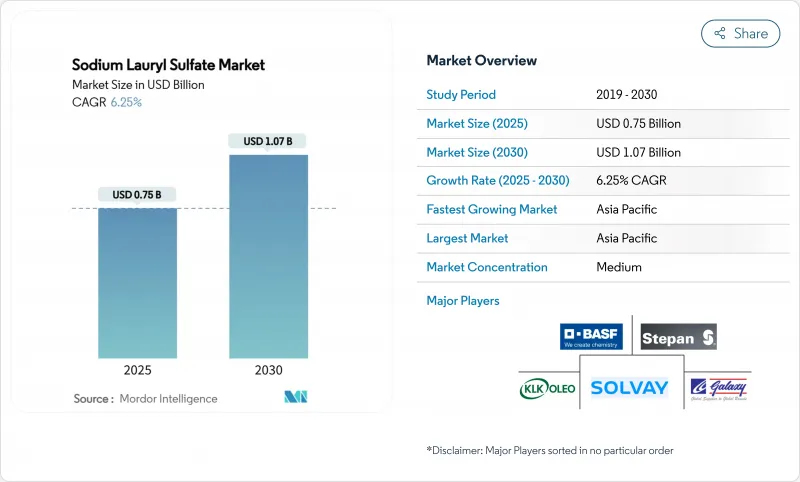

라우릴 황산나트륨 시장 규모는 2025년에 7억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 6.25%로, 2030년에는 10억 7,000만 달러에 달할 것으로 예상됩니다.

이 기세는 "황산염 프리"의 표시에 의해 배합자가 보다 마일드한 대체품을 요구하게 되어도, 이 화합물이 세제, 퍼스널케어 제품, 유전용 화학제품, 농작물 보호 애주번트에서 확고한 역할을 하고 있는 것에 기인하고 있습니다. 원료, 특히 팜 유래 지방 알코올은 불안정하고 생산자의 금리를 압박하고 있지만 동시에 완전 바이오 계면 활성제보다 비용면에서 유리하다는 것을 돋보이게합니다. 중국, 말레이시아, 인도네시아에서의 생산 능력 확대로 아시아태평양은 구조적으로 비용 리드의 포지션을 유지하고 있는 한편, 다국적 메이저에 의한 적극적인 탈탄소화 프로그램에 의해 북미와 유럽에서는 이 화합물이 규제 당국에 받아들여지도록 보호되고 있습니다.

가전제품 소유율의 급상승과 세탁 빈도 증가는 라우릴 황산나트륨 시장 수요의 가장 강한 출구를 지원하고 있습니다. 배합업자는 경수 조건 하에서 음이온 계면활성제의 안정성을 높이 평가하고 있으며, 세탁 성능을 유지하면서 빌더 부하를 낮출 수 있습니다. 또한, 거품 형성 프로파일을 통해 농축액은 소비자가 기대하는 감각적인 단서를 제공할 수 있으며, 시각적 거품이 효능과 동일시되는 신흥 경제권에서는 중요한 성공 요인이 됩니다. 개질된 고효율 세탁액은 라우릴 황산나트륨의 프로테아제, 리파아제, 셀룰라아제 효소와의 호환성을 이용하여 에너지 비용을 줄이는 저온 세탁을 촉진합니다. 2024년 EPA 세이퍼 초이스 재인증을 통해, 이 화합물은 양판 클리너의 주류, 규제 당국 먹이 포함된 성분으로서의 지위를 더욱 향상시켰습니다.

BASF의 100억 달러 규모의 센강 바밴드 콤플렉스를 필두로 하는 대규모 설비투자 프로젝트는 중국, 인도, 동남아시아에서 헤어케어 제품과 목욕케어 제품의 폭발적인 수요에 맞추어 브랜드 소유자가 원료 공급을 현지화하고 있다고 이야기하고 있습니다. 경쟁력있는 가격의 팜 지질 원료와 재생 가능한 전력을 이용하여 단가를 낮게 억제하면서 탄소 배출량을 삭감하고 있습니다. 클러스터 효과는 수탁 제조업체와 패키징 공급업체를 모아 세계 FMCG 대기업의 리드 타임을 단축합니다. 이러한 역학은 프리미엄 황산염 미사용 제품이 보급되어도 APAC에서 라우릴 황산나트륨 시장의 회복력을 강화합니다.

