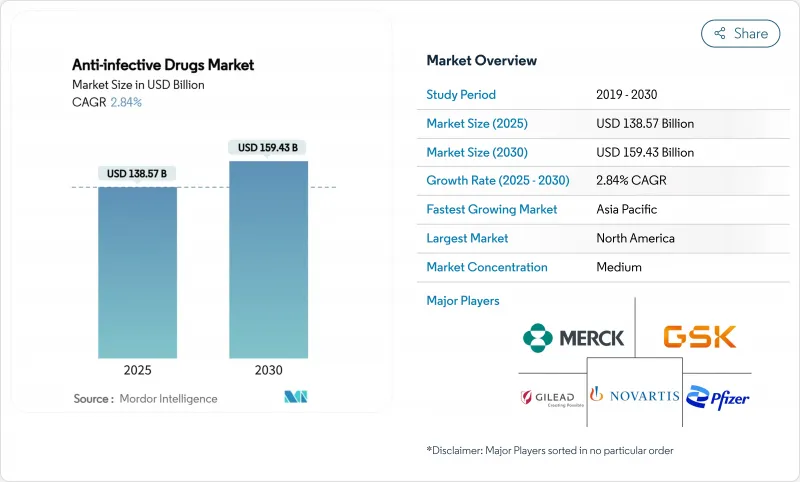

항감염제 시장 규모는 2025년에 1,385억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 2.84%로, 2030년에는 1,594억 3,000만 달러에 달할 것으로 예상됩니다.

항감염제 시장의 꾸준한 확대는 항균제 내성(AMR) 증가를 배경으로 공중 보건 긴급 수요, 규제 인센티브 및 지속적인 R&D 기금에 의해 지원됩니다. 암메트 니즈가 높은 감염에 대한 항균제 개발 경로를 합리화하는 FDA의 2025년 6월의 최종 지침으로 대표되는 바와 같이, 규제 환경은 여전히 지원적입니다. 전 세계 의약품 원료 생산 능력의 67%가 인도와 중국에 집중되어 있으며, 항감염제 시장을 지정학적 및 물류 위험에 노출시켜 공급망의 취약성이 계속되고 있습니다. 한편, 기술에 뒷받침된 스튜어드십 이니셔티브와 AI 주도의 탐색 파트너십이 내성 병원체에 대처하는 새로운 치료제를 지지하고, 성숙하고 있는 제1세대의 약물 클래스가 전체적인 성장에 미치는 마이너스면의 영향을 완화하고 있습니다.

대부분의 건강 관리 시스템에서 패혈증과 관련된 입원 일수, 비용 및 사망률이 계속 증가하고 있으며 신뢰할 수 있는 항감염 요법에 대한 수요가 증가하고 있습니다. 노인과 면역 결핍 환자에서 신속하고 광범위한 스펙트럼 치료가 필요한 심각한 감염으로 고통받는 빈도가 높아지고 입원 기간이 장기화되고 평균 재원 일수는 유행 이전 수준을 초과합니다. 질병의 유행은 AI를 활용한 신속 진단 플랫폼에 대한 투자를 촉진하고, 동정에 걸리는 시간을 몇 시간 단축함으로써, 보다 조기 및 적정한 치료를 가능하게 하고 있습니다. 세계의 정책 입안자들은 풍부한 사람들을 대상으로 하는 지역 기반의 감염 프로그램에 자원을 돌리며 항감염제 시장에서 분산 치료 모델을 형성하는데 기여하고 있습니다. 그 결과 전통적인 의약품 가격 하락을 상쇄하고 성숙한 경제권에서도 판매량의 성장을 유지하는 지속적인 수요 기반이 형성되는 것입니다.

