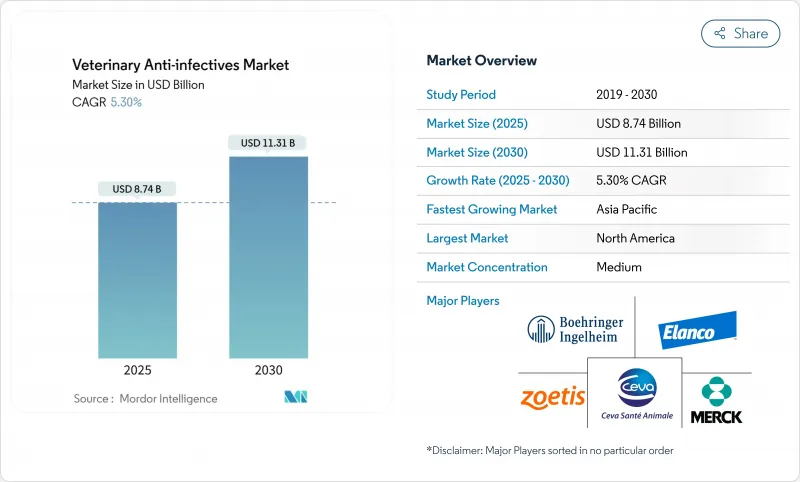

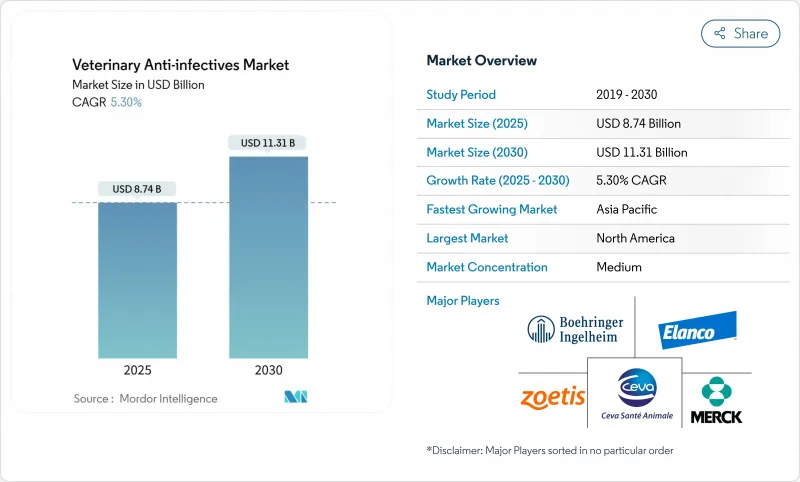

동물용 항감염제 시장은 2025년에 87억 4,000만 달러에 이르며, CAGR 5.3%를 나타내 2030년에는 113억 1,000만 달러에 이를 것으로 예측되고 있습니다.

항감염제는 호흡기 감염, 장내 감염, 피부 감염의 관리에 필수적이므로 수요는 식용 동물과 반려동물 모두에 퍼져 있습니다. 특히 아시아태평양에서는 가축의 증산이 진행되고 수요가 높아지고 있습니다. 한편 신흥경제국에서는 반려동물 사육 증가와 '인간화' 동향으로 프리미엄 제품 판매가 확대되고 있습니다. 각국 정부는 동시에 항감염제 관리규칙을 강화하고 정밀투여기술, 표적제제, 내성을 완화하는 대체약에 대한 투자를 촉진하고 있습니다. 동물용 항감염제 시장에서 각 회사는 규모, 규제에 관한 전문 지식, 소비자에게 직접 판매를 요구하고 있기 때문에 제조업체 간의 통합과 디지털 약국 채널에 대한 축족이 경쟁 전략을 더욱 형성하고 있습니다.

가금류에서 H5N1이 빈발하고 미국의 낙농우군에서 최근 검출되었기 때문에 종을 넘은 감염 위험에 대한 인식이 높아져, Elanco와 Medgene의 긴급 백신 공동 개발이 촉진되었습니다. 감시 보고에 따르면 신흥 감염의 75%는 인수 공통 감염이며 수의 당국은 모니터링 예산을 늘리고 신속 진단 승인을 신속하게 진행하게 되었습니다. Zoetis는 기준 실험실 품질 결과를 제공하고 치료 결정을 가속화하며 데이터 중심의 항감염제 스튜어드십을 지원하는 AI 대응 임상 혈액학 분석기를 발표했습니다. 그 결과, 동물용 항감염제 시장 전체에서 광역 스펙트럼과 장시간 작용형의 약제에 대한 수요가 증가하고 있습니다. 각국 정부는 또한 인간과 동물의 역학 데이터를 통합하는 One-Health 이니셔티브에 자금을 제공하고, 항감염제의 비축을 위한 지속적인 조달 파이프라인을 구축하고 있습니다. 바이오 보안에 대한 투자가 증가함에 따라 확장 가능한 제조 및 규제에 익숙한 공급업체가 경쟁력을 얻고 있습니다.