FDA와 Cosmetic Ingredient Review에 의한 세척 독성 검토는 안전성을 재확인하고 있지만, 소셜 미디어 상의 논의는 일화적인 두피 자극의 주장을 증폭시켜 중·고급 헤어 케어 브랜드를 황산염 프리 포지셔닝으로 밀고 있습니다. 이 제품은 북미에서 20-30%의 가격 프리미엄을 획득했습니다. 시장 세분화에서는 '클린 뷰티' 전용 공간이 할당되어 프레스티지 부문의 라우릴 황산나트륨 시장이 눈에 띄게 세분화되어 있습니다. 유럽의 에코 라벨 시스템은 배출 독성의 역치를 엄격히 하고 식기 세척액의 기관 투자자 바이어에게 보다 온화한 배합을 시험적으로 사용하도록 촉구하고 있습니다.

SLS Liquid는 2024년 수익의 61.35%를 차지했고, CAGR 6.85%에서 라우릴 황산나트륨 시장 전체를 상회할 것으로 예측됩니다. 인라인 투여, 완전 자동 배치 처리, 즉 용해성으로 인해 액체는 중국과 미국의 메가톤급 세제 플랜트의 기본 옵션이 되었습니다. 액체 유형은 또한 노동 안전 규정 준수의 우선순위인 분진 노출을 최소화할 수 있습니다. 드라이 SLS는 수출 주도의 섬유 보조제와 SDS-PAGE 시약 분야에서 발판을 유지하고 있어 수송량의 감소가 물류의 절약으로 이어지지만 성장률은 5% 미만에 그칩니다.

농축 포드와 막대 모양의 세제를 대상으로 하는 조제사는 점도 조절과 물 운반을 줄이기 위해 분말 SLS를 첨가합니다. 분무건조의 공정개선으로 에너지 사용량이 15% 삭감되어 분말의 경제성이 약간 개선되었습니다. 그럼에도 불구하고, 2026년 말레이시아와 텍사스에서 발표된 액체 용량의 확장은 라우릴 황산나트륨 시장이 여전히 유동성 형식으로 기울어지고 있음을 보여줍니다.

라우릴 황산나트륨 보고서는 제품 형태(라우릴 황산나트륨(SLS) 액, 라우릴 황산나트륨(SLS) 건식), 등급(산업 등급, 화장품 및 퍼스널케어 등급, 의사 약품 등급, 식품 등급), 최종 사용자 산업(세제 및 클리너, 퍼스널케어 제품, 산업용 청소기 및 기타 용도), 지역(아시아태평양, 북미, 유럽 및 기타)으로 구분됩니다.

아시아태평양은 세계 매출의 45.16%를 차지하며 2030년까지 연평균 복합 성장률(CAGR)은 8.03%를 나타낼 전망입니다. 저비용 원료, 견조한 소비재 생산, 말레이시아, 태국, 중국 연안의 새로운 유지 화학 조합이 이 지역의 구조적 우위를 유지하고 있습니다. 샤오강 바밴드는 2030년까지 APAC 수요의 3분의 1을 충족하는 음이온성 계면활성제 베이스를 공급하고 있습니다.

북미는 장수명의 세탁 세제 브랜드와 활기찬 유전용 화학제품 부문에 지지되어, 성숙하면서도 안정된 지위를 유지하고 있습니다. 스테판의 PerformanX 인수는 부가가치가 높은 농업용 계면활성제의 생산 능력을 확대하여 수입 의존도를 줄여줍니다.

유럽에서는 보다 엄격한 규제 강화를 위해 노력하고 있지만, 라우릴 황산나트륨은 산업용 식기세척기와 패브릭 케어 태블릿에 정착하고 있으며, 신규 진출기업에 대한 생분해성 장애물도 마찬가지로 엄격합니다. 개정 세제 규제 하에서 디지털 디스플레이의 시험 운영은 스마트폰에 세분화된 성분 데이터를 전송하고 처방 담당자를 추적성이 있는 지속 가능한 인증 팜 유도체로 유도하고 있습니다. 중견 제조업체는 BASF의 에코 밸런스 등급과 유사한 바이오 물질 수지 모델을 채택하여 마진 감소에 대응하고 있습니다.

The Sodium Lauryl Sulfate Market size is estimated at USD 0.75 billion in 2025, and is expected to reach USD 1.07 billion by 2030, at a CAGR of 6.25% during the forecast period (2025-2030).

