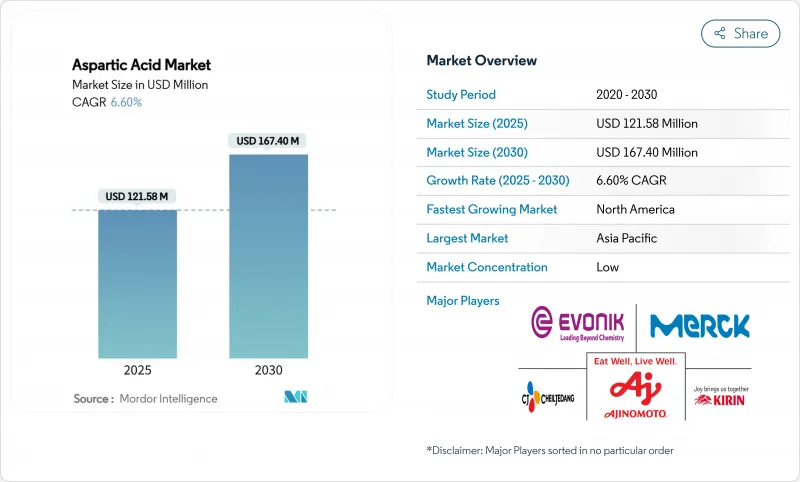

아스파르트산 시장은 2025년에 1억 2,158만 달러로 추정되고, CAGR 6.60%로 성장할 전망이며, 2030년에는 1억 6,740만 달러에 이를 것으로 예측됩니다.

이 시장은 여러 산업에 걸친 필수적인 용도로 일관된 성장을 보여줍니다. 아스파르트산은 식음료 제조, 특히 아스파르트산과 같은 인공 감미료의 제조에 있어서 주요 성분으로서 기능하여 소비자의 기호에 따른 무당 및 저칼로리 제품의 개발을 가능하게 합니다. 의약품에서 아스파르트산은 의약품과 보충제의 제형에서 중요한 역할을 하며 치료와 영양 요구를 모두 지원합니다. 또한 생분해성 폴리머나 인산염이 없는 세제 등 현재의 환경규제에 따른 지속가능한 공업 프로세스에 대한 용도도 시장 성장의 원동력이 되고 있습니다. 퍼포먼스 영양 및 영양 보충제에 대한 수요가 증가함에 따라 스포츠 및 웰니스 제품에서 아스파르트산의 사용이 강화되고 있습니다. 바이오 발효 생산 기술의 향상과 함께, 아스파르트산의 용도 범위가 확대되고 있으며, 아스파르트산은 건강에 초점을 맞춘 지속 가능한 솔루션에 필수적인 성분이 되고 있습니다.

아스파르트산 시장은 주로 아시아의 세제 첨가제에 대한 배합 증가로 인해 상당한 성장을 이루고 있습니다. 이 확대는 소비자 선호도의 진화, 엄격한 규제 프레임워크, 지역 전체의 지속적인 제품 혁신에 의해 기본적으로 형성됩니다. 아시아태평양에서는 환경에 대한 의식이 높아져 친환경 세탁 세제에 대한 소비자의 구매 패턴에 큰 영향을 미칩니다. 이 동향은 2023년 일본 가정이 세탁용 세제에 평균 4,500엔을 지출한다고 보고한 총무성의 데이터에서도 분명합니다. 이 시장의 진화에 대응하기 위해 세제 제조업체는 생분해성, 무해한 성분을 포함한 제품 포트폴리오를 전략적으로 재구성하고 있습니다. 아스파르트산 유래의 폴리머는 이러한 배합에 있어서 중요한 성분으로서 부상하고 있으며, 환경의 지속가능성과 스케일 및 할라이트 억제제로서의 우수한 성능이라는 2가지 이점을 제공합니다. 아시아 시장에서 이러한 지속 가능한 세제 첨가제로의 전환은 아스파르트산의 세계 수요를 지속적으로 강화하고 시장의 강력한 성장 궤도를 확립하고 있습니다.

