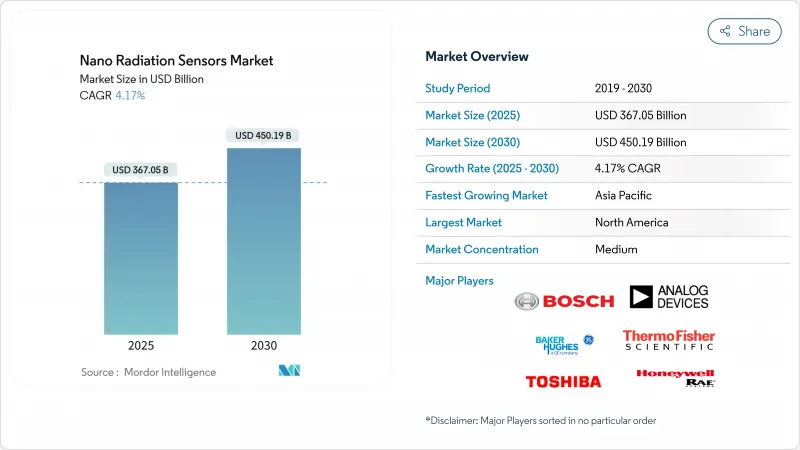

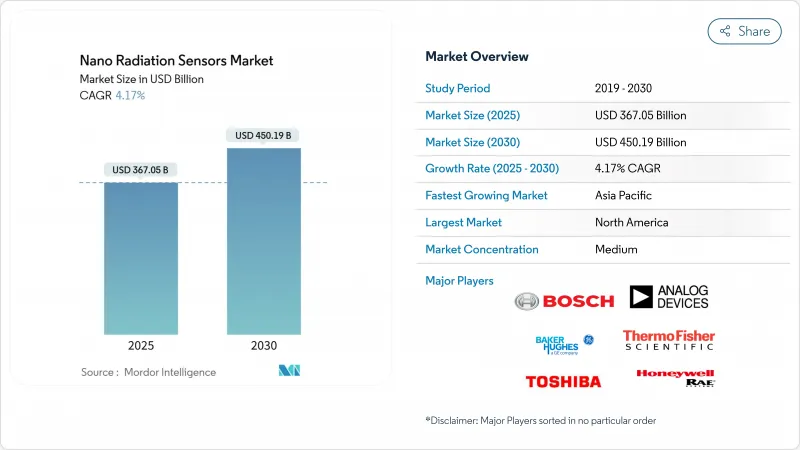

나노 방사선 센서 시장은 2025년에 3,670억 5,000만 달러로 평가되었고, CAGR 4.17%를 나타낼 것으로 예측되며, 2030년에는 4,501억 9,000만 달러에 이를 전망입니다.

성장은 소비자 가전, 항공우주, 자동차 시스템 전반에 걸친 지속적인 소형화와 함께 원자력 해체 및 우주 탐사 분야의 엄격한 안전 규정이 반영된 결과입니다. 최근 페로브스카이트 반도체 소재의 획기적인 발전으로 이제 스마트폰 통합 및 웨어러블 패치에 적용 가능한 수준의 소형 검출기 구현이 가능해져 오랜 기간 지속된 크기와 전력 장벽이 해소되었습니다. 영국 원자력 해체 당국의 3천만 파운드 지원 패키지에서 아날로그 디바이스에 대한 1억 5백만 달러 규모의 CHIPS 법 지원금에 이르기까지 정부의 지원책은 상용화 주기를 단축하고 공급 확대를 가속화합니다. 특히 대학 및 스타트업 임무에서 큐브샛(CubeSat)의 확산은 초경량 센서의 잠재적 시장 규모를 확대하는 동시에, 의료 방사선 측정 및 자동차 안전 하위 시스템에서도 병행 수요가 발생하고 있습니다. 제조 복잡성과 수율 손실은 여전히 가장 큰 제약 요소이지만, 재료 안정성 문제를 해결하면서 비용 통제를 유지하는 기업들은 즉각적인 경쟁 우위를 점하게 됩니다.

