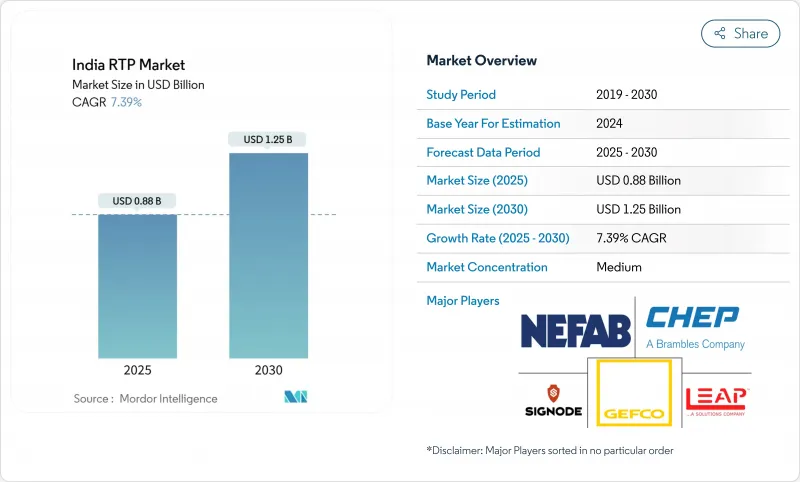

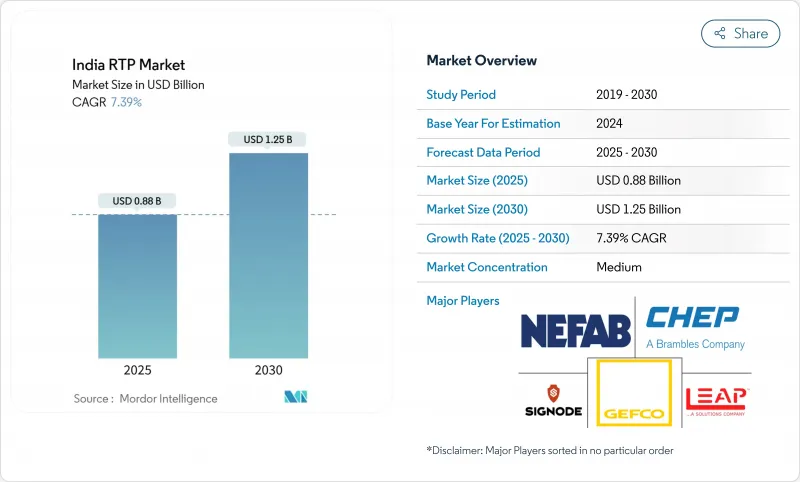

2025년 인도의 RTP(Returnable transport packaging) 시장 규모는 8억 7,500만 달러로, 2030년에는 12억 5,000만 달러에 이르고, CAGR 7.39%를 나타낼 것으로 예측됩니다.

규제 압력 증가, 특히 2025년 4월까지 경질 플라스틱의 재활용률을 30%로 하기로 결정한 확대 생산자 책임(EPR) 의무화는 일회용에서 다중 사이클 자산으로의 전환을 가속화하고 있습니다. 2030년까지 3,000억 달러의 비즈니스 기회를 향한 전자상거래의 급속한 급증은 단편화된 마지막 원마일 네트워크를 순환할 수 있는 풀링된 팔레트, 크레이트, 중간 벌크 컨테이너에 대한 수요를 확대하고 있습니다. LEAP 인도를 통한 CHEP 인도 인수와 같은 자산 풀 통합은 규모의 효율성을 높이는 동시에 추정 연간 10%의 팔레트 손실을 억제하는 디지털 추적 시스템을 통합합니다. 한편 2030년까지 물류비용을 세계 벤치마크까지 줄이는 국가물류정책의 비전은 인도의 RTP(Returnable transport packaging) 시장 전체에서 보다 신속한 자산 회전과 이용률 향상을 촉진하는 인프라 투자를 뒷받침하고 있습니다.

2025년 4월부터 경질 플라스틱에 30%의 재활용 함량이 의무화됨에 따라 음료 제조업체, FMCG 제조업체, 전자 제조업체는 재사용 가능한 자산을 중심으로 공급망을 재설계할 필요가 있습니다. 보틀러로부터의 저항에 의해 재활용 능력의 격차가 드러나고 있지만, EPR은 동시에 2024년 PET의 재활용 생산량을 3배의 4만 2,000톤/년으로 확대한 Ganesha Ecopet과 같은 조기 참가 기업에도 이익을 가져왔습니다. 2026년까지 EPR이 모든 기판으로 확대될 것으로 예상에 따라 컴플라이언스 영역이 넓어지고 인도의 RTP(Returnable Transport Card) 시장은 기업의 순환 전략의 중심에 자리잡게 됩니다. 리버스 로지스틱스의 루프를 확립하고 있는 기업은 현재 지연을 겪고 있는 기업의 스위칭 비용을 인상하는 규제상의 해자를 즐기고 있습니다. 마하라슈트라 주와 구자라트 주에서 예금 수익 제도와 리버스 벤딩 네트워크에 대한 투자는 지역 정책 리더십이 자산 순환을 가속화하는 방법을 보여줍니다.

