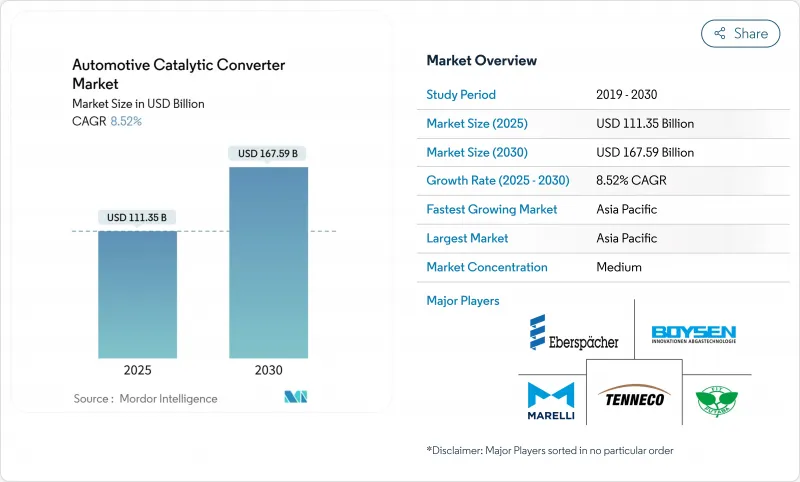

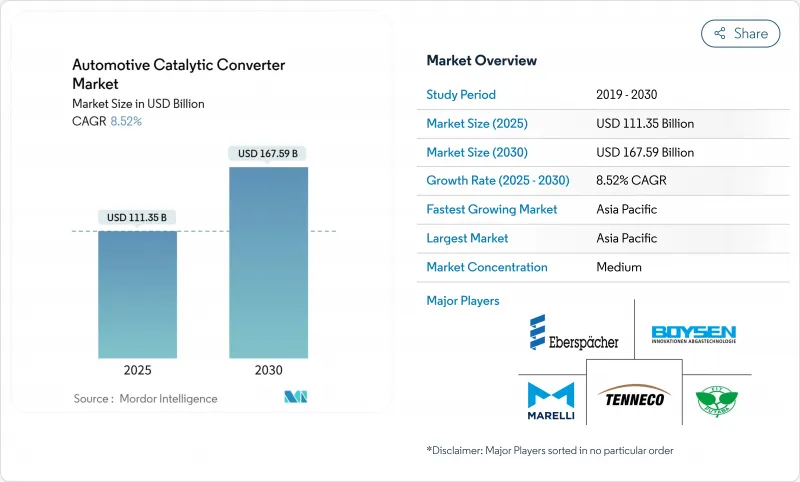

촉매 컨버터 시장은 2025년에 1,113억 5,000만 달러를 창출하고, 2030년에는 1,675억 9,000만 달러에 이를 것으로 예상되며, CAGR은 8.52%를 나타낼 전망입니다.

2025년 이후의 일관된 규제 강화를 반영한 것으로, Euro 7, China 7, 미국 규격의 갱신 등 모두 귀금속의 고충전과 고도의 워시코트 케미스트리를 의무화하고 있습니다. 추가적인 기세는 세계 내연 및 하이브리드 자동차 생산 회복, 비용 및 위험을 줄이는 귀금속 대체 전략, 비도로 기계 함대의 개조 활동에서 비롯됩니다. 공급망 회복력, 새로운 수소 내연 기관 프로젝트, 유망한 단일 소재 촉매가 촉매 컨버터 시장의 비즈니스 기회에 박차를 가하고 있습니다.

Euro 7은 2025년 7월부터 단계적으로 도입되어 적합 내구성이 8년/16만km로 연장됨에 따라 자동차 제조업체는 보다 두꺼운 귀금속층과 고급 가솔린 미립자 필터의 사양을 강요합니다. 차이나 7은 유로 7을 반영하고, 일부 점에서는 유로 7을 웃도는 것으로, 플랫폼 전체에서 미립자 수 규제와 실주행 배기 가스 시험을 의무화하고 있습니다. 미국에서는 오프로드 차량과 경차 규제가 강화되어 역사적인 규제의 격차가 해소되었습니다. 전 세계적으로 통일된 임계값은 OEM이 이전에 사용했던 시간 지연 쿠션을 제거하여 고급 3웨이 및 4웨이 시스템의 설계 사이클을 가속화합니다.