소비자 가전 및 자동차 플랫폼의 끊임없는 소형화는 방사선 센서 모듈을 웨이퍼 레벨 통합으로 이끌고 있습니다. 샤프는 7.5mW만 소비하는 25 X 20 X 2.5mm 모듈을 시연하여 스마트폰 기반 방사선 추적을 실용화했습니다. 5nm 및 3nm 공정 노드의 병행 발전으로 논리 회로와 감지 회로가 공통 다이(die)를 공유할 수 있게 되어 OEM(주문자 상표 부착 생산) 업체의 부품 비용이 절감됩니다. 자동차 분야에서는 소형 센서가 기존 전자 제어 장치(ECU) 내부에 장착되어 실내 디자인 변경 없이도 첨단 운전자 보조 시스템(ADAS)을 지원합니다. IoT 아키텍처가 확산됨에 따라 분산형 나노 방사선 센서를 공장 및 병원에 5년 전에는 달성 불가능했던 노드 단위 비용으로 배치할 수 있게 되었다.

표적화된 공공 프로그램은 인증을 조화시키면서 장기적 수요를 보장합니다. 미국 상무부는 아날로그 디바이시스(Analog Devices)의 국내 3개 팹 현대화를 위해 1억 5백만 달러를 배정하며 상업용 및 방위용 방사선 감지를 우선 출력물로 명시했습니다. 영국 원자력 해체 당국은 구형 원자로의 안전한 해체를 지원하기 위해 센서 연구개발에 3,000만 파운드를 투자했습니다. 동시에 유럽연합 집행위원회의 ‘호라이즌 유럽’ 플랫폼은 지속 가능한 방사선 보호 기술에 자원을 집중하고 있습니다. ISO와 IEEE 작업 그룹은 현재 통합 나노 센서 테스트 프로토콜을 마련 중으로, 이를 통해 규정 준수 주기를 단축하고 국경을 초월한 조달이 가능해질 전망입니다.

최신 검출기 구조에 필요한 10nm 미만 특징은 주류 로직 칩보다 높은 불량률을 보이며, 여러 파운드리에서 1차 수율을 60% 미만으로 떨어뜨리고 있습니다. 포토리소그래피 마스크 블랭크에 고순도 실리카를 공급하는 스프루스 파인(Spruce Pine)의 석영 광산 일시 폐쇄와 같은 공급망 충격은 핵심 소재 공급을 제한하여 비용 압박을 가중시킵니다. 팹 운영사는 더 엄격한 입자 제어 및 첨단 계측 기술을 도입해야 하므로 단기적으로 웨이퍼당 운영 비용이 증가합니다.

나노 방사선 센서 시장 내 2024년 매출의 58%를 점유한 고체 상태 검출기는 CMOS 호환성을 활용해 감지 요소를 혼합 신호 칩에 직접 내장합니다. 이 아키텍처는 전력 예산을 절감하고 기판 레이아웃을 단순화하며, 이는 의료 영상 콘솔 및 위성 페이로드에서 가치 있는 특성입니다. 신틸레이션 유닛은 점유율은 낮지만, 100,000 foton/MeV 이상의 광수율을 제공하는 페로브스카이트 나노크리스탈 기술의 돌파구와 연계된 6.5% CAGR 전망의 혜택을 받습니다. 하이브리드 설계는 이제 고체 상태 판독 장치와 나노크리스탈 신틸레이터를 결합하여 웨이퍼 레벨 공정 경제성을 유지하면서 400 ps 미만의 응답 속도를 달성합니다.