Tier II 및 III 도시는 2022년 온라인 소매 취급량의 41.5%를 차지했으며, 3PL은 재포장 비용 없이 여러 터치 포인트를 수용할 수 있는 표준화된 토트와 접을 수 있는 나무 상자를 채택해야 했습니다. 창고 재고는 2025년까지 3억 ft2를 넘어 니도그룹과 같은 사업자는 공유 크레이트에 내장된 RFID 태그를 읽는 스캐너로 분류를 자동화하고 있습니다. 이러한 규모의 집적은 물류 비용을 최대 15%까지 줄이고, 이 절약은 전자상거래의 경쟁가격 모델에 직접 반영됩니다. 2023년도에 240억 달러를 넘는 정부의 e마켓플레이스 주문은 기관 조달 채널의 풀 자산 경제성을 더욱 증명했습니다. 이러한 역학은 인도의 RTP(Returnable transport packaging) 시장의 고객 기반을 기존 제조업 이외에도 넓혀 디지털 무역 회랑의 성장을 지지하고 있습니다.

종합적인 RTP 프로그램은 금형, 금형 및 함대를 강화하는 데 수백만 달러가 필요하며 소규모 기업의 현금 흐름에 문제가 있습니다. 타임테크노플라스트의 1,500루피(1억 8,000만 달러)의 지출은 전국 전개에 필요한 규모의 크기를 나타냅니다. 투자 회수 기간이 18개월에서 36개월에 이르기 때문에 CFO는 수지 가격과 수요가 변동하는 가운데 망설이고 있습니다. 슈프림 인더스트리즈의 2025년도 2분기 수익 하락은 PVC 가격 변동에 의해 악화된 것으로, 소재 사이클이 투자 회수 기간을 얼마나 늘리는지를 부각하고 있습니다. 자산 대출 수단에 대한 접근이 제한되어 있기 때문에 많은 중소기업들이 두 발을 밟고 있으며 인도의 RTP(Returnable transport packaging) 시장에서 잠재적인 보급을 방해하고 있습니다.

2024년, 인도의 RTP(Returnable transport packaging) 시장은 플라스틱이 58.42%를 차지하고, 그 경량 강도와 저렴한 금형 비용을 반영했습니다. 이 부문의 리더십은 헤비 듀티 성능보다 속도를 선호하는 음료, FMCG, 전자 제품공급망에 정착되어 있습니다. 그러나 지속가능성에 대한 요구가 높아지고 보다 높은 내열성의 필요성으로 인해 제약·화학제품 수출업체는 금속 용기로 방향타를 끊고 있으며, 이 부문의 2030년까지의 CAGR은 9.32%를 나타낼 전망입니다. 폴리프로필렌의 가격 급락은 구매자를 선행투자 단가보다 라이프사이클 전체의 경제성을 조사하는 방향으로 향하고 있으며, 이익률이 높은 적재물에는 스테인리스 스틸이나 알루미늄의 IBC가 선호되는 경우가 많습니다. Nilcamar의 식품 HDPE 크레이트에 대한 투자는 금속 침입에 대한 방어책으로 틈새 전문성을 강조합니다. 2,000 루피(2억 4,000만 달러)의 신규 생산 능력을 뒷받침하는 바이오 PLA 이니셔티브는 10년 후반까지 재료 우선순위를 바꿔 인도의 RTP(Returnable transport packaging) 시장에 녹색 프리미엄층을 추가할 수 있습니다.

현재 재료 공급의 안정성은 가격과 마찬가지로 조달 계약에 영향을 미칩니다. 수지 바이어는 정유소의 운영 중단과 화물 운송 중단을 새로운 긴급성으로 모니터링하고 위험 위험 회피를 위해 플라스틱 및 금속 이중 포장을 채택합니다. 한편, 금속 수영장 운영자는 8-10년의 서비스 수명과 높은 설비 투자를 상쇄하는 2차 스크랩 가치를 강조하고 있습니다. 서큘러 이코노미 스코어 카드가 입찰 평가의 일부가 됨에 따라, 브랜드 소유자는 폐쇄형 루프 폴리머 및 무한히 재활용 가능한 합금과 관련된 정량화된 CO2 감소를 반영하기 위해 재료 테이블을 점차 혁신하고 있습니다. 이러한 경쟁은 플라스틱의 우위를 유지하면서도 규제된 최종 시장에서의 점유율을 깎아 인도의 RTP(Returnable transport packaging) 시장 전체에서 소재의 선택을 유동적으로 하고 있습니다.