남성 불임 치료 및 스포츠 영양에서 D-아스파르트산(DAA) 수요 증가는 인구 동향과 시장 혁신 모두에서 강력하게 지지되어 아스파르트산 시장의 주요 성장 요인이 되고 있습니다. 중앙정보국(CIA)의 2024년 데이터에 따르면 대만과 한국의 여성 1인당 출생률은 각각 1.11명과 1.12명으로 세계에서 가장 낮고 동아시아에서 출생률의 큰 과제가 부각되고 있습니다. 이 인구 역학의 상황은 리프로덕티브 헬스(성과 생식에 관한 건강) 솔루션에 대한 소비자와 정부의 관심을 강화하고 있습니다. D-아스파르트산이 정자 생산과 운동성을 높이는 역할을 과학적으로 검증함으로써 불임 치료 보충제로서 채용이 증가했습니다. 각 회사는 남성의 생식에 관한 건강 요구에 대응하기 위해 D-아스파르트산을 보완적인 생식 기능 강화 성분과 조합한 신제품을 출시하고 있습니다. 이러한 보충제는 불임에 관심이 있는 소비자와 스포츠 영양 이용자 모두를 대상으로 하며, 정자의 질 개선, 호르몬 조절, 운동 능력 향상 등의 효과를 노리고 판매되고 있습니다. 불임 치료에 대한 관심과 스포츠 영양 요구의 융합은 D-아스파르트산 시장 위치를 지속적으로 강화하고 있으며, 아스파르트산 시장의 지속적인 성장 가능성을 보여줍니다.

D-아스파르트산(DAA) 보충제의 표시에 관한 규제 요건은 제품의 처방, 마케팅, 소비자의 수용에 영향을 주어 아스파르트산 시장을 제약하고 있습니다. 캐나다 보건부와 식품의약국(FDA)은 주의사항, 용량 제한, 건강 강조 표시 제한 등 영양보조 식품에 대한 종합적인 표시 요건을 실시했습니다. 식품의약국(FDA)의 2025년 2월 아스파르트산 검토는 아미노산 보충제와 그 건강 강조 표시에 대한 모니터링의 강화를 보여줍니다. 이러한 규제는 소비자를 보호하는 반면, 규정 준수 비용 및 시장 잠재력 감소를 통해 고용량 또는 장기 D-아스파르트산 보충제 제조업체에 도전 과제를 안겨줍니다. D-아스파르트산과 같은 새로운 영양 성분은 안전과 효능의 과학적 검증이 요구되므로 제품 승인은 더욱 복잡해지고 지연됩니다. 이러한 규제 요건은 제품 개척, 마케팅, D-아스파르트산 보충제에 대한 소비자의 신뢰에 장애를 가져오고 시장 확대를 제한하고 있습니다.

L-아스파르트산은 2024년에 71.16%의 점유율로 시장을 독점했습니다. 이 중요한 시장 지위는 여러 산업에서 필수적인 역할을 담당하고 있기 때문입니다. 식품 분야에서 L-아스파르트산은 식품 및 식품 및 식음료 제조에서 일반적인 인공 감미료인 아스파르트산의 합성에 필수적이며, 저칼로리 및 설탕 미사용 제품에 대한 수요 증가에 대응하고 있습니다. 이 화합물은 또한 의약품과 보충제의 성분으로서 의약 제제에 필수적이며, 세정 성능을 향상시키는 킬레이트제로서 산업용 세제의 제조에도 사용됩니다. L-아스파르트산의 확립된 생산 인프라와 광범위한 산업 용도 분야는 시장에서의 입지를 강화하고 있습니다.

D-아스파르트산은 2025-2030년 CAGR 7.93%로 예측되는 시장에서 가장 급성장하고 있는 부문입니다. 이 성장은 퍼포먼스 영양 및 생식 건강 보충제에서 사용 증가 때문입니다. 이 화합물은 호르몬 밸런스, 특히 테스토스테론 수치를 지원함으로써 인식되며 운동 선수와 피트니스 애호가를 위한 스포츠 영양 제품에 유용합니다. 또한, 남성 생식 건강에서의 역할은 불임 치료 보충제의 존재감을 높입니다. 피트니스, 운동 능력, 생식 건강에 대한 소비자의 관심의 높아짐과 D-아스파르트산의 유효성을 뒷받침하는 조사의 조합이, 특수한 건강 및 영양 제품에 있어서 시장 확대의 원동력이 되고 있습니다.

