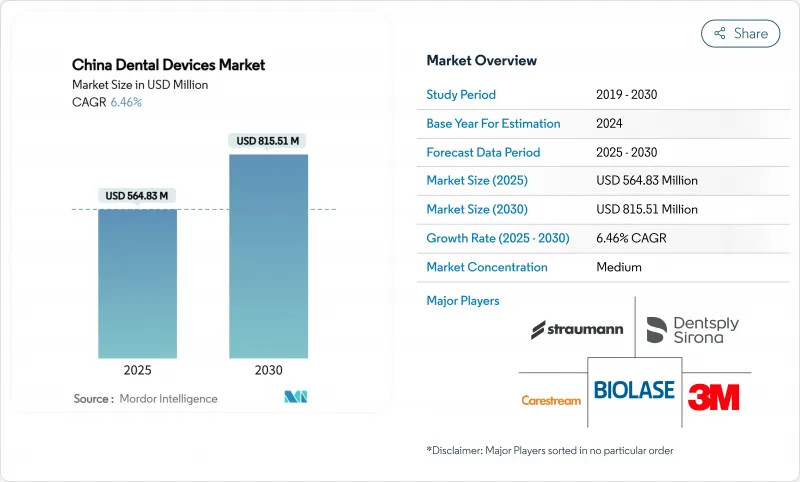

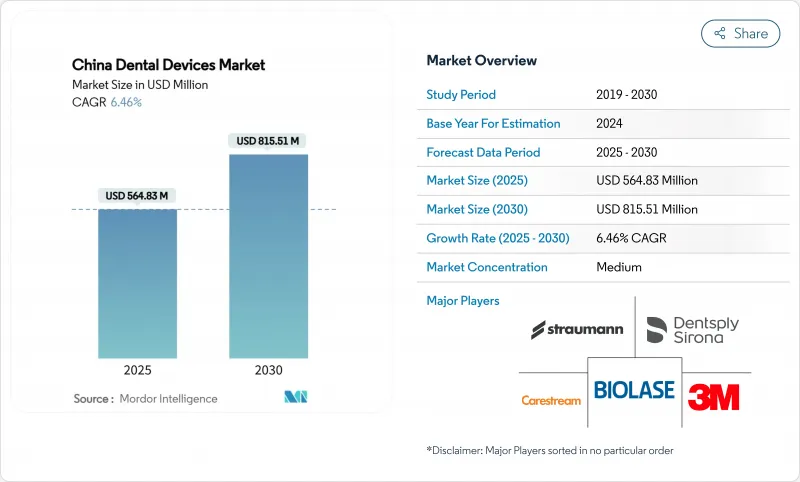

중국의 치과용 장비 시장 규모는 2024년에 5억 6,483만 달러로 평가되었고, 2030년에는 8억 1,551만 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 6.46%를 나타낼 전망입니다.

강력한 정책 지원, 급성장하는 중산층, 디지털 워크플로우의 확산이 해당 분야를 고부가가치 시술로 이끌고 있습니다. 임플란트의 대량 구매, ‘건강중국 2030’ 예방 목표, 치과 서비스 조직(DSO)의 급부상이 가격 책정, 환자 접근성, 구매 관행을 재편하고 있습니다. 국내 제조사들은 이러한 변화를 활용해 2·3선 도시 시장 점유율을 확대하고 있으며, 글로벌 브랜드들은 기술 리더십을 통해 프리미엄 틈새 시장을 방어하고 있습니다. 첨단 영상 장비와 진료실 내 CAD/CAM 장비는 도시 중심지로 빠르게 확산되고 있으며, 소셜미디어 미학에 영향을 받은 밀레니얼 세대 환자들에게 투명 교정 치료가 기본적인 교정 치료 옵션으로 자리 잡고 있습니다.

