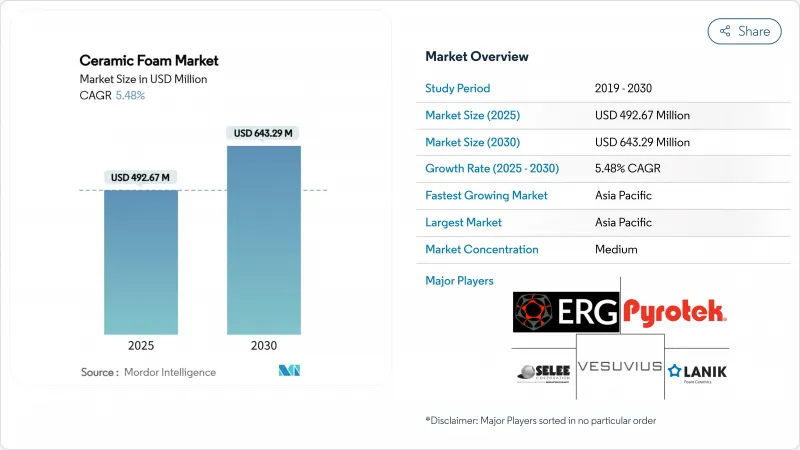

세라믹 폼 시장 규모는 2025년에 4억 9,267만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.48%로 성장할 전망이며, 2030년에는 6억 4,329만 달러에 달할 것으로 예측됩니다.

세라믹 폼이 고온 안정성, 내약품성, 제어된 기공률을 실현하고, 종래의 내화물이나 여과 매체의 대부분을 능가하기 때문에 수요가 가속하고 있습니다. 전기자동차 주조 허브, 수소 제조 시설, 서큘러 이코노미 철강 미니 밀의 급성장으로 고객 기반이 확대되고 있습니다. 첨단 복제 공정은 대량 생산에서 비용 우위를 유지하는 반면, 적층 성형은 복잡한 개방형 셀 형상의 수익성이 높은 틈새 시장을 엽니다. 또한 북미와 유럽의 제로 에너지 건축 기준이 강화됨에 따라, 생산자는 새로운 단열재 제조의 기회를 발견하고 있습니다. 한편, 원료 가격의 변동과 전자동 주조의 취성 과제가 당면의 이익을 줄이기 위해 공급업체는 재료 강화와 공급망 헤지 전략을 추구하게 됩니다.

전기자동차 플랫폼은 전도성과 피로의 목표를 충족시키기 위해 매우 깨끗한 용융이 필요한 대형 알루미늄 구조 주물을 사용합니다. 세라믹 폼 필터는 배터리 하우징과 모터 케이싱에 10ppm 이하의 용융 금속을 함유시킬 수 있습니다. Vesuvius는 기존 자동차용 라인에 비해 EV 전용 파운드리에서 SEDEX 실리콘 카바이드 필터의 사용률이 40% 높다고 보고했습니다. 테슬라의 상하이 사업소와 아시아의 유사한 시설에서는 고압 다이캐스팅용으로 탄화규소 발포체가 지정되어 있어 지역의 생산량을 견인하고 있습니다. 이러한 사양은 처리량과 재현성 기준을 높여 개선된 복제 방법으로 제조된 견고한 개방형 셀 형상을 선호합니다. 아시아태평양에서 공급망의 현지화 노력은 세라믹 폼 시장의 지역적 이점을 더욱 견고하게 만들었습니다.

세계적인 전해조와 수증기 개질의 확대에 의해 부식성 분위기에서의 600-900℃의 반복 운전에 견디는 내화물 담체가 요구되고 있습니다. Ceramics UK 컨소시엄은 100% 수소 연소 킬른을 검증하여 세라믹 폼이 차세대 에너지 시스템에 적합한지 확인했습니다. 산고방은 촉매 담체의 생산량을 확대하기 위해 뉴욕에 4,000만 달러를 투자하고 있으며, 북미의 기세를 강조하고 있습니다. 세라믹 폼으로 강화된 코디에라이트 모노리스는 800℃에서 최적의 선택성을 달성하여 개질기와 고체 산화물 연료전지의 사용 간격을 연장합니다. 수소 로드맵을 발표하는 지역이 늘어남에 따라, 촉매 담체의 주문은 세라믹 폼 시장의 지속적인 성장 경로가 됩니다.