2세대 고체 상태 플랫폼은 설치 공간을 확대하지 않으면서 광자 수집 효율을 3배로 높이는 나노 플라즈모닉 증강층을 채택합니다. 페로브스카이트 코팅 기술이 성숙해짐에 따라 제조사들은 실리콘 포토다이오드 위에 고원자량(high-Z) 신틸레이터를 단일 칩으로 통합하는 실험을 진행 중이며, 이는 내시경 수술용 단일 칩 감마 카메라 개발을 시사합니다. 이러한 진화는 고체 상태 방식과 신틸레이션 방식 간의 범주적 경계가 모호해질 것임을 보여주며, 나노 방사선 센서 산업 전반에 걸쳐 새로운 수익원을 창출할 전망입니다.

실리콘은 2024년 매출의 46%를 차지하며 안정적인 공급과 광범위한 파운드리 지원을 제공하여 주류 애플리케이션의 현재 나노 방사선 센서 시장 규모를 뒷받침하고 있습니다. 생산 학습 곡선은 평균 판매 가격을 예측 가능하게 유지하며, 이는 10년 이상의 제품 주기를 약속하는 자동차 1차 공급업체에게 필수적인 특성입니다. 페로브스카이트 검출기는 연평균 복합 성장률(CAGR) 8.2%를 기록하며, 유연한 기판에 롤투롤 코팅이 가능한 용액 공정 기술의 혜택을 받아 웨어러블 건강 모니터 및 드론 플랫폼 분야의 적용 가능성을 확대하고 있습니다.

실리콘 ASIC과 얇은 페로브스카이트 흡수층을 결합한 복합 스택은 단일 외피 내에서 연 X선 및 저에너지 감마 광자 검출을 가능하게 하여 비파괴 검사를 위한 다중 스펙트럼 이미징 성능을 향상시킵니다. 망간 복합체를 활용한 무연 조성물은 80% 이상의 광발광 양자수율을 달성하여 검출 효율을 저하시키지 않으면서 환경적 개선을 제공합니다. 이러한 하이브리드 스택은 재료 선택이 공급망 제약이 아닌 응용 분야 특성에 따라 결정되는 전환점을 시사합니다.

나노 방사선 센서 시장은 유형(신틸레이션 검출기, 고체 검출기), 소재(실리콘 기반 반도체, 무기 결정(GAGG, LSO, Csi) 등), 응용 분야(자동차, 소비자 가전 등), 기술(간접 신틸레이션-CMOS 등), 검출 방사선 유형, 폼 팩터 및 지역별로 세분화됩니다. 시장 전망은 가치(USD) 기준으로 제공됩니다.

북미는 2024년 시장 점유율 35%로 선두를 유지하며, 93기의 가동 중인 원자로를 대상으로 한 지속적인 국방 조달 및 수십억 달러 규모의 현대화 사업이 이를 뒷받침합니다. 아날로그 디바이스는 CHIPS 법에 따라 매사추세츠와 오리건에서 웨이퍼 생산량을 3배로 확대하여 군용 등급 검출기의 장기적 공급 안정성을 확보하고 있습니다. 써모피셔사이언티픽은 64개 제조 사이트로 구성된 확대된 미국 네트워크를 통해 의료, 산업용 비파괴검사(NDT), 국토안보 프로그램에 대한 국내 공급을 강화하고 있으며, 두 개의 미국 가압수형 원자로에서 AI 기반 모니터링을 통해 예측 분석으로 예정되지 않은 가동 중단 시간을 줄이고 있습니다.

아시아태평양(APAC) 지역은 5.9%의 가장 빠른 연평균 성장률(CAGR)을 보일 것으로 예상되며, 이는 대중 안전 분야 적용을 확대하는 스마트폰 호환 방사선 칩의 중국 내 성공적인 규모 확대에 기반합니다. 일본은 샤프의 초박형 센서 모듈과 JAEA의 실리콘 감마선 검출기(비등수형 원자로 개조에 적합)를 통해 전문성을 유지하고 있습니다. 한국의 NEXTSat-2에 탑재된 LEO-DOS 페이로드는 저지구궤도 선량계용 국산 방사선 내성 설계의 유효성을 입증하며, 동남아시아 신흥 우주 경제권에 수출 가능한 역량을 시사합니다.