베이징, 상하이, 광저우, 선전의 클리닉들은 아날로그 인상에서 완전한 디지털 구강 스캐닝 및 CAD/CAM 제작으로 도약하며 치료 계획 시간을 60% 단축하고 케이스 수락률을 32% 높였습니다. 치과용 장비의 클라우드 통합으로 의료진은 실험실과 실시간으로 보철물을 공동 설계할 수 있어 처리 시간이 며칠에서 몇 시간으로 단축됩니다. 경쟁 강도는 소프트웨어 생태계로 이동하며, 스캐너, 밀링 장비, AI 설계 모듈을 단일 구독으로 묶어 제공할 수 있는 업체에 유리하게 작용합니다. 이들 도시의 초기 기술 도입자들은 전국적인 의뢰 패턴에 영향을 미쳐 2선 시장으로의 디지털 도구 확산을 가속화하고 중국 치과 기기 시장의 장기적 수요를 뒷받침합니다.

최초의 치과 임플란트 전국 입찰을 통해 병원 평균 가격이 55% 하락했으며, 225만 세트를 대상으로 연간 약 40억 위안의 환자 부담금 절감 효과가 예상됩니다. 과거 자비 부담 엘리트 계층의 전유물이었던 임플란트가 이제 더 넓은 중산층에게 접근 가능해져 2030년까지 잠재적 수요층이 30% 확대될 전망입니다. 입찰 물량을 확보한 병원은 중앙 정부 보조금을 지원받으며, 확장 가능한 현지 생산 능력을 보유한 제조사는 시장 점유율을 확보합니다. 지방 시범 사업이 영구적 보험 적용 체계로 통합되면서 중국 치과 기기 시장은 구조적 변화를 겪고 있습니다. 고가 제품의 단위 물량이 급증하고, 프리미엄 시스템은 차별화된 표면 기술을 통해 틈새 시장 지위를 방어합니다.

임플란트 입찰에 이어 병원 컨소시엄이 CBCT 및 체어사이드 밀링 장비로 공동 구매를 확대하면서 평균 판매 가격이 최대 35%까지 하락했습니다. 제조사들은 계층화된 제품 포트폴리오로 대응하며 비핵심 기능을 제거해 목표 가격대를 달성하고 있습니다. 이 정책은 비용 구조가 효율적인 국내 생산자에게 유리하게 작용하여 다국적 기업의 프리미엄 시장 점유율을 잠식하고 중국 치과 기기 시장의 전반적인 매출 성장세를 완화시키고 있습니다.

2024년 치과 소모품 부문은 대량 사용되는 임플란트, 크라운, 생체재료에 힘입어 전체 매출의 46.51%를 차지했습니다. 국가 차원의 임플란트 입찰 제도는 환자 본인 부담금을 대폭 낮춰 군·구 병원에서의 나사 고정식 크라운 보급률을 높였습니다. 소모품 부문은 2030년까지 연평균 3.23% 성장률(CAGR)을 유지하며 중국 치과 기기 시장 규모에서 가장 큰 비중을 차지할 전망입니다. 진단 장비는 규모는 작지만, AI 도구가 진료 효율성을 높이고 ‘건강중국 2030’ 목표에 부합하는 예방적 개입을 가능케 함에 따라 가장 빠른 비율 성장이 예상됩니다. AI 기반 충치 탐지 소프트웨어는 중국 진료소에서 93.40%의 정확도를 보여 대규모 도입 준비가 완료되었음을 입증했습니다.

클라우드 연결 구강 스캐너는 인상 작업 흐름을 단축하고 진료실 밀링 장비와 연동되어 하이브리드 세라믹 블록의 추가 판매를 촉진합니다. 치료 장비, 특히 CAD/CAM 시스템은 당일 진료로 환자 만족도를 높이는 고수요 진료소에서 초기 수요를 확보하고 있습니다. 에어 폴리셔 및 수술용 모터를 포함한 '기타 기기'는 전국 개인 치과 진료소 설치 기반이 12만 개를 넘어섬에 따라 꾸준히 성장 중입니다. 이러한 부문 간 상호작용은 생태계 유대감을 강화하여 중국 치과 기기 시장 내 다중 수익 흐름을 공고히 합니다.