고순도 알루미나와 지르코니아는 세라믹 폼 제조에서의 변동비의 대부분을 차지합니다. 급격한 가격 변동으로 인해 분기별 계약 재협상과 비싼 스팟 구매가 강요되고 있습니다. 지르코니아 강화는 압축 강도를 206% 향상시키지만 원료 지수가 상승하면 경제성이 저하됩니다. 모건 어드밴스드 머티리얼스는 열 세라믹 부문의 수주가 안정화되었음에도 불구하고 매출이 4.6% 감소했다고 지적했습니다. 장기 계약이 없는 아시아의 소규모 제조업체는 마진 압축에 휩싸였으며, 세라믹 폼 산업에서 플랜트 업그레이드와 능력 증진이 지연되었습니다.

탄화규소는 1,500℃ 이상의 안정성, 용융 알루미늄에 대한 내성, 우수한 열전도성으로 2024년 세라믹 폼 시장에서 45.18%의 점유율을 차지했습니다. EV 주조량 증가와 엄격한 함량 제한이 수요의 지속을 지원하고 있습니다. 마그네슘 알루미네이트 스피넬, 붕화물 세라믹, 하이브리드 복합재료 등의 다른 첨단 조성물은 CAGR 7.76%에서 가장 급성장하는 클러스터를 형성하여 항공우주, 원자력, 초고온의 요구를 충족하고 있습니다. 산화알루미늄은 그 온도 상한이 새로운 EV나 수소 부문에 대한 침투를 제약하고 있는 것, 높은 비용 효율로 범용 주철용으로서 여전히 매력적입니다. 산화지르코늄은 화학적으로 침식성이 높은 용융물에서 틈새 지위를 유지하고 있으며, 수명 연장과 내식성 강화에 의해 그 비싼 가격이 정당화되고 있습니다.

2세대 붕화물 발포체는 1,800℃ 이상의 내산화성을 나타내며 극초음속기의 열보호부품으로 자리매김합니다. 설문조사의 프로토타입은 1,000회의 열 사이클 후 질량 감소가 5% 미만이며, 이는 미래 상업화에 박차를 가할 이정표입니다. 재료 과학자가 위스커 보강과 산화물 스케일을 결합한 다상 발포체를 합성함에 따라 세라믹 폼 시장은 극한 환경에서 기존의 알루미나를 단계적으로 대체할 수 있습니다.

복제 또는 폴리머 스펀지 법은 수십년동안 설비 상각, 낮은 스크랩 비율 및 익숙한 품질 관리를 통해 2024년에 출하된 전체 세라믹 폼의 67.24%를 생산했습니다. 10-60ppi의 일관된 구멍 직경의 필터 제조가 뛰어나 대량의 비철 주조에 공헌하고 있습니다. 그 이점에도 불구하고, 세라믹 폼 시장은 CAGR 7.91%에서 가장 빠르게 성장하는 라미네이션 모델로 축발을 옮기고 있습니다. 레이저 소결된 알루미나 격자와 직접 잉크로 칠한 코디에라이트 캐리어는 복제 루트에서는 달성할 수 없는 단계적인 기공률과 토폴로지 최적화를 가능하게 합니다. 촉매 담체와 항공우주 분야에서 신속하게 채택된 기업은 설계의 자유도를 이용하여 유동의 균일성과 기계적 탄력성을 높이고 있습니다.

세라믹 슬러리에 가스를 혼합하고 생성된 거품을 소결하는 직접 발포는 폴리 우레탄 템플릿과 이에 따른 소손 배출을 제거합니다. 그린 빌딩의 크레딧을 타겟으로 한 단열 패널에 가장 많이 채용되고 있습니다. 겔 캐스팅은 바이오메디컬 임플란트나 반도체 웨이퍼 서포트 등, 넷 셰이프에 가까운 정밀도가 요구되는 용도에 사용되고 있지만, 사이클 타임이 비교적 길기 때문에 보급에는 한계가 있습니다.

아시아태평양의 2024년 판매 점유율 46.82%는 원재료, 주조 시설 및 하류 EV 생산을 포함한 통합 공급망을 반영합니다. 중국의 지속적인 철강 생산과 일본의 첨단 세라믹 연구가 기준선량을 유지하고 한국의 수소경제 로드맵이 촉매 폼의 미래 수요를 높입니다. 예측에 의하면, 이 지역의 세라믹 폼 시장은 예측 기간 중 CAGR 7.42%의 견조한 성장을 나타내고 현저한 성장을 이룰 것으로 예측됩니다. 스마트 매뉴팩처링과 에너지 효율을 위한 정부 보조금은 주조, 자동차, 건설 분야에서의 채용을 촉진합니다.