반려동물의 사육률은 2025년에 다시 상승했지만 미국 주인의 절반 이상이 주로 비용 측면에서 우려를 받고 적어도 하나의 의료 서비스를 미루고 있습니다. 이러한 경제적인 갭은 세포베신과 같은 장시간 작용형 주사제에 대한 관심을 높이고 있습니다. 기업의 진료 그룹과 보험사는 진단과 처방을 번들로 한 웰니스 플랜 모델을 시험적으로 도입하고 동물용 항감염제 시장에서의 프리미엄 치료제의 예측 가능한 보급을 지원하고 있습니다. 베링거 잉겔하임이 2024년 사이버 애니멀헬스를 인수함에 따라 개 만성질환의 치료용 백신 제조를 목적으로 한 바이러스양 입자 플랫폼이 추가되어 신규 치료법에 대한 폭넓은 수요가 반영되고 있습니다. 텔레토리아지와 전자 처방전 서비스는 급속히 확대되고 있으며, 지금까지 충분한 치료를 받지 않았던 주인을 공식적인 치료 경로로 이끌어 항감염제의 처방 기반을 확대하고 있습니다. 디지털 약국은 이러한 서비스와 원활하게 통합되어 야간 납품 및 자동 리필 알림을 제공하고 컴플라이언스를 강화합니다.

사하라 이남의 아프리카에서는 의약품의 5분의 1이 품질 표준을 충족시키지 못하고 치료 성적을 위협하고 내성을 가속화하고 있다는 치료 보고서가 있습니다. 비정규 농업 동물 병원에 의존하는 단편 공급망은 인기있는 브랜드 이름을 씌운 위조품의 침입을 초래합니다. 다국적 제조업체가 시작한 직렬화와 블록체인을 통한 추적조사의 시험운용은 기술적 실현가능성을 나타내고 있지만, 이익률이 낮은 농촌시장에 대해서는 여전히 비용이 높습니다. ECOWAS를 포함한 지역 경제권은 비정규 수입을 막기 위해 등록 과정의 조화를 시작했지만 집행 능력은 늦었습니다. 이러한 확산은 브랜드 자금을 낮추고 스튜어드십을 복잡하게 하여 동물용 항감염제 시장의 가치 성장을 억제합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년 동물용 항감염제 시장에서 가장 큰 수익을 올린 것은 소였으며 점유율은 39.7%였습니다. 소용 항감염제 시장 규모는 대규모 소군 경영이 복용량을 억제하면서 1회당 가치를 높이는 정밀투여 툴을 채용함에 따라 꾸준히 성장할 것으로 예측됩니다. 한편, 가금은 중국, 인도, 브라질에서 육계 생산 능력의 확대에 힘입어 2030년까지의 CAGR이 6.4%를 나타내 다른 모든 동물종을 웃도는 것으로 예측됩니다. 수출업체가 잔류 규제 강화에 대응하기 때문에 휴약 시간이 짧은 조류 전용의 제제가 보급됩니다. 양돈업자는 이유 후 설사와 아프리카 돼지 열 위협과의 싸움을 계속하고 있으며 항생제와 면역조절 사료 첨가물 수요를 지지하고 있습니다. 반려동물은 주인이 편리한 제형을 선호하기 때문에 여전히 프리미엄 틈새 시장이지만, 저소득층에서는 비용에 민감함이 구매 결정을 형성하고 있습니다.

암소 사육장에는 클라우드 대시보드에 연결된 RFID 귀 태그가 통합되어 수의사에게 불현성 질환을 경고합니다. 이러한 시스템은 질병주기의 초기 단계에서 사용되는 고 역가 주사제로 구매를 이동시키고 치료 성적이 향상됨과 동시에 투여 기간을 단축합니다. 가금류 통합자는 실시간 무리의 지표를 기반으로 복용량을 조정하는 워터 라인 투약 컨트롤러에 투자하여 가변 pH 환경을 위해 설계된 가용성 분말에 대한 수요를 높입니다. 수산 양식은 애틀랜틱 연어의 생산자가 파손에 의한 생물 방제나 나노캡슐화 항생제를 시험적으로 사용하고 있기 때문에 밀짚이나 비브리오 감염과 싸우기 때문에 전략적 프론티어로서 부상하고 있습니다. 동물용 항감염제 시장은 스튜어드십의 압력에서 개별 사용 패턴이 변화해도 다양한 동물종이 혼재하고 있기 때문에 바닥 단단합니다.

