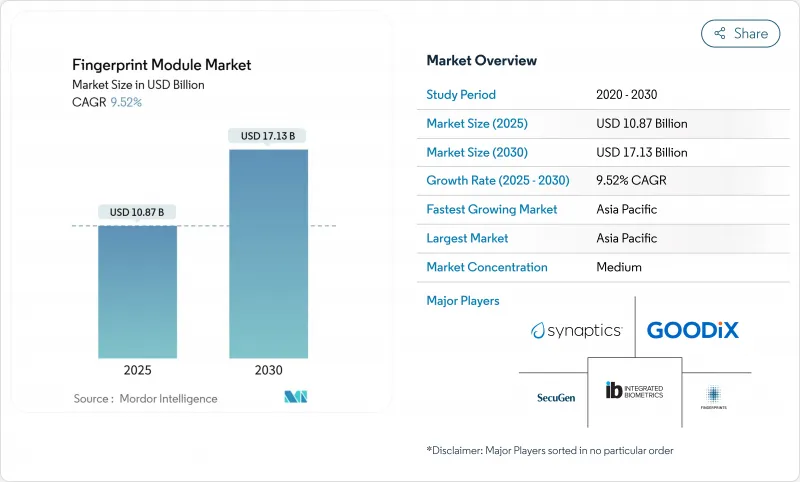

지문 모듈 시장 규모는 2025년에 108억 7,000만 달러로 평가되며, CAGR 9.52%를 나타내 2030년에는 171억 3,000만 달러에 이를 것으로 예상됩니다.

이 기세는 주권자에 의한 디지털 신원 프로젝트, 스마트폰 인증의 급속한 업그레이드, 바이오메트릭스 결제 카드의 상업 전개에 기인하고 있습니다. 정전용량 센서는 여전히 양적 수요의 대부분을 차지하고 있지만, 고급 디바이스가 더 높은 내 스푸프성을 요구하고 있기 때문에 초음파 기술이 가장 빠르게 확대되고 있습니다. 시스템 온칩(SoC) 통합은 실적와 부품 비용을 줄이고, 인디스플레이 모듈은 베젤리스 터미널 설계의 추진을 지원합니다. 아시아태평양 정부 프로그램을 위한 대량 조달, 평균 판매 가격 하락, 자동차 채용이 결합되어 지문 모듈 시장은 다년간의 성장 궤도를 유지하고 있습니다.

대규모 국가 ID 프로그램이 기본 수요를 바꿉니다. 에티오피아의 Fayda 계획은 다자간 자금 3억 5,000만 달러를 배경으로 2030년까지 9,000만 명의 등록을 목표로 하고 있습니다. 나이지리아의 4억 3,000만 달러의 디지털 ID 프로젝트는 2억 명 이상의 시민을 위한 보편적인 커버리지를 추구하고 있습니다. 이러한 계약은 견고하고 수명이 긴 모듈을 지정하여 수년간의 보충 수익을 창출합니다. 그 양은 소비자 장치의 사이클을 상당히 웃돌고 공급자에게는 예측 가능한 인계가 확보되어 지문 모듈 시장 전체의 공장 가동률이 안정됩니다.

플래그십 및 중급 휴대폰은 현재 지문 생체 인증을 기본 기능으로 취급하고 있습니다. 디스플레이 하단 모듈은 전체 화면 디자인을 가능하게 하며 초음파 장치는 표피 아래의 융기를 영상화하여 보안을 강화합니다. 북미와 중국의 안드로이드 단말기 제조업체는 듀얼 감지 영역을 통합하여 잠금 해제 속도를 높이고 단말기당 평균 컨텐츠를 늘리고 있습니다. 이러한 추세는 대응 가능한 수량을 확대하고 공급업체는 보다 엄격한 두께와 전력 예산의 범위를 충족해야 합니다.

일리노이주의 BIPA와 같은 법률에 근거한 집단 소송에서는 부적절한 지문 취득에 대해 수백만 달러의 화해금이 발생하여 기업의 컴플라이언스 오버헤드가 증가하고 있습니다. 엔터프라이즈 바이어는 현재 디바이스에서 템플릿 스토리지 및 취소 가능한 동의 흐름을 요구하고 있으며 디자인 인사이클 및 규제 협의를 연장하고 있습니다. 지문 모듈 시장 솔루션을 판매하는 공급업체는 암호화, 보안 요소 분리 및 타사 감사를 추가해야 하며, 이는 재료 비용과 인증 비용을 팽창시킵니다.