북미는 성숙하면서도 혁신적인 분야입니다. 이 지역은 적층 조형의 선구자이며 연방 정부의 수소 및 배터리 공급망 보조금의 혜택을 받고 있습니다. 산고방의 뉴욕 진출은 국내 촉매 지원 수요에 대한 자신감을 뒷받침합니다. 미국의 자동차 배기 가스 규제 강화가 세라믹 배기 필터의 소비를 자극합니다. 중서부에서의 안정된 철 주조 사업과 EV 부품용의 성장하는 알루미늄 주조가 수요의 회복력을 확보하고 있습니다.

유럽에서는 순환형 경제와 탄소 중립강의 의무화가 우선되어 미니 밀에서 재활용 가능한 내화 발포체의 이용이 촉진됩니다. 독일, 프랑스, 이탈리아가 자동 필터링 시스템으로 주조 라인을 업그레이드하고 더 강인한 폼 배합 연구에 박차를 가합니다. EU 보조금은 항공우주 및 방위를 위해 맞춤형 세공 구조를 생산하는 첨가제 제조 파일럿 라인을 지원합니다. 엄격한 건축 에너지 지령은 리노베이션 프로젝트에서 세라믹 단열 패널의 전개를 자극합니다.

남미와 중동, 아프리카는 규모는 작지만 성장하고 있습니다. 브라질과 아르헨티나의 자동차 제조업체가 알루미늄 주조 필터를 채택하는 반면, 사우디아라비아의 '비전 2030'에서 새로운 철강 생산 능력은 내화물 수요를 밀어 올립니다. 외국 직접투자는 현지 능력을 높이는 첨단 재료 연구기관을 지원하고 있습니다. 인프라 격차와 제한된 기술 전문 지식은 채용을 늦추고 있지만 현지 생산 파트너십은 세라믹 폼 산업의 잠재적 가능성을 극복할 수 있습니다.

The Ceramic Foam Market size is estimated at USD 492.67 million in 2025, and is expected to reach USD 643.29 million by 2030, at a CAGR of 5.48% during the forecast period (2025-2030).

Demand is accelerating as ceramic foam delivers high-temperature stability, chemical resistance and well-controlled porosity that outperform many legacy refractory and filtration media. Rapid growth in electric-vehicle casting hubs, hydrogen production facilities and circular-economy steel mini-mills is widening the customer base. Advanced replica processes retain cost advantages in high-volume production, while additive manufacturing opens profitable niches for complex open-cell geometries. Producers also see new insulation opportunities as North American and European zero-energy building codes tighten. Meanwhile, raw-material price volatility and brittleness challenges in fully automated foundries temper near-term margins, prompting suppliers to pursue material toughening and supply-chain hedging strategies.

Electric-vehicle platforms use large aluminum structural castings that require exceptionally clean melts to meet conductivity and fatigue targets. Ceramic foam filters now enable sub-10 ppm inclusion levels in battery housings and motor casings. Vesuvius reports 40% higher uptake of SEDEX silicon-carbide filters in EV-dedicated foundries compared with conventional automotive lines. Tesla's Shanghai operations and similar Asian facilities specify silicon-carbide foams for high-pressure die casting, driving regional volume. These specifications raise throughput and repeatability criteria that favor robust open-cell geometries produced via improved replica methods. Supply-chain localization efforts in Asia-Pacific further cement regional dominance of the ceramic foam market.

Global electrolyzer and steam-reform expansion demands refractory carriers that withstand cyclic 600-900 °C operation in corrosive atmospheres. The Ceramics UK consortium validated 100% hydrogen-fired kilns, confirming ceramic foam suitability for next-generation energy systems. Saint-Gobain is investing USD 40 million in New York to scale catalyst-carrier output, highlighting North American momentum. Cordierite monoliths reinforced with ceramic foam achieve optimal selectivity at 800 °C, extending service intervals for reformers and solid-oxide fuel cells. As more regions publish national hydrogen roadmaps, catalyst support orders provide a durable growth pathway for the ceramic foam market.