세계의 소형차 생산량은 가솔린, 디젤, 하이브리드의 각 라인에서 회복되었습니다. 상용 트럭은 물류 수요를 배경으로 생산 대수를 증가시켰고, 아시아태평양의 인프라 자극책은 대형차 조립 라인을 활발한 상태로 유지했습니다. 하이브리드 자동차는 생산량의 약 10%를 차지하고 빈번한 정지 시작 사이클 동안 콜드 스타트 방출을 억제하기 위해 더 많은 양의 촉매가 필요합니다. 중국기차공업협회는 열효율 향상과 선진적인 배기가스 규제 시스템을 통해 2035년까지 이산화탄소 배출량을 20% 삭감하는 것을 목표로 하는 3단계 개발 전략을 실시했습니다. 공장의 가동률이 정상화되면 장기적인 전동화 압력에도 불구하고 촉매 컨버터 시장의 당면 출하량이 증가합니다.

팔라듐은 2022년 1온스당 3,000달러 이상에서 2025년 초에 1,000달러를 인터럽트하고 백금도 900-1,100달러/온스 사이에서 변동하기 때문에 조달 예산이 복잡해지고 대체가 촉진됩니다. 공급업체는 위험 회피를 하고 있지만 소규모 참가자는 가격 변동을 상쇄하는 데 어려움을 겪고 있으며 단기 마진 전망이 없으며 비용 충격 발생 시 주문이 지연될 수 있습니다. 남아프리카의 광산 설비 투자 감축 계획은 10년 후 공급을 강화할 수 있습니다.

2024년 촉매 컨버터 시장은 화학양론적 가솔린 엔진에 대한 보편적인 적합을 반영하여 삼방 컨버터가 66.78%의 점유율을 유지했습니다. 미립자 물질의 수와 내구성에 대한 규제가 강화됨에 따라이 형식은 컴플라이언스의 핵심 역할을 담당하지만 금속 담지와 워시 코트의 배합은 계속 발전하고 있습니다. 3웨이 유닛의 촉매 컨버터 시장 규모는 콜드 스타트 이벤트를 확대하는 하이브리드화에 힘입어 2030년까지 자동차 생산 대수 전체에 맞추어 증가할 것으로 예측됩니다.

사방 컨버터, 린 NOx 트랩, 복합형 선택 촉매 환원 시스템의 새로운 파도는 "기타 유형" 카테고리에 집중되어 CAGR 11.83%를 나타낼 것으로 예측됩니다. 워싱턴 주립대학의 연구실에서는 고배기열에 의해 나노스케일 세리아의 클러스터화가 촉진되어 귀금속의 사용량을 줄이면서 활성이 10배가 되는 것을 발견하고 있습니다. 자기 재생형 페로브스카이트 촉매의 병행 연구는 PGM 함량을 최대 90%까지 줄이는 것을 목표로 하며, 생산 규모와 내구성 벤치마크가 달성되면 보다 광범위한 채용이 가능해집니다.

2024년 촉매 컨버터 시장 점유율은 절대적인 생산 규모를 배경으로 승용차가 63.60%를 차지했습니다. 전동화가 진행됨에 따라 이 비율은 소폭으로 저하되는 것, 승용차용 촉매는 차량 수명의 길이, 하이브리드차의 후기 투입, 디젤·다운·사이즈·가솔린 전략의 대두 등에 의해 여전히 주력 제품이 되고 있습니다.

중형 대형 상용차의 CAGR은 가장 빠른 9.08%를 나타낼 전망입니다. 물류 확대, 인프라 투자, 대형차의 NOx 규제 강화가 차량 관리자를 보다 대용량의 촉매와 보다 긴 보증으로 향하게 합니다. 개발자는 이미 장거리 트럭 수송용 수소-ICE 시스템을 검증하고 있으며, NOx를 억제하면서 고온의 배기 온도에서 100%의 수소 스트림을 견뎌야 하는 삼원 촉매에 새로운 길을 열고 있습니다. 오프로드 기계는 틈새 시장이지만 맞춤형 파이프 가공 하우징이 장착 된 스테이지 V 후면 패키지를 사용하여 성장을 늘립니다.