초음파 유닛은 2025년 매출에서 차지하는 비율은 작지만 급속히 성장하고 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 10.2%를 나타내 다른 모든 카테고리를 상회할 것으로 예측됩니다. 커패시턴스 솔루션은 여전히 선적의 대부분을 차지하고 2024년 지문 모듈 시장 점유율의 58%를 차지했습니다. 정전용량 센서의 지문 모듈 시장 규모는 저가의 안드로이드 모델을 배경으로 상승했지만, 초음파식의 채용은 프리미엄 ASP 스마트폰이나 금융 그레이드의 웨어러블과 상관되고 있습니다.

개발자는 땀구멍과 피하 모세관 구조를 영상화할 수 있는 초음파 기술을 높이 평가하고 있으며, 박막 스크린 프로텍터와 부분 오염물질을 배제하고 있습니다. Qualcomm의 3세대 3D Sonic 패키지는 200마이크론 이하의 Z 스택 높이를 달성하며 OEM은 엣지 투 엣지의 유리 제조를 추구할 수 있습니다. 정전용량 방식의 기존 기업은 계속해서 공간 해상도를 높여 아이돌 전력을 5µA 이하로 삭감함으로써 양판점용 휴대전화나 소비자용 IoT와의 관련성을 유지하고 있습니다. 한편, 광학 모듈은 비용을 줄이기 위해 디스플레이 엔진에서 백라이트를 재사용할 수 있는 중급 장치에 장착됩니다.

지역/터치 모듈은 소비자 장비 및 기업 도어록에서 입증된 신뢰성으로 2024년의 61%를 차지했습니다. 그럼에도 불구하고 디스플레이 내 센서는 2030년까지 매년 11.5% 상승할 것으로 예측되며, 이는 휴대전화 제조업체가 중단 없는 OLED 패널을 찾는 경쟁을 반영합니다. 인디스플레이 설계와 연동하는 지문 모듈 시장 규모는 프리미엄 ASP의 혜택을 받아 단말기당 밀도가 낮습니다.

스와이프 센서는 좁은 베젤이 남는 POS 단말이나 러기드 핸드헬드에 남습니다. 하이브리드 터치 플러스 프레셔 패키지는 인클로저를 늘리지 않고 손목 받침대와 통합할 수 있어 노트북 벤더들 사이에서 브랜드 견인력을 높입니다. 센서 유형의 조합은 산업 디자인 목표와 조화를 이루는 눈에 보이지 않는 생체 인증으로 지문 모듈 산업의 변화를 강조합니다.

아시아태평양은 세계 최대 생산 유역과 최대 전개 프로그램을 결합하여 2024년 시장 점유율은 41%에 달했고, 2030년까지 연평균 복합 성장률(CAGR)은 9.8%를 나타낼 전망입니다. 중국 휴대폰 OEM 생태계는 매달 수천만 개의 센서를 흡수하고 인도의 디지 야트라 확장과 공항 전자 게이트 입찰은 국내 민간 수요를 높이고 있습니다. ASEAN의 상호 운용 가능한 디지털 공공 인프라에 대한 헌신은 표준을 조화시켜 공급자가 여러 관할 구역에 공통 모듈 풋 프린트를 출하 할 수있게합니다.

북미는 성숙하면서도 유리한 상황을 보여줍니다. 휴대기기 교체주기, 웨어러블 업그레이드, 기업 보안 리노베이션이 안정적인 수량을 유지하면서 엄격한 개인정보 보호법이 구매자에게 장치의 템플릿 스토리지를 선호하도록 촉구하여 ASP를 끌어올리고 있습니다. 지문 모듈 시장은 미국의 자동차 바이오메트릭스로부터 계속 이익을 얻고 있으며, 고급 브랜드는 노스캐롤라이나 주 석영 광산의 장애로 웨이퍼 생산이 위협받은 후 공급망의 위험을 헤지하기 위해 현지 조달을 실시했습니다.

유럽은 GDPR(EU 개인정보보호규정)에 따른 국가의 e-ID 계획과 은행 주도의 바이오메트릭스 카드의 발매를 배경으로 전진하고 있습니다. 중동 및 아프리카의 잠재 수요는 카메룬이 15년간의 컨세션 하에서 2025년에 바이오메트릭 카드를 전개하는 등 국가 ID 프로젝트에서 결정화합니다. 남미는 스마트폰이 중소득층에 침투하고 정부가 사회 급여의 지급 플랫폼을 현대화함에 따라 점진적인 이익을 가져오지만 거시 변동은 조달 주기를 장기화하고 있습니다.

The fingerprint module market size is valued at USD 10.87 billion in 2025 and is forecast to reach USD 17.13 billion by 2030, reflecting a 9.52% CAGR.