유럽은 2050년 이전 단계적 폐쇄 예정인 171GW 원자력 설비의 안전한 해체를 최우선 과제로 삼아 분산형 센서 어레이에 대한 단기 수요 급증을 창출하고 있습니다. 영국의 3천만 파운드 연구 지원금은 자율 로봇 모니터 시제품 개발을 위한 대학-산업 컨소시엄을 조성하는 시발점이 되었다. 독일 자동차 1차 공급업체들은 단일 이벤트 장애(SEU)에 대한 전자장치 인증을 위해 ADAS 제어 장치에 방사선 감지 기능을 통합하는 방안을 모색 중이며, 프랑스 EDF는 60년 이상의 발전소 운영 허가 연장을 위해 나노 센서를 활용한 핵심 플럭스 매핑 기술을 업그레이드하고 있습니다. 핀란드 옐바스퀼라 대학은 중성자, 감마선, 베타선 채널을 통합한 휴대용 다목적 검출기를 개발하여 유럽 전역의 초기 대응자 도구 키트를 지원합니다.

The nano radiation sensors market stood at USD 367.05 billion in 2025 and is forecast to register a 4.17% CAGR, reaching USD 450.19 billion by 2030.

Growth reflects consistent miniaturization across consumer electronics, aerospace, and automotive systems, paired with stringent safety rules in nuclear decommissioning and space exploration. Recent breakthroughs in perovskite semiconductor materials now allow detector footprints small enough for smartphone integration and wearable patches, removing long-standing size and power barriers. Government stimulus ranging from the GBP 30 million package under the UK Nuclear Decommissioning Authority to the USD 105 million CHIPS Act grant for Analog Devices shortens commercialization cycles and accelerates supply expansion. CubeSat proliferation, particularly in university and startup missions, compounds the addressable volume for ultra-light sensors, while parallel demand arises from healthcare dosimetry and automotive safety subsystems. Manufacturing complexity and yield losses remain the most significant constraints; however, firms that resolve material-stability issues while maintaining cost control gain an immediate competitive edge.

Relentless downsizing in consumer electronics and automotive platforms pushes radiation sensor modules toward wafer-level integration. Sharp demonstrated a 25 X 20 X 2.5 mm module drawing only 7.5 mW, making smartphone-based radiation tracking practical. Parallel progress in 5 nm and 3 nm process nodes allows logic and detection circuitry to share a common die, lowering bill-of-materials costs for original-equipment manufacturers. In automobiles, compact sensors now fit inside existing electronic control units, supporting Advanced Driver Assistance Systems without altering cabin design. As IoT architectures spread, distributed nano radiation sensors can be deployed in factories and hospitals at node-level costs that were unattainable five years ago.

Targeted public programs guarantee long-term demand while harmonizing certification. The U.S. Department of Commerce earmarked USD 105 million for Analog Devices to modernize three domestic fabs, explicitly citing commercial and defense radiation detection as priority outputs. The UK Nuclear Decommissioning Authority injected GBP 30 million into sensor R & D to support safe dismantling of legacy reactors. In parallel, the European Commission's Horizon Europe platform directs resources toward sustainable radiation-protection technology. ISO and IEEE working groups now draft unified nano sensor test protocols that cut compliance cycles and enable cross-border procurement.