아시아태평양은 2024년 촉매 컨버터 시장 수익의 49.82%를 차지하며 2030년까지 연평균 복합 성장률(CAGR) 7.85%를 나타낼 것으로 예측됩니다. 중국은 유럽 기준치를 초과하는 미립자 물질 수와 실제 주행 프로토콜을 통합한 China 7 표준을 배경으로 이 지역의 성장을 지원하고 있습니다. 인도는 국내 이동성 수요와 수출 주문을 모두 충족하기 위해 자동차 생산이 확대되고 생산량이 증가합니다. 지역의 대형차 생산 대수는 트럭과 오프로드 기기의 판매를 자극하는 인프라 파이프라인으로부터 혜택을 받습니다. 광저우 신거래소에 상장된 플래티넘과 팔라듐의 선물거래는 금속조달 전문성을 높여 현지 제조업체의 가격변동 리스크를 경감시킵니다.

북미는 CAGR 5.10%를 나타낼 것으로 예측됩니다. 연방규칙이 갱신되어 2032년까지 NMOG와 NOx의 50% 삭감이 의무화되어 가솔린의 미립자 필터 채용이 강제되었습니다. 텍사스, 미시간, 온타리오는 경차용 컨버터의 주요 생산 기지이며, 캘리포니아에서는 Tier 5 오프로드 규제가 건설 기계용 첨단 SCR 시스템을 견인하고 있습니다. 수소 ICE 시험소에 대한 투자는이 지역의 대체 추진에 대한 헌신을 보여주는 반면, NOx 감소는 후 처리에 의존합니다.

유럽의 CAGR은 4.80%를 나타낼 전망이지만, 이는 2035년 이후에 제로 방출의 판매가 의무화되어 그 압력하에 있는 성숙한 차량 기반을 반영하고 있습니다. Euro 7에서는 8년간의 내구성이 도입되어 적합 온도도 확대되므로 촉매의 당면 수요가 증가합니다. 선도적인 공급업체는 고밀도 워시코트, 전기 가열식 벽돌, NOx/미립자 재생 복합 알고리즘에 주력하며 Euro 7의 엄격한 규제를 충족합니다. 신차 수요가 평평해지면 논로드 플릿의 복고풍 활동이 애프터마켓 판매량을 유지합니다.

The catalytic converters market generated USD 111.35 billion in 2025 and is forecast to reach USD 167.59 billion by 2030, advancing at an 8.52% CAGR.

The expansion reflects consistent regulatory tightening after 2025, including Euro 7, China 7, and updated United States standards, all of which mandate higher precious-metal loadings and advanced wash-coat chemistries. Further momentum comes from the rebound in global internal-combustion and hybrid vehicle production, precious-metal substitution strategies that cut cost risk, and retrofit activity in non-road machinery fleets. Supply chain resilience, new hydrogen internal-combustion projects, and promising single-material catalysts round out the opportunity set for the catalytic converters market.

Euro 7 begins phasing in from July 2025 and extends compliance durability to eight years/160,000 km, forcing automakers to specify thicker precious-metal layers and sophisticated gasoline particulate filters. China 7 mirrors and, in several respects, exceeds Euro 7, requiring particulate-number limits and real-driving emissions testing across platforms. In the United States, tougher off-road and light-vehicle rules close historical regulatory gaps. Unified global thresholds remove the lag-time cushion OEMs once used, accelerating design cycles for advanced three- and four-way systems.

Worldwide light-vehicle output witnessed volume restoration across gasoline, diesel, and hybrid lines. Commercial trucks added volume on the back of logistics demand, while infrastructure stimulus in Asia-Pacific kept heavy-duty assembly lines active. Hybrids represented approximately 10% of production and need larger catalyst volumes to control cold-start emissions during frequent stop-start cycling. the China Association of Automobile Manufacturers is implementing a three-step development strategy targeting 20% carbon emissions reduction by 2035 through enhanced thermal efficiency and advanced emission control systems. Normalized factory utilization raises near-term unit shipments for the catalytic converters market despite longer-term electrification pressure.