폐렴 간균(Klebsiella pneumoniae)과 아시네토박터 바우만니(Acinetobacter baumannii)의 고내성 균주는 현재 세계 병원을 달리고 있으며, 아시아태평양에서는 카바페넴 내성이 31.3%로 상승하고 B-락탐/B-락타마제 의약품의 파이프라인은 돌연변이 장벽을 몇 자리수 상승시키는 이중 결합 부위 항생제 등 내성균의 출현을 억제하는 메커니즘을 우선하게 되어 왔습니다. 경제적인 영향도 큽니다. 내성 감염은 입원 기간을 늘리고 비용이 많이 드는 진단을 필요로 하므로 지불자의 예산이 줄어들어 가치 기반 가격 협상을 강요할 수 있습니다. 지리적 편차는 두드러지며 남미는 세계적인 내성 곡선을 선도하고 있는 반면, 니트로프란토인은 북미와 서유럽의 요중 분리주에 널리 유효합니다. 감시의 강화와 새로운 작용기전 분자에 대한 인센티브는 항감염제 시장에서 혁신자에게 새로운 수익의 여지를 가져옵니다.

베다키린 내성은 이미 세계에서 5.7%에 달하고 남아프리카에서는 10.4%로 피크에 달하여 다제 내성 결핵의 치료 기간을 단축하고 있습니다. 병원에서는 반코마이신 내성 장구균과 카르바페넴 내성 아시네토박터 증가율이 보고되어 있어 경험적 치료를 복잡하게 하고 사망률을 상승시키고 있습니다. 제약회사는 내성균이 제품 수명을 줄이고 한때 수십년의 수익을 가져온 기존의 광역 스펙트럼 클래스에 대한 투자를 억제하기 때문에 수익 감소에 직면하고 있습니다. 지불자는 내성 억제 효과가 입증된 약제에 프리미엄 가격을 설정하고 신규 메커니즘이 없는 약제의 톱 라인의 전망을 억제함으로써 대응하고 있습니다. 임상적, 경제적으로 복합적인 타격은 항감염제 시장의 장기적인 기세를 약화시키고 있습니다.

B-락탐계 항균제, 마크로라이드계 항균제, 카바페넴계 항균제에 대한 임상적 의존도가 병원 프로토콜에서 여전히 높은 점에서 항균제는 항감염제 시장 점유율의 43.08%를 차지했습니다. 그러나 내성의 지속과 스튜어드십에의 대처에 의해 판매량의 성장에는 톱니가 걸려, 2025년 2월에 FDA의 인가를 취득한 아즈트레오남과 아비박탐과 같은 차세대 콤비네이션을 목표로 한 연구 개발 투자가 행해지고 있습니다. 항바이러스제는 HIV, RSV, 간염의 제제가 장시간 작용형 주사제나 항체 칵테일로 이행하여, 분기 또는 반기에 한 번의 투여가 가능하게 되었기 때문에 CAGR 전망에서 가장 견조한 4.73%를 나타낼 전망입니다. 이 혁신적인 파이프라인을 통해 이 부문은 항감염제 시장에서 전략적인 성장 엔진으로 재지정되었습니다.

획기적인 호흡기계 항바이러스제는 유행 대책 예산에 의한 공급 능력의 급증과 비축의 혜택도 받고 있습니다. 벤처기업에 의한 생명공학 진입이 좁은 스펙트럼 박테리오파지를 도입하는 한편, 브랜드명이 있는 기존 기업이 성숙한 클래스의 바이오시밀러로부터 점유율을 지키기 때문에 경쟁의 격렬함이 증가하고 있습니다. 따라서 가격과 수량의 역학은 다릅니다. 항생제는 대규모 도입량에 의해 상쇄된 완만한 가격 하락을 눈에 띄는 반면, 항바이러스제는 비싼 가격 설정이 되고 있지만, 치료 환자수는 적습니다. 이러한 상호작용은 전반적인 수익 성장을 유지하고 장기적인 R&D 자본 배분을 형성합니다.