바이오 발효는 아스파르트산의 주요 생산 수법으로서의 지위를 확립하고 있으며, 2024년에는 시장 점유율의 59.36%를 차지하였고, 2030년까지의 CAGR은 8.32%로 대폭적인 성장 가능성을 나타내고 있습니다. 이 시장의 장점은 운영 비용 효율성, 생산 확장성, 환경 지속가능성 등으로 인해 대규모 산업 용도 분야에 특히 유리합니다. 이 기술은 원료를 아스파르트산으로 전환시키는 데 특정 미생물을 사용하므로 환경에 미치는 영향을 최소화하면서 지속 가능한 제조 프로토콜에 대한 시장 요구 증가에 대응할 수 있습니다. 바이오 발효 공정은 아스파르트산의 대규모 생산, 특히 생산량과 품질의 안정성이 가장 중요한 과제인 아스파르트산과 같은 감미료 용도에 필수적인 구성 요소로 작용하는 식품 및 식음료 산업에서 큰 지지를 얻고 있습니다.

화학 합성 기술은 특히 신속한 처리 능력, 정확한 수율 관리 및 일관된 제품 사양이 필요한 용도에 있어서 아스파르트산 산업에서 큰 시장 존재를 유지합니다. 이 방법은 말레산 무수물과 푸마르산을 암모놀리시스와 환원적 아미노화라는 확립된 공정으로 변환하는 것으로, 제조업체에게 예측 가능한 비용 구조 및 확립된 산업 공급망 네트워크를 제공합니다. 이 제조법은 석유화학 인프라가 발달하는 지역이나 발효 원료의 입수에 제약이 있는 지역에서는 특히 유효합니다. 게다가, 화학 합성은 L-아스파르트산과 D-아스파르트산을 포함한 다수의 아스파르트산 변이체의 제조를 용이하게 하여, 의약품 및 영양 보충제 제조 용도에서 수요 증가에 대응합니다.

아시아태평양은 아스파르트산 시장의 43.76%를 차지했으며, 제조 인프라, 원료의 이용가능성, 최종 용도 분야에서의 국내 수요 증가가 이를 지원하고 있습니다. 중국은 정부와 민간 부문의 아미노산 제조 시설 투자를 통해 이 지역의 생산 능력을 선도하고 있습니다. 미국 농무부(USDA)의 Grain and Feed Update에 따르면 중국의 옥수수 생산량은 2024-2025년 2억 9,490만 톤에 달했고, 전년도에서 2% 증가했습니다. 이러한 옥수수 생산량 증가는 바이오 발효에 의한 L-아스파르트산 및 D-아스파르트산 생산에 필수적인 포도당 및 전분 유도체를 포함하는 발효 원료의 가용성을 증가시킵니다. 이 지역은 도시화, 소득 증가, 건강 선호도 변화를 원동력으로 하는 생산부터 소비까지 일관된 시스템을 통해 시장 주도권을 유지하고 있습니다.

북미는 지역별로 가장 높은 성장률을 나타내며 2025-2030년 CAGR 8.91%로 성장이 예측됩니다. 이 성장은 아스파르트산이 아미노산 요법, 영양 보조 식품, 호르몬 조정 화합물에 필수적인 의약품 및 영양 보조 식품 분야에서 수요 증가에 기인하고 있습니다. 미국과 캐나다는 견고한 연구개발 인프라와 혁신을 지원하는 규제된 시장 환경에 힘입어 기능성 성분의 상업화에 탁월합니다. 이 지역은 스포츠 영양, 임상 영양, 클린 라벨 제제에 중점을 두고 있으며, 아스파르트산과 그 유도체에 있어서 고도의 용도를 추진하고 있습니다. 수탁 제조업자와 생명공학 기업의 성장으로 새로운 건강 동향에 대응하는 신속한 생산 확대가 가능해지고 있습니다.

유럽은 규제 요건과 지속가능성에 대한 노력을 통해 시장에서의 지위를 유지하고 있습니다. 유럽연합(EU)의 인산염 금지령은 인산염 기반 킬레이트제의 대안으로 세제 및 수처리 용도에서 아스파르트산 유도체의 사용을 증가시키고 있습니다. 이 지역에서는 생분해성 솔루션에 대한 노력으로 농업 용도의 보수 및 영양 공급 시스템에 있어서 아스파르트산계 폴리머의 채용이 증가하고 있습니다. 영국 시장은 소비자의 무당 대체품에 대한 선호와 친환경 소재에 대한 정부 지원으로 성장 잠재력을 발휘합니다. 유럽 제약 산업은 의약품 제제에 아스파르트산을 이용하고 있으며, 이 지역의 다양한 용도 및 시장 안정성에 기여하고 있습니다.