팔레트는 2024년 인도의 RTP(Returnable transport packaging) 시장 규모의 35.42%를 차지해 국내 물류의 만능 선수로서의 지위를 굳혔습니다. 표준화된 실적, 특히 1200 X 1000 mm의 베이스는 등급 A 창고에서 현재 널리 사용되는 자동 보관 및 검색 시스템과 잘 어울립니다. 스낵 과자 공장의 협동 로봇은 팔레트 적재물을 12% 빠르게 적층하여 톤당 인건비를 절감하고 공장 자동화 전략에서 팔레트의 중심성을 강화하고 있습니다. 중간 벌크 컨테이너는 CAGR 8.92%로 가장 빠르게 성장하고 있으며, 높은 적재 밀도와 ISO 탱크화물 레인과의 호환성을 평가하는 화학, 농약, 의약품 수출업체 수요를 끌어들이고 있습니다. 폴드 플랫 모델은 백홀 운송량을 최대 65%까지 줄일 수 있습니다. 이는 주요 항로에서 디젤이 리터당 90루피를 넘는 수준으로 추이하고 있기 때문에 매력적인 장점입니다.

제품 개발은 스마트화를 향하고 있습니다. 플러그 앤 플레이로 센서를 통합할 수 있는 RFID 대응 팔레트, 120시간의 저온 유지가 가능한 상변화물질를 사용한 단열 IBC, 수동 클립의 사용을 삭감하는 셀프 락식의 접이식 크레이트 등입니다. 타임테크노플라스트의 대형 플라스틱 드럼의 점유율 60%는 보다 광범위한 제품 라인이 상품화의 압력에 노출되어도 틈새 분야에서의 이점이 이득을 확보할 수 있음을 보여줍니다. 예측 기간 동안, 옴니채널 완성을 둘러싼 수요의 수렴은 제품 경계를 모호하게 하고, 댄니지 인서트가 장착된 팔레트 크기의 접이식 박스와 같은 하이브리드 솔루션을 생성할 것으로 보입니다. 이러한 혁신은 인도의 RTP(Returnable Transport Card) 시장 전체의 제품 구성 복잡성을 높일 것으로 보입니다.

인도의 RTP(Returnable transport packaging) 시장은 재료(플라스틱, 금속, 목재), 제품 유형(팔레트, 나무 상자 및 트레이, 중간 벌크 컨테이너 등), 최종 사용자 산업(자동차, 식품 및 음료, 소비재 및 소매, 기타), 순환 모드(폐쇄 루프, 오픈/풀링), 소유 모델(임대/임대, 자사 소유)로 분류 시장 예측은 금액(달러)으로 제공됩니다.

The India returnable transport packaging market is valued at USD 0.875 billion in 2025 and is forecast to reach USD 1.25 billion by 2030, advancing at a 7.39% CAGR.

Rising regulatory pressure, especially the Extended Producer Responsibility (EPR) mandate that stipulates 30% recycled content in rigid plastics by April 2025, is accelerating the transition from single-use to multi-cycle assets. The rapid surge of e-commerce toward a USD 300 billion opportunity by 2030 is magnifying demand for pooled pallets, crates, and Intermediate Bulk Containers that can circulate across fragmented last-mile networks. Consolidation of asset pools, such as LEAP India's acquisition of CHEP India, is adding scale efficiencies while embedding digital track-and-trace systems that curb an estimated 10% annual pallet loss rate. Meanwhile, the National Logistics Policy's vision to trim logistics costs to global benchmarks by 2030 underpins infrastructure investments that facilitate faster asset turns and improved utilization across the India returnable transport packaging market.

Mandatory 30% recycled content for rigid plastics effective April 2025 is prompting beverage, FMCG, and electronics players to redesign supply chains around reusable assets. Resistance from bottlers has exposed recycling-capacity gaps, but EPR is simultaneously rewarding early movers such as Ganesha Ecopet, which tripled PET recycling output to 42,000 tpa in 2024. Anticipated expansion of EPR to all substrates by 2026 will widen compliance terrain, placing the India returnable transport packaging market at the center of corporate circularity strategies. Companies with established reverse-logistics loops now enjoy a regulatory moat that raises switching costs for laggards. Investments in deposit-return schemes and reverse-vending networks across Maharashtra and Gujarat illustrate how regional policy leadership can accelerate asset circulation.