HIV 치료제는 인테그라제 억제제 백본의 보급과 노출 전 예방요법(PrEP)의 침투로 2024년 항감염제 시장 규모의 27.33%를 나타냈습니다. 레나카파빌의 잠재적인 연간 생산 비용은 40달러이기 때문에 LMIC에 대한 접근이 확대되고 서유럽의 성숙 시장이 두드러지게 되는 가운데도 수량은 안정됩니다. 한편 호흡기 바이러스 감염증은 닐세비맙에서 유아의 입원이 78% 감소했다는 데이터를 받아 RSV 예방약이 기세를 늘리고 CAGR이 4.51%를 나타낼 것으로 예측됩니다.

결핵은 여전히 주요 임상적 초점이며, 6개월간의 BPaL/M 요법의 단축에 의해 2026년까지 전 세계에서 12만 6,792명의 환자를 치료해, 총 치료 일수를 단축해 의료 시스템의 비용 부담을 경감할 것으로 예측되고 있습니다. 처음 1시간 이내에 광범위한 커버리지를 선호하는 패혈증 프로토콜은 4.9배의 생존 이익을 가져오고, 응급 상황에서 즉시 재투여 가능한 주사제에 대한 수요를 강화하고 있습니다. 이러한 다양한 적응증은 항감염제 시장의 다양화를 강화하고 특정 병원체 부위에 대한 의존도를 감소시킵니다.

북미는 확립된 혁신 생태계, 동적 지불자 구성, 신규 약제의 조기 도입으로 2024년 매출의 33.74%를 차지했습니다. FDA의 미충족 요구사항은 간소화되고 과학적 조언의 사이클은 단축되었으나, 시판 후의 시험 의무가 높아짐에 따라 제조업체가 가격 모델에 포함시켜야 하는 컴플라이언스 비용이 증가하고 있습니다. 미국의 패혈증 환자 수는 연간 250만 명, 총 비용은 521억 달러로 광역 스펙트럼의 주사제의 안정적인 이용을 지원하고 처방전의 교체를 촉진하고 있습니다. 캐나다와 멕시코는 남북 무역의 흐름에 대응하는 특수한 충전·마무리 능력을 제공하는 것으로, 이 지역의 풋 프린트를 증강하고 있지만, 의약품 가격 통제의 차이가 상업적인 고려 사항으로서 남아 있습니다.

유럽은 AMR에 대한 통일된 전략적 자세를 보여줍니다. EU의 약사법 개정은 내성균 모니터링 요건을 조화시켜 기업이 모든 회원국에 대해 단일 감시 계획을 제출할 수 있게 되었습니다. GSK와 영국의 AMR 프로그램으로 대표되는 관민 연계는 리스크 분담 자금 제공에 의해 후기 단계의 항생제 후보를 가속화하는 방법을 보여줍니다. 그러나 남유럽의 긴축재정은 고가 약제의 상환을 제한하고 전유럽 평균 판매가격을 압박하는 가격 전략의 차이를 강요하고 있습니다. 브레그짓은 규제의 분기를 가져오고, 기업은 완전한 시장 진입을 달성하기 위해 두 개의 승인 채널을 구분합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 3.77%를 나타낼 것으로 예측되며 항감염제 시장에서 가장 급성장하고 있는 지역입니다. 중국은 세계 항생제 활성 성분의 생산량을 독점하고 있으며, 국가의 AMR 우선 과제에 따라 17개 현지 기업에 의한 20개의 항균제 프로젝트를 보유하고 있습니다. 인도는 비용 경쟁력 있는 화학 능력을 활용하고 있지만 장기적인 제조 오버헤드를 증가시킬 수 있는 환경 배출 규제를 추진하고 있습니다. 일본에서는 우선순위가 높은 항균제의 신속 승인 패스웨이로 시장 투입까지의 기간을 최대 12개월 단축하고 있습니다. 호주는 혁신적인 항균제 시장 진출보 장금에 자금을 제공하여 현지 공급을 보호하고 있습니다. 그러나, 카바페넴 내성이 31.3%로 지역적으로 높기 때문에 임상상의 긴급성이 높아지고, 내성 억제의 데이터가 제대로 얻어지고 있는 약제가 우선적으로 조달되고 있습니다.