Momentum stems from sovereign digital-identity projects, rapid smartphone authentication upgrades, and the commercial roll-out of biometric payment cards. Capacitive sensors still dominate volume demand, yet ultrasonic technology is expanding fastest as premium devices seek higher spoof-resistance. System-on-chip (SoC) integration is shrinking footprint and bill-of-materials costs, while in-display modules underpin the push for bezel-less handset designs. Volume procurement for Asia-Pacific government programs, falling average selling prices, and automotive adoption together keep the fingerprint module market on a multi-year growth arc.

Large-scale national identity programs are rewriting baseline demand. Ethiopia's Fayda scheme targets 90 million registrations by 2030, backed by USD 350 million in multilateral funding.Nigeria's USD 430 million digital ID project pursues universal coverage for more than 200 million citizens. Such contracts specify robust, long-life modules and create multi-year replenishment revenue. The volume sheerly outstrips consumer-device cycles, ensuring predictable pull for suppliers and stabilizing factory utilization across the fingerprint module market.

Flagship and mid-tier handsets now treat fingerprint biometrics as baseline functionality. Under-display modules permit full-screen designs, while ultrasonic units lift security by imaging sub-epidermal ridges. Android handset makers in North America and China have embedded dual sensing zones to quicken unlock speed, raising average content per device. This trend expands addressable volume and pressures suppliers to meet tighter thickness and power-budget envelopes.

Class actions under statutes such as Illinois' BIPA have generated multimillion-dollar settlements for improper fingerprint capture, raising compliance overheads for enterprises. Corporate buyers now demand on-device template storage and revocable consent flows, extending design-in cycles and regulatory consultations. Vendors marketing the fingerprint module market solutions must add encryption, secure-element isolation, and third-party audits, which inflate the bill-of-materials and certification costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ultrasonic units contributed a minor yet fast-advancing slice of 2025 revenue and should expand at 10.2% CAGR to 2030, outpacing all other categories. Capacitive solutions still delivered the bulk of shipments, anchoring 58% fingerprint module market share in 2024. The fingerprint module market size for capacitive sensors rose on the back of low-cost Android models, whereas ultrasonic adoption correlated with premium ASP smartphones and finance-grade wearables.

Developers prize ultrasonic technology for its capacity to image sweat pores and sub-dermal capillary structures, defeating thin-film screen protectors and partial contaminants. Qualcomm's third-generation 3D Sonic packages achieve sub-200-micron Z-stack height, freeing OEMs to pursue edge-to-edge glass builds. Capacitive incumbents continue to raise spatial resolution and cut idle power below 5 µA, preserving relevance in mass-market phones and consumer IoT. Optical modules, meanwhile, land in mid-tier devices where backlighting can be reused from display engines to trim costs.

Area/touch modules accounted for 61% of 2024 due to proven reliability across consumer devices and enterprise door locks. Nonetheless, in-display sensors are forecast to climb 11.5% annually to 2030, reflecting handset makers' race for uninterrupted OLED panels. The fingerprint module market size linked to in-display designs will benefit from premium ASPs, offsetting lower density per handset.

Swipe sensors linger in point-of-sale terminals and rugged handhelds where narrow bezels remain. Hybrid touch-plus-pressure packages are gaining brand traction among notebook PC vendors, enabling palm-rest integration without enlarging the chassis. The sensor-type mix underlines the fingerprint module industry shift toward invisible biometrics that harmonize with industrial design goals.

The Fingerprint Module Market is Segmented by Technology (Optical, Capacitive, Ultrasonic, and More), Sensor Type (Area/Touch, Swipe, and More), Form Factor (Stand-Alone Module, System-On-Chip Integrated, and More), End-User Industry (Government and Law Enforcement, Consumer Electronics, and More), Application (Identity and Access Management, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific combined the world's biggest production basin with the largest deployment programs, holding 41% market share in 2024 and tracking a 9.8% CAGR to 2030. China's handset OEM ecosystem absorbs tens of millions of sensors monthly, while India's Digi Yatra expansion and airport e-gate tenders elevate domestic civil demand. ASEAN's commitment to interoperable digital public infrastructure harmonizes standards, letting suppliers ship common module footprints across multiple jurisdictions.

North America shows mature yet lucrative conditions: handset replacement cycles, wearables upgrades, and enterprise security retrofits keep volumes stable, whereas stringent privacy legislation prompts buyers to favor on-device template storage, lifting ASPs. The fingerprint module market continues to profit from U.S. automotive biometrics, where luxury brands localize sourcing to hedge supply-chain risk after North Carolina quartz mine disruptions threatened wafer output.

Europe advances on the back of GDPR-aligned national e-ID plans and bank-driven biometric card launches. Middle East & Africa's latent demand crystallizes in national ID projects such as Cameroon's 2025 biometric card roll-out under a 15-year concession. South America provides incremental gains as smartphones penetrate mid-income cohorts and governments modernize social-benefits disbursement platforms, though macro volatility elongates procurement cycles.