High-purity alumina and zirconia constitute a significant portion of the variable costs in ceramic foam production. Sharp price swings have forced quarterly contract renegotiations and spot purchases at elevated premiums. Zirconia toughening boosts compressive strength by 206% yet becomes less economical when raw-material indices spike. Morgan Advanced Materials noted a 4.6% revenue dip in its Thermal Ceramics unit despite stable order intake because surcharges lagged cost inflation. Smaller Asian producers, lacking long-term contracts, experienced margin compression that slowed plant upgrades and capacity additions within the ceramic foam industry.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Silicon carbide commanded 45.18% share of the ceramic foam market in 2024 due to its stability above 1,500 °C, resistance to molten aluminum and superior thermal conductivity. Rising EV casting volumes and stringent inclusion limits underpin sustained demand. Other advanced compositions such as magnesium-aluminate spinel, boride ceramics and hybrid composites form the fastest-growing cluster at a 7.76% CAGR, fulfilling aerospace, nuclear and ultra-high-temperature needs. Aluminum oxide remains attractive for general-purpose iron casting thanks to cost-efficiency, though its temperature ceiling constrains penetration into new EV and hydrogen segments. Zirconium oxide retains a niche in chemically aggressive melts, where its premium price is justified by extended service life and enhanced corrosion resistance.

Second-generation boride foams demonstrate oxidation resistance above 1,800 °C, positioning them for hypersonic vehicle thermal-protection components. Research prototypes exhibit less than 5% mass loss after 1,000 thermal cycles, a milestone that could spur future commercialization. As material scientists synthesize multiphase foams combining whisker reinforcement and oxide scales, the ceramic foam market may witness incremental displacement of legacy alumina in extreme environments.

The replica or polymer-sponge process produced 67.24% of all ceramic foams shipped in 2024 owing to decades of equipment amortization, low scrap rates and familiar quality controls. It excels in producing filters with consistent pore sizes from 10 to 60 ppi, serving high-volume non-ferrous foundries. Despite its dominance, the ceramic foam market is pivoting toward additive manufacturing, the fastest-growing process at 7.91% CAGR. Laser-sintered alumina lattices and direct-ink-written cordierite carriers allow graded porosity and topology optimization unattainable with replica routes. Early adopters in catalyst support and aerospace exploit design freedom to enhance flow uniformity and mechanical resilience.

Direct foaming, which mixes gas into ceramic slurry then sinters the resulting froth, eliminates polyurethane templates and their associated burn-out emissions. Uptake is strongest in insulation panels targeting green-building credits. Gel casting endures in applications requiring near-net-shape precision, such as biomedical implants and semiconductor wafer supports, though its relatively long cycle times limit broader diffusion.

The Ceramic Foam Market Report is Segmented by Type (Aluminum Oxide, Silicon Carbide, and More), Manufacturing Process (Replica/Polymer Sponge Method, Direct Foaming, and More), Application (Molten Metal Filtration, Automotive Exhaust Filters, and More), End-User Industry (Foundry, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's 46.82% revenue share in 2024 reflects its integrated supply chain encompassing raw materials, casting facilities and downstream EV production. China's continual steel output and Japan's advanced ceramics research sustain baseline volumes, while South Korea's hydrogen-economy roadmap raises future demand for catalyst foams. Forecasts indicate the region's ceramic foam market is projected to witness significant growth, supported by a robust 7.42% CAGR during the forecast period. Government grants for smart manufacturing and energy efficiency amplify adoption across foundry, automotive, and construction sectors.

North America represents a mature yet innovative arena. The region fields additive-manufacturing pioneers and benefits from federal hydrogen and battery-supply-chain funding. Saint-Gobain's New York expansion confirms confidence in domestic catalyst-support demand. Tightening US vehicle emissions rules stimulate ceramic exhaust filter consumption. Stable iron foundry operations in the Midwest and growing aluminum casting for EV parts ensure demand resilience.

Europe prioritizes circular economy mandates and carbon-neutral steel, driving uptake of recyclable refractory foams in mini-mills. Germany, France and Italy upgrade casting lines with automated filter-handling systems, spurring research into tougher foam formulations. EU grants back additive-manufacturing pilot lines that fabricate customized pore architectures for aerospace and defense. Stringent building energy directives stimulate ceramic insulation panel deployment in renovation projects.

South America and Middle East & Africa are smaller but rising. Brazilian and Argentinian automakers adopt aluminum casting filters, while new steel capacity in Saudi Arabia's Vision 2030 bolsters refractory demand. Foreign direct investment underpins advanced-materials institutes that enhance local competence. Infrastructure gaps and limited technical expertise slow adoption, yet localized production partnerships could unlock latent potential for the ceramic foam industry.