The Anti-infective Drugs Market size is estimated at USD 138.57 billion in 2025, and is expected to reach USD 159.43 billion by 2030, at a CAGR of 2.84% during the forecast period (2025-2030).

This steady expansion in the anti-infective drugs market is sustained by urgent public-health demand, regulatory incentives, and sustained R&D funding against a backdrop of rising antimicrobial resistance (AMR). The regulatory environment remains supportive, exemplified by the FDA's June 2025 final guidance that streamlines antibacterial development pathways for high-unmet-need infections. Supply-chain vulnerabilities persist because 67% of global active-pharmaceutical-ingredient capacity clusters in India and China, exposing the anti-infective drugs market to geopolitical and logistics risk. Meanwhile, technology-enabled stewardship initiatives and AI-driven discovery partnerships underpin new therapeutics that address resistant pathogens, tempering the downside impact of maturing first-generation drug classes on overall growth.

Sepsis-linked inpatient stays, costs and mortality continue to rise in most healthcare systems, magnifying demand for reliable anti-infective regimens. Older adults and immunocompromised patients now present more frequently with severe infections that require prompt, broad-spectrum cover, lengthening inpatient admissions and driving average lengths of stay above pre-pandemic levels. Heightened disease prevalence has stimulated investment in AI-enabled rapid-diagnostic platforms that can shave hours off identification times, thus enabling earlier and more targeted therapy. Global policymakers channel resources toward community-based infection programs that serve disadvantaged groups, helping shape decentralized treatment models in the anti-infective drugs market. The net effect is an enduring demand baseline that offsets price erosion in traditional molecules and anchors volume growth even in mature economies.

Hyper-resistant strains of Klebsiella pneumoniae and Acinetobacter baumannii now circulate across hospitals worldwide, lifting carbapenem resistance to 31.3% in Asia-Pacific and prompting urgent shifts toward B-lactam/B-lactamase inhibitor combinations. Pharmaceutical pipelines increasingly prioritize mechanisms that impede resistance emergence, such as dual-binding site antibiotics that raise mutation barriers by several orders of magnitude. Economic implications are material: resistant infections lengthen hospital stays and require costlier diagnostics, diluting payer budgets and forcing value-based price negotiations. Geographic variation is pronounced; South Asia leads global resistance curves, whereas nitrofurantoin remains broadly effective against urinary isolates in North America and Western Europe. Heightened surveillance and incentives for novel mode-of-action molecules create fresh revenue headroom for innovators within the anti-infective drugs market.

Bedaquiline resistance has already reached 5.7% globally, peaking at 10.4% in South Africa, compressing therapeutic windows for multidrug-resistant tuberculosis. Hospitals report rising vancomycin-resistant Enterococcus and carbapenem-resistant Acinetobacter rates, complicating empiric therapy and elevating mortality. Pharmaceutical firms confront diminishing returns as resistance shortens product life, deterring investment in traditional broad-spectrum classes that once delivered decades of revenue. Payers respond by limiting premium pricing to drugs with demonstrable resistance-suppression properties, constraining top-line prospects for molecules lacking novel mechanisms. The compounding clinical and economic toll moderates the longer-term momentum of the anti-infective drugs market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Antibiotics delivered a 43.08% market share of the anti-infective drugs market share, as clinical reliance on B-lactams, macrolides, and carbapenems remained heavy in hospital protocols. Persistent resistance and stewardship initiatives, however, have capped volume growth, channeling R&D investment toward next-generation combinations such as aztreonam-avibactam, which gained FDA clearance in February 2025. Antivirals posted the most robust 4.73% CAGR outlook as HIV, RSV, and hepatitis formulations shift to long-acting injectables and antibody cocktails that promise quarterly or semi-annual dosing convenience. That innovation pipeline repositioned the segment as a strategic growth engine inside the anti-infective drugs market.