Palladium's fall from more than USD 3,000/oz in 2022 to under USD 1,000/oz in early 2025, and platinum's swings between USD 900-1,100/oz, complicate sourcing budgets and encourage substitution. Suppliers hedge, but small participants struggle to offset price moves, reducing short-term margin visibility and delaying orders when cost shocks hit. Planned reductions in South African mine capex threaten to tighten supply later in the decade..

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Three-way converters retained a 66.78% share of the catalytic converters market in 2024, reflecting their universal fit for stoichiometric gasoline engines. Tightening particulate-number and durability rules keep this format central to compliance, though metal loading and wash-coat formulations continue to evolve. The catalytic converters market size for three-way units is forecast to rise in line with overall vehicle production through 2030, underpinned by hybridization that magnifies cold-start events.

A new wave of four-way converters, lean-NOx traps, and combined selective catalytic-reduction systems clusters in the "other types" category, which is projected to grow at 11.83% CAGR. Laboratory work at Washington State University shows that nano-scale ceria clustering induced by high exhaust heat boosts activity tenfold while using less precious metal, a discovery that may reshape cost curves. Parallel research into self-regenerating perovskite catalysts aims to cut PGM content by up to 90%, setting the stage for broader adoption once production scale and durability benchmarks are met.

Passenger cars dominated the 2024 volume with 63.60% catalytic converters market share, driven by their absolute production scale. Despite the portion declining modestly as electrification grows, passenger-car catalysts remain a staple due to long fleet lives, late-cycle hybrid launches, and emerging diesel-downsize gasoline strategies.

Medium and heavy commercial vehicles provide the fastest 9.08% CAGR. Logistics expansion, infrastructure spending, and stricter heavy-duty NOx ceilings push fleet managers toward higher-capacity catalyst bricks and longer warranties. Developers are already validating hydrogen-ICE systems for long-haul trucking, opening a fresh avenue for three-way catalysts that must tolerate 100% hydrogen streams at high exhaust temperatures while still curbing NOx. Off-road machinery, though niche, prolongs growth by tapping Stage V retrofit packages with bespoke pipe-fabricated housings.

The Catalytic Converter Market Report is Segmented by Converter Type (Two-Way Catalytic Converters, Three-Way Catalytic Converters, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Fuel Type (Gasoline, Diesel, and Hybrid), Substrate Material (Platinum, Palladium, and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 49.82% of the catalytic converters market revenue in 2024 and is expected to expand at a 7.85% CAGR through 2030. China anchors regional growth on the back of China 7 standards that embed particulate-number and real-driving protocols exceeding European thresholds. India adds volume as automotive production ramps up to meet both domestic mobility demand and export orders. Regional heavy-duty output benefits from infrastructure pipelines that stimulate truck and off-road equipment sales. Futures contracts for platinum and palladium listed on a new Guangzhou exchange further professionalize metal procurement, lessening price-shock exposure for local manufacturers.

North America is forecast to grow at 5.10% CAGR. Updated federal rules demand 50% NMOG + NOx cuts by 2032 and force gasoline particulate-filter adoption. Texas, Michigan, and Ontario remain key production clusters for light-vehicle converters, while Tier 5 off-road proposals in California pull through advanced SCR systems for construction machinery. Investments in hydrogen-ICE testing labs illustrate the region's commitment to alternative propulsion while still relying on after-treatment for NOx abatement.

Europe's 4.80% CAGR reflects a mature vehicle base under pressure from mandated zero-emission sales after 2035. Near-term catalyst demand rises as Euro 7 introduces eight-year durability and extended temperature compliance windows. Leading suppliers focus on higher density wash-coats, electrically heated bricks, and combined NOx/particulate regeneration algorithms to meet the stringent Euro 7 limits. Retrofit activity in non-road fleets sustains aftermarket volumes once new-car demand flattens.