This momentum stems from the compound's entrenched role in detergents, personal-care products, oilfield chemicals, and crop-protection adjuvants, even as "sulfate-free" labeling pushes formulators toward milder alternatives. Feedstock volatility, especially in palm-derived fatty alcohols, is compressing producer margins and simultaneously highlighting cost advantages over fully bio-based surfactants. Capacity expansions in China, Malaysia, and Indonesia keep Asia-Pacific in a structural cost-lead position, while aggressive decarbonization programs by multinational majors safeguard the compound's regulatory acceptance in North America and Europe.

Surging appliance ownership and rising laundry frequency underpin the most resilient outlet for the sodium lauryl sulfate market demand. Formulators value the anionic surfactant's stability under hard-water conditions, enabling lower builder loading while preserving wash performance. Its foaming profile also allows concentrated liquids to deliver the sensory cues consumers expect, a critical success factor in emerging economies where visual foam is equated with efficacy. Reformulated high-efficiency laundry liquids rely on sodium lauryl sulfate's compatibility with protease, lipase, and cellulase enzymes, facilitating lower-temperature washes that trim energy bills. EPA Safer Choice recertification in 2024 further elevates the compound's status as a mainstream, regulatory-endorsed ingredient for mass-market cleaners.

Massive capital projects, most notably BASF's USD 10 billion Zhanjiang Verbund complex, illustrate how brand owners are localizing ingredient supply to match explosive demand for hair-care and bath-care products in China, India, and Southeast Asia. Access to competitively priced palm lipid feedstocks and renewable electricity keeps unit costs low while trimming embedded carbon. The clustering effect attracts contract manufacturers and packaging suppliers, shortening lead times for global FMCG leaders. These dynamics strengthen the sodium lauryl sulfate market's resilience in APAC even as premium sulfate-free lines proliferate.

Although wash-off toxicology reviews from the FDA and the Cosmetic Ingredient Review reaffirm safety, social-media discussions amplify anecdotal scalp-irritation claims, pushing mid- to high-end hair-care brands toward sulfate-free positioning. These products achieve price premiums of 20-30% in North America. Retail shelf resets allocate dedicated "clean beauty" space, visibly fragmenting the sodium lauryl sulfate market in prestige segments. European eco-label schemes tighten discharge-toxicity thresholds, nudging institutional buyers of dish-wash liquids to pilot milder blends.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SLS Liquid captured 61.35% of 2024 revenue and is forecast to outpace the overall sodium lauryl sulfate market at a 6.85% CAGR. Inline dosing, fully automated batching, and instant solubility make liquids the default choice for megatonne detergent plants in China and the United States. Liquid format also minimizes dust exposure, a growing occupational-safety compliance priority. Dry SLS retains a foothold in export-driven textile auxiliaries and SDS-PAGE reagents, where lower freight mass drives logistics savings, but clocks sub-5% growth.

Formulators targeting concentrated pods or bar detergents add powder SLS for viscosity control and reduced water carry. Process improvements in spray-drying cut energy use by 15%, modestly improving powder economics. Even so, liquid capacity expansions announced for 2026 in Malaysia and Texas point to a continued tilt toward flowable formats in the sodium lauryl sulfate market.

The Sodium Lauryl Sulfate Report is Segmented by Product Form (Sodium Lauryl Sulfate (SLS) Liquid and Sodium Lauryl Sulfate (SLS) Dry), Grade (Industrial Grade, Cosmetic and Personal Care Grade, Pharmaceutical Grade, and Food Grade), End-User Industry (Detergents and Cleaners, Personal Care Products, Industrial Cleaners, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and More).

Asia-Pacific anchors 45.16% of global sales and will accelerate at 8.03% CAGR to 2030. Low-cost feedstock, robust consumer-goods output, and new oleochemical complexes in Malaysia, Thailand, and coastal China preserve the region's structural advantage. Zhanjiang Verbund alone supplies enough anionic surfactant base to serve one-third of the incremental APAC demand through 2030.

North America holds a mature yet steady position, bolstered by long-lived laundry-detergent brands and a vibrant oilfield-chemicals sector. Stepan's PerformanX acquisition expands value-added agriculture surfactant capacity, mitigating import reliance.

Europe grapples with stiffer regulatory overhead, but sodium lauryl sulfate remains entrenched in industrial dish-washers and fabric-care tablets, where biodegradability hurdles for newcomers are equally onerous. Digital labeling pilots under the revised Detergent Regulation funnel granular ingredient data to smartphones, nudging formulators toward traceable, certified-sustainable palm derivatives. Mid-tier manufacturers counter margin erosion by adopting biomass-balance models similar to BASF's EcoBalanced grades.