Breakthrough respiratory antivirals also benefit from pandemic preparedness budgets that bankroll surge capacity and stockpiling. Competitive intensity deepens as brand-name incumbents defend share against biosimilars in mature classes while venture-backed biotech entrants introduce narrow-spectrum bacteriophages. Price-volume dynamics therefore diverge: antibiotics witness modest price erosion offset by large installed volume, whereas antivirals command premium pricing but face smaller treated-patient bases. The interplay sustains overall revenue growth and shapes long-term R&D capital allocation.

HIV therapy retained 27.33% of the anti-infective drugs market size in 2024 thanks to widespread adoption of integrase inhibitor backbones and growing uptake of pre-exposure prophylaxis (PrEP). Lenacapavir's potential annual production cost of USD 40 invites broader LMIC access, underpinning volume stability even as mature Western markets plateau. In contrast, respiratory virus infections are projected to log a 4.51% CAGR as RSV prophylaxis gains momentum following data showing a 78% reduction in infant hospitalizations with nirsevimab.

Tuberculosis remains a major clinical focus, with shorter six-month BPaL/M regimens projected to treat 126,792 patients globally by 2026, shrinking total therapy days and reducing health-system cost burdens. Sepsis protocols that prioritize broad-spectrum coverage within the first hour have driven a 4.9-fold survival benefit, intensifying demand for ready-to-reconstitute injectables in emergency settings. These varied indication trajectories collectively reinforce the anti-infective drugs market diversification, lessening dependence on any single pathogen area.

The Anti Infective Drugs Market Report is Segmented by Drug Class (Antibiotics, Antivirals, Antifungals, Antiparasitics), Indication (HIV Infection, Pneumonia, and More), Route of Administration (Oral, Parenteral, and More), Distribution Channel (Hospital Pharmacy, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 33.74% of 2024 revenue through an entrenched innovation ecosystem, dynamic payer mix, and early adoption of novel agents. The FDA's streamlined unmet-need guidance reduces scientific advice cycles, yet heightened post-market study obligations inflate compliance costs that manufacturers must factor into pricing models. U.S. sepsis admissions number 2.5 million annually with aggregate costs of USD 52.1 billion, anchoring steady utilization of broad-spectrum injectables and driving formulary turnover. Canada and Mexico augment the regional footprint by contributing specialized fill-finish capacity that feeds northbound and southbound trade flows, though divergent pharmaceutical price controls remain a commercial consideration.

Europe exhibits a unified strategic stance against AMR. Revised EU pharmaceutical legislation harmonizes resistance-monitoring requirements, enabling companies to file a single surveillance plan for all member states. Public-private alliances exemplified by the GSK-UK AMR program demonstrate how shared-risk funding accelerates late-stage antibiotic candidates. However, austerity in Southern Europe constrains reimbursement for premium-priced agents, forcing differential pricing strategies that weigh on pan-European average selling prices. Brexit introduces regulatory bifurcation, with companies navigating dual approval channels to achieve full market reach.

Asia-Pacific is projected to grow at 3.77% CAGR to 2030, making it the fastest-expanding component of the anti-infective drugs market. China dominates global antibiotic active-ingredient output and hosts 20 antibacterial projects across 17 local firms that align with national AMR priorities. India leverages cost-competitive chemistry capabilities but grapples with environmental discharge controls that could raise long-term manufacturing overhead. Japan's expedited approval pathway for high-priority antimicrobials shortens time-to-market by up to 12 months, while Australia funds market-entry rewards for innovative antibiotics to safeguard local supply. Yet, elevated carbapenem resistance 31.3% regional prevalence amplifies clinical urgency and shapes procurement preferences toward agents with robust resistance-suppression data.