Tier II and III cities contributed 41.5% of online retail volumes in 2022, compelling 3PLs to adopt standardized totes and foldable crates that survive multiple touchpoints without repacking costs. Warehousing stock exceeded 300 million ft2 by 2025, and operators such as NIDO Group are automating sortation with scanners that read RFID tags embedded in shared crates. The collective scale is shrinking unit logistics spend by up to 15%, a saving that directly feeds e-commerce's competitive pricing model. Government e-Marketplace orders topping USD 24 billion in FY 2023 further validate pooled-asset economics for institutional procurement channels. These dynamics widen the India returnable transport packaging market's customer base beyond traditional manufacturing, anchoring growth in digital trade corridors.

A comprehensive RTP program can demand millions of USD in tooling, moulds, and fleet build-out, which challenges the cash flow of small enterprises. Time Technoplast's Rs 1,500 crore (USD 180 million) outlay illustrates the scale required for nationwide presence. With payback periods spanning 18-36 months, CFOs hesitate amid volatile resin prices and demand swings. Supreme Industries' revenue dip during Q2 FY 2025, aggravated by PVC price fluctuations, highlights how material cycles can stretch ROI horizons. Limited access to asset-financing instruments keeps many SMEs on the fence, muting potential penetration in the India returnable transport packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic retained 58.42% of the India returnable transport packaging market in 2024, reflecting its lightweight strength and affordable tooling costs. The segment's leadership is entrenched in beverage, FMCG, and electronics supply chains that prioritize speed over heavy-duty performance. Yet escalating sustainability mandates and the need for higher heat resistance are steering pharmaceutical and chemical exporters toward metal containers, propelling the segment at a 9.32% CAGR to 2030. Polypropylene's price creep is pushing buyers to scrutinize total life-cycle economics rather than upfront unit costs, a calculus that often favors stainless-steel or aluminum IBCs for high-margin payloads. Nilkamal's investment in food-grade HDPE crates underlines niche specialization as a defense against metal incursion. Bio-based PLA initiatives backed by Rs 2,000 crore (USD 240 million) in new capacity could reorder material preference by late decade, adding a green premium layer to the India returnable transport packaging market.

Material supply stability now influences sourcing contracts as much as price. Resin buyers monitor refinery shutdowns and freight disruptions with new urgency, adopting dual-spec packaging qualified across plastic and metal to hedge risk. Meanwhile, metal pool operators highlight 8-10-year service lives and secondary scrap value that offsets higher capex. As circular-economy scorecards become part of tender evaluations, brand owners increasingly refresh bills of material to reflect quantified CO2 reductions linked to closed-loop polymers and infinitely recyclable alloys. The competitive interplay is likely to sustain plastic's headline dominance yet chip away incremental share in regulated end-markets, keeping material choice fluid across the India returnable transport packaging market.

Pallets represented 35.42% of the India returnable transport packaging market size in 2024, cementing their status as the universal workhorse of domestic logistics. Standardized footprints, especially the 1200 X 1000 mm base, mesh well with automated storage and retrieval systems now proliferating in Grade A warehouses. Collaborative robots at snack-food plants stack pallet loads 12% faster, cutting labor cost per ton and reinforcing the pallet's centrality to factory automation strategies. Intermediate Bulk Containers are the fastest riser with an 8.92% CAGR, drawing demand from chemical, agrochemical, and pharmaceutical exporters that value their high payload density and compatibility with ISO tank freight lanes. Fold-flat models pare backhaul volume by up to 65%, a compelling benefit as diesel remains above INR 90 per liter in key corridors.

Product development is tilting toward smart variants: RFID-enabled pallets capable of plug-and-play sensor integration, insulated IBCs with phase-change materials for 120-hour cold hold, and collapsible crates that self-lock to cut manual clip usage. Time Technoplast's 60% share in large plastic drums shows how dominance in a niche can shield margins even when broader product lines face commoditization pressures. Over the forecast period, demand convergence around omnichannel fulfillment will blur product boundaries, birthing hybrid solutions such as pallet-sized foldable boxes fitted with dunnage inserts. These innovations will elevate product mix complexity across the India returnable transport packaging market.

India Returnable Transport Packaging Market is Segmented by Material (Plastic, Metal, Wood), Product Type (Pallets, Crates and Trays, Intermediate Bulk Containers, and More), End-User Industry (Automotive, Food and Beverage, Consumer Goods and Retail, and More), Circulation Mode (Closed-Loop, Open/Pooling), and Ownership Model (Rental/Leasing, In-House Ownership). The Market Forecasts are Provided in Terms of Value (USD).