The China dental devices market size stands at USD564.83 million in 2024 and is projected to reach USD815.51 million by 2030, expanding at a 6.46% CAGR during 2025-2030 .

Robust policy support, a fast-growing middle-class, and the rising penetration of digital workflows are steering the sector toward higher-value procedures. Volume-based procurement of implants, the Healthy China 2030 preventive targets, and the burgeoning power of dental service organizations (DSOs) are reshaping pricing, patient access, and procurement norms. Domestic manufacturers are capitalising on these shifts to gain share in tier-2 and tier-3 cities, while global brands defend premium niches through technology leadership. Advanced imaging and chairside CAD/CAM equipment are diffusing rapidly across urban hubs, and clear-aligner therapy is becoming a default orthodontic choice for millennial patients driven by social-media aesthetics.

Clinics in Beijing, Shanghai, Guangzhou, and Shenzhen are leapfrogging from analogue impressions to fully digital intraoral scanning and CAD/CAM fabrication, cutting treatment-planning time by 60% and lifting case-acceptance rates by 32%. The cloud integration of chairside devices lets practitioners co-design restorations with labs in real time, compressing turnaround from days to hours. Competitive intensity is shifting toward software ecosystems, tilting advantage to vendors able to bundle scanners, mills, and AI design modules as a single subscription. Early technology adopters in these cities influence referral patterns nationwide, accelerating the diffusion of digital tools into tier-2 markets and undergirding long-run demand across the China dental devices market.

The first national tender for dental implants reduced average hospital prices by 55%, targeting 2.25 million sets and saving patients an estimated CNY4 billion annually. Implants-once confined to self-pay elites-are now affordable to a broader middle-income cohort, enlarging the addressable pool by 30% through 2030. Hospitals able to guarantee tender volumes benefit from central subsidies, while manufacturers with scalable local capacity win share. As provincial pilots converge into a permanent reimbursement schedule, the China dental devices market experiences a structural shift: value items rise sharply in unit volume, premium systems defend niche positioning through differentiated surface technologies.

Following the implant tender, hospital consortia are extending pooled procurement to CBCT and chairside milling units, compressing average selling prices by up to 35%. Makers respond with tiered portfolios, stripping non-essential features to hit target price points. The policy favours domestic producers with leaner cost structures, eroding premium share for multinationals and moderating overall revenue expansion within the China dental devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Dental consumables commanded 46.51% revenue in 2024, anchored by high-volume implants, crowns, and biomaterials. The national implant tender slashed patient out-of-pocket costs, widening penetration of screw-retained crowns across county hospitals. Consumables are projected to expand at a 3.23% CAGR, sustaining the largest slice of the China dental devices market size through 2030. Diagnostic equipment, though smaller in value, is set for the fastest proportional climb as AI tools elevate chair productivity and enable preventive interventions aligned with Healthy China 2030 targets. AI-guided caries-detection software demonstrated 93.40% accuracy in Chinese clinics, illustrating readiness for widescale rollout.

Cloud-connected intraoral scanners shorten impression workflows and dovetail with chairside mills, encouraging upsell of hybrid ceramic blocks. Therapeutic equipment, notably CAD/CAM systems, finds early traction in high-footfall practices where same-day dentistry boosts patient satisfaction. 'Other devices', including air-polishers and surgical motors, grow steadily as the installed base of private clinics rises above 120,000 nationwide. The interplay among these segments strengthens ecosystem stickiness, reinforcing multi-line revenue flows within the China dental devices market.

The China Dental Devices Market Report is Segmented by Product (Diagnostics Equipment, Therapeutic Equipment, Dental Consumables, Other Dental Devices), Treatment (Orthodontic, Endodontic, Peridontic, Prosthodontic), End User (Dental Hospitals, Dental Clinics, Academic & Research Institutes). The Market Forecasts are Provided in Terms of Value (USD).