The Aspartic Acid market is valued at USD 121.58 million in 2025 and is expected to reach USD 167.40 million by 2030, registering a CAGR of 6.60%.

The market demonstrates consistent growth due to its essential applications across multiple industries. Aspartic Acid serves as a key component in food and beverage manufacturing, particularly in the production of artificial sweeteners like aspartame, which enables the development of sugar-free and low-calorie products aligned with consumer preferences. In pharmaceuticals, aspartic acid plays a vital role in medication and supplement formulations, supporting both therapeutic and nutritional needs. The market growth is also driven by its applications in sustainable industrial processes, including biodegradable polymers and phosphate-free detergents, which align with current environmental regulations. The increasing demand for performance nutrition and dietary supplements has enhanced aspartic acid usage in sports and wellness products. The expanding application range, coupled with improvements in bio-fermentation production techniques, establishes aspartic acid as an essential component in health-focused and sustainable solutions.

The aspartic acid market is experiencing substantial growth, primarily driven by its increasing incorporation in Asian detergent additives. This expansion is fundamentally shaped by evolving consumer preferences, stringent regulatory frameworks, and continuous product innovations across the region. In the Asia-Pacific region, heightened environmental awareness has significantly influenced consumer purchasing patterns toward eco-friendly laundry detergents. This trend is evidenced by data from the Ministry of Internal Affairs and Communications, which reported that Japanese households allocated an average of 4.5 thousand yen to laundry detergents in 2023 . In response to this market evolution, detergent manufacturers have strategically reformulated their product portfolios to include biodegradable and non-toxic components. Aspartic acid-derived polymers have emerged as a crucial ingredient in these formulations, offering dual benefits of environmental sustainability and superior performance as scale and halite inhibitors. This shift toward sustainable detergent additives in the Asian market continues to strengthen the global demand for aspartic acid, establishing a robust growth trajectory for the market.

The escalating demand for D-aspartic acid (DAA) in male fertility and sports nutrition is a key growth driver for the aspartic acid market, strongly supported by both demographic trends and market innovation. According to the Central Intelligence Agency (CIA) data for 2024, Taiwan and South Korea reported fertility rates of 1.11 and 1.12 children per woman, respectively, the lowest worldwide, highlighting a significant fertility challenge in East Asia. This demographic situation has intensified consumer and government attention on reproductive health solutions. The scientific validation of D-aspartic acid's role in enhancing sperm production and motility has increased its adoption in fertility supplements. Companies are introducing new products incorporating D-Aspartic Acid with complementary fertility-enhancing ingredients to address male reproductive health needs. These supplements target both fertility-focused consumers and sports nutrition users, marketed for their benefits in sperm quality improvement, hormonal regulation, and athletic performance enhancement. The convergence of fertility concerns and sports nutrition requirements continues to strengthen the market position of D-Aspartic Acid, indicating sustained growth potential in the aspartic acid market.

Regulatory requirements for D-aspartic acid (DAA) supplementation labeling constrain the aspartic acid market by affecting product formulation, marketing, and consumer acceptance. Health Canada and the Food and Drug Administration (FDA) enforce comprehensive labeling requirements for dietary supplements, including cautionary statements, dosage limits, and health claim restrictions. The Food and Drug Administration (FDA)'s February 2025 aspartame review indicates increased scrutiny of amino acid supplements and their health claims. While these regulations protect consumers, they create challenges for manufacturers of high-dose or long-term D-aspartic acid supplements through compliance costs and reduced market potential. The requirement for scientific validation of safety and efficacy for new dietary ingredients like D-aspartic acid further complicates and delays product approvals. These regulatory requirements limit market expansion by creating obstacles for product development, marketing, and consumer confidence in D-aspartic acid supplements.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

L-Aspartic Acid dominates the market with a 71.16% share in 2024. This significant market position stems from its essential role across multiple industries. In the food sector, L-Aspartic Acid is essential for aspartame synthesis, a common artificial sweetener in food and beverage manufacturing, meeting the increasing demand for low-calorie and sugar-free products. The compound is also vital in pharmaceutical formulations as a component for drugs and supplements, and in industrial detergent manufacturing as a chelating agent that improves cleaning performance. The established production infrastructure and broad industrial applications of L-Aspartic Acid strengthen its market position.