2024년 동물용 항감염제 시장 규모에서 항감염제의 점유율은 29.3%로, 여러 동물종에서 인가된 B-락탐계, 테트라사이클린계, 매크로라이드계의 폭넓은 카탈로그에 지지되었습니다. 스튜어드십의 대처에 의해 현재는 특정의 병원체를 대상으로 한 스펙트럼의 좁은 배합제가 선호되게 되어 있어, 대기업 브랜드 각사의 처방 변경 활동이 활성화하고 있습니다. H5N1, 돼지 생식·호흡기 증후군, 비단잉어 헤르페스 바이러스의 발생이 예방 대책의 갭을 드러내고 있기 때문에 항바이러스제의 CAGR은 가장 빠른 8.3%를 나타낼 것으로 예측됩니다. 뉴클레오시드 유사체 및 바이러스-유사 입자 백신의 개발 파이프라인은 치료 기간의 단축과 내성균 발생 가능성의 감소를 약속하고 있습니다. 항진균제는 매출 규모가 작은 것, 반려동물에 있어서의 마라세티아 및 아스페르길루스 감염증 증가에 대응하고 있으며, Otiserene이나 Mometamax Single과 같은 단회 투여의 안과용 겔은 컴플라이언스의 간소화에 의해 채용이 진행되고 있습니다. 콕시듐증과 바베시아증과 싸우는 풍토병 지역에서는 항원충제의 중요성이 유지되고 있으며, 현재 진행중인 톨트라즈릴 배합제의 임상시험에서는 멀티타겟 치료로의 변화가 강조되고 있습니다.

혁신의 파이프라인은 배달 강화에 집중하고 있습니다. 장시간 작용하는 주사 현탁액은 최대 2주에 걸쳐 안정한 혈장 농도를 유지하며, 복용 어드히어런스를 증가시키면서 재진단을 제한합니다. 물 안정성 마이크로 펠릿은 닭과 새우 연못에 균일하게 분산되어 침전물 낭비를 없앨 수 있습니다. 각 회사는 또한 돼지의 예방과 치료의 교량이되는 서방형 항바이러스 펩티드에 대한 생분해성 임플란트 매트릭스를 연구하고 있습니다. 이러한 진보를 종합하면, 동물용 항감염제 시장은 확립된 클래스와 동물종 특유의 질병 부담에 대응하는 획기적인 치료법이 균형있게 혼합되어 있을 것입니다.

북미는 첨단 수의학적인프라와 동물 1마리당 고액 지출을 배경으로 2024년에 최대 매출을 유지했습니다. FDA의 처방전 개혁을 통해 취미로 항생제를 구입하는 농가는 억제되었지만, 스튜어드십이 엄격화된 환경에서 개업의가 치료를 정당화하는 데 도움이 되는 진단약이나 정교한 투약 도구 수요는 자극되었습니다. 캐나다의 동물용 의약국(Veterinary Drugs Directorate)은 미국의 규제와 긴밀하게 연계되어 국경을 넘는 거래를 완화하고 신약의 라벨 확장의 조화를 촉진하고 있습니다. 멕시코는 통합 공급망에서 이익을 얻었지만, 구현 능력에 편차가 있기 때문에 다국적 기업은 브랜드 무결성을 보호하기 위한 교육 및 품질 보증 노력을 강조하고 있습니다.

유럽에서는 ESVAC 감시 네트워크를 통해 12년간 동물용 항생제 판매량의 50% 절감을 달성하여 세계에서 가장 엄격한 항감염제 사용 관리 체제를 제시하고 있습니다. 유통업체는 현재 EU의 중앙 집중화된 데이터베이스에 사용량을 보고하고 구매 및 공급업체와의 협상에 영향을 미치는 투명성을 확보하고 있습니다. 카테고리 B의 상한은 매출을 제1선택약으로 돌려보내는 것으로, 기업은 신규 신청서를 제출할 때 확고한 스튜어드십의 논거를 밝히도록 요구되고 있습니다. Brexit 후, 영국은 혁신적인 동물용 의약품에 패스트 트럭 절차를 도입해, 상시를 가속시켰지만, 내성균 대책으로서 약물감시의 후속을 유지하고 있습니다.