Sub-10 nm features needed for latest detector architectures experience higher defect rates than mainstream logic chips, depressing first-pass yields below 60% at several foundries. Supply-chain shocks-such as the temporary shutdown of Spruce Pine's quartz mine that feeds high-purity silica into photolithography mask blanks-amplify cost pressures by constricting vital materials. Fab operators must adopt tighter particulate controls and advanced metrology, driving up per-wafer operating expenses in the short run.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solid-state detectors captured 58% of 2024 revenue within the nano radiation sensors market, leveraging CMOS compatibility to embed sensing elements directly onto mixed-signal chips. This architecture trims power budgets and simplifies board layouts, attributes valued in medical imaging consoles and satellite payloads. Scintillation units, though smaller in share, benefit from 6.5% CAGR prospects tied to perovskite nanocrystal breakthroughs delivering light yields above 100,000 photons MeV-1. Hybrid designs now merge solid-state readout with nanocrystal scintillators, achieving sub-400 ps response while retaining wafer-level processing economies.

Second-generation solid-state platforms adopt nano-plasmonic enhancement layers that triple photon-collection efficiency without expanding footprint. As perovskite coatings mature, manufacturers experiment with monolithic integration of high-Z scintillators atop silicon photodiodes, pointing toward single-chip gamma cameras for endoscopic surgery. The evolution indicates that categorical boundaries between solid-state and scintillation approaches will blur, generating new revenue pools throughout the nano radiation sensors industry.

Silicon maintained 46% contribution to 2024 revenue, offering reliable supply and extensive foundry support that underpins the current nano radiation sensors market size for mainstream applications. Production learning curves keep average selling prices predictable, a trait essential for automotive Tier-1 suppliers committing to decade-long product cycles. Perovskite detectors, at 8.2% CAGR, benefit from solution processing that allows roll-to-roll coating of flexible substrates, widening addressable opportunities in wearable health monitors and drone platforms.

Composite stacks merging silicon ASICs with thin perovskite absorber layers allow detection of soft X-ray and low-energy gamma photons in a single envelope, improving multispectral imaging for nondestructive testing. Lead-free compositions featuring manganese complexes reach photoluminescence quantum yields above 80%, providing an environmental upgrade without sacrificing detection efficiency. These hybrid stacks signal an inflection point where material-choice decisions become application-specific rather than supply-chain constrained.

Nano Radiation Sensors Market Segmented by Type (Scintillation Detectors, Solid-State Detectors), Material (Silicon-Based Semiconductors, Inorganic Crystals (GAGG, LSO, Csi) and More), Application (Automotive, Consumer Electronics and More), Technology, Indirect Scintillation-CMOS and More), Detection Radiation Type, Form Factor and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North American leadership, with 35% 2024 share, is anchored by continuous defense procurement and multi-billion-dollar modernization across 93 operating nuclear reactors. Analog Devices is tripling wafer starts in Massachusetts and Oregon under the CHIPS Act, securing long-run availability of military-grade detectors. Thermo Fisher's enlarged US network of 64 manufacturing sites reinforces domestic supply for healthcare, industrial NDT, and homeland-security programs, while AI-augmented monitoring at two US pressurized-water reactors cuts unscheduled outage hours through predictive analytics.

APAC shows the fastest 5.9% CAGR forecast, underpinned by China's successful scaling of smartphone-compatible radiation chips, which broaden public-safety adoption. Japan maintains domain expertise via Sharp's ultra-thin sensor module and JAEA's silicon gamma-ray detectors qualified for boiling-water reactor retrofits. South Korea's LEO-DOS payload on NEXTSat-2 validates homegrown radiation-hard designs for low-Earth-orbit dosimetry, signalling export-ready competence for emerging space economies in Southeast Asia.

Europe prioritizes safe dismantling of 171 GW of nuclear capacity set for phase-out before 2050, creating near-term demand peaks for distributed sensor arrays. The UK's GBP 30 million research grant seeds university-industry consortia to prototype autonomous robotic monitors. Germany's automotive Tier-1 suppliers explore integrating radiation sensing into ADAS control units to certify electronics against single-event upsets, while France's EDF upgrades core flux mapping with nano sensors to extend plant licenses beyond 60 years. Finland's University of Jyvaskyla produced a handheld multi-purpose detector that merges neutron, gamma, and beta channels, supporting first-responder toolkits across the continent.