D-Aspartic Acid represents the market's fastest-growing segment, with a projected CAGR of 7.93% from 2025 to 2030. This growth results from its increased use in performance nutrition and reproductive health supplements. The compound has gained recognition for supporting hormonal balance, particularly testosterone levels, making it valuable in sports nutrition products for athletes and fitness enthusiasts. Its role in male reproductive health has also increased its presence in fertility supplements. The combination of growing consumer interest in fitness, athletic performance, and reproductive health, along with research supporting D-Aspartic Acid's effectiveness, drives its market expansion in specialized health and nutrition products.

Bio-fermentation has established itself as the predominant production methodology for aspartic acid, commanding 59.36% of the market share in 2024 and exhibiting substantial growth potential with an 8.32% CAGR through 2030. This market dominance is attributed to its operational cost-effectiveness, production scalability, and environmental sustainability characteristics, rendering it particularly advantageous for large-scale industrial applications. The methodology employs specific microorganisms for the conversion of raw materials into aspartic acid, consequently minimizing environmental impact while addressing increasing market requirements for sustainable manufacturing protocols. The bio-fermentation process has gained significant traction in the food and beverage industry, where it serves as an essential component in the large-scale production of aspartic acid, particularly for sweetener applications such as aspartame, where production volume and quality consistency are paramount considerations.

Chemical synthesis methodologies maintain a substantial market presence in the aspartic acid industry, particularly in applications necessitating expedited processing capabilities, precise yield control, and consistent product specifications. The methodology encompasses the transformation of maleic anhydride or fumaric acid through established processes of ammonolysis or reductive amination, providing manufacturers with predictable cost structures and well-established industrial supply chain networks. This production approach remains particularly viable in geographical regions characterized by developed petrochemical infrastructure or areas experiencing limitations in fermentation feedstock availability. Furthermore, chemical synthesis facilitates the production of multiple aspartic acid variants, including L-aspartic acid and D-aspartic acid, thereby addressing increasing demand requirements within pharmaceutical and nutraceutical manufacturing applications.

The Aspartic Acid Market is Segmented by Product Type (L-Aspartic Acid, and D-Aspartic Acid), by Production Method (Bio-Fermentation, and More), by Purity Grade (Food Grade, Pharmaceutical Grade, and More), by Application (Food and Beverages, Nutraceuticals and Dietary Supplements, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commands 43.76% of the aspartic acid market, supported by its manufacturing infrastructure, feedstock availability, and increasing domestic demand across end-use sectors. China leads the regional production capacity through government and private sector investments in amino acid manufacturing facilities. The country's agricultural strength provides a significant advantage; the United States Department of Agriculture (USDA)'s Grain and Feed Update reports China's corn production reached 294.9 million metric tons in MY 2024/25, a 2% increase from the previous year . This corn production growth increases the availability of fermentation feedstocks, including glucose and starch derivatives, essential for L- and D-aspartic acid production through bio-fermentation. The region maintains its market leadership through an integrated production-to-consumption system, driven by urbanization, increasing incomes, and changing health preferences.

North America demonstrates the highest regional growth rate, with a projected CAGR of 8.91% from 2025 to 2030. This growth stems from increased demand in pharmaceutical and nutraceutical sectors, where aspartic acid is essential for amino acid therapies, dietary supplements, and hormone-regulating compounds. The United States and Canada excel in commercializing functional ingredients, backed by robust research and development infrastructure and a regulated market environment that supports innovation. The region's focus on sports nutrition, clinical nutrition, and clean-label formulations drives advanced applications of aspartic acid and its derivatives. The growth of contract manufacturers and biotechnology companies enables rapid production scaling to meet emerging health trends.

Europe maintains its market position through regulatory requirements and sustainability initiatives. The European Union's phosphate ban has increased the use of aspartic acid derivatives in detergents and water treatment applications as alternatives to phosphate-based chelating agents. The region's commitment to biodegradable solutions has increased the adoption of aspartic acid-based polymers in agricultural applications for water retention and nutrient delivery systems. The United Kingdom market demonstrates growth potential due to consumer preference for sugar-free alternatives and government support for environmentally friendly materials. Europe's pharmaceutical industry utilizes aspartic acid in drug formulations, contributing to the region's diverse application range and market stability.