아시아태평양은 CAGR 7.2%를 나타내 가장 급성장하는 분야이며 중국과 인도의 단백질 선호도 확대와 동반 동물 시장의 성숙에 힘쓰고 있습니다. 낙농 및 육계 부문의 현대화를 목표로 하는 정부 프로그램은 바이오 보안을 우선시하고 있으며, 고품질 주사용 세프티오플 및 풀 페니콜 주문이 증가하고 있습니다. 동시에 중국에서는 제약공장의 배수에 대한 환경단속이 정기적으로 이루어져 원약의 수출이 제한되므로 테트라사이클린계 항생물질과 마크로라이드계 항생물질의 지역공급이 불안정해집니다. 일본의 농수성은 2026년부터 농장 수준에서 항생제의 연례 보고를 의무화하고 있지만, 이 선례는 ASEAN 전역에서 유사한 의무화를 촉진하여 동물용 항감염제 시장을 더욱 발전시킬 가능성이 있습니다.

The veterinary anti-infectives market reached USD 8.74 billion in 2025 and is forecast to climb to USD 11.31 billion by 2030, reflecting a 5.3% CAGR.

Robust demand spans both food-producing and companion animals as antimicrobial agents remain essential for managing respiratory, enteric, and dermatological infections. Livestock intensification, especially in Asia Pacific, is lifting volume needs, while rising pet ownership and "humanization" trends are expanding premium product sales in developed economies. Governments are simultaneously tightening antimicrobial stewardship rules, stimulating investment in precision-dosing technologies, targeted formulations, and alternatives that mitigate resistance. Consolidation among manufacturers and a pivot toward digital pharmacy channels further shape competitive strategies as companies seek scale, regulatory expertise, and direct-to-consumer reach within the veterinary anti-infectives market.

Frequent H5N1 outbreaks in poultry and recent detections in US dairy herds have heightened awareness of cross-species transmission risks, prompting emergency vaccine collaborations between Elanco and Medgene. Surveillance reports show 75% of emerging infectious diseases are zoonotic, leading veterinary authorities to boost monitoring budgets and fast-track rapid diagnostic approvals. Zoetis introduced an AI-enabled in-clinic hematology analyser that delivers reference-lab quality results, accelerating therapy decisions and supporting data-driven antimicrobial stewardship. Demand for broad-spectrum and long-acting drugs consequently increases across the veterinary anti-infectives market. Governments are also funding One-Health initiatives that merge human and animal epidemiological data, creating sustained procurement pipelines for anti-infective stockpiles. As biosecurity investments rise, suppliers with scalable manufacturing and regulatory fluency gain competitive leverage.

Pet ownership rates climbed again in 2025, yet more than half of US pet owners deferred at least one medical service primarily due to cost concerns. This affordability gap fuels interest in long-acting injectables such as cefovecin, which provide two-week coverage from a single dose and reduce repeat clinic visits. Corporate practice groups and insurers are piloting wellness-plan models that bundle diagnostics and prescriptions, supporting predictable uptake of premium therapeutics in the veterinary anti-infectives market. Boehringer Ingelheim's 2024 acquisition of Saiba Animal Health added a virus-like-particle platform that aims to produce therapeutic vaccines for chronic canine diseases, reflecting broader demand for novel modalities. Tele-triage and e-prescribing services are scaling rapidly, bringing previously underserved owners into the formal care pathway and expanding the prescription base for anti-infectives. Digital pharmacies integrate seamlessly with these services, offering overnight delivery and automated refill reminders that enhance compliance.

The WHO estimates that antimicrobial and antimalarial agents dominate global counterfeit seizures, with veterinary channels particularly vulnerable in regions lacking robust regulatory oversight.Studies indicate one-fifth of medicines in sub-Saharan Africa fail quality specifications, threatening treatment outcomes and accelerating resistance. Fragmented supply chains that rely on informal agro-vet stores invite infiltration by falsified products bearing popular brand names. Serialization and blockchain track-and-trace pilots launched by multinational producers demonstrate technical feasibility but remain costly for low-margin rural markets. Regional economic blocs, including ECOWAS, have begun harmonizing registration processes to block unlicensed imports, yet enforcement capacity lags. This proliferation depresses brand equity and complicates stewardship, restraining value growth within the veterinary anti-infectives market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cattle generated the most significant revenue within the veterinary anti-infectives market in 2024, with a 39.7% share, as dairy and beef operations relied on antimicrobials for mastitis and respiratory disease control. The veterinary anti-infectives market size for bovine therapeutics is forecast to grow steadily as large herd operations adopt precision-dosing tools that increase value per dose while containing volumes. Poultry, however, is projected to outpace all other species at a 6.4% CAGR through 2030, propelled by expanding broiler capacity in China, India, and Brazil. Avian-specific formulations with short withdrawal times gain uptake as exporters comply with tighter residue limits. Swine producers continue to grapple with post-weaning diarrhea and African swine fever threats, supporting demand for both antibiotics and immune-modulating feed additives. Companion animals remain a premium niche as owners prioritize convenience formulations, though cost sensitivity shapes purchasing decisions in lower-income brackets.

The segmental outlook is increasingly shaped by digital surveillance, with cattle feedlots integrating RFID ear tags connected to cloud dashboards that alert veterinarians to subclinical illnesses. These systems shift purchases toward high-potency injectables used earlier in disease cycles, enhancing therapeutic outcomes while reducing course length. Poultry integrators invest in waterline medication controllers that adjust dosing based on real-time flock metrics, raising demand for soluble powders designed for variable pH environments. Aquaculture, though still modest in revenue, emerges as a strategic frontier as Atlantic salmon producers trial phage biocontrol and nano-encapsulated antibiotics to combat sea lice and vibrio infections. The diversified species mix ensures resilience in the veterinary anti-infectives market even as stewardship pressure alters individual usage patterns.

Antibacterials retained a 29.3% share of the veterinary anti-infectives market size in 2024, supported by a broad catalogue of B-lactams, tetracyclines, and macrolides cleared across multiple species. Stewardship initiatives now favor narrow-spectrum and combination products aimed at specific pathogens, prompting reformulation activity among leading brands. Antivirals are forecast to register the fastest 8.3% CAGR as H5N1, porcine reproductive and respiratory syndrome, and koi herpesvirus outbreaks expose gaps in preventive measures. R&D pipelines feature nucleoside analogues and virus-like particle vaccines that promise shorter treatment courses and lower resistance development potential. Antifungals, while representing a smaller revenue pool, address rising incidences of Malassezia and Aspergillus infections in pets, with single-dose otic gels such as Otiserene and Mometamax Single gaining adoption due to simplified compliance. Antiprotozoals maintain relevance in endemic regions battling coccidiosis and babesiosis, and ongoing trials of toltrazuril combinations highlight a shift toward multi-target therapies.

The innovation pipeline concentrates on delivery enhancements. Long-acting injectable suspensions deliver steady plasma levels for up to two weeks, boosting adherence while limiting clinic revisits. Water-stable micropellets allow uniform dispersion in poultry and shrimp ponds, reducing sediment wastage. Companies also explore biodegradable implant matrices for slow-release antiviral peptides in swine, bridging prophylaxis and treatment. Collectively, these advances ensure the veterinary anti-infectives market retains a balanced mix of established classes and breakthrough modalities that respond to species-specific disease burdens.

The Veterinary Anti-Infectives Market is Segmented by Animal Type (Cattle, Poultry, and More), Product Type (Antibacterials, Antivirals, and More), Mode of Administration (Oral, Parenteral, and More), Distribution Channel (Veterinary Hospitals, Veterinary Clinics, and More), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America retained the largest revenue in 2024, anchored by advanced veterinary infrastructure and high per-animal spending. FDA prescription-only reforms curtailed hobby-farmer antibiotic purchases, but stimulated demand for diagnostics and refined dosing tools that help practitioners justify therapies in stewardship-scrutinized environments. Canada's Veterinary Drugs Directorate aligns closely with US regulations, easing cross-border trade and encouraging harmonized label expansions for new molecules. Mexico benefits from integrated supply chains, though varied enforcement capacity leads multinational firms to emphasize training and quality-assurance initiatives to safeguard brand integrity.

Europe showcases the world's strictest antimicrobial-usage controls, achieving a 50% reduction in veterinary antibiotic sales over 12 years through the ESVAC surveillance network. Distributors now report usage volumes into a centralized EU database, a transparency measure that influences purchasing and supplier negotiations. Category-B caps reorient sales toward first-line products, prompting companies to divulge robust stewardship arguments when submitting new dossiers. Post-Brexit, the UK introduced fast-track procedures for innovative veterinary medicines, accelerating launches but maintaining follow-up pharmacovigilance to guard against resistance.

Asia Pacific is the fastest-growing arena at 7.2% CAGR, propelled by China and India's expanding protein appetites and maturing companion-animal markets. Government programs to modernize dairy and broiler sectors prioritize biosecurity, elevating orders for high-quality injectable ceftiofur and florfenicol. Simultaneously, environmental crackdowns on pharmaceutical-plant effluent in China periodically tighten API exports, adding volatility to regional supply of tetracyclines and macrolides. Japan's Ministry of Agriculture requires annual farm-level antibiotic reporting from 2026, a precedent that could inspire similar mandates across ASEAN and further evolve the veterinary anti-infectives market.